Chapter 13

Macroeconomic Policy and Aggregate

Demand and Supply Analysis

◼ Chapter Outline, Overview, and Teaching Tips

Chapter Outline

The Objectives of Macroeconomic Policy

Stabilizing Economic Activity

Stabilizing Inflation: Price Stability

Establishing Hierarchical Versus Dual Mandates

The Relationship Between Stabilizing Inflation and Stabilizing Economic Activity

Monetary Policy and the Equilibrium Real Interest Rate

Policy and Practice: The Federal Reserve’s Use of the Equilibrium Real Interest Rate, r*

Response to an Aggregate Demand Shock

Response to a Permanent Supply Shock

Response to a Temporary Supply Shock

The Bottom Line: The Relationship Between Stabilizing Inflation and Stabilizing Economic Activity

How Actively Should Policy Makers Try to Stabilize Economic Activity?

Lags and Policy Implementation

Policy and Practice: The Activist/Nonactivist Debate Over the Obama Fiscal Stimulus Package

The Taylor Rule

The Taylor Rule Equation

The Taylor Rule Versus the Monetary Policy Curve

The Taylor Rule in Practice

Policy and Practice: The Fed’s Use of the Taylor Rule

Inflation: Always and Everywhere a Monetary Phenomenon

Causes of Inflationary Monetary Policy

High Employment Targets and Inflation

Application: The Great Inflation

Monetary Policy at the Zero Lower Bound

Deriving the Aggregate Demand Curve with the Zero Lower Bound

The Disappearance of the Self-Correcting Mechanism at the Zero Lower Bound

Chapter 13 Macroeconomic Policy and Aggregate Demand and Supply Analysis 137

Application: Nonconventional Monetary Policy and Quantitative Easing

Liquidity Provision

Asset Purchases

Quantitative Easing Versus Credit Easing

Management of Expectations

Policy and Practice: Abenomics and the Shift in Japanese Monetary Policy in 2013

Chapter Overview and Teaching Tips

Chapter 13 shifts the perspective by bringing a new set of actors into the AD/AS framework: policy

makers. We look at how they react to shocks to the economy in order to stabilize both inflation and economic

activity. One unique feature of the dynamic AD/AS framework in this book is that it can address policy

138 Mishkin • Macroeconomics: Policy and Practice, Second Edition

1. Stabilizing economic activity and price stability are the two primary objectives of macroeconomic

stabilization policy. Stabilizing economic activity requires keeping unemployment at the natural rate

2. Policy makers should not strive to achieve zero rates of unemployment and inflation. Even at full

employment, unemployment is not zero because of the existence of frictional and structural

unemployment. Frictional unemployment is beneficial to the economy as it arises from the search

3. A hierarchical mandate gives top priority to the objective of price stability. Under this mandate,

policy makers may pursue the goal of stabilizing economic activity only if it does not compromise

4. The equilibrium real interest rate is the real interest rate that keeps the quantity of aggregate output

5. Stabilization policy is conducted more frequently using monetary policy rather than fiscal policy

Chapter 13 Macroeconomic Policy and Aggregate Demand and Supply Analysis 139

6. The divine coincidence exists when policies that are appropriate to achieve price stability also

stabilize economic activity. When it prevails, policy makers have easier jobs because there is no

tradeoff between policy objectives and they do not have to choose between them. They can, in other

words, have their cake and eat it, too. The divine coincidence prevails when the economy is beset

with aggregate demand shocks or permanent supply shocks but not when it experiences temporary

supply shocks. When faced with either of the first two shocks, policy makers can stabilize both

inflation and economic activity by enacting policies to shift the economy’s aggregate demand curve

and return to long-run equilibrium at potential output. In the case of a temporary supply shock,

however, policies that shift the aggregate demand curve to achieve price stability will move the

economy further away from potential output and those aimed at stabilizing economic activity at

potential output will cause the inflation rate to change.

How Actively Should Policy Makers Try to Stabilize Economic Activity?

