Chapter 4

Internal Control & Cash

Ethics Check

(5-10 min.) EC 4-1

a. Integrity

b. Objectivity and independence

c. Integrity

Short Exercises

1. Motive — Fraud generally results from either critical need or greed on

3. Rationalization — The perpetrator(s) is (are) convinced, in their own

(5 min.) S 4-2

Alston should report the errors to Golden because Golden is Alston’s

(10 min.) S4-3

A computer virus enters program code without your consent and

performs destructive action to your computer files or programs.

A Trojan Horse is a malicious computer program that hides inside a

legitimate program and works like a virus to corrupt your computer files

or programs.

(5-10 min.) S 4-4

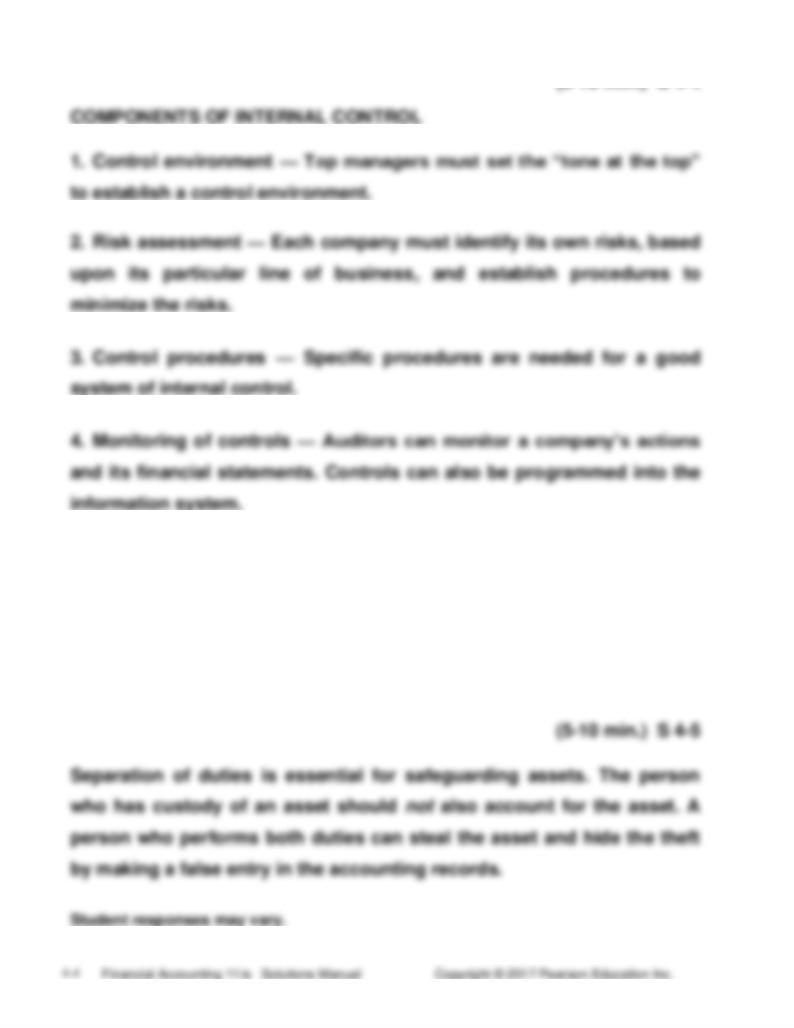

5. Information system — Accurate information is essential for success

in business. Accounting information enters and exits through the

information system.

Student responses may vary for the descriptions.

(5-10 min.) S 4-6

1. Smart hiring practices. The company should be careful to hire both

2. Comparisons and compliance monitoring. No person or department

should be allowed to completely process a transaction from beginning

3. Adequate records help to assure that sufficient hard copy documents

or electronic information is kept by the entity to support the validity of

4. Limited access goes hand in hand with separation of duties to assure

that only authorized individuals are allowed access to (a) the assets of

(continued) S 4-6

5. Proper approvals. No transaction should be processed without

management’s general or specific approval. Generally, the larger the

transaction, the higher the organizational level of approval necessary.

