Chapter 13: Risk and Capital Budgeting

Chapter 13

Risk and Capital Budgeting

Discussion Questions

13-2.

Discuss the concept of risk and how it might be measured.

13-3.

When is the coefficient of variation a better measure of risk than the standard

deviation?

13-4.

Explain how the concept of risk can be incorporated into the capital budgeting

process.

Risk may be introduced into the capital budgeting process by requiring higher

Chapter 13: Risk and Capital Budgeting

13-5.

If risk is to be analyzed in a qualitative way, place the following investment

decisions in order from the lowest risk to the highest risk:

a. New equipment

b. New market

c. Repair of old machinery

13-6.

Assume a company, correlated with the economy, is evaluating six projects, of

which two are positively correlated with the economy, two are negatively

correlated, and two are not correlated with it at all. Which two projects would

you select to minimize the company’s overall risk?

13-7.

Assume a firm has several hundred possible investments and that it wants to

analyze the risk-return trade-off for portfolios of 20 projects. How should it

proceed with the evaluation?

Chapter 13: Risk and Capital Budgeting

13-8.

Explain the effect of the risk-return trade-off on the market value of common

stock.

13-9.

What is the purpose of using simulation analysis?

Chapter 13

Problems

1. Risk-averse (LO13-2) Assume you are risk-averse and have the following three choices.

Which project will you select? Compute the coefficient of variation for each.

VD

=

A. $1,440/$2,200 = .65

B. 1,960/2,730 = .72

C. $1,490/$2,250 = .66

Chapter 13: Risk and Capital Budgeting

Based on the coefficient of variation, you should select Project A

because it is the least risky.

2. Expected value and standard deviation (LO13-1) Myers Business Systems is evaluating

the introduction of a new product. The possible levels of unit sales and the probabilities of

their occurrence are given next:

Possible

Market Reaction

Sales

in Units

Probabilities

Low response ............................................

20

.10

Moderate response ....................................

40

.30

High response ...........................................

55

.40

Very high response ...................................

70

.20

Myers Business Systems

a.

D DP=

D P DP

60 =

D

b.

