Chapter 16

Fiscal Policy and the Government Budget

◼ Chapter Outline, Overview, and Teaching Tips

Chapter Outline

The Government Budget

Government Spending

Revenue

Budget Deficits and Surpluses

Government Budget Constraint

Size of the Government Debt

Growth of U.S. Government Debt Over Time

Policy and Practice: The Entitlements Debate: Social Security and Medicare/Medicaid

International Comparison: The Size of Government Debt

Sovereign Debt Crises

Policy and Practice: The European Sovereign Debt Crisis

Fiscal Policy and the Economy in the Long Run

Why High Government Debt Is Not a Burden

Why Government Debt Is a Burden

Policy and Practice: Tax Smoothing

Fiscal Policy and the Economy in the Short Run

Aggregate Demand and Fiscal Policy

Expenditure and Tax Multipliers

Policy and Practice: The 2009 Debate Over Tax-Based Versus Spending-Based Fiscal Stimulus

Chapter 16 Fiscal Policy and the Government Budget 175

Table 16.1 in class, which shows the different spending and revenue items in government budgets in the

United States. An important point to make is that the federal government is only part of the story because

spending by state and local governments is almost as large as federal spending. This table can also be used

to show how budget deficits or surpluses are measured. (An appendix to this chapter on the book’s Website

shows that there are actually many different measures of government budget deficits or surpluses, showing

that interpretation of these numbers is not completely straightforward.) With this understanding of budget

deficits, the chapter then discusses how government budget deficits cause government debt to increase

over time and compares the size of government debt relative to the economy across countries. The Policy

and Practice case, “The Entitlements Debate: Social Security and Medicare/Medicaid,” can stimulate a

good class discussion on the looming fiscal crisis that students will face during their lifetimes.

The chapter then provides analysis of the impact of fiscal policy on the economy in the long run and

discusses the debate over whether government debt is a burden on future generations. The Policy and

Practice case on tax smoothing raises an interesting policy issue for students, that it does not always make

sense to balance the budget as some politicians seem to suggest because it is worth running large budget

deficits temporarily in order to smooth taxes when there are temporary surges in government spending as

during war time.

The chapter next describes the dynamic of sovereign debt crises, which have become a much bigger

problem in the aftermath of the global financial crisis that has weakened government finances throughout

the world. The Policy and Practice case on the European sovereign debt crisis is particularly worth

covering in class because, not only has it been much in the news lately, it illustrates that the United States

may be in a dangerous environment where it too could experience a sovereign debt crisis. The next topic is

the impact of fiscal policy on the economy in the short run. Here the chapter uses the AD/AS model to go

176 Mishkin • Macroeconomics: Policy and Practice, Second Edition

1. The four main components of government spending are expenditures to purchase goods and services,

which can be subdivided into government investment spending on capital goods such as highways

and schools and government consumption spending on such things as operating national parks and

2. A government budget deficit means that government spending over some time period is greater than

the revenues government has collected over that period. According to government’s budget constraint,

3. Heavy government borrowing (deficit spending) during World War II caused the debt-to-GDP ratio

to increase sharply. Rapid real GDP growth and inflation both contributed to the ratio falling just as

sharply in the post-war era, until the large income tax cuts of the Reagan administration in the 1980s

reversed this trend. Strong economic growth and an effort to balance the budget in the 1990s caused

Chapter 16 Fiscal Policy and the Government Budget 177

4. Government debt will not burden the future generations that must repay it if it is used to finance

investments in government and human capital that increase their productivity (and income) and if those

repaying the debt also hold the government bonds (in which case they are simply paying themselves). A

number of counterarguments, however, support a less rosy assessment of the burden of the debt: Budget

deficits reduce national saving and crowd out private investment; most government spending is for

5. Government can increase the quantity of aggregate output demanded by increasing government

spending or by cutting taxes. Both changes increase planned spending at any given rate of inflation

and shift the aggregate demand curve to the right. Both also produce a change in equilibrium output

that exceeds their own size. For example, a $500 billion increase in government spending may lead to

6. An analysis based on aggregate demand generally concludes that a tax cut increases aggregate demand,

shifts the aggregate demand curve to the right, and increases both aggregate output and inflation in

the short run but only inflation in the long run. Supply-side analysis argues that tax cuts that are

permanent also have significant positive effects on aggregate supply (and conversely, permanent tax

7. Not necessarily. Efforts to reduce the budget deficit by reducing government spending or raising taxes

shift the aggregate demand curve to the left but can also lower expected future taxes and motivate

8. Fiscal multipliers are higher when the zero lower bound occurs because expansionary fiscal policy

not only adds to aggregate demand directly but also raises inflation. The higher inflation rate at the

zero lower bound then results in a decline in the real interest rate, which leads to a further increase in

178 Mishkin • Macroeconomics: Policy and Practice, Second Edition

9. Whether budget deficits lead to inflation in the long run depends on how they are financed. As long

as they are financed by issuing new bonds, they will not be inflationary if the monetary authorities

focus on price stability and can employ contractionary policies to offset the impacts of the budget

