Chapter 12: The Capital Budgeting Decision

Chapter 12

The Capital Budgeting Decision

Discussion Questions

12-1.

What are the important administrative considerations in the capital budgeting

process?

12-2.

Why does capital budgeting rely on analysis of cash flows rather than on net

income?

12-3.

What are the weaknesses of the payback method?

12-4.

What is normally used as the discount rate in the net present value method?

12-5.

What does the term mutually exclusive investments mean?

12-6.

How does the modified internal rate of return include concepts from both the

traditional internal rate of return and the net present value methods?

Chapter 12: The Capital Budgeting Decision

12-7.

If a corporation has projects that will earn more than the cost of capital, should

it ration capital?

12-8.

What is the net present value profile? What three points should be determined

to graph the profile?

12-9.

How does an asset’s ADR (asset depreciation range) relate to its MACRS

category?

Chapter 12

Problems

1. Cash flow (LO12-2) Assume a corporation has earnings before depreciation and taxes of

$90,000, depreciation of $40,000, and a 30 percent tax bracket. Compute its cash flow using the

following format:

Earnings before depreciation and taxes _____

Chapter 12: The Capital Budgeting Decision

Earnings before depreciation and taxes $90,000

Depreciation –40,000

Earnings before taxes 50,000

Taxes @ 30% –15,000

Earnings after taxes $35,000

Depreciation +40,000

Cash flow $75,000

2. Cash flow (LO12-2) Assume a corporation has earnings before depreciation and

taxes of $100,000, depreciation of $40,000, and that it has a 40 percent tax bracket.

a. Compute its cash flow using the following format:

Earnings before depreciation and taxes _____

Depreciation _____

Earnings before taxes _____

Taxes @ 40% _____

Earnings after taxes _____

Depreciation _____

b. Compute the cash flow for the company if depreciation is only $20,000.

c How much cash flow is lost due to the reduced depreciation from $40,000 to

$20,000?

a. Earnings before depreciation and taxes $100,000

Depreciation – 40,000

Earnings before taxes 60,000

Chapter 12: The Capital Budgeting Decision

Taxes @ 40% 24,000

Earnings after taxes 36,000

Depreciation + 40,000

Cash flow $ 76,000

12-3. Solution:

a. Earnings before depreciation and taxes $200,000

Depreciation – 0

Earnings before taxes 200,000

Taxes @ 40% – 80,000

Earnings after taxes 120,000

Chapter 12: The Capital Budgeting Decision

Depreciation – 0

Cash flow $120,000

12-4. Solution:

a. Earnings before depreciation and taxes $440,000

Depreciation 140,000

Earnings before taxes 300,000

Taxes @ 35% 105,000

Earnings after taxes 195,000

Chapter 12: The Capital Budgeting Decision

5. Cash flow versus earnings (LO12-2) Al Quick, the president of a New York Stock

Exchange —listed firm, is very short-term oriented and interested in the immediate

consequences of his decisions. Assume a project that will provide an increase of $2 million

in cash flow because of favorable tax consequences, but carries a two-cent decline in

earnings per share because of a write-off against first-quarter earnings. What decision

might Mr. Quick make?

12-5. Solution:

Al Quick

6. Payback method (LO12-3) Assume a $250,000 investment and the following cash flows

for two products:

Year

Product X

Product Y

1

$90,000

$50,000

2

90,000

80,000

3

60,000

60,000

4

20,000

70,000

Which alternatives would you select under the payback method?

12-6. Solution:

Chapter 12: The Capital Budgeting Decision

Payback for Product X Payback for Product Y

7. Payback method (LO12-3) Assume a $40,000 investment and the following cash flows for

two alternatives.

Year

Investment X

Investment Y

1

$ 6,000

$15,000

2

8,000

20,000

3

9,000

10,000

4

17,000

—

5

20,000

—

Which of the alternatives would you select under the payback method?

12-7. Solution:

Payback for Investment X Payback for Investment Y

$40,000–$6,000 1 year $40,000–$15,000 1 year

34,000–8,000 2 years 25,000–20,000 2 years

Chapter 12: The Capital Budgeting Decision

5 .................

25,000

—

a. Calculate the payback for investment A and B.

b. If the inflow in the fifth year for Investment A was $25,000,000 instead of $25,000,

would your answer change under the payback method?

a. Payback for Investment A Payback for Investment B

$90,000 – $25,000 1 year $90,000 – $40,000 1 year

65,000 – 30,000 2 years 50,000 – 40,000 2 years

35,000 – 25,000 3 years 10,000/28,000 .36 years

10,000/19,000 0.53 years

Payback Investment A = 3.53 years

Payback Investment B = 2.36 years

Investment B would be selected because of the faster payback.

b. The $25,000,000 inflow would still leave the payback period for

Investment A at 3.53 years. It would remain inferior to Investment

B under the payback method.

Chapter 12: The Capital Budgeting Decision

4–10.............

10,000

10,000

a. Using the payback method, what will the decision be?

12-9. Solution:

Short-Line Railroad

a.

Payback for Electric Co. Payback for Water Works

$140,000 – $85,000 1 year $140,000 – $30,000 1 year

55,000 – 25,000 2 years 110,000 – 25,000 2 years

30,000 – 30,000 3 years 85,000 – 85,000 3 years

Chapter 12: The Capital Budgeting Decision

3 ....................

6,000

16,000

12-10. Solution:

X-treme Vitamin Company

a. Payback Method

Payback for Project A

10,000 .83 years

12,000 =

Payback for Project B

10,000 1 year

10,000 =

Chapter 12: The Capital Budgeting Decision

Year Cash Flow PVIFA Present Value

1 $10,000 .909 $ 9,090

2 $ 6,000 .826 $ 4,956

3 $16,000 .751 $12,016

Present value of inflows $26,062

Present value of outflows 10,000

Net present value $16,062

Under the net present value method, you should select

Project B because of the higher net present value.

c. A company should normally have more confidence in answer

b because the net present value considers all inflows as well

as the time value of money. The heavy late inflow for Project

B was partially ignored under the payback method.

Calculator Solution:

(b-1)

Project A using a financial calculator:

Use the NPV keys by pressing and entering the following:

Press the following keys: 2nd, CF, 2nd, Clear.

Calculator displays CFo, 10,000 +|– key, press the Enter key.

Press down arrow, enter 12,000, and press Enter.

Press down arrow, enter 1, and press Enter.

Press down arrow, enter 8,000, and press Enter.

Press down arrow, enter 1, and press Enter.