2

()D D P

=−

D

D

()DD−

2

()DD−

P

2

()DD−

P

55

50

+5

25

.40

10

70

50

+20

400

.20

80

210

Chapter 13: Risk and Capital Budgeting

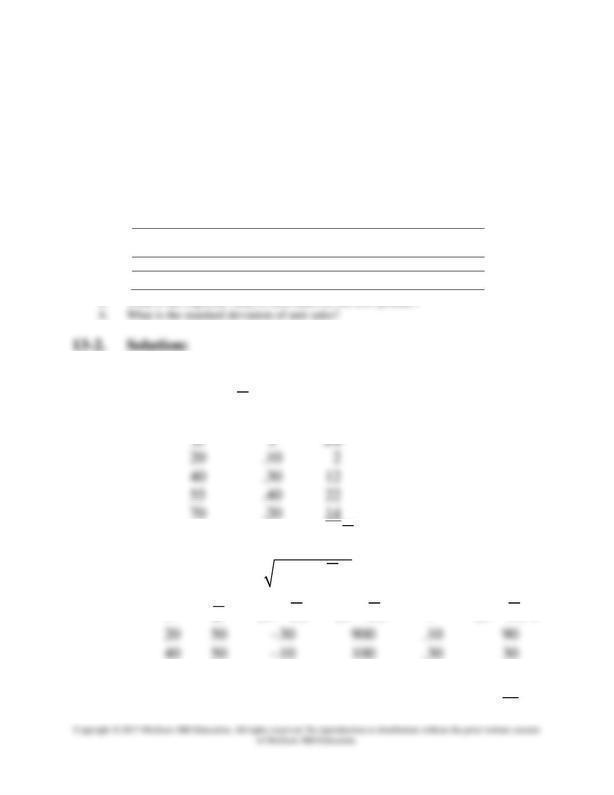

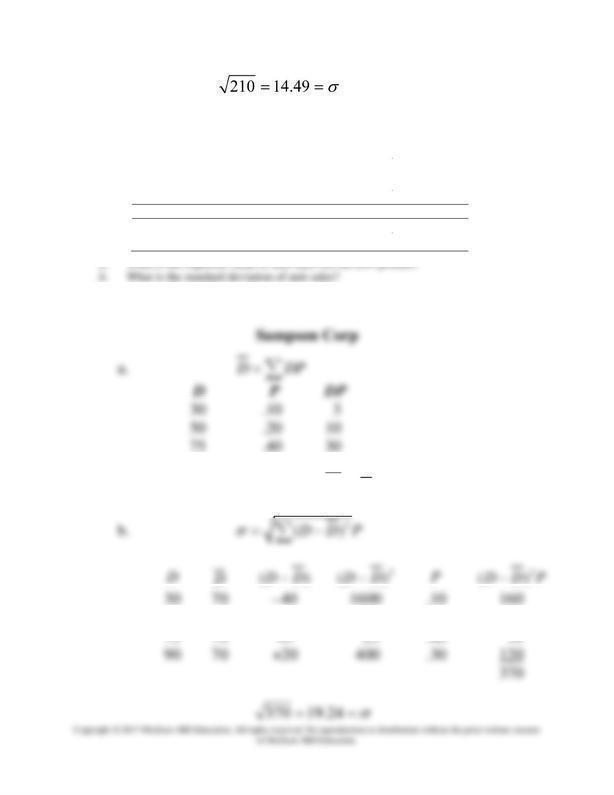

3. Expected value and standard deviation (LO13-1) Sampson Corp. is evaluating the

introduction of a new product. The possible levels of unit sales and the probabilities of their

occurrence are given.

Possible

Market Reaction

Sales

in Units

Probabilities

Low response ............................................

30

.10

Moderate response ....................................

50

.20

High response ..........................................

75

.40

Very high response ..................................

90

.30

13-3. Solution:

90 .30 27

70 =

D

D

P

50

70

–20

400

.20

80

Chapter 13: Risk and Capital Budgeting

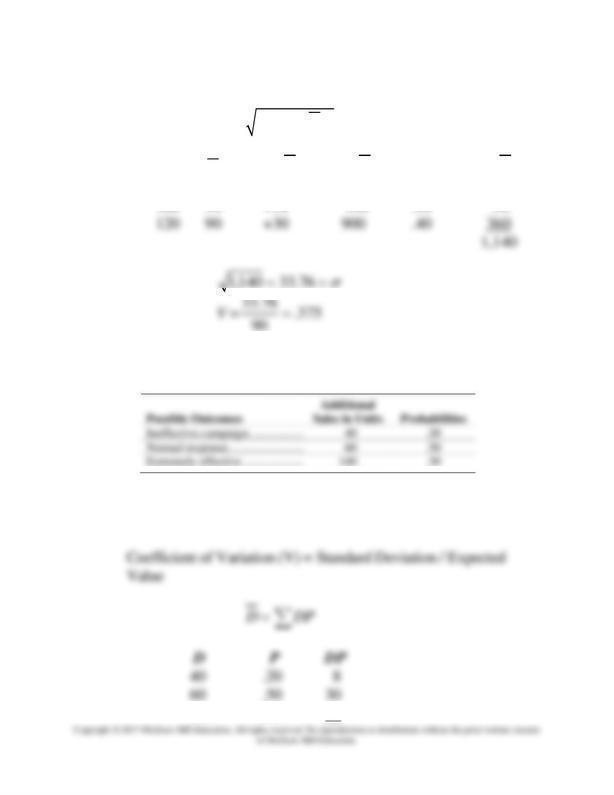

4. Coefficient of variation (LO13-1) Shack Homebuilders Limited is evaluating a new

promotional campaign that could increase home sales. Possible outcomes and probabilities

of the outcomes are shown next. Compute the coefficient of variation.