10. The traditional view, based largely on Keynesian economics, holds that tax cuts increase aggregate

demand, result in higher inflation, and reduce national saving, which leads to an increased burden on

future generations resulting from lower private investment spending or lower net exports and greater

indebtedness to foreigners. The Ricardian equivalence view holds that tax cuts have no effect on

spending and national saving because consumers are forward looking, so when taxes are cut, they

save their increase in disposable income because they recognize that today’s tax cut means higher

taxes tomorrow. Because private saving increases when taxes are cut, aggregate demand does not

2. a. A decrease in the number of employed people results (holding Social Security tax rates constant)

in a decrease in contributions for social insurance. This decreases tax revenue and, therefore,

3. There seems to be no definite consensus about the definition of the government deficit. This example

illustrates many possible approaches to labeling expenditures and receipts. If Social Security contributions

were considered a loan to the government, to be repaid later (plus interest) in the form of benefits,

this would have no effect on the government deficit. However, according to the current definition, an

Chapter 16 Fiscal Policy and the Government Budget 179

4. The prevalence of chronic diseases like diabetes increases the cost of health care in the future. Even if

the dependency ratio is considered to remain constant, this will mean either fewer benefits for individuals

in need of health care, or an increase in Social Security taxes, for the deficit to remain unchanged.

Chances are that treatment for many diseases derived from increasing obesity rates will be in short

5. a. This particular type of spending should be considered government investment because it is aimed

at increasing productivity in the future.

b. If this type of investment is successful in increasing workers’ productivity, we should expect an

6. a. An increase in Treasury note interest rates represents an increase in net interest payments for the

U.S. government and therefore increases the deficit.

b. Although it is not plausible to happen in the near future, there could be some trouble ahead for

the U.S. government to sell its debt. This potential decrease in the demand for U.S. Treasuries

should be considered a wake-up call. Investors are taking into consideration the size and

7. a. According to the estimates of the expenditure and tax multipliers, one should recommend

conducting expansionary fiscal policy by increasing government expenditures, as this will have a

bigger effect on aggregate demand. In this case, government expenditures should be wisely directed

to productive uses, with the potential to improve infrastructure and increase productivity in the

long run.

180 Mishkin • Macroeconomics: Policy and Practice, Second Edition

8. a. The prospect of a government committed to long-run fiscal discipline increases both types of

autonomous expenditure. Usually a commitment to long-run fiscal discipline is one of many

characteristics of a government committed to long -run economic growth. It is quite possible

that such an administration will promote free trade, secure property rights, and encourage

research and development. This spurs consumption and investment spending and adds to

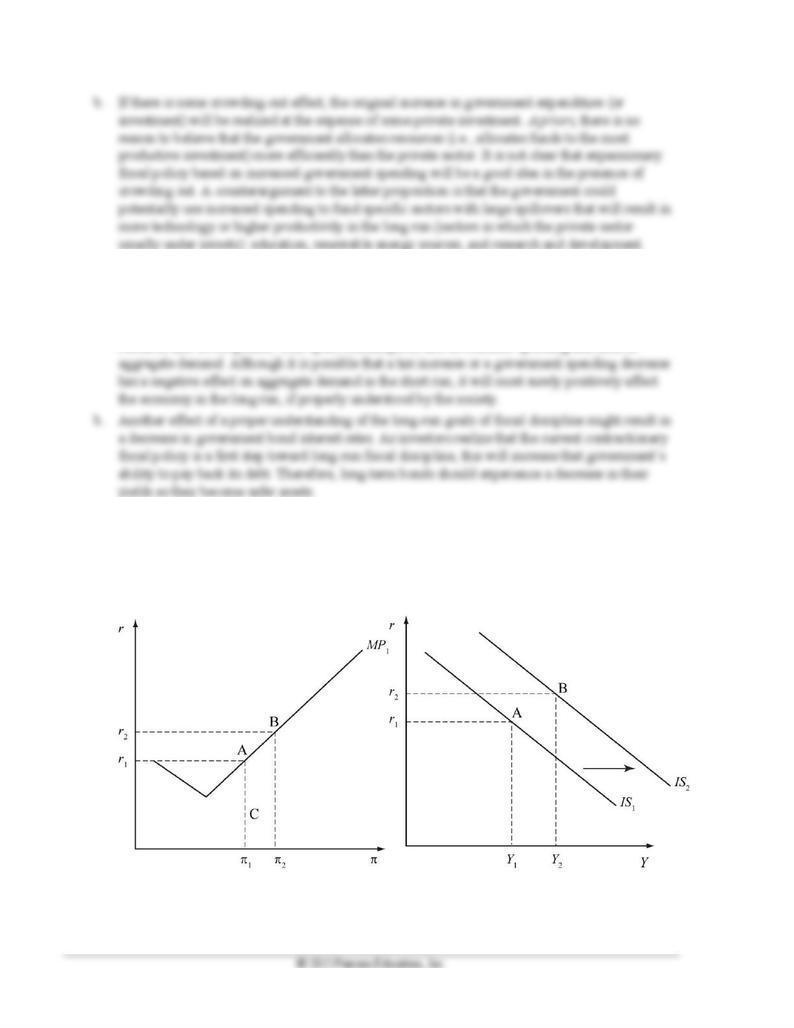

9. a. A decrease in taxes shifts the IS and the AD curves to the right, resulting in an increase in output

and inflation in the short run. As inflation increases, the real interest rate increases along MP1

from point A to point B. With the increase in inflation in the short run, the real interest rate rises

along the MP curve, which crowds out some of the impact of the tax decrease. In the short run,

the economy will be at point B.

