Chapter 12

The Statement of Cash Flows

Ethics Check

(5-10 min.) EC 12-1

a. Integrity

b. Due care

c. Objectivity and independence

d. Integrity

Short Exercises

(10 min.) S 12-1

The statement of cash flows helps investors and creditors:

a. Predict future cash flows by reporting past cash receipts and

payments, which are reasonably good predictors of future cash

receipts and payments.

b. Evaluate management decisions by reporting on how managers got

cash and how they used cash to run the business.

(10-15 min.) S 12-2

DATE: _______________

TO: Managers of Sowell Enterprises, Inc.

FROM: Student Name

SUBJECT: Purposes of the statement of cash flows

The statement of cash flows is designed to help predict the future cash

flows of a business. The statement of cash flows measures past cash

flows, which are a reasonably good predictor of future cash flows. Net

(5-10 min) S 12-3

5. Loss on the sale of long-term assets

Students need to identify 3 items.

(15-30 min.) S 12-4

DATE: _______________

TO: Managers of Jolson Hotels, Inc.

FROM: Student Name

SUBJECT: Assessment of 2016 and Outlook for the Future

2016 was not a good year. Most of the increase in net income resulted

from the gain on the insurance proceeds from fire damage to a building,

which means that normal operations were not very profitable. This is

confirmed by the increase in receivables, which hints that collections

are lagging.

The cash-flow data paint a similar picture. Operating activities used

cash, which is bad news. Over the long run, operations should provide

the bulk of the cash if the business expects to succeed.

During 2016, the insurance recovery helped investing activities produce

(continued) S 12-4

(5-10 min.) S 12-5

Cash flows from operating activities:

Net income ............................................................................

$21,000

Adjustments to reconcile net income to

(10 min.) S 12-6

O+

a.

Increase in accounts

O−

h.

Decrease in accrued

payable

liabilities

O+

b.

Decrease in accounts

O+

i.

Net income

receivable

O+

j.

Decrease in prepaid

O−

c.

Gain on sale of

expense

(10 min.) S 12-7

Williams Corporation

Statement of Cash Flows (partial)

Year ended June 30, 2016

Cash flows from operating activities:

Net income ..........................................................

$70,000*

Adjustments to reconcile net income to

(15 min.) S 12-8

Williams Corporation

Statement of Cash Flows

Year ended June 30, 2016

Cash flows from operating activities:

Net income ...........................................................

$ 70,000*

Adjustments to reconcile net income to

net cash provided by operating activities:

Depreciation expense .....................................

$5,000

Increase in current assets other than

cash .............................................................

(29,000)

Increase in current liabilities .........................

10,000

(14,000)

Net cash provided by operating activities .........

56,000

Cash flows from investing activities:

Purchase of equipment .......................................

$(42,000)

Proceeds from sale of land .................................

27,000

Net cash used for investing activities................

(15,000)

Cash flows from financing activities:

Proceeds from issuance of common stock .......

$ 18,000

Payment of note payable ....................................

(30,000)

Payment of dividends .........................................

(6,100)

Purchase of treasury stock ................................

(7,000)

Net cash used for financing activities ...............

(25,100)

Net increase in cash ................................................

$ 15,900

_____

*$225,000 − $116,000 − $34,000 − $5,000 = $70,000

(15 min.) S 12-10

a. New borrowing on long-term notes payable = $11,000 ($64,000 −

$53,000)

b. Issuance of common stock = $11,000 ($41,000 − $30,000)

c. Payment (and declaration) of dividends = $238,000, as follows:

Beginning

Net

income

Dividend

declarations

Ending

Retained

+

−

=

Retained

Earnings

Earnings

$239,000

+

$230,000

−

X

=

$231,000

X

=

$239,000 + $230,000 − $231,000

X

=

$238,000

Retained Earnings

Beg. bal.

239,000

Dividends declared

(paid)

238,000

Net income

230,000

End. bal.

231,000

(15 min.) S 12-11

a. Collections from customers = $759,000, as follows:

Collections

=

Service

−

Increase in Accounts Receivable

from customers

Revenue

=

$770,000

−

$11,000 ($56,000 − $45,000)

=

$759,000

Accounts Receivable

Beg. Bal.

45,000

Revenue

770,000

Collections

759,000

End. Bal.

56,000

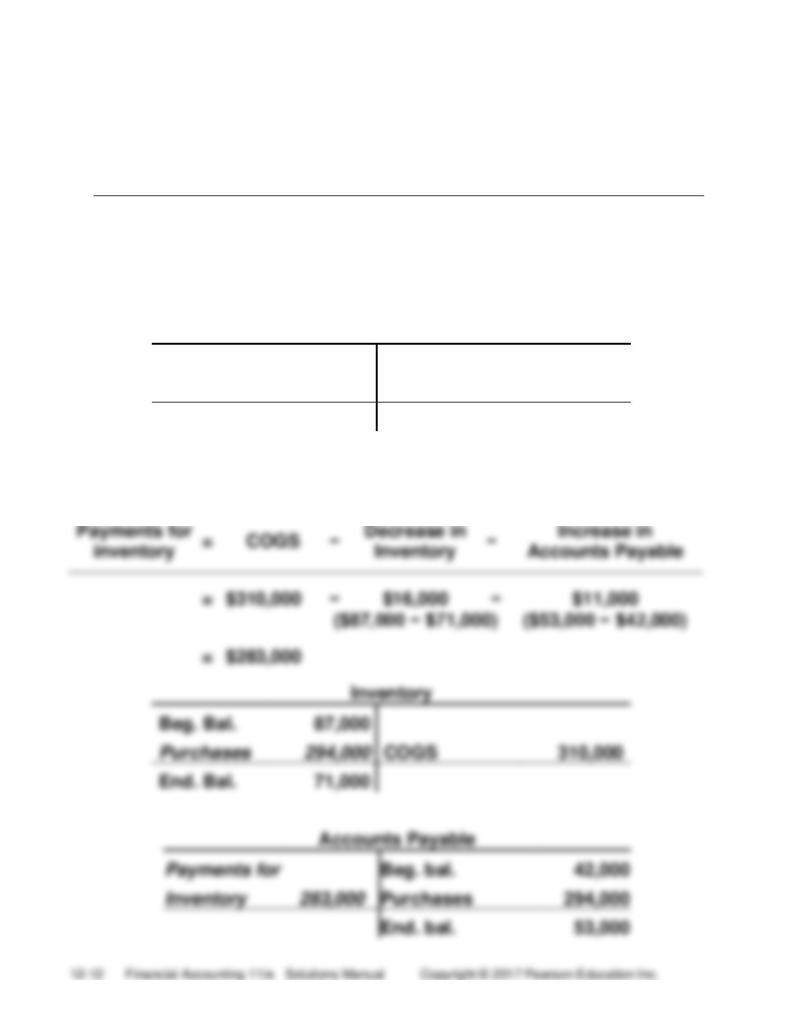

b. Payments for inventory = $283,000, as follows:

(10-15 min.) S 12-12

(15 min.) S 12-13

Laughlin Horse Farms, Inc.

Statement of Cash Flows

Year Ended December 31, 2016

Cash flows from operating activities:

Collections from customers ............................

$ 570,000

Payments to suppliers and employees ..........

(410,000)

Net cash provided by operating activities .....

$160,000

(5 min.) S 12-14

Mulberry Golf Club, Inc.

Statement of Cash Flows (partial)

Year ended September 30, 2016

(15 min.) S 12-15

Mulberry Golf Club, Inc.

Statement of Cash Flows

Year ended September 30, 2016

Cash flows from operating activities:

Collections from customers .................................

$ 202,000

Payments to suppliers ..........................................

(111,000)

Payments to employees .......................................

(74,000)

Payment of income tax .........................................

(15,000)

Net cash provided by operating activities ..........

$ 2,000

Cash flows from investing activities:

Purchase of equipment ........................................

$(43,000)

Proceeds from sale of land ..................................

62,000

Net cash provided by investing activities ...........

19,000

Cash flows from financing activities:

Proceeds from issuance of common stock ........

$ 17,000

Payment of note payable ......................................

(23,000)

Payment of dividends ...........................................

(7,500)

Purchase of treasury stock ..................................

(5,500)

Net cash used for financing activities .................

(19,000)

Net increase in cash ..................................................

$ 2,000

Exercises

(10-15 min.) E 12-16A

F–

a.

Payment of long-term

F+

k.

Issuance of long-term

debt

note payable to borrow

cash

O+

b.

Increase in salary payable

O–

l.

Increase in prepaid

I+

c.

Cash sale of land

expenses

I+

d.

Sale of long-term

O–

m.

Decrease in accrued

investment

liabilities

I–

e.

Acquisition of building by

O+

n.

Loss on sale of equipment

cash payment

O+

o.

Decrease in accounts

O+

f.

Net income

receivable

F+

g.

Issuance of common stock

O+

p.

Depreciation on equipment

for cash

O+

q.

Increase in accounts

F–

h.

Payment of cash dividend

payable

NIF

i.

Acquisition of equipment

O+

r.