Notice that the first letters of these attributes spell the acronym SCALP.

That’s an easy and comprehensive way to remember the control

procedures involved in internal controls.

(20-30 min.) S 4-8

Punching a hole through supporting documents reduces the

opportunity for fraud. Without this control procedure, a dishonest

employee could resubmit documents for payment a second time. The

employee could change the payee’s address and have the check sent

to an address the employee controls. Or the employee could arrange

to have the second payee split the payment with the employee.

Canceling the documents makes it difficult to get approval for a

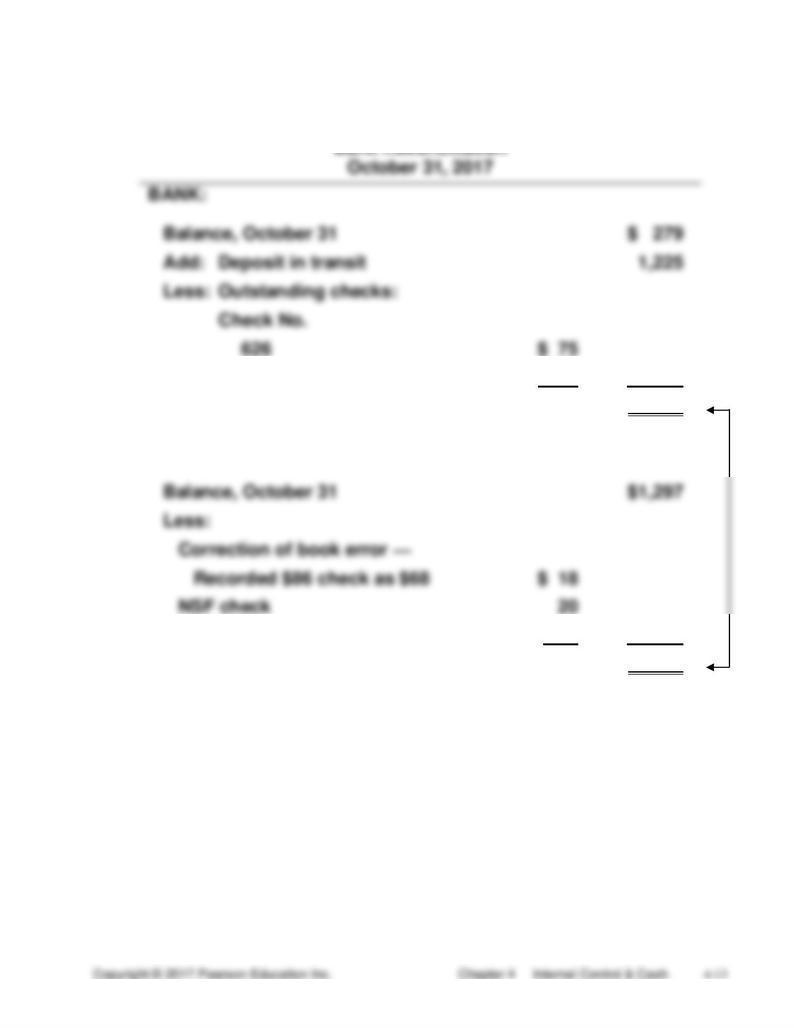

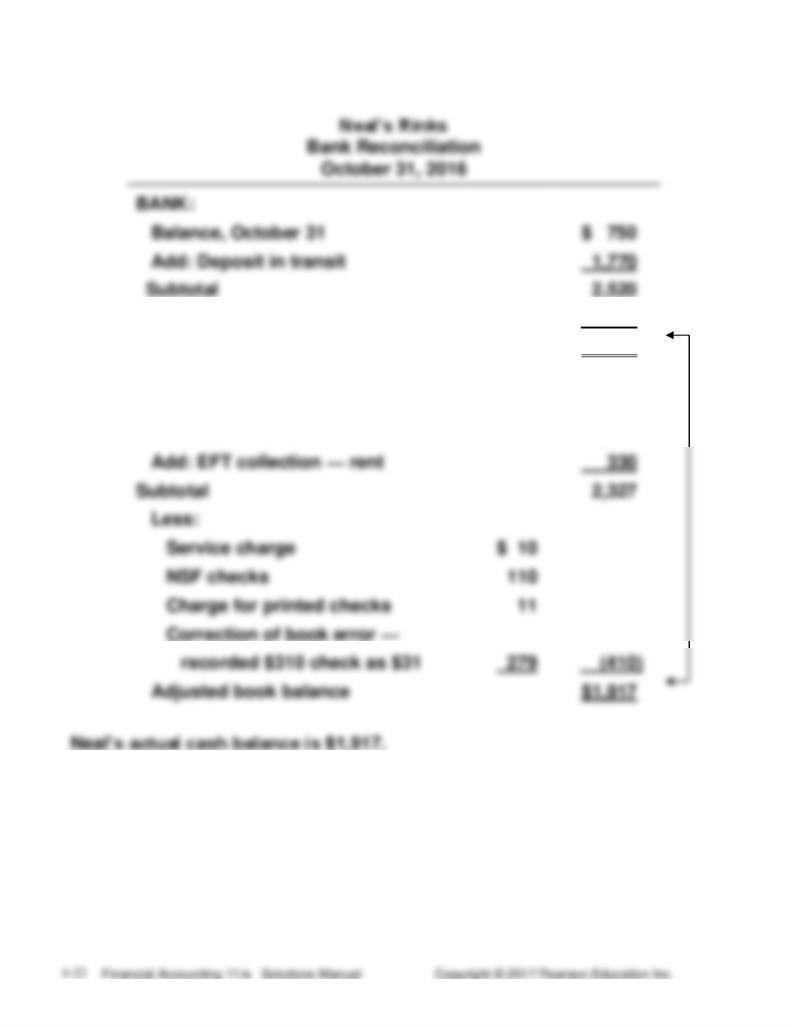

(10 min.) S 4-9

NSF check

(45)

Adjusted bank balance

$4,183

Adjusted book balance

$4,183

Rampart has cash of $4,183.

(5 min.) S 4-10

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

Aug.

31

Cash………………………………………..

691

(5 min.) S 4-11

It appears that the employee has stolen $765 (adjusted book balance,

$4,755 − adjusted bank balance, $3,990). The adjusted bank balance is

1. Paying by check carries three controls over cash:

2. A dishonest purchasing agent could:

• Purchase goods and have them delivered to his home or other location

that he controls.

• Approve payment by the company for goods that he spent too much on,

and then split the excess with the supplier.

Companies avoid this internal control weakness by separating the

following duties related to the purchase of, and payment for, goods:

• purchasing goods

• receiving goods

(5-10 min.) S 4-14

Budgeted cash balance needed

(11)

Cash available for additional investments

$ 4

(5 min.) S 4-15

Exercises

(10-15 min.) E 4-16A

a. Sweitzer has access to the cash collected, and she also prepares the

cash report. With access to both items, Sweitzer can steal cash and

falsify her cash report to conceal her theft.

b. Li prepares the purchase order and also receives the goods. She can

add some items to the purchase order and have these extra items

shipped to a location she controls. When the goods come in, she

checks the incoming shipment, so there’s no outside party to learn of

her dishonesty.

Student responses may vary.

(10 min.) E 4-17A

Cash payments:

a. Strong internal control. There is a good separation of duties.

Supervisors request equipment, and the home office purchases the

equipment.