Press down arrow, enter 6,000, and press Enter.

Press down arrow, enter 1, and press Enter.

Press NPV; calculator shows I = 0; enter 10 and press Enter.

Chapter 12: The Capital Budgeting Decision

11. Internal rate of return (LO12-4) You buy a new piece of equipment for $16,230, and you

receive a cash inflow of $2,500 per year for 12 years. What is the internal rate of return?

Appendix D

IFA $16,230

$2,500

==

IRR = 11%

For n = 12, we find 6.492 under the 11% column.

Calculator Solution:

Using a financial calculator,

12. Internal rate of return (LO12-4) King’s Department Store is contemplating the purchase

Chapter 12: The Capital Budgeting Decision

King’s Department Store

Appendix D

PVIFA = $22,802/$3,500 = 6.515

IRR = 7%

For n = 9, we find 6.515 under the 7% column.

The machine should not be purchased since its return is less

than the 10 percent cost of capital.

Calculator Solution:

(a)

3 .........................

18,000

a. Determine the internal rate of return.

b. With a cost of capital of 18 percent, should the machine be purchased?

Home Security Systems

Chapter 12: The Capital Budgeting Decision

a. Step 1 Average the inflows.

$25,000

23,000

18,000

$66,000 / 3 $22, 000=

Step 2 Divide the inflows by the assumed annuity in Step 1.

Investment $50,000 2.273

Annuity 22,000

==

Chapter 12: The Capital Budgeting Decision

12-13. (Continued)

Year Cash Flow PVIF at 17% Present Value

–49,420 ........... PV @ 17% –50,000............. Cost

$ 757 $ 177

16% + ($177/$757) (1%)

14% + .234 (1%) = 16.23% IRR

The IRR is 16.23%

Chapter 12: The Capital Budgeting Decision

$50,177 ........... PV @ 16% $50,177............. PV @ 16%

$ 1,526 $ 177

16% + ($177/$1,526) (2%)

16% + (.12)(2%) = 16.24%

This answer is very close to the previous answer, the

difference is due to rounding and that the differences

between the numbers in the table are not linear.

b. Since the IRR of 16.23 percent (or 16.24 percent) is less than

the cost of capital of 18 percent, the project should not be

accepted.

Calculator Solution:

Alternatively, use a financial calculator as follows to obtain the correct answer rather than

an approximation.

Press the following keys: 2nd, CF, 2nd, Clear.

14. Net present value method (LO12-4) Aerospace Dynamics will invest $110,000 in a

project that will produce the following cash flows. The cost of capital is 11 percent. Should

the project be undertaken? (Note that the fourth year’s cash flow is negative.)

Chapter 12: The Capital Budgeting Decision

Aerospace Dynamics

Year Cash Flow PVIF at 11% Present Value

1 $36,000 .901 $ 32,436

2 44,000 .812 35,728

3 38,000 .731 27,778

4 (44,000) .659 (28,996)

5 81,000 .593 48,033

Present Value of Inflows $114,979

Present Value of Outflows 110,000

Net Present Value $ 4,979

The net present value is positive and the project should be

undertaken.

Calculator Solution:

Using a financial calculator,

Press the following keys: 2nd, CF, 2nd, Clear.

Calculator displays CFo, 110,000 +|– key, press Enter.

Press down arrow, enter 36,000, and press Enter.

Press down arrow, enter 1, and press Enter.

Press down arrow, enter 44,000, and press Enter.

Chapter 12: The Capital Budgeting Decision

3.................

40,000

The firm will also be required to spend $10,000 to close down the project at the end of the

three years. If the cost of capital is 10 percent, should the investment be undertaken?

12-15. Solution:

Horizon Company

Present Value of Inflows

Year Cash Flow × PVIF at 10% Present Value

1 $15,000 .909 $13,635

2 25,000 .826 20,650

3 40,000 .751 30,040

$64,325

Chapter 12: The Capital Budgeting Decision

Note, the $10,000 outflow could have been subtracted out of

the $40,000 inflow in the third year and the same answer

would result.

Calculator Solution:

Using a financial calculator,

Press the following keys: 2nd, CF, 2nd, Clear.

Calculator displays CFo, 60,000 +|– key, press the Enter key

Press down arrow, enter 15,000, and press Enter.

16. Net present value method (LO12-4) Skyline Corp. will invest $130,000 in a project that

will not begin to produce returns until after the 3rd year. From the end of the 3rd year until

the end of the 12th year (10 periods), the annual cash flow will be $34,000. If the cost of

capital is 12 percent, should this project be undertaken?

Skyline Corporation

Present Value of Inflows

Find the present value of a deferred annuity

A = $34,000, n = 10, i = 12%

PVA = A × PVIFA (Appendix D)

PVA = $34,000 × 5.650 = $192,100

Chapter 12: The Capital Budgeting Decision

Discount from beginning of the third period (end of second

period to present):

FV = $192,100, n = 2, i = 12%

PV = FV × PVIF (Appendix B)

PV = $192,100 × .797 = $153,104

Present Value of Inflows $153,104

Present Value of Outflows 130,000

Net Present Value $ 23,104

The net present value is positive and the project should be

undertaken.

Calculator Solution:

Using a financial calculator,

Press the following keys: 2nd, CF, 2nd, Clear.

3 .................

4,000

a. What is the net present value at an 8 percent discount rate?

Chapter 12: The Capital Budgeting Decision

12-17. Solution:

Hudson Corporation

a. Net Present Value

Year Cash Flow × 8% PVIF Present Value

1 $13,000 .926 $ 12,038

2 13,000 .857 11,141

3 4,000 .794 3,176

12-17. (Continued)

We divide the investment by the assumed annuity value.

IFA

$24,000 2.400 PV

10,000 =

Using Appendix D for n = 3, the first approximation appears

to fall between 12 percent and 14 percent. Since the heavy

inflows are in the early years, we will try 14 percent.