7. Activists see the process of price and wage adjustments that move the economy to long-run

equilibrium as working very slowly. They argue that instead of waiting for these slow adjustments to

move the economy to full employment and potential output, government policy makers instead

8. Activists argue that wages are inflexible and, in particular, that they are not likely to fall as would be

needed for the self-correcting mechanism to adjust to long-run equilibrium if the economy suffers

9. The data lag is the time it takes to collect and process the quarterly, monthly, and other data that tell

policy makers how well or poorly the economy is performing. The recognition lag is the time

policymakers may wait for additional data to come in to be more confident of their interpretations of

economic conditions and trends. The legislative lag is the time it takes to decide on a particular

policy. This generally is not long for monetary policy makers but can be quite long for fiscal policy

10. The Taylor rule advises the Fed to raise the real federal funds rate target when the inflation gap or the

output gap rises, and to lower this target rate when those gaps shrink. Inasmuch as it recommends

raising the real interest rate in response to an increase in inflation, it relates directly to the upward

140 Mishkin • Macroeconomics: Policy and Practice, Second Edition

11. There are a number of reasons why this would not be a good idea. There is no guarantee that the

Taylor rule coefficients are stable across time and no one, policy makers included, knows the size of

inflation and output gaps at any given time. Even if policy makers did have accurate information

about the current size of these gaps, relying solely on the Taylor rule would force them to disregard

12. Monetary policy makers can target any inflation rate they want to simply by implementing autonomous

monetary policy easing (to target a higher inflation rate) or tightening (to target a lower one). However,

13. Cost-push and demand-pull inflation result when policy makers in pursuit of high targets for output

and employment (and hence low targets for the unemployment rate) implement policies that raise

aggregate demand when their targets are not met. The two types of inflation both arise from events

that move the economy away from long-run equilibrium, but their initiating causes differ. Cost-push

inflation starts with temporary negative supply shocks or wage increases in excess of productivity

growth. These shift the short-run aggregate supply curve up and to the left and cause output and

employment to fall. Policy makers respond by increasing aggregate demand, which raises output and

employment but also increases inflation. Following this accommodating policy, workers now have an

incentive to push for further excessive wage increases because they have obtained higher wages but

14. When the zero lower bound is hit, a lower inflation rate leads to a higher real interest rate because the

nominal interest rate is fixed at zero, and this higher real interest rate than causes planned expenditure

Chapter 13 Macroeconomic Policy and Aggregate Demand and Supply Analysis 141

15. A negative output gap leads to a fall in the short-run aggregate supply curve, which lowers inflation,

16. All unconventional policies work by lowering the interest rate for investments and so stimulate

investment spending and shift the aggregate demand curve to the right. Liquidity provision helps to

heal impaired financial markets, thereby lowering financial frictions and, hence, the real interest rate

for investments. Asset purchases of private securities raise the price of these securities, thereby

1. a. According to Section 8 of the Reserve Bank of New Zealand Act of 1989, the Central Bank of

New Zealand has a clear hierarchical mandate to achieve low and stable inflation. The idea

behind such a mandate is that stabilizing prices will create the proper conditions for economic

2. a. According to aggregate demand and supply analysis, the decrease in government expenditures

results in a shift to the left in the aggregate demand curve, as aggregate expenditure decreases at

every inflation rate. As a result, the new intersection point with the short-run aggregate supply

curve determines a lower inflation rate and output level than before. At this point, output is below

3. According to aggregate supply and demand analysis, a less efficient economy will end up in a new

long-run equilibrium at a lower level of output. Depending on the monetary policy response, the

inflation rate might be higher than before the implementation of reforms that made the economy less

efficient or might remain unchanged. In any event, output is lower in the long run. This is why the

