Chapter 07: Current Asset Management

Chapter 7

Current Asset Management

Discussion Questions

7-1.

In the management of cash and marketable securities, why should the primary

concern be for safety and liquidity rather than maximization of profit?

7-2.

Explain the similarities and differences of lockbox systems and regional

collection offices.

7-3.

Why would a financial manager want to slow down disbursements?

200. Which security would you choose for a short-term investment? Why?

Chapter 07: Current Asset Management

7-5.

Why are Treasury bills a favorite place for financial managers to invest excess

cash?

7-6.

Explain why the bad debt percentage or any other similar credit-control

percentage is not the ultimate measure of success in the management of

accounts receivable. What is the key consideration?

7-7.

What are three quantitative measures that can be applied to the collection policy

of the firm?

7-8.

What are the 5 Cs of credit that are sometimes used by bankers and others to

determine whether a potential loan will be repaid?

7-9.

What does the EOQ formula tell us? What assumption is made about the usage

rate for inventory?

Chapter 07: Current Asset Management

7-10.

Why might a firm keep a safety stock? What effect is it likely to have on

carrying cost of inventory?

7-11.

If a firm uses a just-in-time inventory system, what effect is that likely to have

on the number and location of suppliers?

Chapter 7

Problems

1. Cost-benefit analysis of cash management (LO2) City Farm Insurance has collection

centers across the country to speed up collections. The company also makes its

disbursements from remote disbursement centers. The collection time has been reduced by

two days and disbursement time increased by one day because of these policies. Excess

funds are being invested in short-term instruments yielding 12 percent per annum.

a. If City Farm has $5 million per day in collections and $3 million per day in

City Farm Insurance

a. $5,000,000 daily collections × 2.0 days speedup =

$10,000,000 additional collections

$3,000,000 daily disbursements × 1.0 days slowdown =

$ 3,000,000 delayed disbursements

$13,000,000 freed-up funds

Chapter 07: Current Asset Management

b.

$13,000,000 freed-up funds

12% interest rate

$ 1,560,000 interest on freed-up cash

2. Cost-benefit analysis of cash management (LO2) Neon Light Company of Kansas City

ships lamps and lighting appliances throughout the country. Ms. Neon has determined that

through the establishment of local collection centers around the country, she can speed up

the collection of payments by three days. Furthermore, the cash management department of

× 0.5 days slowdown = $525,000 delayed disbursements

$7,275,000 freed-up funds

Chapter 07: Current Asset Management

3. International cash management (LO2) Orbital Communications has operating plants in

Orbital Communications

$40,000 × 1.13 = $45,200

$45,200 × 106% = $47,912

4. International cash management (LO2) Postal Express has outlets throughout the world.

It also keeps funds for transactions purposes in many foreign countries. Assume in 2010 it

held 240,000 reals in Brazil worth 170,000 dollars. It drew 12 percent interest, but the

Brazilian real declined 24 percent against the dollar.

Postal Express

a. $170,000 × 1.12 = $190,400

$190,400 × 76% = $114,704 dollar value of real holdings

b. $170,000 × 1.09 = $185,300

$185,300 × 113% = $209,389 dollar value of real holdings

Chapter 07: Current Asset Management

7-5. Solution:

Thompson Wood Products

7-6. Solution:

Oral Roberts Dental Supplies

Chapter 07: Current Asset Management

$559,000

Average collection period 4,680,000/360

$559,000

$13,000

= 43 days

=

=

7. Accounts receivable balance (LO4) Knight Roundtable Co. has annual credit sales of

$1,080,000 and an average collection period of 32 days in 2008. Assume a 360-day year.

Knight Roundtable Co.

$1,080,000annual credit sales $3,000credit sales a day

360days per year =

$3,000 average 32 average $96,000 average accounts

daily credit sales collection period receivable balance

=

8. Accounts receivable balance (LO4) Darla’s Cosmetics has annual credit sales of

$1,440,000 and an average collection period of 45 days in 2008. Assume a 360-day year.