Chapter 12: The Capital Budgeting Decision

Year Cash Flow × 14% PVIF Present Value

1 $13,000 .877 $ 11,401

2 13,000 .769 9,997

3 4,000 .675 2,700

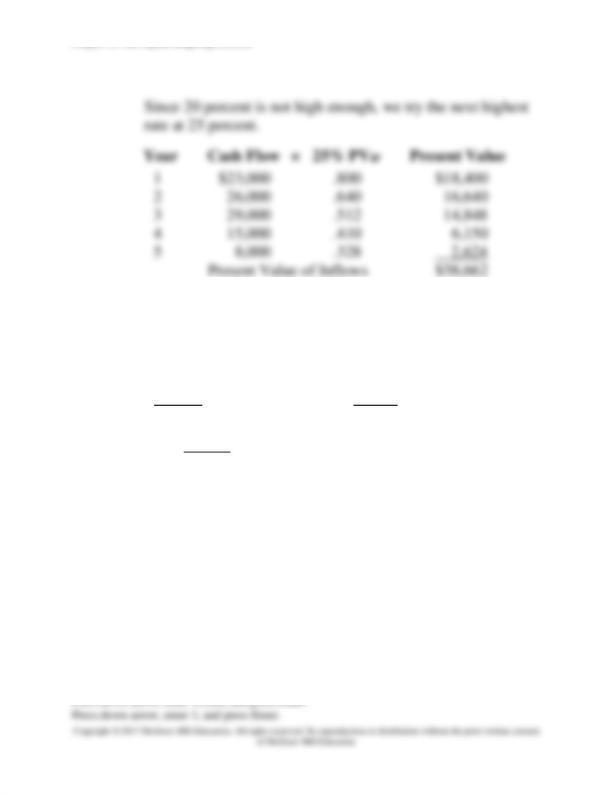

Present Value of Inflows $24,098

Since 14 percent is not high enough to get $24,000 as the

present value, we will try 16 percent. (We could have only

gone up to 15 percent, but we wanted to be sure to include

$24,000 in this calculation. Of course, students who use 15

percent are doing fine.)

Chapter 12: The Capital Budgeting Decision

The correct answer falls between 14 percent and 15 percent.

We interpolate.

$24,098 PV @ 14% $24,098 PV @ 14%

23,770 PV @ 15% 24,000 Cost

328 $ 98

$98

14% (1%) 14% .30 (1%) 14% .30% 14.30%

$328

+ = + = + =

c. Yes. Both the NPV is greater than 0 and the IRR is greater

than the cost of capital.

Calculator Solution:

(a)

Press the following keys: 2nd, CF, 2nd, and Clear.

Calculator displays CFo, 24,000 +|– key, press Enter.

Press down arrow, enter 13,000, and press Enter.

Press down arrow, enter 2, and press Enter.

Press down arrow, enter 4,000, and press Enter.

Press down arrow, enter 1, and press Enter.

18. Net present value and internal rate of return methods (LO12-4) The Pan American

Bottling Co. is considering the purchase of a new machine that would increase the speed of

Chapter 12: The Capital Budgeting Decision

5 ...........

8,000

12-18. Solution:

Pan American Bottling Co.

a. Net Present Value

Year Cash Flow × 13% PVIF Present Value

12-18. (Continued)

b. Internal Rate of Return

We will average the inflows to arrive at an assumed annuity.

$23,000

26,000

Chapter 12: The Capital Budgeting Decision

29,000

15,000

8,000

$101,000/5 = $20,200

We divide the investment by the assumed annuity value.

IFA

$60,000 2.97 PV

$20,200 =

Chapter 12: The Capital Budgeting Decision

12-18. (Continued)

The correct answer must fall between 20 and 25 percent. We

interpolate.

$64,440 ........... PV @ 20% $64,440............. PV @ 20%

58,662 ............ PV @ 25% 60,000............. Cost

$ 5,778 $ 4,440

$4,440

20% (5%) 20% .77 (5%) 20% 3.85% 23.85%

$5,778

+ = + = + =

c. The project should be accepted because the net present value

is positive and the IRR exceeds the cost of capital.

Calculator Solution:

Find the NPV using a financial calculator:

Press the following keys: 2nd, CF, 2nd, Clear.

Calculator displays CFo, 60,000 +|– key, press Enter.

Press down arrow, enter 23,000, and press Enter.

Press down arrow, enter 1, and press Enter.

Press down arrow, enter 26,000, and press Enter.

Press down arrow, enter 1, and press Enter.

Press down arrow, enter 29,000, and press Enter.

Press down arrow, enter 1, and press Enter.

Chapter 12: The Capital Budgeting Decision

19. Use of profitability index (LO12-4) You are asked to evaluate the following two projects

for the Norton Corporation. Using the net present value method combined with the

profitability index approach described in footnote 2 of this chapter, which project would

you select? Use a discount rate of 14 percent.

Chapter 12: The Capital Budgeting Decision

12-19. Solution:

Norton Corporation

NPV for Project X

Year Cash Flow × PVIF at 14% Present Value

1 $10,000 .877 $ 8,770

2 8,000 .769 6,152

3 9,000 .675 6,075

4 8,600 .592 5,091

Present Value of Inflows $26,088

Present Value of Outflows (Cost) –20,000

Net Present Value $ 6,088

Chapter 12: The Capital Budgeting Decision

Present value of inflows

Profitability index ( ) Present value of outflows

$46,459 1.16

$40,000

Y=

==

You should select Project X because it has the higher

profitability index. This is true in spite of the fact that it has a

lower net present value. The profitability index may be

appropriate when you have different size investments.

Calculator Solution:

(a)

Find NPV using a financial calculator:

Press the following keys: 2nd, CF, 2nd, Clear.

Calculator displays CFo, 20,000 +|– key, press the Enter key.

Press down arrow, enter 10,000, and press Enter.

Press down arrow, enter 1, and press Enter.

Press down arrow, enter 8,000, and press Enter.

Press down arrow, enter 1, and press Enter.

Press down arrow, enter 9,000, and press Enter.

Press down arrow, enter 1, and press Enter.

Press down arrow, enter 8,600, and press Enter.

Press down arrow, enter 1, and press Enter.

Press NPV; the calculator shows I = 0; enter 14 and press Enter.

Press down arrow; calculator shows NPV = 0.00.

Press CPT; calculator shows NPV = 6,094.30, which is the net present value of Project X.

Profitability index using a financial calculator:

Profitability Index = Present Value of Inflows / Present Value of Outflows

Present Value of Inflows = NPV + Outflows

Chapter 12: The Capital Budgeting Decision

5 .................

29,000

The internal rate of return is 11 percent.

Turner Video

a. Reinvestment assumption of NPV

No. of Future

Year Inflows Rate Periods Value Factor Value

1 $15,000 12% 4 1.574 $23,610

2 17,000 12% 3 1.405 23,885

Chapter 12: The Capital Budgeting Decision

3 21,000 12% 2 1.254 26,334

4 25,000 12% 1 1.120 28,000

5 29,000 – 0 1.000 29,000

$130,829

b. Reinvestment assumption of IRR

No. of Future

Year Inflows Rate Periods Value Factor Value

1 $15,000 11% 4 1.518 $ 22,770

2 17,000 11% 3 1.368 23,256

3 21,000 11% 2 1.232 25,872

4 25,000 11% 1 1.110 27,750

5 29,000 – 0 1.000 29,000

$128,648

c. No. However, for investments with a very high IRR, it may

be unrealistic to assume that reinvestment can take place at

an equally high rate. The net present value method makes the

more conservative assumption of reinvestment at the cost of

capital.