182 Mishkin • Macroeconomics: Policy and Practice, Second Edition

10. If the inflation rate is very high, the tax size (i.e., the inflation rate) will be high, but the tax base (i.e.,

the real money supply) will be really low and decreasing, as the price level keeps increasing. As a

result, the revenue from seignorage will eventually decrease, as happens with any tax when the tax

11. a. Even if individuals are forward looking and decide to save in advance to pay higher future taxes,

an underdeveloped financial system might not allow them to do so. One of the characteristics of

an underdeveloped financial system is its reduced supply of financial instruments. Usually

developing countries do not have efficient bond or stock markets that allow individuals to buy

assets to postpone current consumption. If that is the case, they will either consume more today

or find another way of postponing consumption (outside the financial system). An increase in

current consumption will decrease national saving.

Chapter 16 Fiscal Policy and the Government Budget 183

was 64.3 percent. The last time it reached a peak was in 1995:Q2, when it was 65.1 percent; this

is considerably lower than the current value of 101.6 percent.

b. Over the last year, debt to GDP has increased 101.6 percent – 97.3 percent = 4.3 percentage

points; over the last five years, it has increased 101.6 percent – 64.3 percent = 37.3 percentage

points.

c. From 2012:Q1 to 2013:Q1, GDP has increased by 3.1 percent; from 2008:Q1 to 2013:Q1, GDP

2. a. In 2013:Q1, foreign and international investors held 34.3 percent of all U.S. government debt.

This is a relatively high number and, as seen below, is in fact an all-time high considering the

steady increase over time in foreign debt holdings.

b. See graph below. The amount of U.S. debt held by foreigners has steadily increased since the

184 Mishkin • Macroeconomics: Policy and Practice, Second Edition

3. a. See the figure on the next page. Not surprisingly, from 1980 to 2012, there appears to be a very

strong relationship between deficits and the change in bond holdings by the public, as the fitted

line is very steep (and has a high R2 if using a regression line).

b. For the change in holdings by the Federal Reserve, there appears to be a positive relationship, but

this is much less obvious (and using a fitted regression line indicates a much smaller relationship,

with less predictive power).

c. There appears to be some amount of debt monetization in the scatterplot data: in general, as the

deficits get larger, the change in bond holdings by the Fed gets larger, indicating the central bank

is facilitating higher deficits. However, this appears to be driven by the large outlier deficits in

Chapter 16 Fiscal Policy and the Government Budget 185

186 Mishkin • Macroeconomics: Policy and Practice, Second Edition

1. a. and b.

Primary Deficit

Current Deficit

220), country A’s primary deficit is zero. Country B is not able to pay for its current purchases of

3. According to the current deficit measure, country A is increasing its holdings of net assets (i.e., negative

current deficit). Although country A is running a total government deficit, 25 percent of its purchases

4. The inflation-adjusted deficit for country A is: $100 billion = 0 (primary deficit) + 0.02 5,000.

Accounting for the real value of net interest payments, the government of country A has a $100

billion inflation-adjusted deficit. The inflation-adjusted deficit for country B is $600 billion = 500

(primary deficit) + 0.02 5,000. As with country A, a positive real interest rate increases the primary

deficit (as countries hold a positive stock of outstanding debt).

◼ Data Sources, Related Articles, and Discussion Questions

A. For Information About Policy and Practice: The Entitlements Debate: Social

Security and Medicare/Medicaid

Data Source

Congressional Budget Office: Social Security Disability Insurance: Participation Trends and Their Fiscal

Implications”: http://www.cbo.gov/doc.cfm?index=11673. Here you can access the entire report made by

the Congressional Budget Office about the impact of social security disability insurance.

Related Article

U.S. Census Bureau, “Aging Boomers Will Increase Dependency Ratio, Census Bureau Projects”:

http://www.census.gov/newsroom/releases/archives/aging_population/cb10-72.html. This article focuses

on the evolution of the dependency ratio according to recent trends in the U.S. demographic characteristics.

Chapter 16 Fiscal Policy and the Government Budget 187

Discussion Question

Considering that the “baby boom” phenomenon also happened in Europe, how do you think the burden of

social security programs will affect the government deficits of European countries in the future?

188 Mishkin • Macroeconomics: Policy and Practice, Second Edition

Chapter 16 Fiscal Policy and the Government Budget 189

190 Mishkin • Macroeconomics: Policy and Practice, Second Edition