Chapter 1

Accounting and the Business Environment

Chapter 1: Overview

The chapter begins with an introduction to accounting and a brief discussion of why accounting is

important. The differences between financial and managerial accounting are delineated. The text

discusses how accounting information is needed by various users—individuals, businesses, investors,

creditors, and taxing authorities. Reasons accounting is important to students not majoring in accounting

and career paths available to accounting majors are briefly described, including a comparison of various

accounting positions. The role of governing organizations such as the Financial Accounting Standards

Board (FASB) and the Securities and Exchange Commission (SEC) as well as the FASB’s relationships

with both congressionally created and private accounting groups are explained. Generally Accepted

Accounting Principles (GAAP) are introduced. The sole proprietorship, partnership, corporation, and

limited liability company (LLC) forms of business are briefly described in the context of the economic

entity assumption. In addition, the cost principle, going concern assumption, and monetary unit

assumption are explained. The nature of International Financial Reporting Standards (IFRS) and the role

Chapter 1: Learning Objectives

Chapter 1: Teaching Outline with Lecture Notes

LO 1. Explain why accounting is important and list the users of accounting information

a) Define the term accounting and explain what accountants do

b) Exhibit 1-1: Pathways Vision Model

Lecture Notes: Accounting is defined as the information system that measures business activities,

processes the information into reports, and communicates the results to decision makers. However,

accountants do not simply prepare various types of accounting reports and tax returns. They also

review and interpret business information using critical thinking and judgment to partner with clients

and managers to help them make better business decisions.

c) Differentiate between financial accounting and managerial accounting

d) Exhibit 1-2: Decision Making: Financial Versus Managerial Accounting

Lecture Notes: Financial accounting provides historical information—the company reports on events

that have already occurred—to external decision makers, including investors and creditors.

Managerial accounting provides more future-oriented information—many companies prepare

budgets, forecasts, and projections based on future events—for internal decision makers (company

managers and executives).

e) Identify the users of accounting information:

i. Individuals

Manager (CGFM), Certified Fraud Examiner (CFE), Certified Financial Manager (CFM), Enrolled

LO 2. Describe the organizations and rules that govern accounting

a) Identify accounting governing organizations, including the Financial Accounting Standards

Board (FASB), the Security Exchange Commission (SEC), and the International Accounting

Standards Board (IASB)

b) Describe Generally Accepted Accounting Principles (GAAP) and introduce the primary

objective of financial reporting

c) Explain the economic entity assumption

i. Identify the different types of business organizations:

▪ Sole proprietorship

▪ Partnership

▪ Corporation

▪ Limited-liability company (LLC)

ii. Exhibit 1-4: Business Organizations

iii. Describe the distinguishing characteristics and organization of a corporation:

▪ Separate legal entity

▪ Continuous life and transferability of ownership

▪ No mutual agency

▪ Limited liability of stockholders

▪ Separation of ownership and management

▪ Corporate taxation

▪ Government regulation

▪ Organization

iv. Exhibit 1-5: Structure of a Corporation

Lecture Notes: Corporate status is not based on the size of the company. Not all large companies are

corporations, and not all small companies are sole proprietorships or partnerships. A corporation

could have only one stockholder. Why would a one-shareholder business incorporate the business in

this case? One reason is limited liability protection. Regardless of the number of stockholders, all

corporations follow the same general corporate procedures.

d) Explain the cost principle

e) Explain the going concern assumption

Although much has been written and discussed about the possibility of convergence of U.S. GAAP

LO 3. Describe the accounting equation and define assets, liabilities, and equity

a) The accounting equation: Assets = Liabilities + Equity

b) Define assets

c) Define liabilities

d) Define equity

Lecture Notes: The accounting equation must always balance. Demonstrate that the accounting

equation always balances, not just at the beginning of the year (or any accounting period). During

the year, the change in assets equals the change in liabilities plus the change in equity. At the end of

the year, the new values of the accounting equation will balance.

LO 4. Use the accounting equation to analyze transactions

a) Transaction analysis for Smart Touch Learning

i. Transaction 1—Stockholder contribution

ii. Transaction 2—Purchase of land for cash

iii. Transaction 3—Purchase of office supplies on account

iv. Transaction 4—Earning of service revenue for cash

3. Determine if the accounting equation is in balance.

When this process is applied correctly, the accounting equation will always balance. Thus, for all

transactions that occur during the year:

During the Year

Δ Assets =

Δ Liabilities +

Δ Equity

Note that every transaction affects the balance sheet in some way—increasing or decreasing an asset,

liability, or equity account—but may or may not affect another financial statement. Remind students

that there are four kinds of equity accounts: contributed capital, revenues, expenses, and dividends.