(a)

Calculator Solution:

Find PV of cash inflow using a financial calculator at 12 percent:

Press the following keys: 2nd, CF, 2nd, Clear.

Calculator displays CFo, 0, press the Enter key.

Press down arrow, enter 15,000, and press Enter.

Press down arrow, enter 1, and press Enter.

Press down arrow, enter 17,000, and press Enter.

Press down arrow, enter 1, and press Enter.

Press down arrow, enter 21,000, and press Enter.

Chapter 12: The Capital Budgeting Decision

3 ............

9,000

Chapter 12: The Capital Budgeting Decision

12-21. Solution:

Caffeine Coffee Company

Terminal Value (end of year 3)

a. FV Factor

Period of (11%) Future

Growth (Appendix A) Value

Year 1 $12,000 2 1.232 $14,784

Year 2 11,000 1 1.110 12,210

Year 3 9,000 0 1.000 9,000

Terminal Value $35,994

To determine the modified internal rate of return, calculate

the yield on the investment.

IF PV

PV (Appendix B)

FV

$26,000

= .722

35,994

==

=

Use Appendix B for three periods, the answer is

approximately 11 percent (.731).

b. The answer is lower than 17.5 percent under the Modified

IRR because inflows are reinvested at the cost of capital of

11 percent. Under the traditional IRR, inflows are reinvested

at the internal rate of return of 17.5 percent, which leads to

a higher terminal value.

Calculator Solution:

Chapter 12: The Capital Budgeting Decision

Using a financial calculator:

Find the PV of cash inflow using a financial calculator at 11 percent:

Press the following keys: 2nd, CF, 2nd, Clear.

Calculator displays CFo, 0, press the Enter key.

Press down arrow, enter 12,000, and press Enter.

Press down arrow, enter 1, and press Enter.

Press down arrow, enter 11,000, and press Enter.

Press down arrow, enter 1, and press Enter.

Press down arrow, enter 9,000, and press Enter.

Press down arrow, enter 1, and press Enter.

Press NPV; calculator shows I = 0; enter 11 and press Enter.

Press down arrow; calculator shows NPV = 0.00.

Press CPT; calculator shows NPV = 26,319.38, which is the present value of the inflow.

Next find the FV of the 26,319.38 as of year 3 at an 11 percent annual rate.

(a)

N

I/Y

PV

PMT

FV

3

11

26,319.38

0

CPT FV 35,995.20

3

CPT I I/Y 11.45

26,000

0

–35,995.20

22. Capital rationing and mutually exclusive investments (LO12-4) The Suboptimal Glass

Company uses a process of capital rationing in its decision making. The firm’s cost of

capital is 10 percent. It will only invest $77,000 this year. It has determined the internal

rate of return for each of the following projects.

Project

Project Size

Internal Rate of

Return

A .....................

$10,500

21%

B .....................

30,500

22

C .....................

25,500

18

D .....................

10,500

13

E .....................

10,500

20

F ......................

20,500

11

G .....................

10,500

16

a. Select the projects that the firm should accept.

Chapter 12: The Capital Budgeting Decision

b. If Projects A and B are mutually exclusive, how would that affect your overall

answer? That is, which projects would you accept in spending the $77,000?

12-22. Solution:

Suboptimal Glass Company

You should rank the investments in terms of IRR.

Project IRR Project Size Total Budget

B 22% $30,500 $ 30,500

A 21 10,500 41,000

E 20 10,500 51,500

C 18 25,500 77,000

23. Net present value profile (LO12-4) Keller Construction is considering two new

investments. Project E calls for the purchase of earthmoving equipment. Project H

represents an investment in a hydraulic lift. Keller wishes to use a net present value profile

in comparing the projects. The investment and cash flow patterns are as follows:

Chapter 12: The Capital Budgeting Decision

4 ...........................

10,000

a. Determine the net present value of the projects based on a zero discount rate.

b. Determine the net present value of the projects based on a 9 percent discount rate.

c. The internal rate of return on Project E is 13.25 percent, and the internal rate of return

Keller Construction Company

a. Zero discount rate

Project E

Inflows Outflow

8,000 = ($5,000 + $6,000 + $7,000 + $10,000) – $20,000

Project H

Inflows Outflow

$ 5,000 = ($16,000 + $5,000 + $4,000) – $20,000

Chapter 12: The Capital Budgeting Decision

b. 9 percent discount rate

Project E

12-23. (Continued)

Project H

Year Cash Flow PVIF at 9% Present Value

Chapter 12: The Capital Budgeting Decision

c. Net Present Value Profile

d. Since the projects are not mutually exclusive, they both can

be selected if they have a positive net present value. At a 9

percent cost of capital, they should both be accepted. As a

side note, we can see Project E is superior to Project H.

e. With mutually exclusive projects, only one can be accepted.

Of course, that project must still have a positive net present

value. Based on the visual evidence, we see:

(i) 6 percent cost of capital—select Project E

(ii) 13 percent cost of capital—select Project H

(iii) Do not select either project

Calculator Solution:

(b)

Using a financial calculator:

Project E:

Press the following keys: 2nd, CF, 2nd, Clear.

Calculator displays CFo, press 20,000 +|–, press the Enter key.

Press down arrow, enter 5,000, and press Enter.

Press down arrow, enter 1, and press Enter.

Press down arrow, enter 6,000, and press Enter.

Press down arrow, enter 1, and press Enter.

Press down arrow, enter 7,000, and press Enter.

Press down arrow, enter 1, and press Enter.

Press down arrow, enter 10,000, and press Enter.

Chapter 12: The Capital Budgeting Decision

3 .................