Shack Homebuilders Limited

Coefficient of Variation (V) = Standard Deviation / Expected

Value

D DP=

90=

D

Chapter 13: Risk and Capital Budgeting

2

()D D P

=−

D

D

()DD−

2

()DD−

P

2

()DD−

P

40

90

–50

2,500

.30

750

5. Coefficient of variation (LO13-1) Al Bundy is evaluating a new advertising program that

could increase shoe sales. Possible outcomes and probabilities of the outcomes are shown

next. Compute the coefficient of variation.

13-5. Solution:

Al Bundy

140 .30 42

Chapter 13: Risk and Capital Budgeting

D

P

6. Coefficient of variation (LO13-1) Possible outcomes for three investment alternatives and

their probabilities of occurrence are given next.

Alternative 1

Alternative 2

Alternative 3

Chapter 13: Risk and Capital Budgeting

135

0.4

54

225

0.4

90

380

0.2

76

225

174

+51

2,601

.4

1040.40

$3,234.00

D

Chapter 13: Risk and Capital Budgeting

380

224

+156

24,336

.2

4,867.20

$8,244.00

7. Coefficient of variation (LO1) Five investment alternatives have the following returns and

standard deviations of returns:

Returns—

Standard

13-7. Solution:

Chapter 13: Risk and Capital Budgeting

Coefficient of variation (V) = Standard deviation/Mean return

8. Coefficient of variation (LO13-1) Five investment alternatives have the following returns

and standard deviations of returns:

Returns:

Standard

13-8. Solution:

Chapter 13: Risk and Capital Budgeting

9. Coefficient of variation and time (LO13-1) Digital Technology wishes to determine its

coefficient of variation as a company over time. The firm projects the following data (in

millions of dollars):

Year

Profits:

Expected Value

Standard Deviation

1 ......................................

$180

$62

3 ......................................

240

104

6 ......................................

300

166

9 ......................................

400

292

a. Compute the coefficient of variation (V) for each time period.

Digital Technology

a.

Year

Profits:

Expected Value

Standard

Deviation

Coefficient

of Variation

1

180

62

.34

3

240

104

.43

6

300

166

.55

9

400

292

.73

b. Yes, the risk appears to be increasing over time. This may

be related to the inability to make forecasts far into the

future. There is more uncertainty.

10. Risk-averse (LO13-2) Tim Trepid is highly risk-averse, while Mike Macho actually

enjoys taking a risk.

Chapter 13: Risk and Capital Budgeting

Coefficient of Variation (V) = Standard Deviation / Expected

Value

Buy Stocks $6,140/9,140 = .672

Buy Bonds $2,560/7,680 = .333

Buy Commodity Futures $26,700/19,100 = 1.398

Buy Options $18,200/17,700 = 1.028

a. Tim should buy the bonds because bonds have the lowest

coefficient of variation.

b. Mike should buy the commodity futures because they have

the highest coefficient of variation.

11. Risk-averse (LO13-2) Mountain Ski Corp. was set up to take large risks and is willing to

take the greatest risk possible. Lakeway Train Co. is more typical of the average

corporation and is risk-averse.

a. Which of the following four projects should Mountain Ski Corp. choose? Compute

the coefficients of variation to help you make your decision.

b. Which one of the four projects should Lakeway Train Co. choose based on the same

criteria of using the coefficient of variation?

Chapter 13: Risk and Capital Budgeting

13-11. Solution:

Mountain Ski Corp. and Lakeway Train Co.

Coefficient of Variation (V) = Standard Deviation / Expected

Value

12. Coefficient of variation and investment decision (LO13-1) Kyle’s Shoe Stores Inc. is

considering opening an additional suburban outlet. An aftertax expected cash flow of $130

per week is anticipated from two stores that are being evaluated. Both stores have positive

net present values.

13-12. Solution:

Kyle’s Shoe Stores Inc.