Amortization of intangible

by issuance of note

assets

payable

F–

s.

Purchase of treasury stock

I–

j.

Purchase of long-term

investment with cash

(5-10 min.) E 12-17A

a.

Investing

h.

Financing

b.

Financing

i.

Financing

c.

Financing

j.

Investing

(10-15 min.) E 12-18A

(15-20 min.) E 12-19A

(20-30 min.) E 12-20A

Increase in prepaid expenses ........................

(900)

Increase in accounts payable ........................

13,000

Increase in accrued liabilities ........................

17,000

89,100

Net cash provided by operating activities ....

119,000

Cash flows from investing activities:

Acquisition of plant assets ..................................

$(90,000)

Proceeds from sale of land ..................................

34,000

Net cash used for investing activities ...........

(56,000)

Cash flows from financing activities:

Proceeds from issuance of common stock ........

$ 60,000

Payment of long-term note payable ....................

(14,000)

Payment of dividends ..........................................

(12,000)

Net cash provided by financing activities .....

34,000

Net increase in cash ................................................

$ 97,000

Cash balance, December 31, 2015 ..........................

68,000

Cash balance, December 31, 2016 ..........................

$165,000

Noncash investing and financing activities:

Acquisition of plant assets by issuing note payable

$ 44,000

(continued) E 12-20A

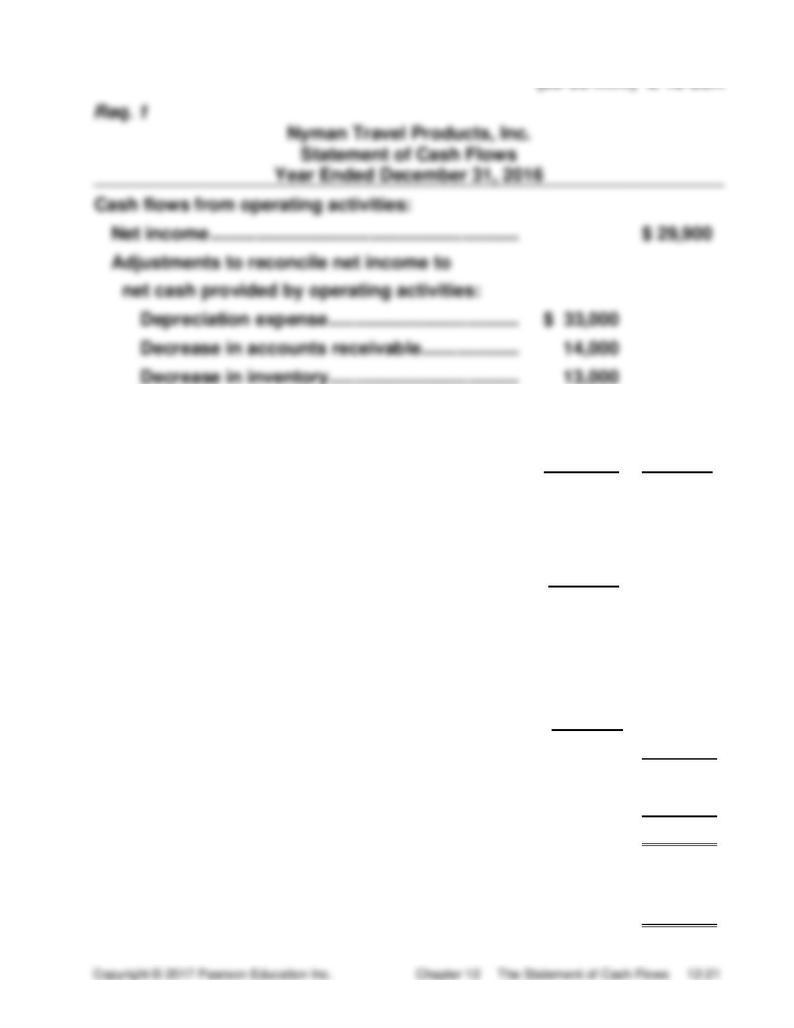

Req. 2

Nyman’s cash flows look strong. Operations are the main source of

cash. The company is investing in new plant assets without having to

borrow. It was able to issue stock, pay dividends, and pay off a long-

term note payable — all financing transactions. All of these signs are

favorable.

(5-10 min.) E 12-21A

Case A — A combination of operations and issuing stock generated

most of the cash for acquisition of plant assets. The company

also sold plant assets for cash.

Case B — The sale of plant assets generated the cash needed to acquire

new plant assets. Operations provided a positive cash flow.

Case C — Issuing stock and the sale of plant assets generated the cash

to acquire plant assets. Operations did not provide a positive

cash flow.

Most healthy financially — Case A

Mid-range — Case B

Least healthy financially — Case C

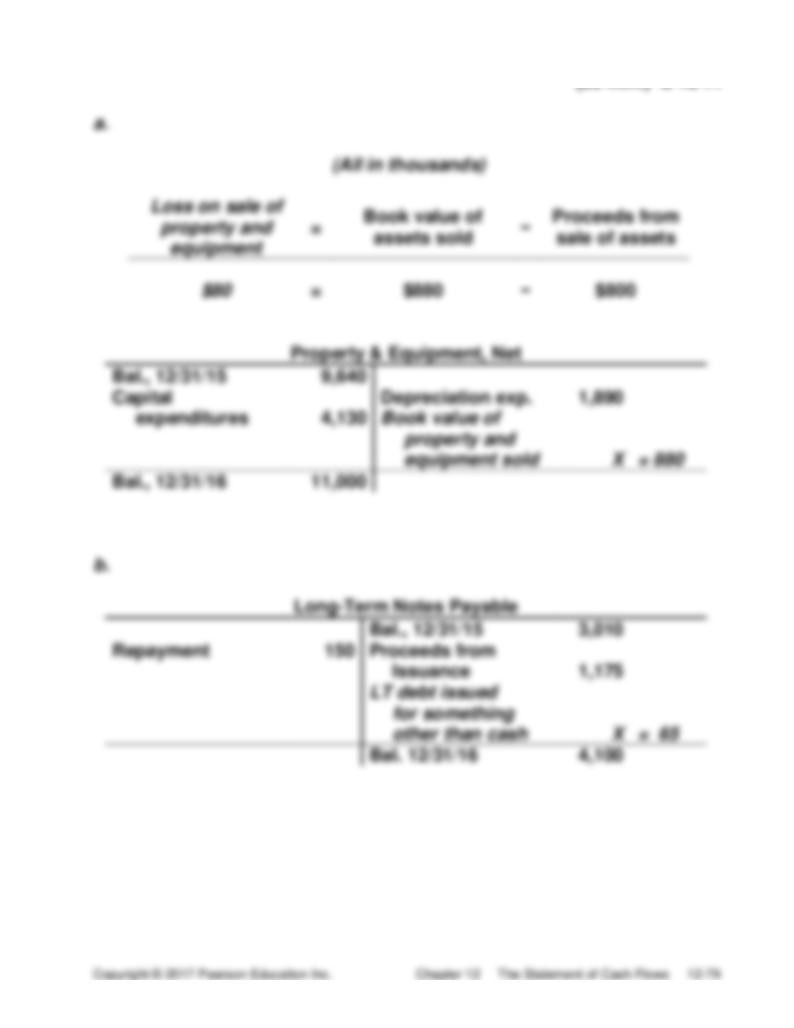

(10-15 min.) E 12-22A

a. Cash proceeds of sale = Book value of asset sold, $7,000* –

Loss on sale, $5,000

= $2,000

_____

*$120,000 + $15,000 − $13,000 − Book value sold (X) = $115,000

Book value sold = $7,000

Plant Assets, Net

Beginning balance

120,000

Depreciation expense

13,000

Purchases

15,000

Book value sold*

7,000

Ending balance

115,000

b. Cash dividend declared = $28,000*

_____

*$44,000 + $59,000 − $6,000 − Cash dividends (X) = $69,000

Cash dividends = $28,000

(10-15 min.) E 12-23A

(5-10 min.) E 12-24A

(20-30 min.) E 12-25A

Net decrease in cash .................................................

$ ( 400)

Cash balance, June 30, 2015 ....................................

25,000

Cash balance, June 30, 2016 ....................................