142 Mishkin • Macroeconomics: Policy and Practice, Second Edition

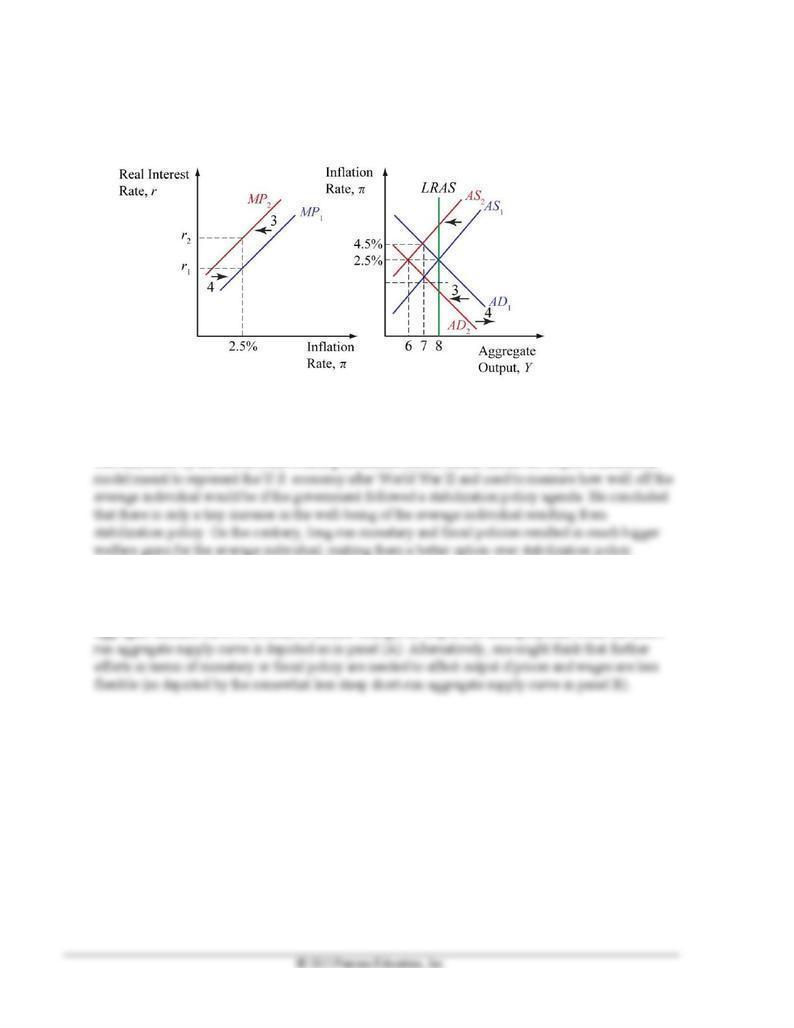

4. a. Changes described by data suggest that policy makers decided to stabilize inflation in the short

run, with the corresponding decrease in output, during period 3.

b. Labeled arrows in the graph refer to the table time periods.

How Actively Should Policy Makers Try to Stabilize Economic Activity?

5. Evidence that shows that the welfare gains from stabilizing output and unemployment are relatively

small, which supports the nonactivist case. This is actually a major topic in macroeconomics, which

was addressed by the Nobel Prize-winning economist Robert Lucas. Lucas developed a theoretical

6. In panel (A) the short-run aggregate supply curve has a steeper slope, meaning that wages and prices

in general are more flexible (i.e., changes in output result in larger changes in the inflation rate). This

situation constitutes a stronger argument in favor of nonactivist policy because changes in the

aggregate demand curve will result in smaller changes in output and unemployment when the short-

Chapter 13 Macroeconomic Policy and Aggregate Demand and Supply Analysis 143

7.

a.

