Chapter 4

Completing the Accounting Cycle

Chapter 4: Overview

The chapter begins with a review of the financial statements, emphasizing the relationships

among them. The classified balance sheet is explained, focusing on the classification of assets

and liabilities as current or long term. Assets are listed based on liquidity, starting with the most

liquid—Cash. Liabilities are listed in the order in which they must be paid. Stockholders’ equity

reflects stockholders’ contributions through common stock and earnings retained in the business.

The report format and the account format of the balance sheet are illustrated.

Next, the text discusses how the worksheet introduced in Chapter 3 aids in preparing the

financial statements. The income statement, balance sheet, and net income/loss sections of the

worksheet are reviewed and completed. Students follow the preparation of the worksheet from

the trial balance through adjustments, to extending account balances to the proper columns, and

finally to computing net income or net loss.

Chapter 4: Learning Objectives

Chapter 4: Teaching Outline with Lecture Notes

LO 1. Prepare the financial statements including the classified balance sheet

a) Review the income statement, statement of retained earnings, and balance sheet

i. Exhibit 4-1: Adjusted Trial Balance

b) Relationships among the financial statements

i. Exhibit 4-2: Smart Touch Learning Financial Statements

c) The classified balance sheet

i. Classify assets and liabilities as current or long term

ii. Stockholders’ equity reflects owner contributions and retained earnings

LO 2. Use the worksheet to prepare financial statements

a) Complete the remaining sections of the worksheet (sections 1–4 are introduced in

Chapter 3)

statements may also be prepared directly from the adjusted trial balance. If the worksheet

method is used, it can be prepared manually or with the assistance of a software program.

The textbook uses a 10-column worksheet, with 5 sets of debit/credit columns. This format

can vary in practice. The worksheet provides a check figure in that the first 3 sets of columns

should have equal debits and credits. The last two sets of columns, the income statement and

balance sheet, will not have equal debits and credits (unless net income is zero). Instead, the

difference in these columns should be the same amount, but on opposite sides (debit versus

credit), and represents the net income/loss for the period. The net income/loss amount is a

balancing amount⎯the amount is entered in the appropriate column for the income statement

and balance sheet in order for debits to equal credits.

Students may be confused with the amount of net income/loss being placed in the debit or

credit column. Net income or net loss is the balancing amount on the worksheet. It should

LO 3. Explain the purpose of, journalize, and post closing entries

a) Explain the closing process and define the following terms:

b) Exhibit 4-5: The Closing Process

c) Exhibit 4-6: Journalizing and Posting Closing Entries

Lecture Notes: The closing process consists of journalizing and posting the closing entries to

set the balances of the revenues, expenses, Income Summary, and Dividends accounts to zero

for the next period. Closing entries reflect the action taken “on paper” when the statement of

LO 4. Prepare the post-closing trial balance

a) Exhibit 4-7: Post-Closing Trial Balance

LO 5. Describe the accounting cycle

a) Exhibit 4-8: The Accounting Cycle

LO 7. Explain the purpose of, journalize, and post reversing entries (Appendix 4A)

a) Accounting for accrued expenses

b) Accounting without a reversing entry

c) Accounting with a reversing entry

Chapter 4: Handout for Student Notes

LO 1. How do we prepare financial statements?

LO 2. How could a worksheet help in preparing financial statements?

LO 3. What is the closing process, and how do we close the accounts?

o Closing temporary accounts—Net loss for the period

LO 4. How do we prepare a post-closing trial balance?

LO 5. What is the accounting cycle?

LO 6. How do we use the current ratio to evaluate business performance?

LO 7. What are reversing entries? (Appendix 4A)

Chapter 4: Student Chapter Summary

LO 2. Use the worksheet to prepare financial statements

LO 3. Explain the purpose of, journalize, and post closing entries

LO 4. Prepare the post-closing trial balance

LO 7. Explain the purpose of, journalize, and post reversing entries (Appendix 4A)

Chapter 4: Assignment Grid and Other Materials

P4-33A, P4-39B

X

X

X

X

X

Other End-of-Chapter Materials:

Using Excel P4-41

1. What is the last step in the accounting cycle?

2. Which columns of the accounting worksheet show unadjusted amounts?

3. Which of the following accounts may appear on a post-closing trial balance?

4. Which situation indicates a net income within the Income Statement columns of the worksheet?

5. Christopher’s Closet sells men’s clothing. At the end of the current year, Christopher’s Closet

has Rent Expense of $1,500, and Supplies Expense of $829. What closing entry will

Christopher’s Closet make for these expense accounts?

Date

Accounts and Explanations

Debit

Credit

A.