12,000

You are going to use the net present value profile to approximate the value for the internal

rate of return. Please follow these steps:

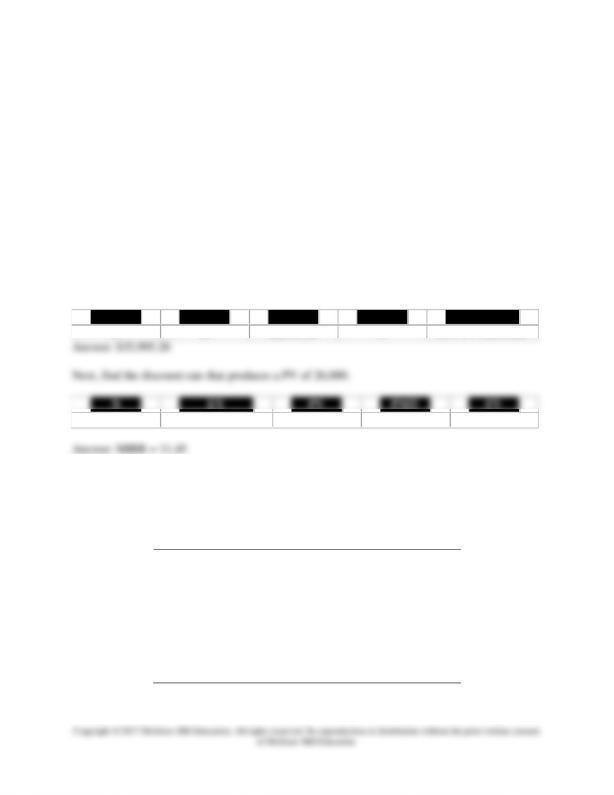

a. Determine the net present value of the project based on a zero discount rate.

Davis Chili Company

a. NPV @ 0% discount rate

Inflows Outflow

$8,000 = ($16,000 + $15,000 + $12,000) – $35,000

b.

Year Cash Flow PVIF at 10% Present Value

1 $16,000 .909 $ 14,544

Chapter 12: The Capital Budgeting Decision

2 15,000 .826 12,390

3 12,000 .751 9,012

Present Value of Inflows $35,946

Present Value of Outflows 35,000

Net Present Value $ 946

c.

Year Cash Flow PVIF at 15% Present Value

1 $16,000 .870 $ 13,920

2 15,000 .756 11,340

3 12,000 .658 7,896

Present Value of Inflows $33,156

Present Value of Outflows 35,000

Net Present Value ($ 1,844)

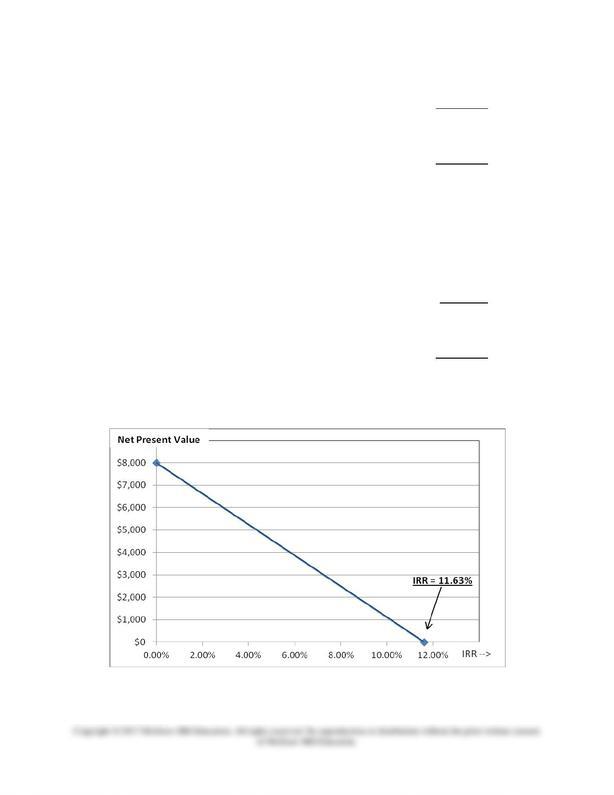

d. Net Present Value Profile

Calculator Solution:

Chapter 12: The Capital Budgeting Decision

(b)

25. MACRS depreciation and cash flow (LO12-2) Telstar Communications is going to

purchase an asset for $380,000 that will produce $180,000 per year for the next four years

in earnings before depreciation and taxes. The asset will be depreciated using the three-year

MACRS depreciation schedule in Table 12-12. (This represents four years of depreciation

based on the half-year convention.) The firm is in a 35 percent tax bracket. Fill in the

schedule below for the next four years.

Chapter 12: The Capital Budgeting Decision

12-25. Solution:

Telstar Communications Corporation

First, determine annual depreciation.

Percentage

Depreciation Depreciation Annual

Year Base (Table 12-9) Depreciation

1 $380,000 .333 $ 126,540

2 380,000 .445 169,100

3 380,000 .148 56,240

4 380,000 .074 28,120

$380,000

Chapter 12: The Capital Budgeting Decision

26. MACRS depreciation categories (LO12-4) Assume $65,000 is going to be invested in

12-26. Solution:

a. Office furniture – Based on Table 12-8, this falls under

7-year MACRS depreciation. Then, examining Table 12-9,

the first year depreciation rate is .143. Thus:

$65,000 .143 $9,295=

b. Automobile – This falls under 5-year MACRS depreciation.

This first year depreciation rate is .200.

Chapter 12: The Capital Budgeting Decision

Year 4 ................... 40,000

The firm is in a 35 percent tax bracket and has an 8 percent cost of capital. Should it

purchase the asset? Use the net present value method.

12-27. Solution:

Summit Petroleum Corporation

First, determine annual depreciation.

Percentage

Depreciation Depreciation Annual

Year Base (Table 12-9) Depreciation

1 $160,000 .333 $53,280

2 160,000 .445 71,200

3 160,000 .148 23,680

Chapter 12: The Capital Budgeting Decision

12-27. (Continued)

Then, determine the net present value.

Cash Flow Present

Year (inflows) PVIF at 8% Value

1 $64,148 .926 $59,401

2 80,170 .857 68,706

3 35,588 .794 28,257

4 30,144 .735 22,156

Present Value of Inflows $178,520

Present Value of Outflows 160,000

Net Present Value $ 18,520

The asset should be purchased based on the net present value.

Calculator Solution:

Chapter 12: The Capital Budgeting Decision

Year 6 ...................... 32,000

The firm is in a 30 percent tax bracket and has a 14 percent cost of capital. Should

Oregon Forest Products purchase the equipment? Use the net present value method.

Oregon Forest Products

First, determine annual depreciation.