Darla’s Cosmetic Company

$1,440,000 annual credit sales/360 = $4,000 per day credit sales

Chapter 07: Current Asset Management

$4,000 credit sales × 45 average collection period = $180,000

average accounts receivable balance

7-9. Solution:

Barney’s Antique Shop (Continued)

Accounts receivable

Average collection period Average daily credit sales

$157,500

=

Chapter 07: Current Asset Management

10. Determination of credit sales (LO4) Mervyn’s Fine Fashions has an average collection

period of 50 days. The accounts receivable balance is $95,000. What is the value of its

credit sales?

Mervyn’s Fine Fashion

Accounts receivable

Average collection period Average daily credit sales

$95,000

50 days Credit sales

360

credit sales $95,000

360 50

Credit sales/360 $1,900

Credit sales $1,900 360 $684,000

=

=

=

=

= =

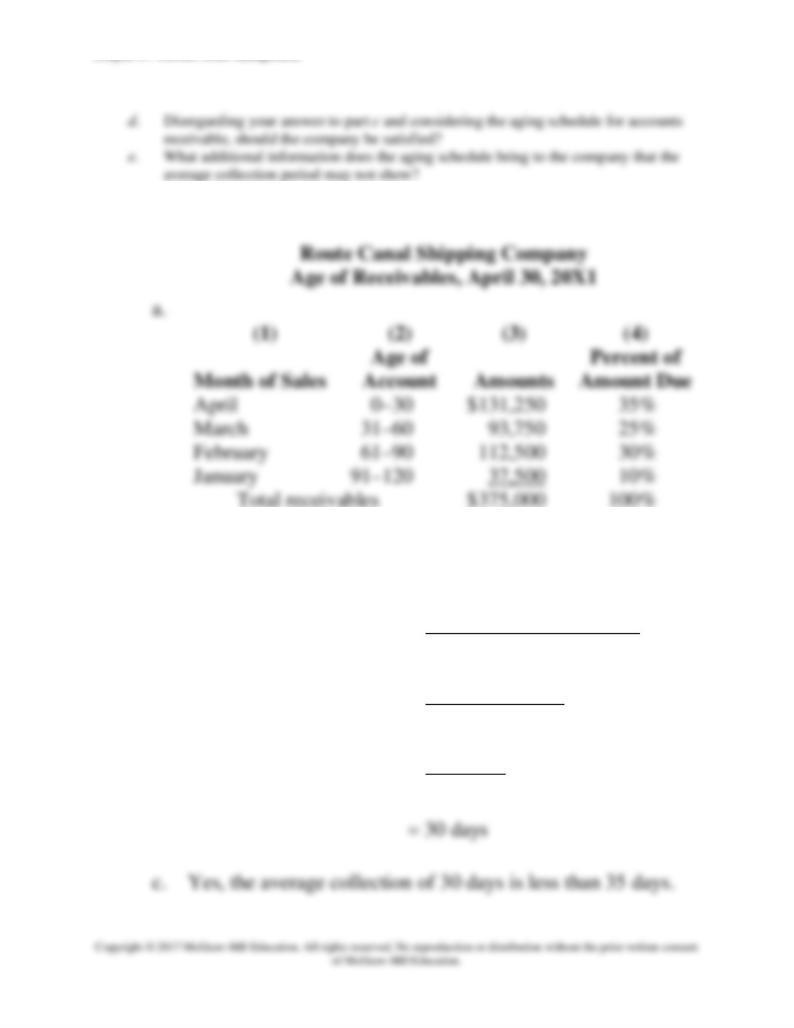

January .............................

91–120

37,500

____

Total receivables ...........

$ 375,000

100%

a. Fill in column (4) for each month.

b. If the firm had $1,500,000 in credit sales over the four-month period, compute the

Chapter 07: Current Asset Management

7-11. Solution:

7-11. (Continued)

b.