Standard Deviations of Sites A and B

Chapter 13: Risk and Capital Budgeting

130

130

–0–

–0–

.3

–0–

160

130

+30

900

.1

90

170

130

+40

1,600

.3

480

$1,320

130

130

–0–

–0–

.3

–0–

VB = $65.08/$130 = .5006

Site A is the preferred site since it has the smallest coefficient of

Chapter 13: Risk and Capital Budgeting

5 ......................

30,000

The coefficient of variation for the project is .847.

Based on the following table of risk-adjusted discount rates, should the project be

undertaken? Select the appropriate discount rate and then compute the net present value.

Waste Industries

Year

Inflows

PVIF @ 14%

PV

1

$11,000

.877

$ 9,647

2

16,000

.769

12,304

3

21,000

.675

14,175

4

24,000

.592

14,208

5

30,000

.519

15,570

PV of Inflows

$65,904

Investment

70,000

NPV

$(4,096)

Based on the negative net present value, the project should not

be undertaken.

Calculator solution:

Find the PV of cash inflow using a financial calculator at 14 percent:

Chapter 13: Risk and Capital Budgeting

Press the following keys: 2nd, CF, 2nd, Clear.

Calculator displays CFo, enter 70,000 and press +|–, press the Enter key.

Press down arrow, enter 11,000, and press Enter.

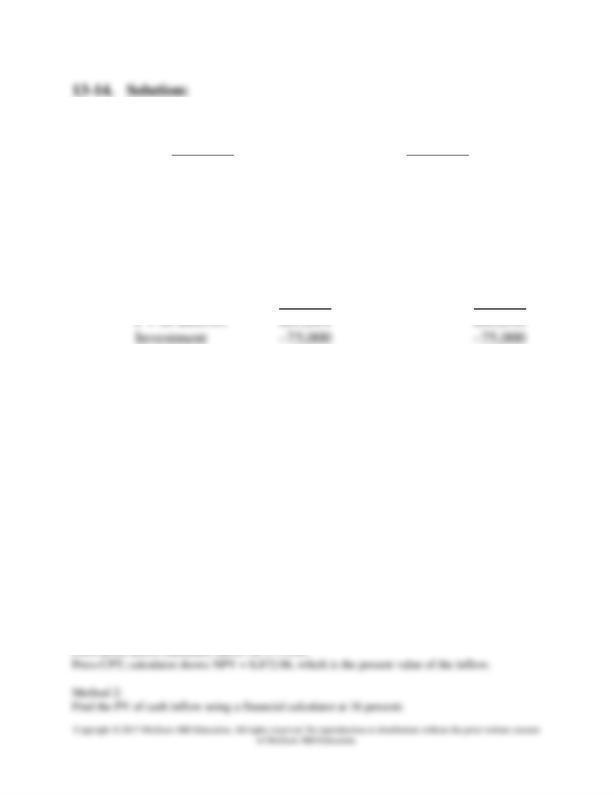

14. Risk-adjusted discount rate (LO13-3) Dixie Dynamite Company is evaluating two

methods of blowing up old buildings for commercial purposes over the next five years.

Method one (implosion) is relatively low in risk for this business and will carry a 12

percent discount rate. Method two (explosion) is less expensive to perform but more

dangerous and will call for a higher discount rate of 16 percent. Either method will require

an initial capital outlay of $75,000. The inflows from projected business over the next five

years are given next. Which method should be selected using net present value analysis?

Chapter 13: Risk and Capital Budgeting

Dixie Dynamite Co.

Method 1 Method 2

Year

Inflows

PVIF

@

12%

PV

Inflows

PVIF

@

16%

PV

1

$18,000

.893

$16,074

$20,000

.862

$17,240

2

24,000

.797

19,128

25,000

.743

18,575

3

34,000

.712

24,208

35,000

.641

22,435

4

26,000

.636

16,536

28,000

.552

15,456

5

14,000

.597

7,938

15,000

.476

7,140

NPV

$ 8,884

$ 5,846

Select Method 1

Calculator solution:

Method 1:

Find the PV of cash inflow using a financial calculator at 12 percent:

Press the following keys: 2nd, CF, 2nd, Clear.