$ 24,600

Noncash investing and financing activities:

Acquisition of plant assets by issuing note payable

$ 100,000

(continued) E 12-25A

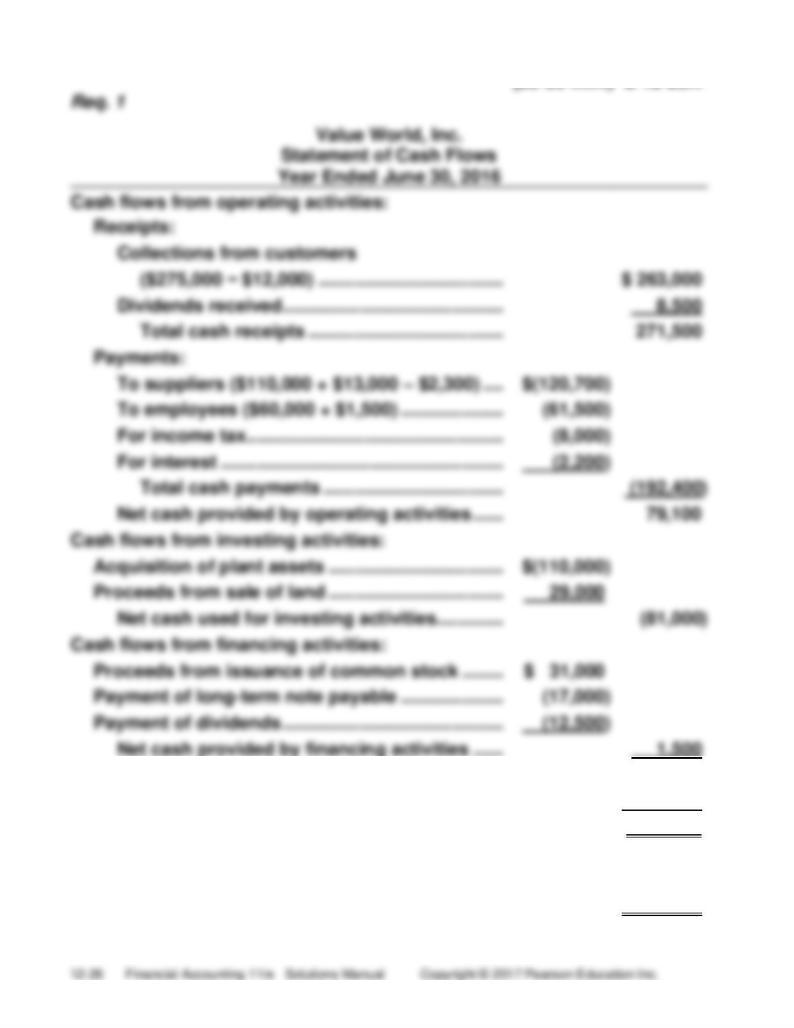

Req. 2

Value World’s cash flows look strong. Operations are the main source of

cash. The company invested in new plant assets without having to

borrow. Value World was able to issue stock, pay dividends, and pay off

a long-term note payable — all financing transactions. All of these signs

are favorable.

(10-15 min.) E 12-26A

$6,000 increase in

a.

Cash collections

=

$141,000

−

Accounts Receivable

($53,000 − $47,000)

=

$135,000

Cash payments

for inventory

$4,000 decrease in

$3,000 increase in

b.

=

$76,000

−

Inventory

−

Accounts Payable

($39,000 − $35,000)

($32,000 − $29,000)

=

$69,000

(10-15 min.) E 12-27B

O+

a.

Increase in salary payable

O+

k.

Net income

O+

b.

Depreciation of equipment

O+

l.

Loss on sale of equipment

I+

c.

Sale of long-term

O+

m.

Decrease in accounts

investment

receivable

F+

d.

Issuance of common stock

NIF

n.

Acquisition of equipment

for cash

by issuance of note

payable

O–

e.

Decrease in accrued

liabilities

O+

o.

Increase in accounts

payable

O+

f.

Amortization of intangible

assets

F–

p.

Payment of cash dividend

I–

g.

Acquisition of building by

I–

q.

Purchase of long-term

cash payment

Investment with cash

F–

h.

Payment of long-term debt

I+

r.

Cash sale of land

F+

i.

Issuance of long-term note

O–

s.

Increase in prepaid

payable to borrow cash

expenses

F–

j.

Purchase of treasury stock

(5-10 min.) E 12-28B

a.

Financing

h.

Investing

(10-15 min.) E 12-29B

(15-20 min.) E 12-30B

(20-30 min.) E 12-31B

Increase in prepaid expenses ......................

(700)

Increase in accounts payable ......................

11,000

Decrease in accrued liabilities ....................

(25,000)

15,300

Net cash provided by operating activities .....

62,200

Cash flows from investing activities:

Acquisition of plant assets .................................

$(99,000)

Proceeds from sale of land .................................

25,000

Net cash used for investing activities ............

(74,000)

Cash flows from financing activities:

Proceeds from issuance of common stock .......

$ 47,000

Payment of long-term note payable ...................

(17,000)

Payment of dividends .........................................

(12,000)

Net cash provided by financing activities ......

18,000

Net increase in cash ................................................

$ 6,200

Cash balance, December 31, 2015 ..........................

83,800

Cash balance, December 31, 2016 ..........................

$ 90,000

Noncash investing and financing activities:

Acquisition of plant assets by issuing note payable

$ 51,000

(continued) E 12-31B

Req. 2

Norman’s cash flows look strong. Operations are the main source of

cash. The company is investing in new plant assets without having to

borrow. It was able to issue stock, pay dividends, and pay off a long-

term note payable — all financing transactions. All of these signs are

favorable.

(5-10 min.) E 12-32B

Case A — A combination of operations and issuing stock generated

most of the cash for acquisition of plant assets. The

company also sold plant assets for cash. Operations

provided more cash than did cases B or C.

Case B — The sale of plant assets generated the cash needed to

acquire new plant assets. They could also have used cash

from the stock issue or cash from operations.

Case C — Issuing stock generated the cash to acquire plant assets.

Operations used cash while in cases A and B operations

provided cash. They also could have used cash from the

sale of plant assets.

Most healthy financially — Case A

Mid-range — Case B

Least healthy financially — Case C

(10-15 min.) E 12-33B

a. Cash proceeds of sale = Book value of asset sold, $18,000* –

Loss on sale, $8,000

= $10,000

_____

*$120,000 + $26,000 − $16,000 − Book value sold (X) = $112,000

Book value sold = $18,000

Plant Assets, Net

Beginning balance

120,000

Depreciation expense

16,000

Purchases

26,000

Book value sold*

18,000

Ending balance

112,000

b. Cash dividend declared = $30,000*

_____

*$48,000 + $61,000 − $6,000 − Cash dividends (X) = $73,000

Cash dividends = $30,000*

Retained Earnings

Stock dividends

6,000

Beginning balance

48,000

Cash dividends*

30,000

Net income

61,000

Ending balance

73,000

(10-15 min.) E 12-34B

Cash flows from operating activities:

Receipts:

Collections from customers

($125,000 + $34,000) ...........................

$ 159,000

Collection of dividend revenue ..............

8,000

Total cash receipts .............................

167,000

(5-10 min.) E 12-35B

(20-30 min.) E 12-36B

(continued) E 12-36B

(10-15 min.) E 12-37B

Quiz

Q12-57

a [$59,700 − ($4,000 − $3,000) = $58,700]

Problems

(40 min.) P 12-58A

Req. 1

Klaben Motors, Inc.

Income Statement

Year Ended December 31, 2016

Sales revenue ........................................................................

$649,000

Cost of goods sold [$243,000 + (2 × $39,000)] ....................

321,000

Salary expense ......................................................................

151,000

Depreciation expense ($220,000 / 5) ....................................

44,000

Rent expense.........................................................................

25,000

Income tax expense ..............................................................

22,000

Net income ............................................................................

$ 86,000

Req. 2

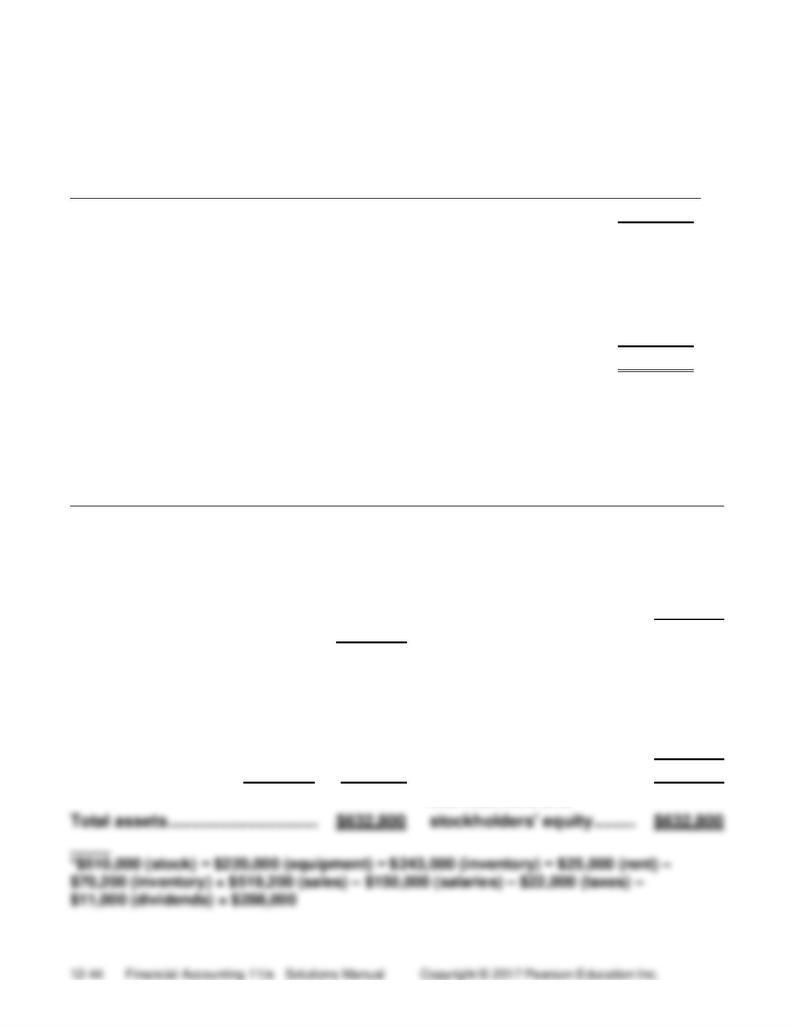

Klaben Motors, Inc.