Accounts receivable

Average collection period Average daily credit sales

$375,000

$1,500,000 /120

$375,000

$12,500

=

=

=

Chapter 07: Current Asset Management

7-12. Solution:

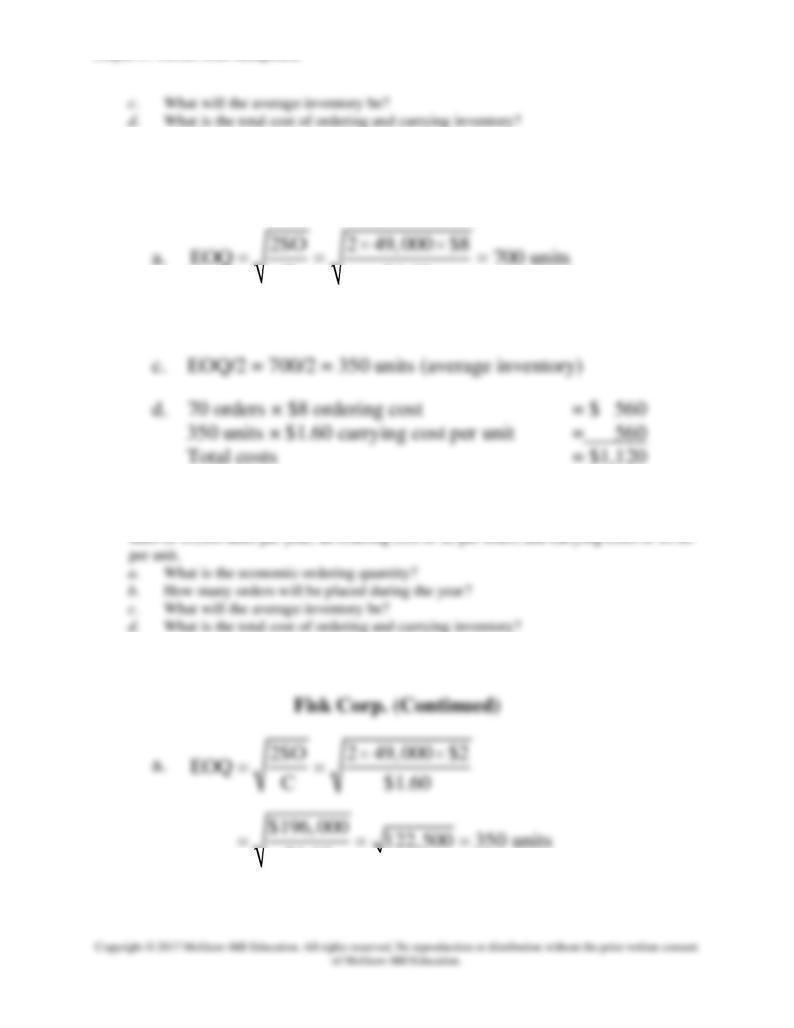

13. Economic ordering quantity (LO5) Fisk Corporation is trying to improve its inventory

control system and has installed an online computer at its retail stores. Fisk anticipates

sales of 49,000 units per year, an ordering cost of $8 per order, and carrying costs of $1.60

Chapter 07: Current Asset Management

7-13. Solution:

Fisk Corp.

C $1.60

b. 49,000 units/700 units = 70 orders

14. Economic ordering quantity (LO5) Fisk Corporation is trying to improve its inventory

control system and has installed an online computer at its retail stores. Fisk anticipates

7-14. Solution:

$1.60

b. 49,000 units/350 units = 140 orders

15. Economic ordering quantity with safety stock (LO5) Diagnostic Supplies has expected

7-15. Solution:

Diagnostic Supplies

a.

2SO 2 84,100 $10

EOQ C $5

==

$1,682,000 $336,400 580 units

$5

= = =

b. EOQ/2 = 580/2 = 290 units (average inventory)

Chapter 07: Current Asset Management

16. Level versus seasonal production (LO5) Wisconsin Snowmobile Corp. is considering a

switch to level production. Cost efficiencies would occur under level production, and

aftertax costs would decline by $36,000, but inventory would increase by $300,000.

Wisconsin Snowmobile has to finance the extra inventory at a cost of 13.5 percent.

a. Determine the extra cost or savings of switching over to level production. Should the

7-16. Solution:

Wisconsin Snowmobile Corporation

a. Inventory increases by $300,000

× Interest expense 13.5%

Increased costs $ 40,500

Savings $36,000

Less: Increased costs ($40,500)

Loss ($ 4,500)

Don’t switch to level production.