The decline in potential output shifts the LRAS

curve to the left. The lower potential output

increases the output gap, prompting an

autonomous tightening of policy and a shift of

the MP curve to MP2. In the short-run, the

economy ends up at point B. As a result of the

self-correcting mechanism, the AS curve shifts

up, resulting in higher inflation and raising the

real interest rate along MP2. Eventually the

economy reaches the new long-run equilibrium at

point C, at a permanently higher level of

144 Mishkin • Macroeconomics: Policy and Practice, Second Edition

Chapter 13 Macroeconomic Policy and Aggregate Demand and Supply Analysis 145

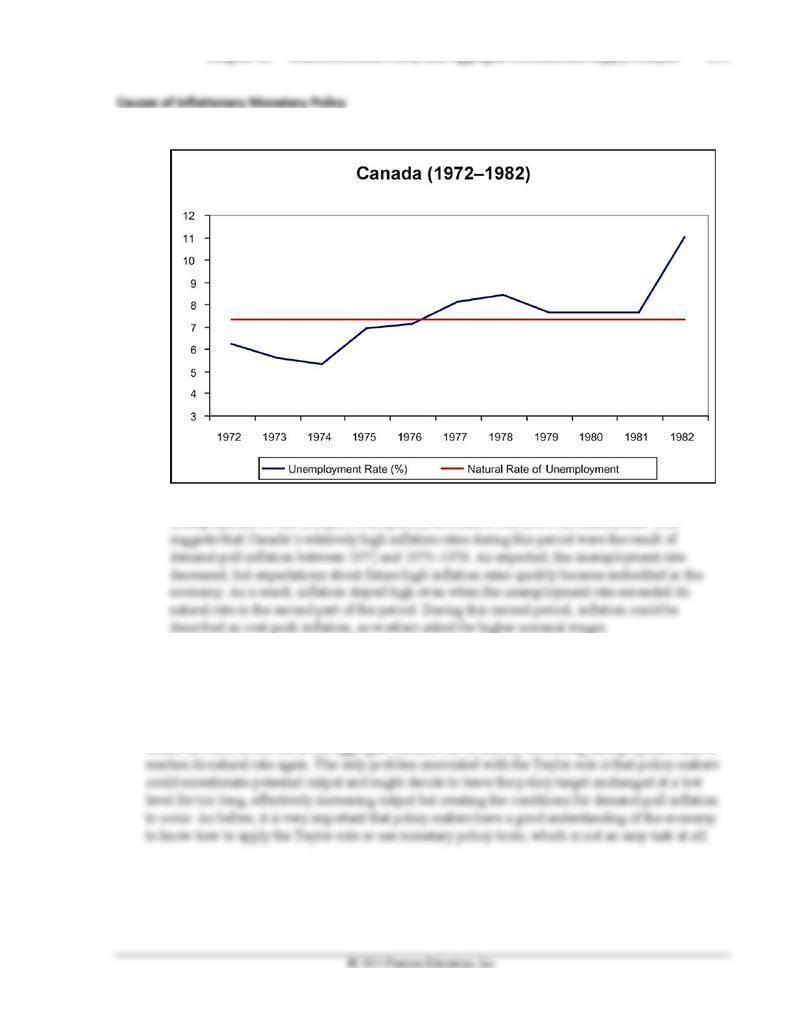

8. a.

b. According to the graph, Canada’s unemployment rate was below the estimated natural rate of

unemployment for the first part of the period, and then it was above the natural rate. This

9. The Taylor rule suggests that the policy rate target should be increased when the output gap is

positive. This rule is perfectly consistent with avoiding demand-pull inflation. The natural rate of

unemployment is the unemployment rate at which output is at its potential level. A positive output

gap means that the economy is producing more output, a situation in which unemployment is below

its natural rate. Therefore, increasing interest rates at every inflation rate (shifting the MP curve up)

results in a shift to the left in the aggregate demand curve, thereby increasing unemployment until it