Percentage

Depreciation Depreciation Annual

Year Base (Table 12-9) Depreciation

1 $300,000 .200 $ 60,000

2 300,000 .320 96,000

3 300,000 .192 57,600

4 300,000 .115 34,500

5 300,000 .115 34,500

6 300,000 .058 17,400

$300,000

Chapter 12: The Capital Budgeting Decision

12-28. (Continued)

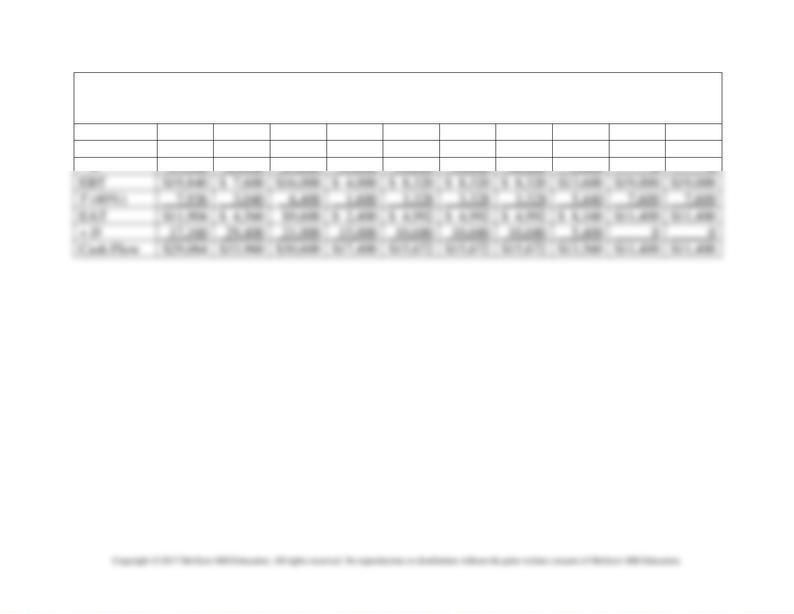

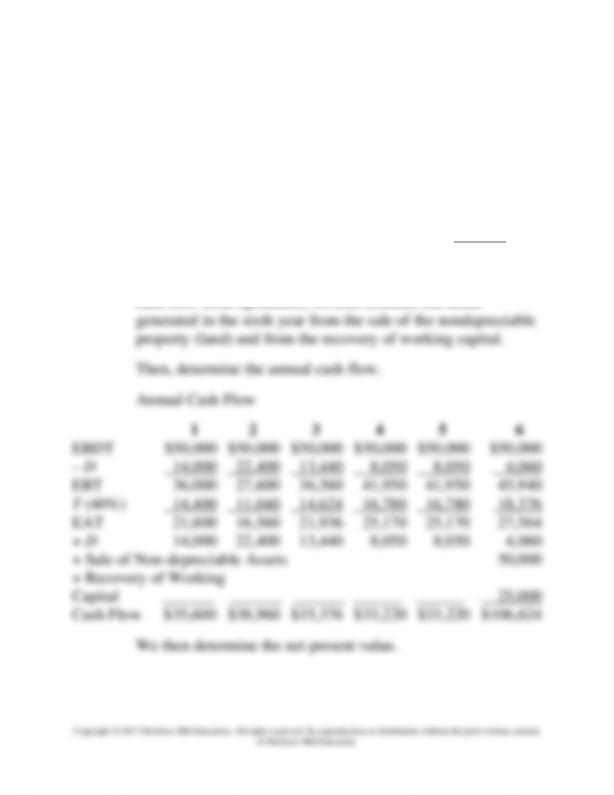

Then, determine the annual cash flow.

Annual Cash Flow

1 2 3 4 5 6

EBDT $112,000 $105,000 $82,000 $53,000 $37,000 $32,000

– D 60,000 96,000 57,600 34,500 34,500 17,400

EBT 52,000 9,000 24,400 18,500 2,500 14,600

T (30%) 15,600 2,700 7,320 5,550 750 4,380

EAT 36,400 6,300 17,080 12,950 1,750 10,220

+ D 60,000 96,000 57,600 34,500 34,500 17,400

Cash Flow $ 96,400 $102,300 $74,680 $47,450 $36,250 $27,620

Then, determine the net present value.

Cash Flow Present

Year (Inflows) PVIF @ 14% Value

1 $ 96,400 .877 $ 84,543

2 102,300 .769 78,669

3 74,680 .675 50,409

4 47,450 .592 28,090

5 36,250 .519 18,814

6 27,620 .456 12,595

Chapter 12: The Capital Budgeting Decision

29. MACRS depreciation and net present value (LO12-4) Universal Electronics is considering

the purchase of manufacturing equipment with a 10-year midpoint in its asset depreciation

range (ADR). Carefully refer to Table 12-11 to determine in what depreciation category the

asset falls. (Hint: It is not 10 years.) The asset will cost $120,000, and it will produce earnings

before depreciation and taxes of $37,000 per year for three years, and then $19,000 a year for

seven more years. The firm has a tax rate of 40 percent. With a cost of capital of 12 percent,

Because the manufacturing equipment has a 10-year midpoint

of its asset depreciation range (ADR), it falls into the 7-year

MACRS category as indicated in Table 12-8. Furthermore, we

see that most types of manufacturing equipment fall into the 7-

year MACRS category.

With seven-year MACRS depreciation, the asset will be

depreciated over eight years (based on the half-year

convention). Also, we observe that the equipment will produce

earnings for 10 years, so in the last 2 years there will be no

depreciation write-off.

We first determine the annual depreciation.

Chapter 12: The Capital Budgeting Decision

Percentage

Depreciation Depreciation Annual

Year Base (Table 12-9) Depreciation

Chapter 12: The Capital Budgeting Decision

12-29. (Continued)

Annual Cash Flow

1

2

3

4

5

6

7

8

9

10

EBDT

$37,000

$37,000

$37,000

$19,000

$19,000

$19,000

$19,000

$19,000

$19,000

$19,000

Chapter 12: The Capital Budgeting Decision

12-29. (Continued)

Next, determine the net present value.

Cash Flow Present

Year (Inflows) PVIF at 12% Value

1 $29,064 .893 $ 25,954

2 33,960 .797 27,066

3 30,600 .712 21,787

4 17,400 .636 11,066

5 15,672 .567 8,886

6 15,672 .507 7,946

7 15,672 .452 7,084

8 13,560 .404 5,478

9 11,400 .361 4,115

10 11,400 .322 3,671

Present Value of Inflows $123,053

Present Value of Outflows 120,000

Net Present Value $ 3,053

New asset should be purchased.