Balance Sheet

December 31, 2016

ASSETS

LIABILITIES

Current:

Current:

Cash ........................................

$288,000*

Accounts payable

Accounts receivable

($117,000 − $70,200) .....

$ 46,800

($649,000 × .20) ....................

129,800

Salary payable ................

1,000

Inventory (1 × $39,000) ..........

39,000

Total current liabilities ...

47,800

Total current assets ..............

456,800

STOCKHOLDERS’ EQUITY

Property, plant, and equipment:

Common stock ...................

510,000

Equipment .............

$220,000

Retained earnings

Less:Accumulated

($86,000 − $11,000) ...........

75,000

depreciation .......

(44,000)

176,000

Total equity .....................

585,000

Total liabilities and

Total assets ................................

$632,800

stockholders' equity .........

$632,800

____

*$510,000 (stock) − $220,000 (equipment) − $243,000 (inventory) − $25,000 (rent) –

$70,200 (inventory) + $519,200 (sales) – $150,000 (salaries) – $22,000 (taxes) –

$11,000 (dividends) = $288,000

(continued) P 12-58A

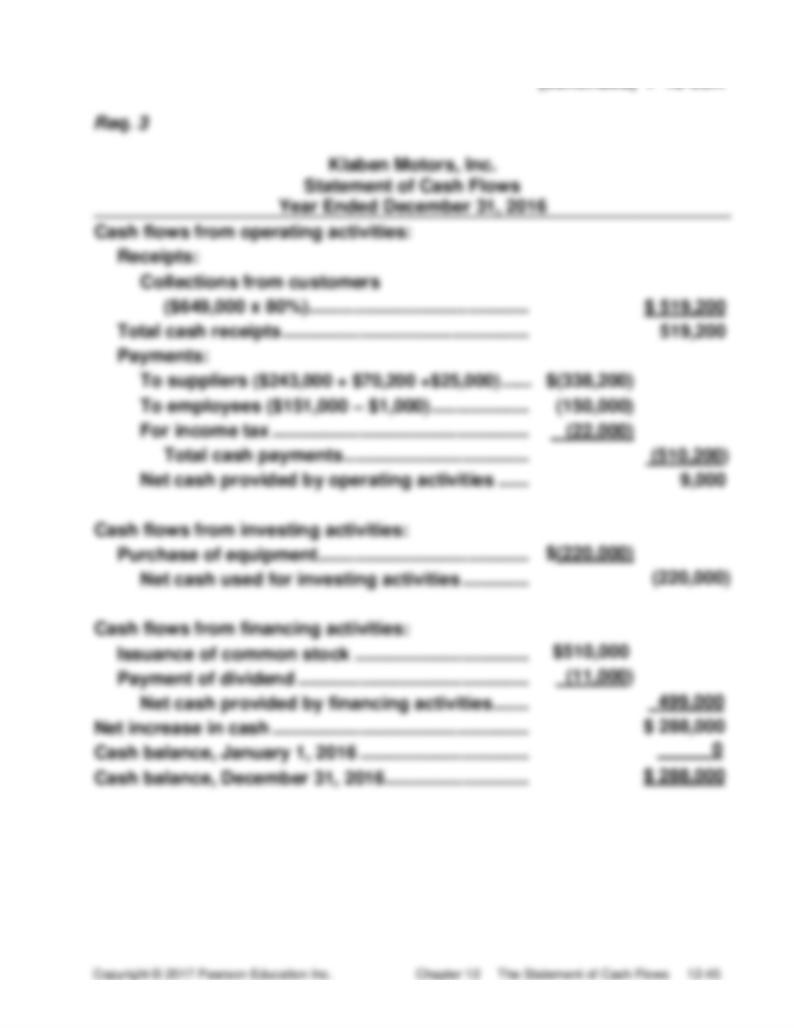

Req. 3

Klaben Motors, Inc.

Statement of Cash Flows

Year Ended December 31, 2016

Cash flows from operating activities:

Net income ..........................................................

$ 86,000

Adjustments to reconcile net income to

net cash provided by operating activities:

Depreciation expense ...............................

$ 44,000

Increase in accounts receivable ..............

(129,800)

Increase in inventory ................................

(39,000)

Increase in accounts payable ...................

46,800

Increase in salary payable ........................

1,000

(77,000)

Net cash provided by operating activities ...

9,000

Cash flows from investing activities:

Purchase of equipment ......................................

$(220,000)

Net cash used for investing activities ..........

(220,000)

Cash flows from financing activities:

Issuance of common stock ...............................

$510,000

Payment of dividend ..........................................

(11,000)

Net cash provided by financing activities ....

499,000

Net increase in cash ...............................................

$ 288,000

Cash balance, January 1, 2016 ..............................

0

Cash balance, December 31, 2016 .........................

$ 288,000

(40 min.) P 12-59A

Req. 1

Klaben Motors, Inc.

Income Statement

Year Ended December 31, 2016

Sales revenue ........................................................................

$649,000

Cost of goods sold [$243,000 + (2 × $39,000)] ....................

321,000

Salary expense ......................................................................

151,000

Depreciation expense ($220,000 / 5) ....................................

44,000

Rent expense.........................................................................

25,000

Income tax expense ..............................................................

22,000

Net income ............................................................................

$ 86,000

Req. 2

Klaben Motors, Inc.

Balance Sheet

December 31, 2016

ASSETS

LIABILITIES

Current:

Current:

Cash ........................................

$288,000*

Accounts payable

Accounts receivable

($117,000 − $70,200) .....

$ 46,800

($649,000 × .20) ....................

129,800

Salary payable ................

1,000

Inventory (1 × $39,000) ..........

39,000

Total current liabilities ...

47,800

Total current assets ..............

456,800

STOCKHOLDERS’ EQUITY

Property, plant, and equipment:

Common stock ...................

510,000

Equipment .............

$220,000

Retained earnings

Less:Accumulated

($86,000 − $11,000) ...........

75,000

depreciation .......

(44,000)

176,000

Total equity .....................

585,000

Total liabilities and

(continued) P 12-59A

(35-45 min.) P 12-60A

(continued) P 12-60A

(35-45 min.) P 12-61A

Increase in prepaid expenses ......................

(900)

Increase in accounts payable .......................

1,700

Decrease in accrued liabilities .....................

(14,000)

Decrease in income tax payable ..................

(1,100)

11,000

Net cash provided by operating activities ......

65,000

Cash flows from investing activities:

Purchase of equipment ......................................

$(34,600)

Purchase of building ..........................................

(44,000)

Sale of long-term investment .............................

15,500

Net cash used for investing activities .............

(63,100)

Cash flows from financing activities:

Issuance of long-term note payable ..................

$ 47,000

Issuance of common stock ................................

10,000

Payment of cash dividend ..................................

(28,000)

Net cash provided by financing activities.......

29,000

Net increase in cash and cash equivalents ..........

$ 30,900

Cash and cash equivalents balance, June 30, 2015

14,500

Cash and cash equivalents balance, June 30, 2016

$ 45,400

Noncash investing and financing activities:

Acquisition of land by issuing note payable ....