Chapter 07: Current Asset Management

17. Credit policy decision (LO4) Johnson Electronics is considering extending trade credit to

some customers previously considered poor risks. Sales would increase by $150,000 if credit

is extended to these new customers. Of the new accounts receivable generated, 5 percent will

7-17. Solution:

Johnson Electronics

a. Additional sales .................................................... $150,000

Accounts uncollectible (5% of new sales) ........... – 7,500

Annual incremental revenue ................................ $ 142,500

Chapter 07: Current Asset Management

b.

Incremental income

Incremental return on sales Incremental sales

$18,525 / $150,000 12.35%

=

==

c. Receivable turnover = Sales/Receivable turnover = 3x

Receivables = Sales/Receivable turnover

= $150,000/3

= $50,000.00

Incremental return on new average investment =

$18,525/$50,000.00 = 37.05%

18. Credit policy decision-receivables and inventory (LO4 and 5) Henderson Office Supply

is considering a more liberal credit policy to increase sales, but expects that 9 percent of the

new accounts will be uncollectible. Collection costs are 6 percent of new sales, production

and selling costs are 74 percent, and accounts receivable turnover is four times. Assume

income taxes of 20 percent and an increase in sales of $65,000. No other asset buildup will

be required to service the new accounts.

7-18. Solution:

Chapter 07: Current Asset Management

Henderson Office Supply

a.

$65,000

Investment in accounts receivable $16,250

4

==

7-18. (Continued)

c. Yes! 35.20 percent exceeds the required return of 16 percent.

$65,000

Chapter 07: Current Asset Management

$5,720/$48,750 = 11.73% return on investment

e. No! 11.73 percent is less than the required return of 16

percent.

19. Credit policy decision with changing variables (LO4) Fast Turnstiles Co. is evaluating

the extension of credit to a new group of customers. Although these customers will provide

$180,000 in additional credit sales, 12 percent are likely to be uncollectible. The company

will also incur $16,200 in additional collection expense. Production and marketing costs

1.6, and 12 percent of the accounts are uncollectible. Should credit be extended if the

receivables turnover drops to 1.6, and 12 percent of the accounts are uncollectible (as

in part a)?

Fast Turnstiles Co.

a. Added sales ............................................................. $180,000

Accounts uncollectible (12% of new sales) ............ 21,600

Annual incremental revenue ................................... 158,400

Collection costs ....................................................... 16,200

Production and selling costs

(72% of new sales) ................................................ 129,600

Annual income before taxes .................................... 12,600

Taxes (34%) ............................................................ 4,284

Incremental income after taxes ............................... $ 8,316

Chapter 07: Current Asset Management

$180,000

Receivable turnover $45,000

4.0

$8,316

Return on incremental investment 18.48%

$45,000

==

==

Yes, extend credit to these customers since the incremental

return of 18.48 percent is greater than 10 percent.

b. Added sales .......................................................... $180,000

Accounts uncollectible (15% of new sales) ......... 27,000

Annual incremental revenue ................................ $153,000

Collection costs .................................................... 16,200

Production and selling costs

(72% of new sales) .............................................. 129,600

new receivables

Chapter 07: Current Asset Management

20. Credit policy decision with changing variables (LO4) Slow Roll Drum Co. is evaluating

the extension of credit to a new group of customers. Although these customers will provide

$180,000 in additional credit sales, 12 percent are likely to be uncollectible. The company

will also incur $16,200 in additional collection expense. Production and marketing costs

represent 72 percent of sales. The firm is in a 34 percent tax bracket. No other asset buildup

will be required to service the new customers. The firm has a 10 percent desired return.

Assume the average collection period is 120 days.

a. Compute the return on incremental investment

b. Should credit be extended?