Calculator Solution:

Chapter 12: The Capital Budgeting Decision

30. Working capital requirements in capital budgeting (LO12-4) The Spartan Technology

Company has a proposed contract with the Digital Systems Company of Michigan. The initial

investment in land and equipment will be $120,000. Of this amount, $70,000 is subject to five-

year MACRS depreciation. The balance is in nondepreciable property. The contract covers six

years; at the end of six years, the nondepreciable assets will be sold for $50,000. The

depreciated assets will have zero resale value.

The contract will require an additional investment of $55,000 in working capital at the

beginning of the first year and, of this amount, $25,000 will be returned to the Spartan

Technology Company after six years.

The investment will produce $50,000 in income before depreciation and taxes for each of

the six years. The corporation is in a 40 percent tax bracket and has a 10 percent cost of capital.

Should the investment be undertaken? Use the net present value method.

Spartan Technology Company

Although there are some complicated features to this problem,

we are still comparing the present value of cash flows to the

total initial investment.

The initial investment is:

Land and equipment ......... $120,000

Working capital ................ 55,000

Initial investment .............. $175,000

In computing the present value of the cash flows, we first

determine annual depreciation based on a $70,000 depreciation

base.

Chapter 12: The Capital Budgeting Decision

Percentage

Depreciation Depreciation Annual

Year Base (Table 12-9) Depreciation

1 $70,000 .200 $14,000

2 70,000 .320 22,400

3 70,000 .192 13,440

4 70,000 .115 8,050

5 70,000 .115 8,050

6 70,000 .058 4,060

$70,000

We then determine the annual cash flow. In addition to normal

Chapter 12: The Capital Budgeting Decision

Cash Flow Present

Year (Inflows) PVIF @ 10% Value

1 $ 35,600 .909 $ 32,360

2 38,960 .826 32,181

3 35,376 .751 26,567

4 33,220 .683 22,689

5 33,220 .621 20,630

6 106,624 .564 60,136

Present Value of Inflows $194,563

Present Value of Outflows 175,000

Net Present Value $ 19,563

The investment should be undertaken.

Calculator Solution:

Using a financial calculator:

Press the following keys: 2nd, CF, 2nd, Clear.

Calculator displays CFo, press 175,000 +|–, press the Enter key.

Press down arrow, enter 35,600, and press Enter.

Press down arrow, enter 1, and press Enter.

31. Tax losses and gains in capital budgeting (LO12-2) An asset was purchased three years

12-31. Solution:

Chapter 12: The Capital Budgeting Decision

First determine the book value of the asset.

Percentage

Depreciation Depreciation Annual

Year Base (Table 12-9) Depreciation

1 $120,000 .200 $24,000

2 120,000 .320 38,400

3 120,000 .192 23,040

Total Depreciation to Date $85,440

32. Capital budgeting with cost of capital computation (LO12-5) DataPoint Engineering is

considering the purchase of a new piece of equipment for $240,000. It has an eight-year

midpoint of its asset depreciation range (ADR). It will require an additional initial

Chapter 12: The Capital Budgeting Decision

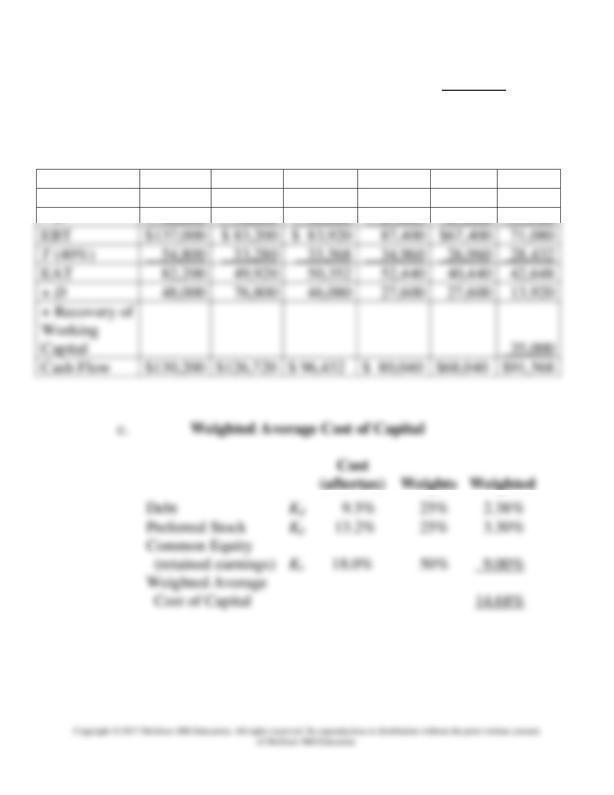

Common equity (retained earnings). ..........

Ke

18.0

50

DataPoint Engineering

a. An eight-year midpoint of the ADR leads to five-year

MACRS depreciation.

Percentage

Depreciation Depreciation Annual

Year Base (Table 12-9) Depreciation

1 $ 240,000 .200 $ 48,000

2 240,000 .320 76,800

3 240,000 .192 46,080

4 240,000 .115 27,600

5 240,000 .115 27,600

Chapter 12: The Capital Budgeting Decision

6 240,000 .058 13,920

$240,000

b. Annual Cash Flow

1

2

3

4

5

6

EBDT

$185,000

$160,000

$130,000

$115,000

$95,000

$85,000

Chapter 12: The Capital Budgeting Decision

d. Net Present Value

Cash Flow Present

Year (inflows) PVIF at 15% Value

1 $130,200 .870 $113,274

2 126,720 .756 95,800

3 96,432 .658 63,452

4 80,040 .572 45,783

5 68,040 .497 33,816

6 91,568 .432 39,557

Present Value of Inflows $391,682

* Present Value of Outflows 380,000

Net Present Value $ 11,682

*This represents the $240,000 for the equipment plus the

$140,000 in initial working capital.

The net present value ($11,682) is positive and DataPoint

Engineering should purchase the equipment.

Calculator Solution:

Using a financial calculator:

(d)

Press the following keys: 2nd, CF, 2nd, Clear.

Calculator displays CFo, press 380,000 +|–, press the Enter key.

Press down arrow, enter 130,200 and press Enter.

Press down arrow, enter 1, and press Enter.

Press down arrow, enter 126,720, and press Enter.

Press down arrow, enter 1, and press Enter.

Chapter 12: The Capital Budgeting Decision

33. Replacement decision analysis (LO12-4) Hercules Exercise Equipment Co. purchased a

computerized measuring device two years ago for $58,000. The equipment falls into the

five-year category for MACRS depreciation and can currently be sold for $24,800.

6 ............