Thus, there are four ways that equity can change during the year:

During the Year

Δ Assets =

Δ Liabilities .

+ Contributed Capital

+ Revenues

– Expenses

– Dividends

Some students may be confused by how the issuance of stock increases a company’s equity. “If the

Also, it may be helpful to point out that some transactions affect only one side of the accounting

LO 5. Prepare financial statements

a) Exhibit 1-7: Financial Statements

i. Exhibit 1-8: Income Statement

ii. Exhibit 1-9: Statement of Retained Earnings

iii. Exhibit 1-10: Balance Sheet

iv. Exhibit 1-11: Statement of Cash Flows

Lecture Notes: Each of the financial statements required by GAAP focuses on a different aspect of

the company’s financial position or financial activity. All four statements should be analyzed in

order to get a complete picture of a company. Emphasize the links between the statements.

The income statement shows the change in equity that results from the operation of the business

during the year. The retained earnings statement shows the change in equity from profits earned less

dividends paid to the stockholders during the year. Balance sheets show the financial position of the

company at specific points in time. The statement of cash flows shows the change in Cash in relation

to everything else that changed during the year.

Each financial statement should have a company name, a statement title, and some form of date. The

balance sheet shows the financial composition of the company at a specific point in time, such as at

the end of the year. The balance sheet will probably change the day after it is prepared. All the other

financial statements describe what happened to the company during the year. The income statement

tracks profitability—revenues minus expenses. Remember that “profit” doesn’t necessarily mean

“money”; the profit may not have been collected in cash yet. The statement of retained earnings

The cash flow statement shows how the company is generating and using its cash. Students may

LO 6. Use financial statements and return on assets (ROA) to evaluate business performance

a) Review financial statements of Kohl’s Corporation. (see

http://www.pearsonhighered.com/Horngren)

b) Explain return on assets (ROA)

Lecture Notes: Information presented in the financial statements is largely based on historical cost—

the cost principle. Beginning students may think the value of total assets on the balance sheet

represents the “true” value of the company, which is incorrect. The balance sheet values of major

assets such as land, buildings, and equipment are based on the historical cost of those assets and may

not represent their fair market value. For example, land purchased 10 years ago is likely to be worth

Chapter 1: Handout for Student Notes

LO 1. Why is accounting important?

LO 2. What are the organizations and rules that govern accounting?

▪ Distinguishing characteristics and organization of a corporation

LO 3. What is the accounting equation?

LO 4. How do you analyze a transaction?

▪ Transaction 2—Purchase of land for cash

LO 5. How do you prepare financial statements?

LO 6. How do you use financial statements to evaluate business performance?

Chapter 1: Student Chapter Summary

LO 1. Explain why accounting is important and list the users of accounting information

Accounting is the language of business. Financial accounting is used by a variety of decision

LO 2. Describe the organizations and rules that govern accounting

The rules that govern accounting are called Generally Accepted Accounting Principles (GAAP).

The Financial Accounting Standards Board (FASB) is responsible for the creation and

governance of U.S. GAAP. The Securities and Exchange Commission (SEC) oversees the U.S.

financial markets and other standard setters, such as the FASB.

A thorough understanding of GAAP is essential to the use and preparation of financial

statements. The primary objective of financial reporting is to provide information useful for

LO 3. Describe the accounting equation and define assets, liabilities, and equity

LO 4. Use the accounting equation to analyze transactions

LO 5. Prepare financial statements

Four financial statements are prepared for each accounting period. The income statement reports

LO 6. Use financial statements and return on assets (ROA) to evaluate business performance

The income statement evaluates profitability. The statement of retained earnings shows the

amount of earnings kept and reinvested in the company. The balance sheet lists the economic

Chapter 1: Assignment Grid and Other Materials

P 1-46A, P1-53B

X

X

S – Short Exercises (Easy)

E – Exercises (Moderate)

P – Problems (Difficult)

Other End-of-Chapter Materials:

Using Excel Problem P1-54

CHAPTER 1

3. Which accounting principle or assumption assumes that an entity will remain in operation for the

4. Red Door Boutique is famous for fashion wristwatches and leather purses. At the end of a recent year,

5. Assume that Red Door Boutique purchased supplies on account for $58,000. How would this

6. Which field of accounting provides information to external decision makers such as investors and

8. Last year, Internet Service Company (ISC) sold services on account for $75,000 and incurred

expenses totaling $48,000. At the end of the year, the balance for Accounts Receivable was $10,000,