$104,000

(continued) P 12-61A

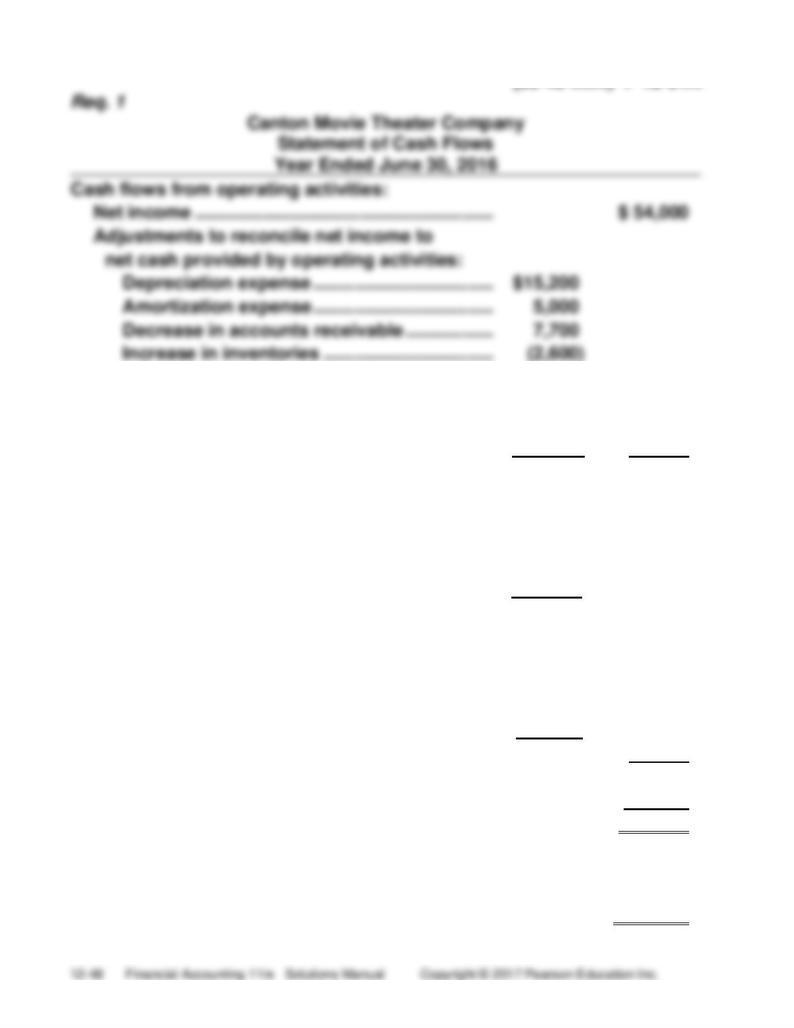

Req. 2

Evaluation: Canton Movie Theater Company’s cash flows look strong.

Operations are the main source of cash. The company is

investing in new plant assets and therefore had a negative

cash flow from investing activities. Canton generated a

positive cash flow from financing activities. These

financing activities indicate that Canton is considered

credit-worthy to issue long-term notes. We also see that

the company has sufficient funds to pay cash dividends.

(30-40 min.) P 12-62A

Req. 1

King Supply Corp.

Statement of Cash Flows

Year Ended December 31, 2016

Cash flows from operating activities:

Net income ...............................................................

$61,000

Adjustments to reconcile net income to

net cash provided by operating activities:

Depreciation expense ........................................

$ 15,000

Increase in accounts receivable .......................

(1,000)

Increase in inventories ......................................

(14,400)

Decrease in prepaid expenses ..........................

2,100

Increase in accounts payable ............................

8,500

Increase in salary payable………………………..

8,000

Decrease in other accrued liabilities ................

(2,100)

16,100

Net cash provided by operating activities ..........

77,100

Cash flows from investing activities:

Purchase of land ......................................................

$(43,600)

Purchase of equipment ($49,900 − depreciation

expense of $15,000 = $34,900; $53,100 −

$34,900) ...............................................................

(18,200)

Net cash used for investing activities .................

(61,800)

Cash flows from financing activities:

Payment of dividends ($27,000 + $61,000 − $39,800)..

$(48,200)

Issuance of note payable ........................................

24,000

Issuance of common stock .....................................

22,200

Net cash used for financing activities ................

(2,000)

Net increase in cash and cash equivalents ................

$ 13,300

Cash and cash equivalents balance, December 31, 2015

4,000

Cash and cash equivalents balance, December 31, 2016

$ 17,300

(continued) P 12-62A

Req. 2

This problem will help students learn how operating activities, investing

activities, and financing activities generate cash receipts and cash

payments. By solving this problem, students will learn how companies

prepare the statement of cash flows and will thus be able to understand

the meaning of cash flows from the three basic categories of business

activities. This knowledge will aid their analysis of investments. For

example, students should know that net cash provided by operating

activities conveys a more positive signal about a company than net cash

used for operations.

Student responses will vary.

(30-40 min.) P 12-63A

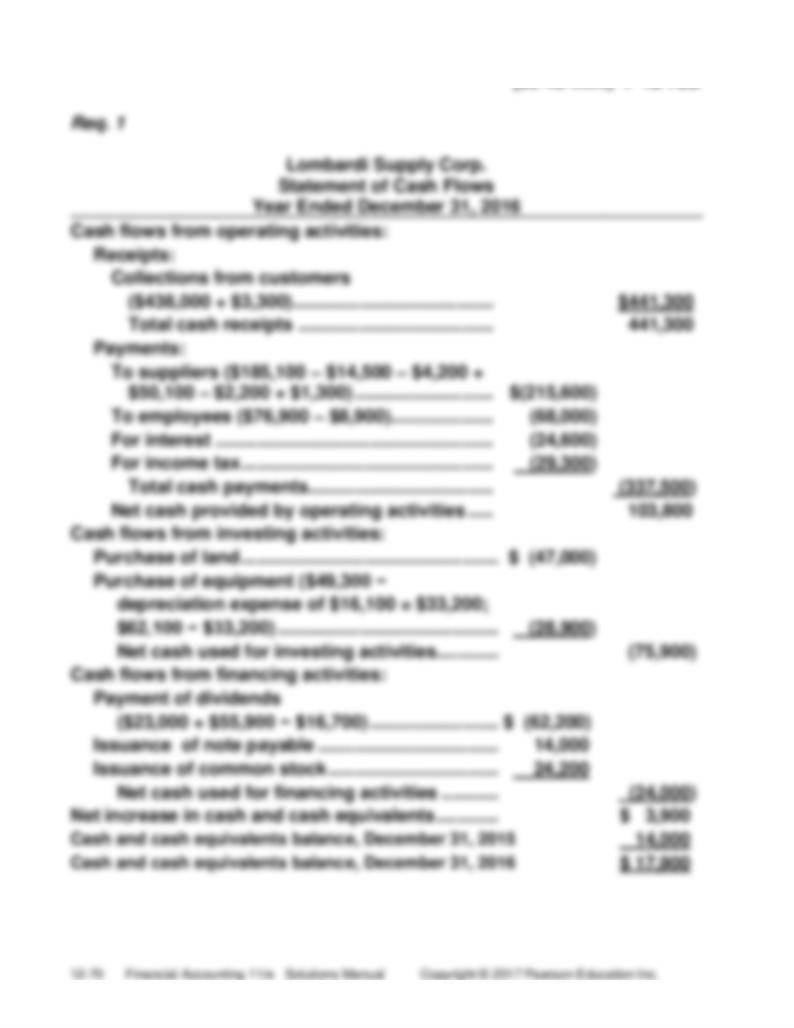

Req. 1

King Supply Corp.

Statement of Cash Flows

Year Ended December 31, 2016

Cash flows from operating activities:

Receipts:

Collections from customers

($442,000 – $1,000) .........................................

$441,000

Total cash receipts ........................................

441,000

Payments:

To suppliers ($186,500 + $14,400 – $8,500 +

$50,300 – $2,100 + $2,100) .............................

$242,700

To employees ($76,000 – $8,000)......................

68,000

For interest ........................................................

24,200

For income tax ...................................................

29,000

Total cash payments ......................................

(363,900)

Net cash provided by operating activities .......

77,100

Cash flows from investing activities:

Purchase of land ......................................................

$(43,600)

Purchase of equipment ($49,900 − depreciation

expense of $15,000 = $34,900; $53,100 −

$34,900) ...............................................................

(18,200)

Net cash used for investing activities .................

(61,800)

Cash flows from financing activities:

Payment of dividends ($27,000 + $61,000 − $39,800)

$(48,200)

Issuance of note payable ........................................

24,000

Issuance of common stock .....................................

22,200

Net cash used for financing activities ................

(2,000)

Net increase in cash and cash equivalents ................

$ 13,300

Cash and cash equivalents balance, December 31, 2015

4,000

Cash and cash equivalents balance, December 31, 2016

$ 17,300

(continued) P 12-63A

Req. 2

This problem will help students learn how operating activities, investing

activities, and financing activities generate cash receipts and cash

payments. By solving this problem, students will learn how companies

prepare the statement of cash flows and will thus be able to understand

the meaning of cash flows from the three basic categories of business

activities. This knowledge will aid their analysis of investments. For

example, students should know that net cash provided by operating

activities conveys a more positive signal about a company than net cash

used for operations.

Student responses will vary.

(35-45 min.) P 12-64A

Req. 1

Crutchfield Furniture Gallery, Inc.

Statement of Cash Flows

Year Ended October 31, 2017

Cash flows from operating activities:

Receipts:

Collections from customers

($406,000 + $182,700) .................................

$588,700

Interest received ............................................

4,500

Dividends received ........................................

4,700

Total cash receipts .....................................

$597,900

Payments:

To suppliers ...................................................

$(368,000)

To employees ................................................

(93,700)

For interest .....................................................

(13,400)

For income tax ...............................................

(38,300)

Total cash payments ..................................

(513,400)

Net cash provided by operating activities ...

84,500

Cash flows from investing activities:

Purchase of plant assets ..................................

$ (44,400)

Sale of plant assets ..........................................

22,300

Collection of loans ............................................

11,200

Loan to another company ................................

(12,800)

Sale of investments ..........................................

9,500

Net cash used for investing activities ..........

(14,200)

Cash flows from financing activities:

Payments of long-term notes payable .............

$ (71,000)

Payment of dividends .......................................

(48,700)

Issuance of note payable .................................

20,200

Issuance of common stock ..............................