Calculator displays CFo, enter 75,000 and press +|–, press the Enter key.

Press down arrow, enter 18,000, and press Enter.

Press down arrow, enter 1, and press Enter.

Press down arrow, enter 24,000, and press Enter.

Press down arrow, enter 1, and press Enter.

Press down arrow, enter 34,000, and press Enter.

Press down arrow, enter 1, and press Enter.

Press down arrow, enter 26,000, and press Enter.

Press down arrow, enter 1, and press Enter.

Press down arrow, enter 14,000, and press Enter.

Press down arrow, enter 1, and press Enter.

Press NPV; calculator shows I = 0; enter 12 and press Enter.

Chapter 13: Risk and Capital Budgeting

15. Discount rate and timing (LO13-1) Fill in the following table from Appendix B. Does a

high discount rate have a greater or lesser effect on long-term inflows compared to recent

ones?

Discount Rate

Years

5%

20%

1

.952

.833

10

.614

.162

20

.377

.026

The impact of a high discount rate is much greater on long-term

value. For example, after the first year, the high rate discount

value produces an answer that is 87.5 percent of the low

Chapter 13: Risk and Capital Budgeting

discount rate (.833/.952). However, after the 20th year, the high

rate discount rate is only 6.90 percent of the low discount rate

(.026/.377).

16. Expected value with net present value (LO13-1) Debby’s Dance Studios is considering

the purchase of new sound equipment that will enhance the popularity of its aerobics

9,930..............

.2

Debby’s Dance Studios

a. Expected Cash Flow

Cash Flow P

$4,570

×

.1

$ 457

5,550

×

.3

1,665

7,400

×

.4

2,960

9,930

×

.2

1,986

$7,068

b. Net Present Value (Appendix D)

$7,068 × 3.352 (PVIFA @ 15%, n = 5) =

Chapter 13: Risk and Capital Budgeting

$23,692 Present Value of Inflows

27,900 Present Value of Outflows

$(4,208) Net Present Value

c. Debby should not buy this new equipment because the net

present value is negative.

Calculator solution:

b.

Find the PV of cash inflow using a financial calculator at 15 percent:

17. Deferred cash flows and risk-adjusted discount rate Highland Mining and Minerals Co.

is considering the purchase of two gold mines. Only one investment will be made. The

Australian gold mine will cost $1,649,000 and will produce $353,000 per year in years 5

through 15 and $503,000 per year in years 16 through 25. The U.S. gold mine will cost

$2,054,000 and will produce $282,000 per year for the next 25 years. The cost of capital is

13 percent.

Highland Mining and Minerals Co.

a. Calculate the net present value for each project.

The Australian Mine

Chapter 13: Risk and Capital Budgeting

Years

Cash

Flow

n Factor

PVIFA@13%

Present

Value

16–25

$503,000

(25 – 15)

(7.330 – 6.462)

$ 436,604

Present Value of Inflows $1,667,868

1–25

$282,000

(25)

7.330

$2,067,060

Present Value of Inflows $2,067,060

Present Value of Outflows $2,054,000

Net Present Value $ 13,060

16–25

$503,000

(25 – 15)

(6.464 – 5.847)

$ 310,351

Chapter 13: Risk and Capital Budgeting

Net Present Value $ (282,473)

Now the decision should be made to reject the purchase of the

Australian Mine and purchase the U.S. Mine.

18. Coefficient of variation and investment decision (LO13-1) Mr. Sam Golff desires to

invest a portion of his assets in rental property. He has narrowed his choices down to two

Mr. Sam Golff

D DP=

Palmer Heights

Crenshaw Village

Chapter 13: Risk and Capital Budgeting

Expected Cash

Flow

$90.0

(thousands)

Expected Cash

Flow

$85.0

(thousands)

75

90

–15

225

.20

45

90

90

0

0

.20

0

105

90

+15

225

.20

45

D

P

$60.0

Chapter 13: Risk and Capital Budgeting

b. Based on the coefficient of variation, Palmer Heights has

more risk (.176 versus .091).