(10 min.) E 4-18A

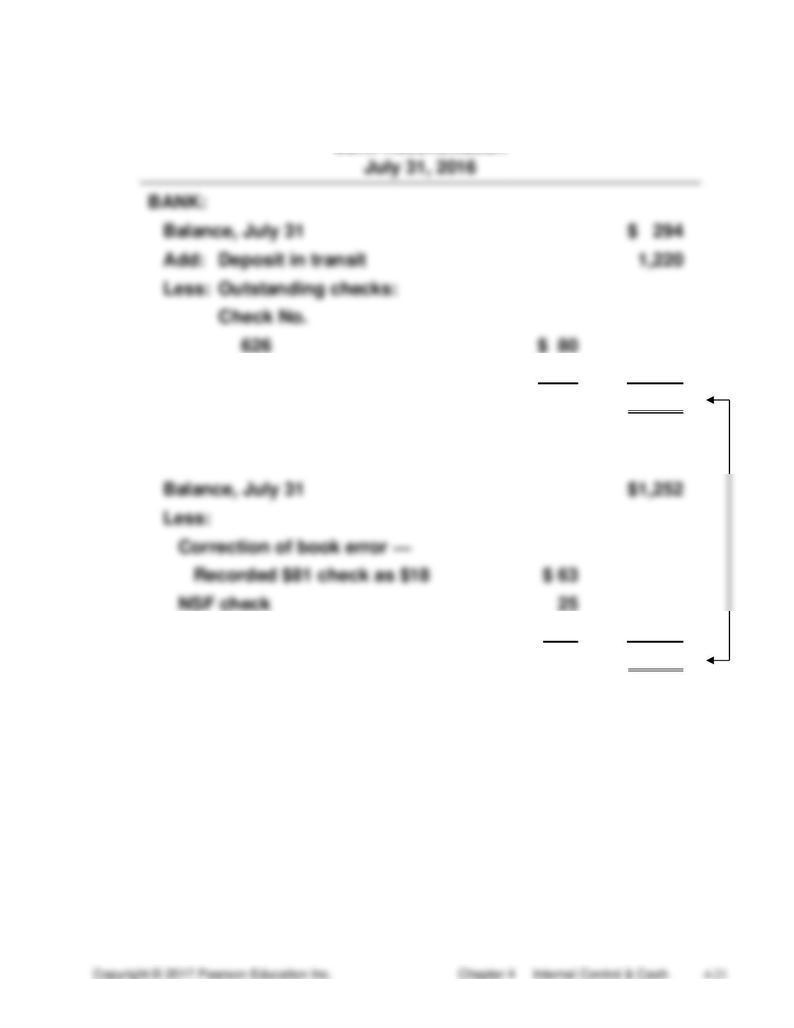

(10-20 min.) E 4-19A

F.L. Hardy

627

175

(250)

Adjusted bank balance

$1,254

BOOKS:

Service charge

5

(43)

Adjusted book balance

$1,254

(10-20 min.) E 4-20A

Less: Outstanding checks

(610)

Adjusted bank balance

$1,920

BOOKS:

Balance, March 31

$1,980

(10-15 min.) E 4-21A

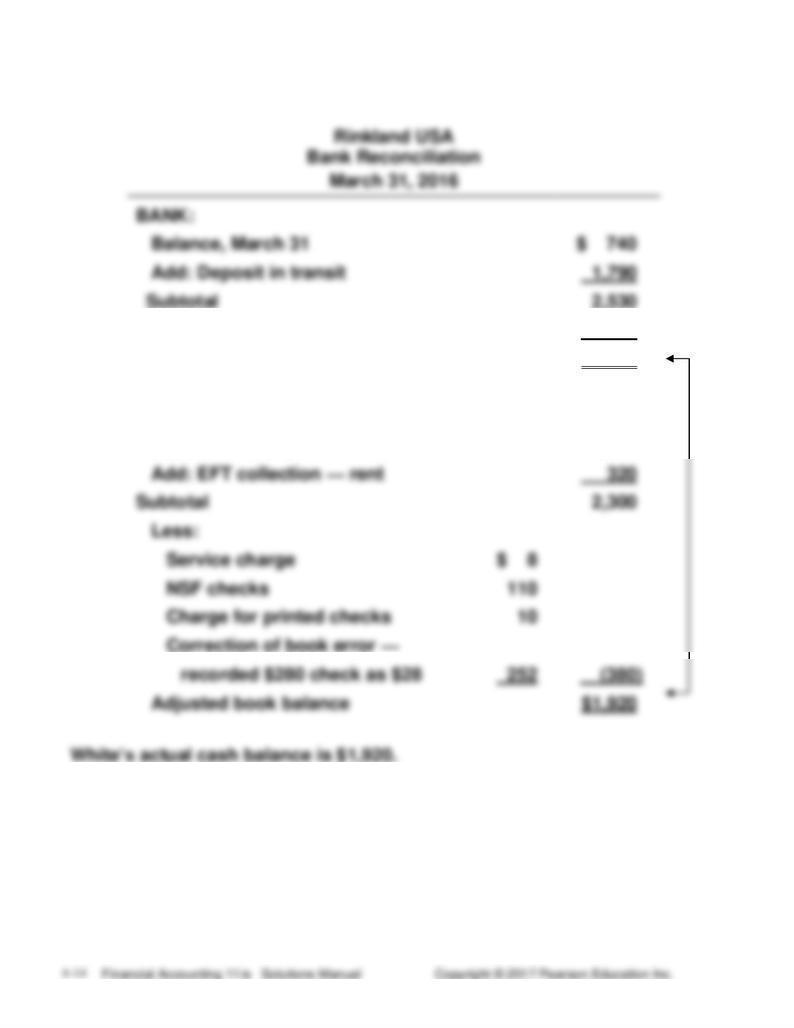

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

Mar.

31

Cash .............................................................

320

Rent Revenue .........................................

320

EFT collection of rent.

31

Miscellaneous Expense ($8 + $10) .............

18

Cash ........................................................

18

Bank service charge and charge

for printed checks.

31

Accounts Receivable ..................................

110

(10-15 min.) E 4-22A

(10-15 min.) E 4-23A

The main internal control weakness is that the payroll department both

prepares and distributes the paychecks. With both duties, a dishonest

person in the payroll department can create a time sheet for a fictitious

employee and then keep the related paycheck after the treasurer returns

the signed checks to the payroll department.

To correct this weakness, Linus Manufacturing should have someone

other than the payroll department or the shop foreman distribute

paychecks to employees. For example, the human resources

department, which has no control over the time sheets or the paychecks,

could distribute paychecks to the workers.

(20-30 min.) E 4-24A

(10-15 min.) E 4-25B

a. Morrison has access to the cash collected, and she also prepares the

cash report. With access to both items, Morrison can steal cash and

falsify her cash report to conceal her theft.

b. Peterson prepares the purchase order and also receives the goods.

She can add some items to the purchase order and have these extra

items shipped to a location she controls. When the goods come in,

she checks the incoming shipment, so there’s no outside party to

learn of her dishonesty.

Student responses may vary.

(10 min.) E 4-26B

Cash payments:

a. Strong internal control. There is a good separation of duties.

Supervisors request equipment, and the home office purchases the

equipment.

b. Weak internal control. Supervisors both request, purchase, and pay

(10 min.) E 4-27B

(10-20 min.) E 4-28B

F. L. Hill

Bank Reconciliation

627

280

(360)

Adjusted bank balance

$1,154

BOOKS:

Service charge

10

(98)

Adjusted book balance

$1,154

(10-20 min.) E 4-29B

Less: Outstanding checks

(603)

Adjusted bank balance

$1,917

BOOKS:

Balance, October 31

$1,997

(10-15 min.) E 4-30B

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

Oct

31

Cash .........................................................

330

Rent Revenue .....................................

330

EFT collection of rent.

31

Miscellaneous Expense ($10 + $11) .......