7,000

Net cash used for financing activities ..........

(92,500)

Net (decrease) in cash .........................................

$ (22,200)

Cash balance, October 31, 2016 ..........................

40,200

Cash balance, October 31, 2017 ..........................

$ 18,000

(continued) P 12-64A

Noncash investing and financing transactions:

Payment of short-term note payable by

issuing long-term note payable ..................................

$41,000

Acquisition of equipment by issuing

short-term note payable ..............................................

16,300

Total noncash investing and financing transactions .........

$57,300

Req. 2

Year 2017 was a strong year from a cash-flow standpoint. Operations

provided the bulk of the company’s cash and the company was able to

issue new stock and debt. This means stockholders and creditors have

faith in the company. The business acquired additional plant assets,

reduced their debt, and paid dividends which generally bodes well for

the future.

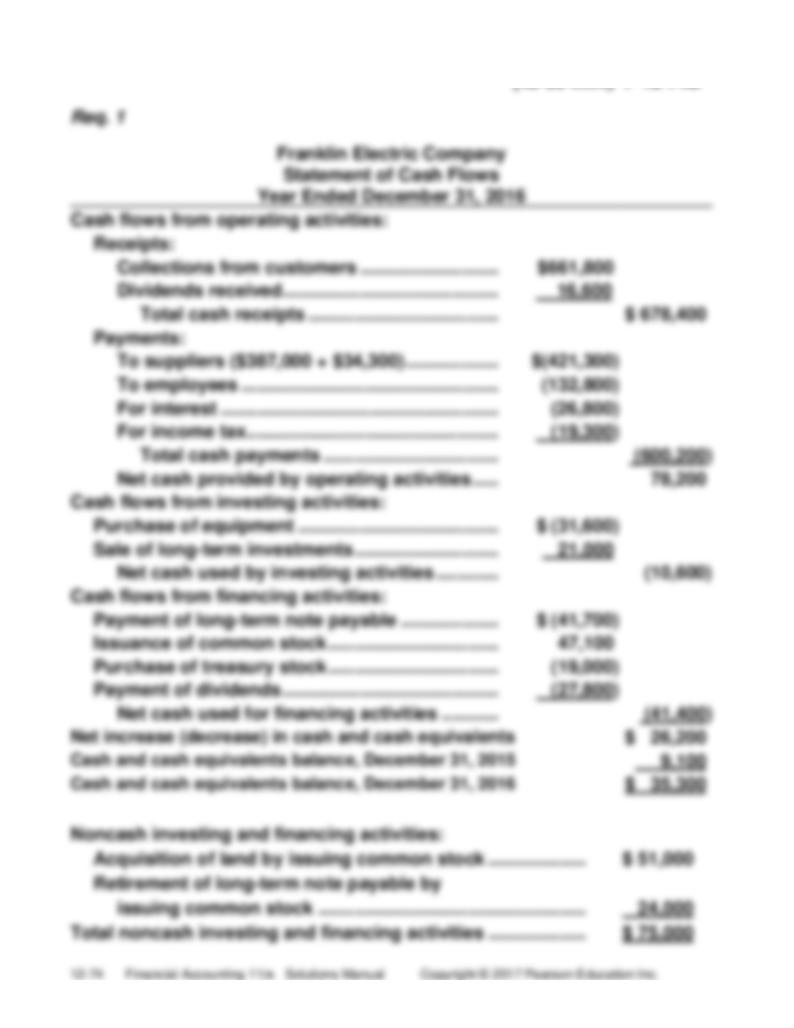

(45-60 min.) P 12-65A

Req. 1

Percy Electric Company

Statement of Cash Flows

Year Ended December 31, 2016

Cash flows from operating activities:

Receipts:

Collections from customers ..................................

$661,500

Dividends received .................................................

16,900

Total cash receipts .............................................

$678,400

Payments:

To suppliers ($446,000 + $34,100) ........................

$(480,100)

To employees ..........................................................

(139,200)

For interest ..............................................................

(25,500)

For income tax ........................................................

(19,100)

Total cash payments ..........................................

(663,900)

Net cash provided by operating activities ...........

14,500

Cash flows from investing activities:

Purchase of equipment .............................................

$ (31,700)

Sale of long-term investments ..................................

21,300

Net cash used for investing activities ..................

(10,400)

Cash flows from financing activities:

Issuance of common stock .......................................

$ 47,600

Payment of long-term note payable .........................

(41,100)

Payment of dividends ................................................

(27,900)

Purchase of treasury stock .......................................

(25,700)

Net cash used for financing activities ..................

(47,100)

Net decrease in cash .....................................................

$ (43,000)

Cash balance, December 31, 2015 ...............................

71,500

Cash balance, December 31, 2016 ...............................

$ 28,500

Noncash investing and financing activities:

Acquisition of land by issuing common stock

$ 80,300

Retirement of note payable by issuing common stock

20,000

Total noncash investing and financing activities

$100,300

(continued) P 12-65A

Req. 2

Percy Electric Company

Cash Flows from Operating Activities

Year Ended December 31, 2016

Cash flows from operating activities:

Net income .............................................................

$12,200

Adjustments to reconcile net income to

net cash provided by operating activities:

Depreciation expense .....................................

$ 19,900

Loss on sale of investments ..........................

1,100

Increase in accounts receivable ....................

(27,700)

Decrease in inventories .................................

9,000

Decrease in prepaid expenses ......................

5,000

Decrease in accounts payable .......................

(7,800)

Increase in interest payable ...........................

2,300

Decrease in salary payable ............................

(7,800)

Increase in other accrued liabilities ..............

10,300

Decrease in income tax payable ....................

(2,000)

2,300

Net cash provided by operating activities ...........

$14,500

(45-60 min.) P 12-66A

Req. 1

Donna Dunn Design Studio, Inc.

Statement of Cash Flows

Year Ended June 30, 2016

Cash flows from operating activities:

Net income ............................................................

$ 70,600

Adjustments to reconcile net income to

net cash provided by operating activities:

Depreciation expense ....................................

$ 13,500

Loss on sale of land .......................................

7,200

Increase in accounts receivable ...................

(26,500)

Increase in inventories ..................................

(35,300)

Decrease in prepaid expenses ......................

1,300

Decrease in accounts payable ......................

(11,000)

Decrease in income tax payable ...................

(1,000)

Increase in accrued liabilities ........................

8,600

Increase in interest payable ..........................

800

Increase in salary payable .............................

300

(42,100)

Net cash provided by operating activities .......

28,500

Cash flows from investing activities:

Sale of land ............................................................

$ 58,200

Purchase of long-term investment ......................

(13,400)

Net cash provided by investing activities ........

44,800

Cash flows from financing activities:

Payment of long-term note payable .....................

$(61,500)

Payment of cash dividends ..................................

(7,500)

Issuance of common stock ..................................

16,000

Net cash used for financing activities ..............

(53,000)

Net increase in cash .................................................

$ 20,300

Cash balance, June 30, 2015 ...................................

8,100

Cash balance, June 30, 2016 ...................................

$ 28,400

(continued) P 12-66A

Req. 1

Noncash investing and financing activities:

Acquisition of equipment by issuing

long-term note payable ................................................

$14,400

Payment of short-term note payable by

issuing common stock .................................................

5,600

Total noncash investing and financing activities ................

$20,000

Req. 2

Donna Dunn Design Studio, Inc.

Statement of Cash Flows

Year Ended June 30, 2016

Cash flows from operating activities:

Receipts:

Collections from customers .........................

$ 239,000

Interest received ............................................

1,500

Total cash receipts ....................................

$ 240,500

Payments:

To suppliers ...................................................

$(146,900)

To employees .................................................

(48,100)

For income tax ...............................................

(12,000)

For interest .....................................................

( 5,000)

Total cash payments .................................

(212,000)

Net cash provided by operating activities ........

$ 28,500

(40 min.) P 12-67B

Req. 1

Pruitt Motors, Inc.

Income Statement

Year Ended December 31, 2016

Sales revenue ..............................................................

$488,000

Cost of goods sold [$203,000 + (1 × $40,000)] ...........

243,000

Salary expense ............................................................

125,000

Rent expense ...............................................................

17,000

Depreciation expense ($180,000 / 5) ...........................

36,000

Income tax expense .....................................................

12,600

Net income ...................................................................

$ 54,400

Req. 2

Pruitt Motors, Inc.

Balance Sheet

December 31, 2016

ASSETS

LIABILITIES

Current:

Current:

Cash ........................................

$252,800*

Accounts payable

Accounts receivable

($80,000 − $24,000) .....

$ 56,000

($488,000 × .20) ..................

97,600

Salary payable ................

3,000

Inventory (1 × $40,000) ..........

40,000

Total current liabilities ...

59,000

Total current assets ...........

390,400

STOCKHOLDERS’ EQUITY

Property, plant, and equipment:

Common stock ...................

440,000

Equipment .............

$180,000

Retained earnings

Less:Accumulated

($54,400 − $19,000) .........

35,400

depreciation .......

(36,000)

144,000

Total equity .....................

475,400

Total liabilities and

Total assets ................................