146 Mishkin • Macroeconomics: Policy and Practice, Second Edition

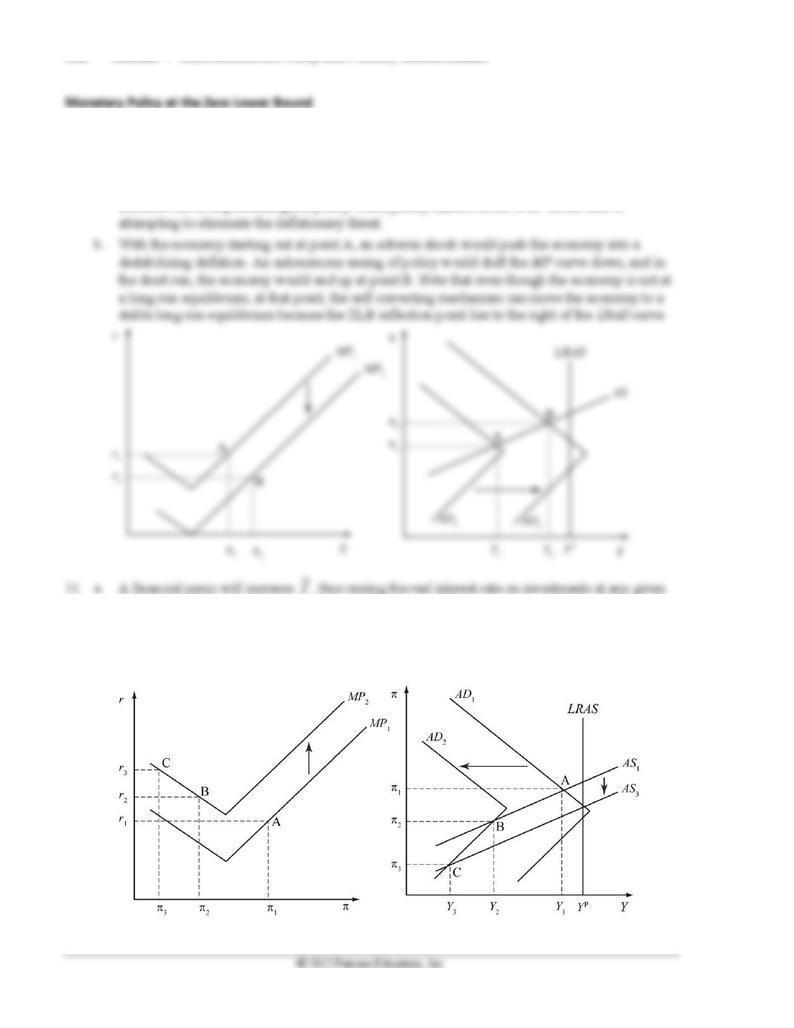

10. a. Policy makers were worried that a shock could push the economy into a deflationary spiral, in

which the short-term nominal policy rate would be bound at the zero lower bound. At that point,

conventional monetary policy would be ineffective. Policy makers viewed the risk of economic

damage in the event of a deflationary spiral to be significant enough to overcome any potential

inflation risk in implementing the policy. Thus, policy makers chose to err on the side of

11. a. A financial panic will increase

, thus raising the real interest rate on investments at any given

inflation rate. A sufficiently large panic will push the economy to point B, where the self-

correcting mechanism will lower inflation, and real rates will rise because the economy is beyond

the ZLB. This results in a deflationary spiral in which the economy will move toward (and past) a

point such as point C.