7-20. Solution:

Slow Roll Drum Co.

a. Added sales ............................................................. $180,000

Accounts uncollectible (12% of new sales) ............ 21,600

Annual incremental revenue ................................... 158,400

Collection costs ....................................................... 16,200

Production and selling costs

(72% of new sales) ................................................ 129,600

Annual income before taxes .................................... 12,600

Chapter 07: Current Asset Management

$8,316 13.86%

$60,000 =

Yes, extend credit. 13.86 percent is greater than 10 percent.

21. Credit policy and return on investment (LO4) Global Services is considering a

promotional campaign that will increase annual credit sales by $450,000. The company

will require investments in accounts receivable, inventory, and plant and equipment. The

turnover for each is as follows:

Accounts receivable ....................................

2x

Inventory .....................................................

6x

Plant and equipment ....................................

1x

All $450,000 of the sales will be collectible. However, collection costs will be 6 percent of

sales, and production and selling costs will be 71 percent of sales. The cost to carry

Global Services

a. Accounts receivable = Sales/Accounts receivable turnover

$225,000 $450,000/2=

Inventory = Sales/Inventory turnover

$75,000 $450,000/6=

Plant and equipment = Sales/(Plant and equipment turnover)

Chapter 07: Current Asset Management

$450,000 450,000 1

$/

=

$750,000 Total investment

7-21. (Continued)

b. Collection cost = 6% × $450,000 $ 27,000

Production and selling costs = 71% × $450,000 = 319,500

Total costs related to accounts receivable $346,500

c. Cost of carrying inventory

4% × inventory

4% × $75,000 $3,000

d. Depreciation expense

5% × $450,000 $22,500

e. Total costs related to accounts receivable $346,500

Cost of carrying inventory 3,000

Depreciation expense 22,500

Total costs $372,000

Chapter 07: Current Asset Management

22. Credit policy decision with changing variables (LO4) Dome Metals has credit sales of

$180,000 yearly with credit terms of net 60 days, which is also the average collection

period. Dome does not offer a discount for early payment, so its customers take the full 60

days to pay. What is the average receivables balance? Receivables turnover?

7-22. Solution:

Dome Metals

Sales/360 days = Average daily sales

$180,000/360 = $500

23. Dome Metals had credit sales of $180,000 yearly. Dome offered a 3 percent discount for

payment in 18 days. What would the average receivables balance be?

7-23. Solution:

24. Dome Metals had credit sales of $180,000 yearly with credit terms of net 60 days, which is

also the average collection period. If Dome offered a 3 percent discount for payment in 18

days and every customer took advantage of the new terms and reduced its bank loans,

Chapter 07: Current Asset Management

which cost 12 percent, by the cash generated from its reduced receivables, what will be the

net gain or loss to the firm? Should it offer the discount?

7-24. Solution:

Sales / 360 days = Average daily sales

$180,000 / 360 = $500

Old receivable balance = $500 × 60 days = $30,000

New receivable balance= $500 × 18 days = $9,000

25. Dome Metals has credit sales of $180,000 yearly with credit terms of net 60 days, which is

also the average collection period. Dome offered a 3 percent discount for payment in 18

days, and Dome reduced its bank loans, which cost 12 percent. Assume that the new trade

terms of 3/18, net 60 will increase sales by 15 percent because the discount makes the

Dome’s price competitive. If Dome earns 20 percent on sales before discounts, what will

be the net change in income? Should it offer the discount?

7-25. Solution:

New sales = $180,000 × 1.15 = $207,000

Change in sales = $207,000 – $180,000 = $ 27,000

Chapter 07: Current Asset Management

Net change in income ............................................ $ 1,548

Yes, offer the discount because total profit increases.