$534,400

stockholders' equity ......

$534,400

____

*$440,000 (stock) − $180,000 (equipment) − $203,000 (inventory) − $17,000 (rent) −

$24,000 (inventory) + $390,400 (sales) − $122,000 (salaries) − $12,600 (taxes) –

$19,000 (dividends) = $252,800

(continued) P 12-67B

Req. 3

Pruitt Motors, Inc.

Statement of Cash Flows

Year Ended December 31, 2016

Cash flows from operating activities:

Net income ...............................................................

$ 54,400

(40 min.) P 12-68B

(continued) P 12-68B

(35-45 min.) P 12-69B

(continued) P 12-69B

(35-45 min.) P 12-70B

(continued) P 12-70B

(30-40 min.) P 12-71B

(continued) P 12-71B

(30-40 min.) P 12-72B

(continued) P 12-72B

(35-45 min.) P 12-73B

(continued) P 12-73B

(45-60 min.) P 12-74B

(continued) P 12-74B

(45-60 min.) P 12-75B

Decrease in salary payable ..........................

(600)

11,500

Net cash provided by operating activities ......

82,100

Cash flows from investing activities:

Sale of land ..........................................................

$ 39,900

Purchase of long-term investments ...................

(14,600)

Net cash provided by investing activities .......

25,300

Cash flows from financing activities:

Payment of cash dividends .................................

$(37,700)

Issuance of common stock .................................

6,900

Payment of long-term note payable ...................

(59,000)

Net cash used for financing activities ............

(89,800)

Net increase in cash .................................................

$ 17,600

Cash balance, June 30, 2015 ...................................

10,800

Cash balance, June 30, 2016 ...................................

$ 28,400

(continued) P 12-75B

Req. 1

Noncash investing and financing activities:

Acquisition of equipment by issuing

long-term note payable ...................................

$13,600

Paid off short-term note payable by issuing

common stock .................................................

7,000

Total noncash investing and financing activities ...

$20,600

Req. 2

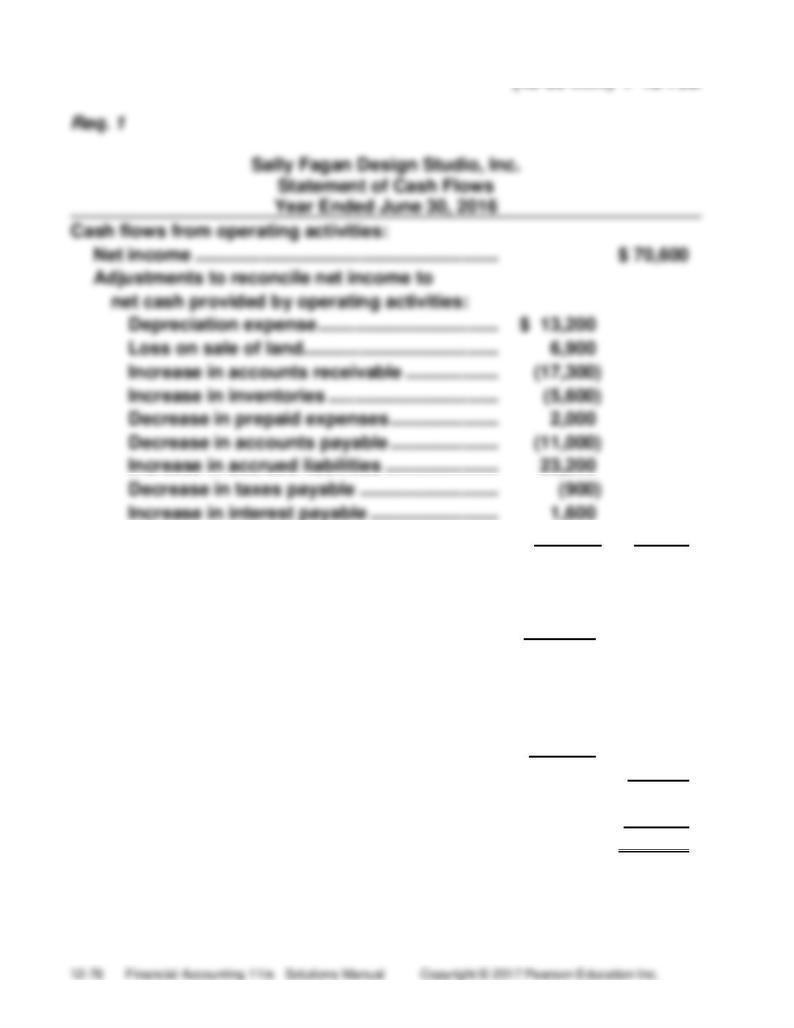

Sally Fagan Design Studio, Inc.

Statement of Cash Flows

Year Ended June 30, 2016

Cash flows from operating activities:

Receipts:

Collections from customers ..........................

$ 231,600

Interest received .............................................

1,200

Total cash receipts .....................................

$ 232,800

Payments:

To suppliers ....................................................

$(95,100)

To employees ..................................................

(39,100)

For income tax ................................................

(12,100)

For interest ......................................................

(4,400)

Total cash payments ..................................

(150,700)

Net cash provided by operating activities .........

$ 82,100

Challenge Exercises and Problem

(20-30 min.) E 12-76

(All amounts in thousands)

Decrease in

Sales

+

Accounts Receivable

a.

Collections

=

$23,996

=

$23,984

+

($609 − $597)

(20 min.) E 12-77

P 12-78

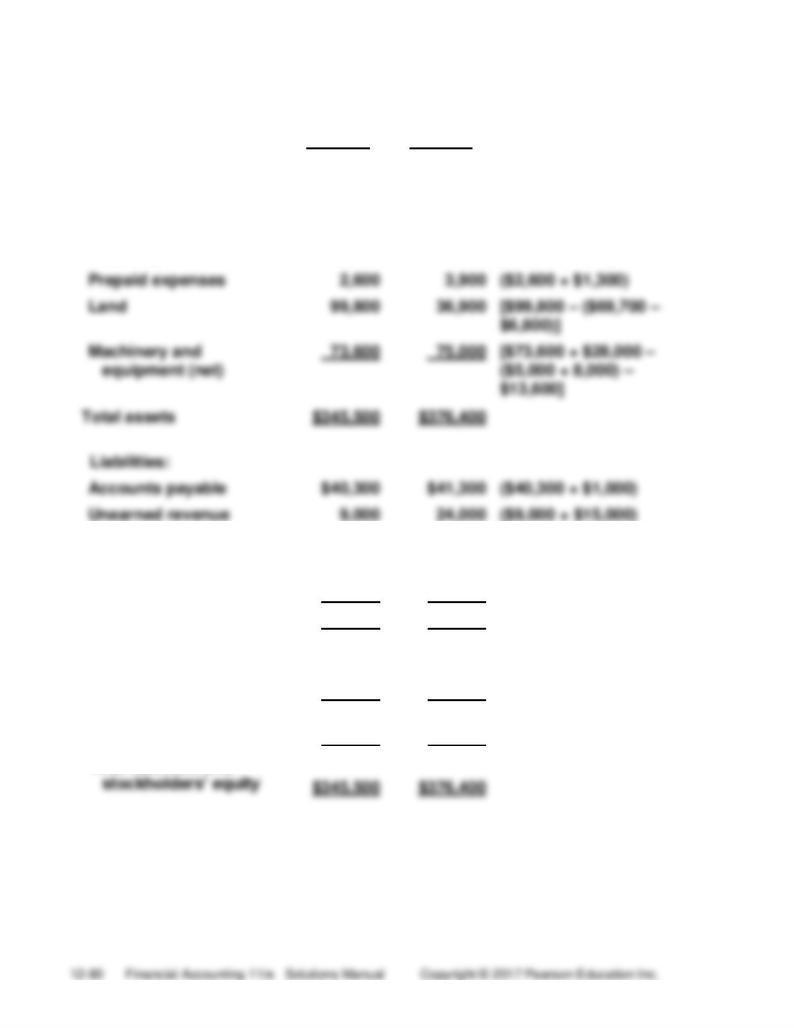

Assets:

December

31, 2015

December

31, 2016

Cash and cash

equivalents

$14,000

$153,500

Given

Accounts receivable

(net)

95,000

28,700

($95,000 – $66,300)

Inventory

60,500

78,400

($60,500 + $17,900)

Dividends payable

-0-

6,000

($9,000 – $3,000)

Income taxes payable

6,000

1,300

($6,000 – $4,700)

Long-term debt

84,100

69,100

($84,100 – $15,000)

Total liabilities

139,400

141,700

Stockholders’ equity:

Common stock, no par

47,300

69,300

($47,300 + $22,000)

Retained earnings

158,800

165,400

($158,800 + $15,600 –

$9,000)