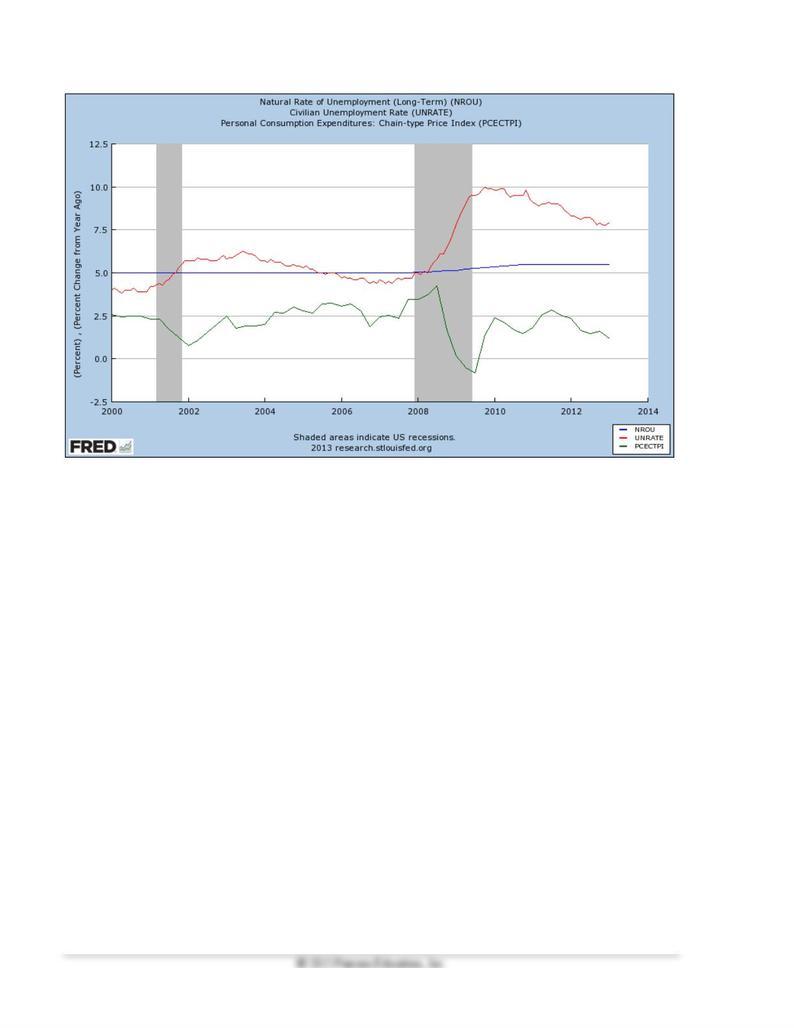

1. a. From 2012:Q2: 2013:Q1, the average inflation gap was –0.5 percent.

b. From 2012:Q2: 2013:Q1, the average output gap was –5.7 percent.

c. From July 2012 to June 2013, the average unemployment gap was 2.2 percent.

(2.5 percent), and the unemployment rate rises and remains above the estimated natural rate during

this time. For a brief time from the middle of 2007 to the middle of 2008, the economy appears to be

hit by a cost-push inflation episode because the inflation rate spikes and the unemployment rate rises

above the natural rate of unemployment. From the middle of 2008 to the most current period, the

middle of 2013, inflation remains at or below what appears to be the longer term trend of 2.5 percent,

while the unemployment rate is well above the natural rate, suggesting that demand-pull forces are at

work.

148 Mishkin • Macroeconomics: Policy and Practice, Second Edition

a. For the most recent period in 2013:Q1, the Fed Funds Rate is 0.14 percent, while the Taylor Rule

predicts a slightly negative –0.07 percent, representing a gap of 0.21 percent. Compared to other

significant deviations, this seems to be a fairly close correspondence, although the negative value

is not possible in practice.