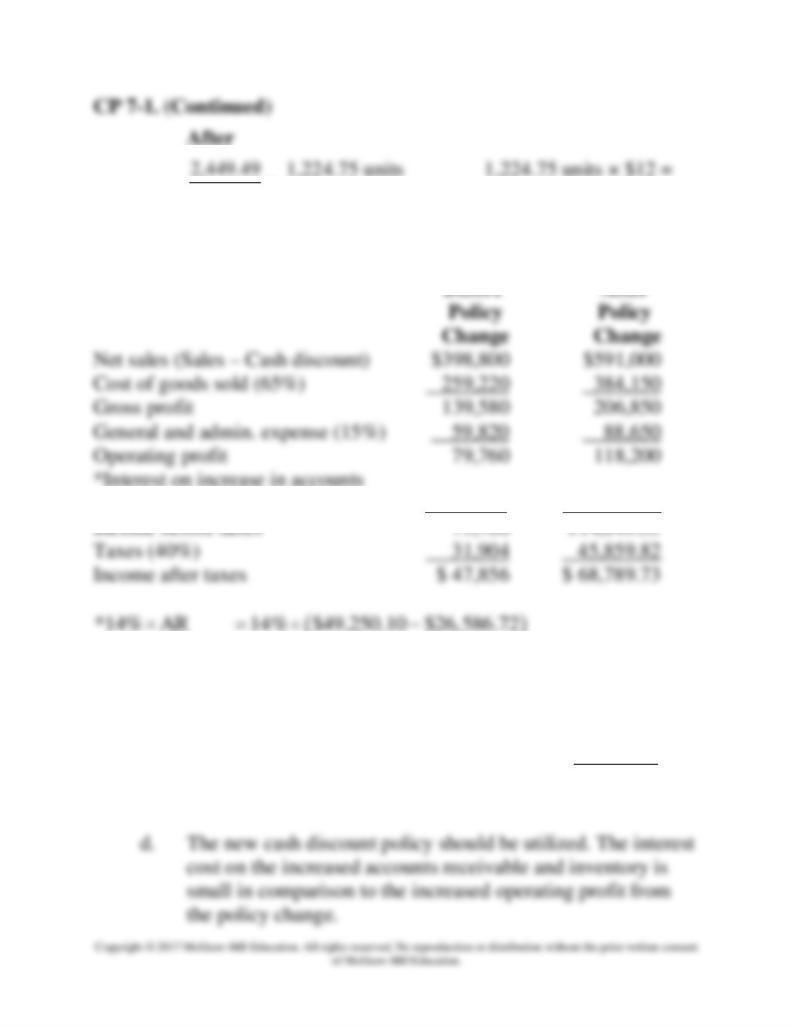

COMPREHENSIVE PROBLEM

Logan Distributing Company (receivables and inventory policy) (LO4 and 5) Logan

Distributing Company of Atlanta sells fans and heaters to retail outlets throughout the Southeast.

Joe Logan, the president of the company, is thinking about changing the firm’s credit policy to

EOQ/2. Each unit in inventory has an average cost of $12.

Cost of goods sold is equal to 65 percent of net sales; general and administrative expenses are

15 percent of net sales, and interest payments of 14 percent will only be necessary for the

increase in the accounts receivable and inventory balances. Taxes will be 40 percent of before-

tax income.

a. Compute the accounts receivable balance before and after the change in the cash

discount policy. Use the net sales (total sales minus cash discounts) to determine the

average daily sales.

b. Determine EOQ before and after the change in the cash discount policy. Translate this

into average inventory (in units and dollars) before and after the change in the cash

discount policy.

a. Accounts receivable = Average collection × Average daily

period sales

Before

24 days (Avg. acc. receivables)

Average daily sales

Chapter 07: Current Asset Management

( )( )( )

$400,000 .01 .30 $400,000

Credit sales Discount

360 days 360 days

$400,000 $1,200

−

−=

−

( )( )( )

Credit sales discount

360 days 360 days

$600,000 $9,000

360 days

$591,000

360 days

Average daily sales $1,641.67

−=

−

=

=

=

Chapter 07: Current Asset Management

$1.50 $1.50

$1.50 $1.50

Average inventory

Chapter 07: Current Asset Management

2=

c.

receivable and inventory (14%)

3,550.45

( )

14% $22,663.38=

$3,172.87=

14% INV

( )

=14% $14,697 $12,000−

14% $2.697=

$ 377.58=

$3,550.45

1,224.75 units 1,224.75 units × $12 =

or 1,225 (rounded) $14,697 or $14,700

(rounded)