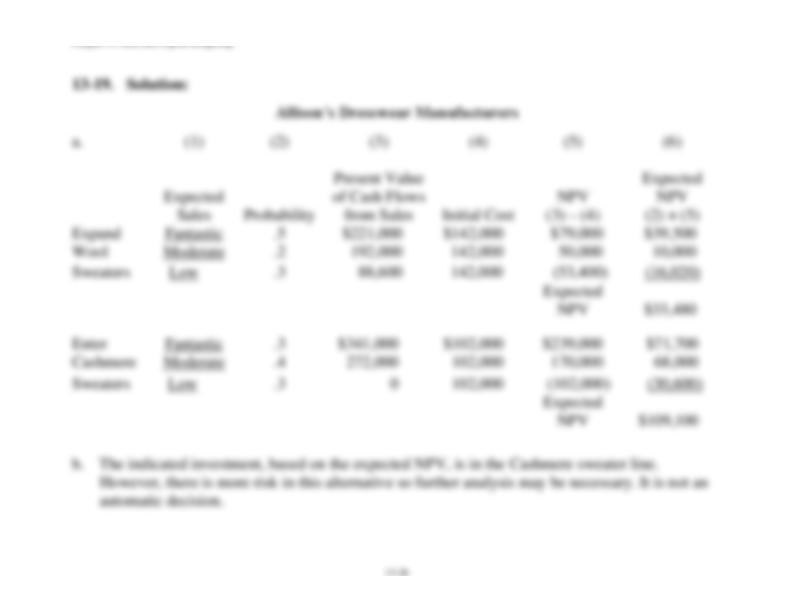

19. Decision-tree analysis (LO13-4) Allison’s Dresswear Manufacturers is preparing a

strategy for the fall season. One alternative is to expand its traditional ensemble of wool

sweaters. A second option would be to enter the cashmere sweater market with a new line

of high-quality designer label products. The marketing department has determined that the

wool and cashmere sweater lines offer the following probability of outcomes and related

cash flows:

Expand Wool

Sweaters Line

Enter Cashmere

Sweaters Line

Expected

Sales

Probability

Present Value

of Cash Flows

from Sales

Probability

Present

Value of

Cash Flows

from Sales

Fantastic ....................

.5

$221,000

.3

$341,000

Moderate ...................

.2

192,000

.4

272,000

Low ...........................

.3

88,600

.3

0

The initial cost to expand the wool sweater line is $142,000. To enter the cashmere sweater

line, the initial cost in designs, inventory, and equipment is $102,000.

a. Diagram a complete decision tree of possible outcomes similar to Figure 13-8. Note

that you are dealing with thousands of dollars rather than millions. Take the analysis

all the way through the process of computing expected NPV (the last column for each

investment).

b. Given the analysis in part a, would you automatically make the investment indicated?

Chapter 13: Risk and Capital Budgeting

Chapter 13: Risk and Capital Budgeting

Chapter 13: Risk and Capital Budgeting

Chapter 13: Risk and Capital Budgeting

Chapter 13: Risk and Capital Budgeting

Chapter 13: Risk and Capital Budgeting

Chapter 13: Risk and Capital Budgeting

Chapter 13: Risk and Capital Budgeting

Chapter 13: Risk and Capital Budgeting

Chapter 13: Risk and Capital Budgeting

Chapter 13: Risk and Capital Budgeting

Chapter 13: Risk and Capital Budgeting

Chapter 13: Risk and Capital Budgeting

Chapter 13: Risk and Capital Budgeting

Chapter 13: Risk and Capital Budgeting

Chapter 13: Risk and Capital Budgeting

Chapter 13: Risk and Capital Budgeting

Chapter 13: Risk and Capital Budgeting

Chapter 13: Risk and Capital Budgeting

Chapter 13: Risk and Capital Budgeting