Rent Expense

1,500

Supplies Expense

829

7. Which of the following statements is true?

8. Which of the following is an appropriate closing entry?

Date

Accounts and Explanations

Debit

Credit

A.

Income Summary

XXX

10. Ellison Electronics has Cash of $200, Accounts Receivable of $800, Office Supplies of $400,

Supplies Expense of $200, and Service Revenue of $900. Ellison owes $300 on Accounts

Payable, $500 on Salaries Payable, and $700 on Long-term Notes Payable. What is Ellison’s

Answer Key to Ten-Minute Quiz:

Extra Critical Thinking Questions

Decision Case 4-1

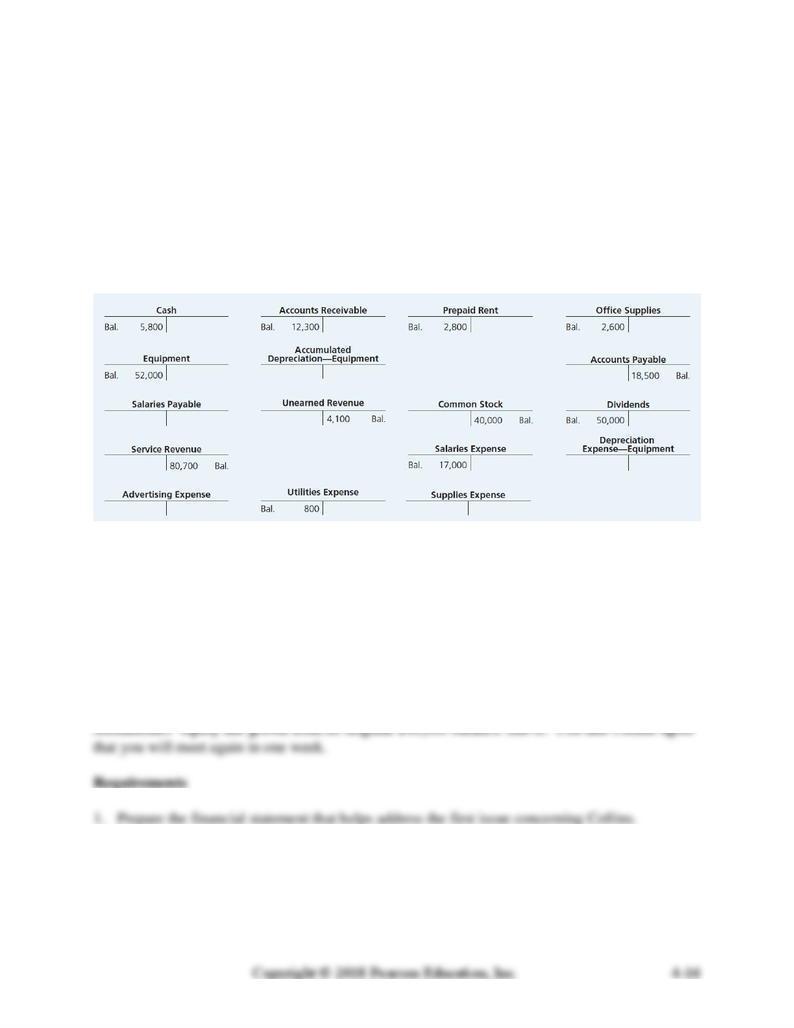

One year ago, Ralph Collins founded Collins Consignment Sales Company, and the business has

prospered. Collins comes to you for advice. He wishes to know how much net income the

business earned during the past year. The accounting records consist of the T-accounts in the

ledger, which were prepared by an accountant who has moved. The accounts at December 31,

20XX, follow:

Collins indicates that, at year-end, customers owe the business $1,000 accrued service revenue,

which the business expects to collect early next year. These revenues have not been recorded.

During the year, the business collected $4,100 service revenue in advance from customers, but

the business has earned only $800 of that amount. During the year Collins Consignment has

incurred $2,400 of advertising expense, but the business has not yet paid for it. In addition, the

business has used up $2,100 of the office supplies. Collins determines that depreciation on

equipment was $7,000 for the year. At December 31, 20XX, the business owes its employee

$1,200 accrued salary.

To get a loan to expand the business, Collins must show the bank that the business’s

2. Can Collins expect to get the loan? Give your reason(s).

Decision Case 4-1: Solution

Requirement 1

Mr. Collins will need to prepare an income statement to answer his question:

COLLINS CONSIGNMENT SALES COMPANY

Income Statement

Year Ended December 31, 20XX

Revenues:

Service Revenue ($80,700 + $1,000 + $800)

$ 82,500

Expenses:

Salaries Expense ($17,000 + $1,200)

$ 18,200

Depreciation Expense—Equipment