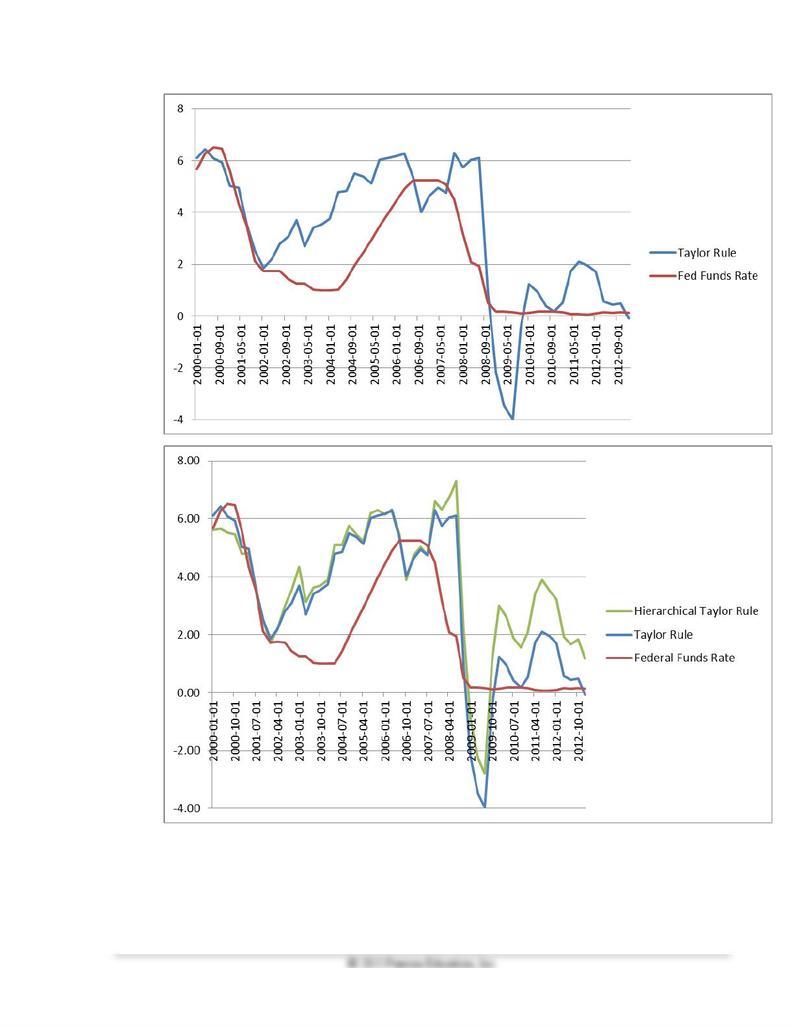

b. See graph below. The Taylor rule since 2000 has periods in which they are fairly closely

correlated, particularly from 2000 to 2002. However, there are significant gaps in other times, or

periods in which they do not seem to move together, such as the period from 2002 to 2006. From

2008 onward, there are significant differences between the two, particularly the period late in

2008 through 2010, in which the Taylor rule predicts the Fed Funds Rate should be negative by

as much as almost –4 percent, which is not possible. It also predicted a significant rise in the fed

funds rate in 2011, which did not materialize.

c. Because the Fed funds rate was at the zero lower bound during that time, conventional monetary

policy through adjustments in the fed funds rate was not possible, and highlights a limitation of

the Taylor rule: under “normal” conditions the Taylor rule provides a good approximation to

appropriate fed funds rate policy. However in extreme situations such as the financial crisis

period, the Taylor rule is less useful because other (unconventional) monetary policy tools are

needed to achieve stimulus.

d. See graph below. For the most part, the baseline Taylor rule and the hierarchical Taylor rule

predict nearly the same fed funds paths. The only significant deviations are from 2008 onwards,

where it predicts a significantly higher fed funds rate due to the inflation spike during that time.

Since 2010, it would predict a fed funds rate around 2 percent, which is much higher than during

that time and what the baseline rule predicts. For the current period, under such a hierarchical

Taylor rule, the fed funds rate would be predicted to be about 1.2 percent, much higher than the

current 0.14 percent.

Chapter 13 Macroeconomic Policy and Aggregate Demand and Supply Analysis 149

150 Mishkin • Macroeconomics: Policy and Practice, Second Edition

◼ Data Sources, Related Articles, and Discussion Questions

A. For Information About Policy and Practice: The Federal Reserve’s Use of

the Equilibrium Real Interest Rate, r*

Data Source

Federal Reserve System: http://www.federalreserve.gov/monetarypolicy/fomc_historical.htm. From this

page you can access previous blue and green books. There are also short descriptions of these publications.

Related Article

Federal Reserve System: FOMC Transcripts and Other Historical Materials, 2004.

http://www.federalreserve.gov/monetarypolicy/files/FOMC20040128bluebook20040122.pdf . This is the

January 27–28, 2004 FOMC Meeting bluebook. Note the Policy Alternatives on page 7 of this document

and the subsequent projections made by the FOMC staff.

Discussion Question

Suppose a new wave of technological innovation shifts the long-run aggregate supply curve to the right.

Everything else the same, what would be the effect on the equilibrium level of the real interest rate?

Chapter 13 Macroeconomic Policy and Aggregate Demand and Supply Analysis 151

152 Mishkin • Macroeconomics: Policy and Practice, Second Edition

Chapter 13 Macroeconomic Policy and Aggregate Demand and Supply Analysis 153