10. On the 20XX income statement, Red Door Boutique reported net income of $900,000. The company

reported beginning total assets of $8,000,000 and ending total assets of $10,000,000. What is Red

Answer Key to Ten-Minute Quiz:

10. B

Return on assets = Net Income / Average total assets = $900,000 / [($800,000,000 + $10,000,000) / 2] =

$900,000 / $9,000,000 = 10.00%

Extra Critical Thinking Questions

Decision Case 1-2

Dave and Reba Guerrera saved all their married life to open a bed and breakfast (B&B) named Tres

Amigos. They invested $100,000 of their own money, and the company issued common stock to them.

The business then got a $100,000 bank loan for the $200,000 needed to get started. The company bought

a rundown old Spanish colonial home in Tucson for $80,000. It cost another $50,000 to renovate.

They found most of the furniture at antique shops and flea markets—for a total cost of $20,000. Kitchen

equipment cost $10,000, and a computer system cost $2,000.

Prior to the grand opening, the banker requests a report on their activities thus far. The bank statement of

Tres Amigos shows a cash balance of $38,000. Dave and Reba believe that the $38,000 represents net

1. Suppose you are the Guerreras’ banker, and they have given you this income statement. Would you

congratulate them on their net income? If so, explain why. If not, how would you advise them to

2. Prepare the balance sheet for Tres Amigos based on these data.

Decision Case 1-2: Solution

Requirement 1

The banker would not congratulate the Guerreras for their net income because they have not measured

net income properly. In fact, they have no net income at all. Net income is revenues minus expenses, and

the Guerreras do not have any revenues or expenses. The amount of cash in the bank does not measure

net income, as it is the result of a loan from the bank.

Requirement 2

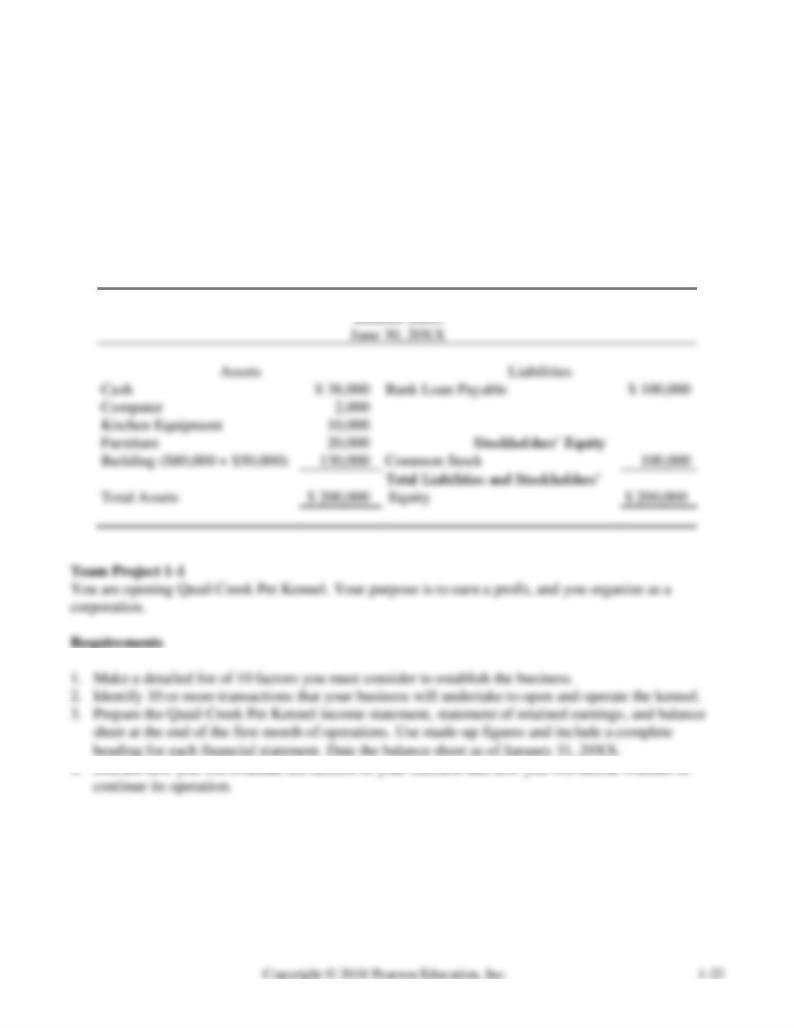

TRES AMIGOS BED AND BREAKFAST

Team Project 1-1: Solution

11. Pay dividends

Student answers may vary.