Total stockholders’ equity

206,100

234,700

Total liabilities and

Decision Cases

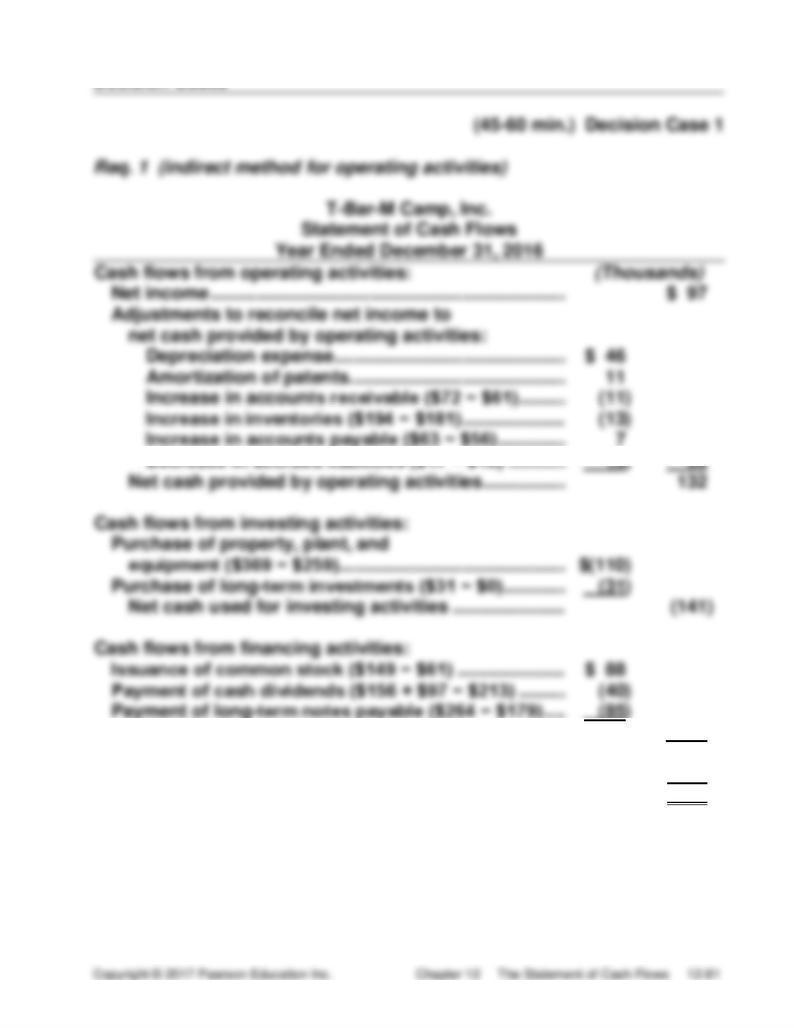

Net cash used for financing activities ......................

(37)

Net (decrease) in cash ......................................................

$ (46)

Cash balance, December 31, 2015 ...................................

63

Cash balance, December 31, 2016 ...................................

$ 17

(continued) Decision Case 1

Req. 2

The cash balance at the end of 2016 is low because:

• The camp paid $110,000 to buy new property, plant, and

equipment.

• The camp paid off $85,000 of notes payable.

(15-25 min.) Decision Case 2

4. Four-Star is raising more cash by selling stock than Applied is. This

gives Four-Star more cash to invest in research and development of

new products and other innovations to enhance the company’s

competitiveness. Applied, on the other hand, is paying off debt. That

is not necessarily bad for Applied, but Four-Star appears to be a step

ahead in terms of financing its operations with stockholders’ equity

and investing the cash in income-producing assets.

Ethical Issue

Req. 1

Cash flows from operating

activities:

Without

Reclassification

With

Reclassification

Net income ...........................

$ 37,000

$37,000

Increase in accounts

receivable .............................

(80,000)

—

Net cash (used for) provided

by operating activities ..............

$(43,000)

$37,000

Columbia looks better with the reclassification because net

cash flow from operations is positive.

Req. 2

The issue is whether or not it is ethical to reclassify accounts receivable

from current assets to long-term assets.

Req. 3 and Req. 4

The stakeholders are Columbia, its officers, directors and employees, as

well as their present and future creditors and stockholders.

Economic analysis: The plan to reclassify accounts receivable would

have an immediate positive impact on Columbia and its employees

because it might enable Columbia to obtain the loan it desperately

needs. However, this might be to the detriment of present and future

creditors, because if Columbia can’t collect the receivables, it may not

be able to pay off its loans to creditors.

(continued) Ethical case

Legal analysis: To reclassify receivables when, in fact, they are not truly

collectible, even in the long run, might leave the company open later to a

lawsuit for damages suffered by creditors who loan Columbia money

based on false information.

Ethical analysis: To reclassify receivables when, in fact, they are not

truly collectible in the long run, deprives the banks of accurate

information they need to make sound financial decisions.

Reclassification would be unethical if Columbia expects to collect within

the current period. In that case, the reclassification would appear to be

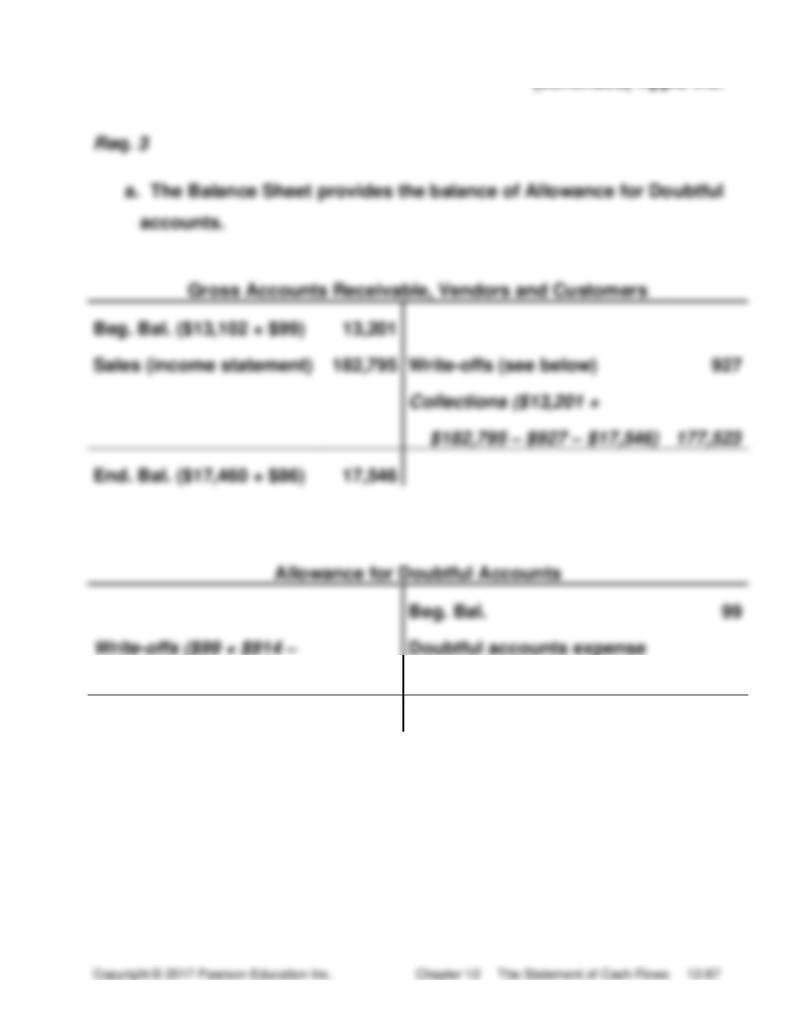

Focus on Financials: Apple Inc.

(continued) Apple Inc.

$86)

927

($182,795 x .005)

914

End. Bal.

86

(continued) Apple Inc.

b. Using the format provided in Exhibit 12-15: (Amounts in millions)

Payments for

=

Cost of

+

Increase in

−

Increase in

inventory

sales

Inventory

Accounts Payable

$104,776

=

$112,258

+

$347

−

$7,829

($2,111 − $1,764)

($30,196 - $22,367)

Payments

for other

=

Other

operating

+

Increase in

−

Increase in

operating

expenses

expenses

Prepaid Assets

Accrued Liabilities

$16,361

=

$18,034

+

$2,924

−

$4,597

($9,806 − $6,882)

($18,453 - $13,856)

Other operating expenses include Depreciation and Amortization

Expense of $7,946 million, so these expenses should be deducted.

Payments for other operating expenses = $16,361 million – $7,946 million

= $8,415 million.

Total

payments

to Suppliers

Payments for

inventory

+

Payments for

other operating

expenses

$113,191

=

$104,776

+

$8,415

(continued) Apple Inc.

Focus on Analysis: Under Armour, Inc.

3. An addition to net income for depreciation and amortization, $72

million, indicates cash flow provided by operations was greater

than net income. Depreciation reduces income but not cash and is

added back to net income.

(continued) Under Armour, Inc.

Req. 3

In 2014, Under Armour’s additions to property, plant, and equipment

were more than previous years’ additions. This is evident in the

investing section of the statement of cash flows where capital spending

in 2014 ($140 million) was more than in 2013 ($88 million) and 2012 ($51

million). The company does not report the sale of fixed assets.

Req. 4

The largest item in Under Armour’ financing section of their

consolidated statement of cash flows is the proceeds from its term loan.

This reveals that the company strategy is to expand through additional

Group Projects