The firm’s tax rate is 35 percent and the cost of capital is 12 percent.

a. What is the book value of the old equipment?

b. What is the tax loss on the sale of the old equipment?

c. What is the tax benefit from the sale?

d. What is the cash inflow from the sale of the old equipment?

e. What is the net cost of the new equipment? (Include the inflow from the sale of the

old equipment.)

Chapter 12: The Capital Budgeting Decision

12-33. Solution:

Hercules Exercise Equipment Co.

a.

Percentage

Depreciation Depreciation Annual

Year Base (Table 12-9) Depreciation

1 $58,000 .200 $11,600

2 58,000 .320 18,560

Total Depreciation to Date $30,160

Purchase Price $58,000

– Total Depreciation to Date 30,160

Book Value $27,840

b. Book Value $27,840

Sales Price 24,800

Tax Loss on the Sale $ 3,040

c. Tax Loss on the Sale $ 3,040

Tax Rate 35%

Tax Benefit $ 1,064

d. Sales Price of the Old Equipment $ 24,800

Tax Benefit from the Sale 1,064

Cash Inflow from the Sale of the Old Equipment $ 25,864

e. Price of the New Equipment $148,000

– Cash Inflow from the Sale of the Old Equipment 25,864

Net Cost of the New Equipment $122,136

Chapter 12: The Capital Budgeting Decision

Chapter 12: The Capital Budgeting Decision

(1)

(2)

(3)

(4)

(5)

(6)

Year

Depreciation

on new

Equipment

Depreciation

on old

Equipment

Incremental

Depreciation

Tax

Rate

Tax

Shield

Benefits

1

$29,600

$11,136

$18,464

.35

$ 6,462

2

47,360

6,670

40,690

.35

14,242

3

28,416

6,670

21,746

.35

7,611

4

17,020

3,364

13,656

.35

4,780

(1)

(2)

(3)

(4)

(5)

(6)

Tax Shield

Benefits

Aftertax

Total

Present

Value

Chapter 12: The Capital Budgeting Decision

4

4,780

32,500

37,280

.636

23,710

5

5,957

30,550

36,507

.567

20,699

6

3,004

23,400

26,404

.507

13,387

Present Value of Incremental Benefits

$168,365

k. Present Value of Incremental Benefits $168,365

Net Cost of New Equipment 122,136

Net Present Value $ 46,229

Based on the present value analysis, the equipment should be

replaced.

Calculator Solution:

Using a financial calculator,

Press the following keys: 2nd, CF, 2nd, Clear.

Calculator displays CF0, press 122,136 +|–, press the Enter key.

Press down arrow, enter 46,762, and press Enter.

Press down arrow, enter 1, and press Enter.

Press down arrow, enter 49,342, and press Enter.

Press down arrow, enter 1, and press Enter.

Press down arrow, enter 41,411, and press Enter.

Press down arrow, enter 1, and press Enter.

Press down arrow, enter 37,280, and press Enter.

Press down arrow, enter 1, and press Enter.

Chapter 12: The Capital Budgeting Decision

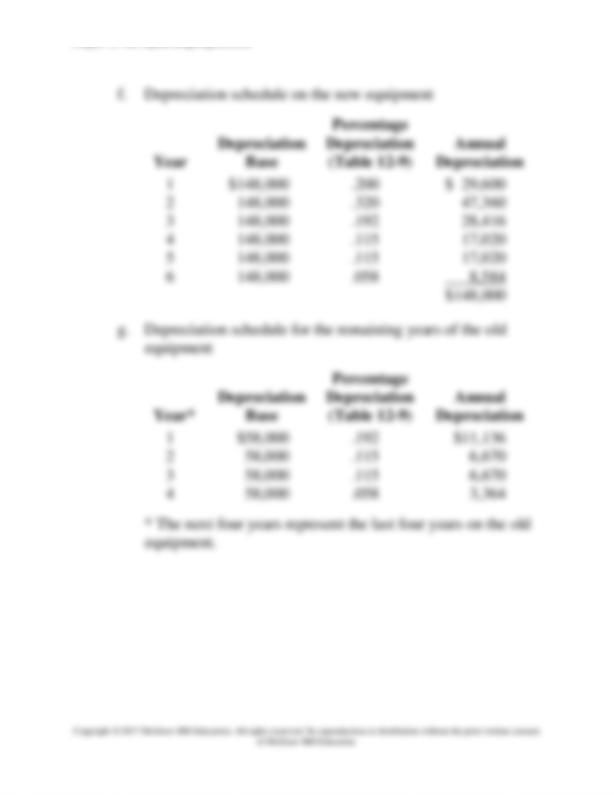

6 ..............

45,000

(7,000)

The firm has a 36 percent tax rate and a 9 percent cost of capital. Should the new equipment

be purchased to replace the old equipment?

Chapter 12: The Capital Budgeting Decision

CP 12-1. Solution:

Woodruff Corporation

Book Value of Old Equipment

(ADR of 8 years indicates the use of the 5-year MACRS

schedule)

Year

Depreciation

Base

Percentage

Depreciation

(Table 12-9)

Annual

Depreciation

1

$230,000

.200

$ 46,000

2

230,000

.320

73,600

3

230,000

.192

44,160

Total Depreciation to Date

$163,760

Purchase Price $230,000

– Total Depreciation to Date 163,760

Book Value $ 66,240

Tax Obligation on the Sale

Sales Price $ 90,000

Book Value 66,240

Taxable Gain 23,760

Tax Rate 36%

Taxes $ 8,554

Cash Inflow from the Sale of the Old Equipment

Sales Price $90,000

Taxes 8,554

$81,446

Net Cost of the New Equipment

Chapter 12: The Capital Budgeting Decision

Chapter 12: The Capital Budgeting Decision

(1)

(2)

(3)

(4)

(5)

(6)

Year

Depreciation

on New

Equipment

Depreciation

on Old

Equipment

Incremental

Depreciation

Tax

Rate

Tax

Shield

Benefits

1

$ 64,000

$26,450

$37,550

.36

$13,518

2

102,400

26,450

75,950

.36

27,342

3

61,440

13,340

48,100

.36

17,316

4

36,800

36,800

.36

13,248

Chapter 12: The Capital Budgeting Decision

(1)

(2)

(3)

(4)

(5)

(6)

Year

Tax Shield

Benefits

from

Depreciation

Aftertax

Cost

Savings

Total

Annuity

Benefits

Present

Value

Factor

9%

Present

Value

1

$13,518

$35,200

$48,718

.917

$ 44,674

2

27,342

38,400

65,742

.842

55,355