Team Project 1-1: Solution (cont’d)

Requirement 3

QUAIL CREEK PET KENNEL

Income Statement

Month Ended January 31, 20XX

Revenue:

Service Revenue

$ 10,000

Expenses:*

Wages Expense

$ 2,000

Supplies Expense

400

Advertising Expense

300

Utilities Expense

100

Total Expense

2,800

Net Income

$ 7,200

*Students may also include depreciation expense on the building.

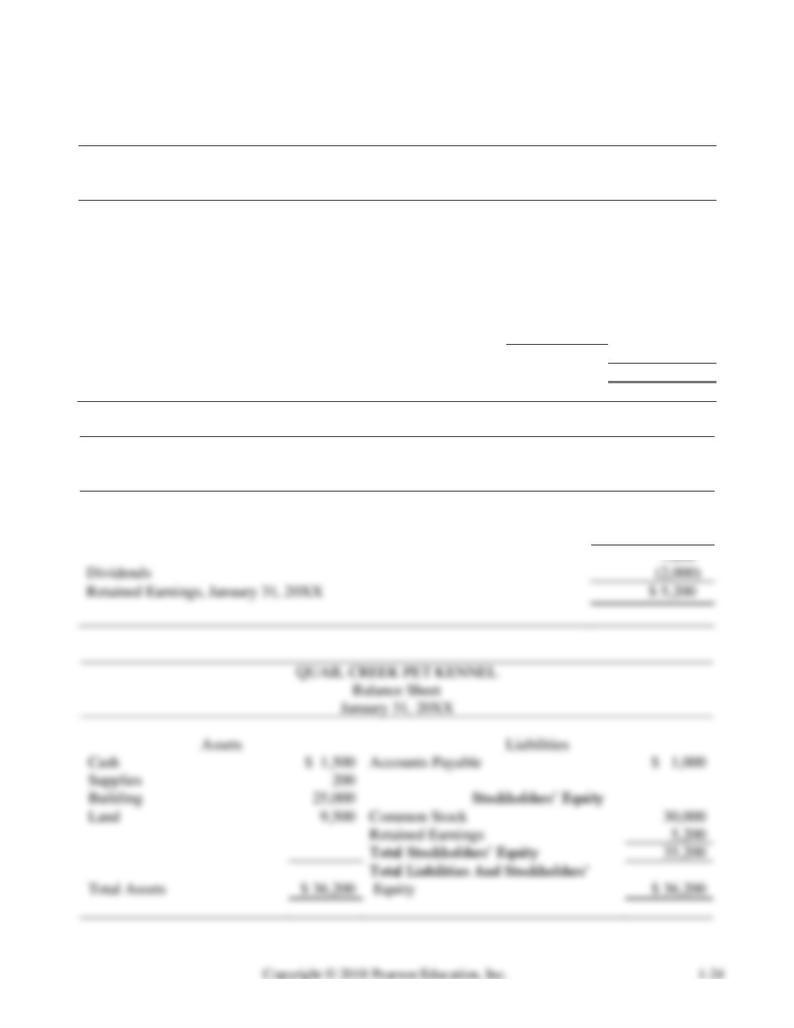

QUAIL CREEK PET KENNEL

Statement of Retained Earnings

Month Ended January 31, 20XX

Retained Earnings, January 1, 20XX

$ 0

Net income for the month

7,200

4. Assume that you will continue to promote rock concerts if the venture is successful. If it is

7. How to offer concessions (buy and sell them yourself or arrange for outside concessionaires). If

10. Timing of the concert in relation to other events in the area at the time.

Team Project 1-2: Solution (cont’d)

Requirement 3

CONCERT ENTERPRISES

Income Statement

Three Months Ended June 30, 20XX

Revenue:

Ticket Sales Revenue

$ 300,000

Concession Revenue

50,000

Total Revenue

350,000

Expenses:

Band Expense

$ 100,000

Advertising Expense

50,000

Concession Expense

20,000

Rent Expense

15,000

Security Expense

10,000

Utilities Expense

3,000

Permits Expense

2,000

Total Expenses

200,000

Net Income

$ 150,000

Team Project 1-2: Solution (cont’d)

CONCERT ENTERPRISES

Statement of Retained Earnings

Three Months Ended June 30, 20XX