21

Cash ....................................................

21

Bank service charge and charge

for printed checks.

31

Accounts Receivable ..............................

110

(10-15 min.) E 4-31B

(10-15 min.) E 4-32B

The main internal control weakness is that the payroll department both

prepares and distributes the paychecks. With both duties, a dishonest

person in the payroll department can create a time sheet for a fictitious

employee and then keep the related paycheck after the treasurer returns

the signed checks to the payroll department.

To correct this weakness, Greentown Company should have someone

other than the payroll department or the shop foreman distribute

paychecks to employees. For example, the human resources

department, which has no control over the time sheets or the paychecks,

could distribute paychecks to the workers.

(20-30 min.) E 4-33B

Quiz

Q4-45

d

Problems

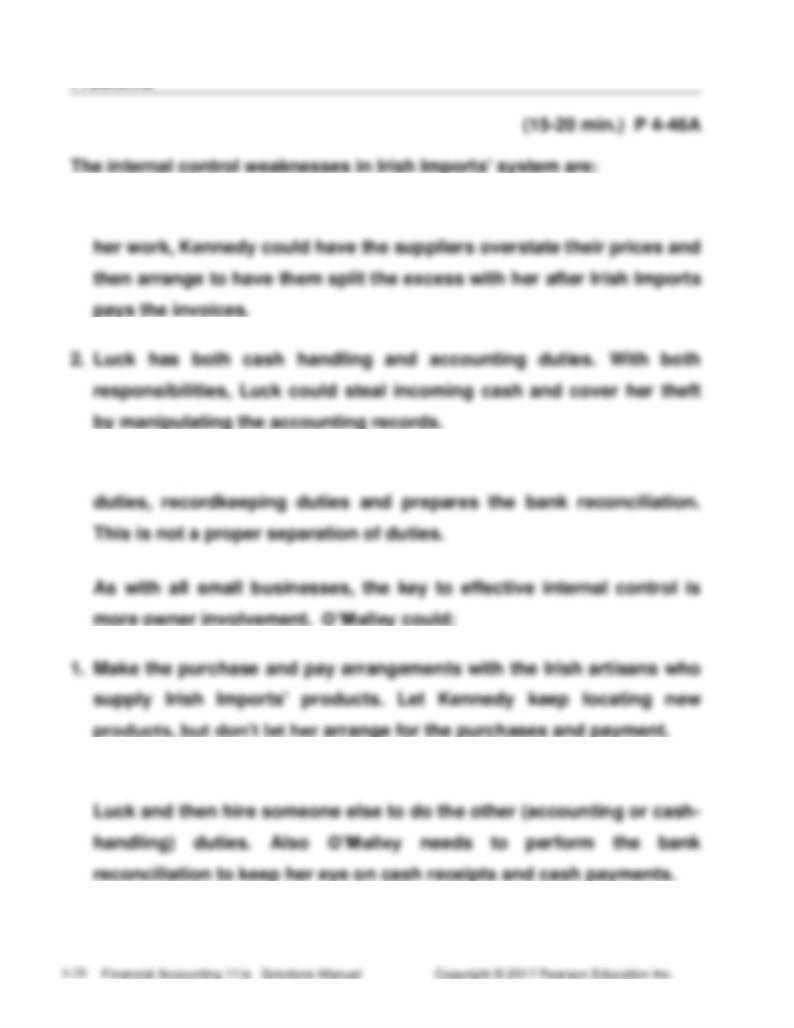

1. Kennedy controls the content of the invoices. With no supervision of

3. Luck prepares the bank reconciliation. Luck has cash handling

2. O’Malley could assign either cash handling or accounting duties to

(10-20 min.) P 4-47A

Requirement 1

Requirement 2

Requirement 3

Missing Internal

Control

Characteristic

Possible Problem

Solution

a.

Separation of

duties

Theft of diamonds

— the purchasing

agent could have

diamonds sent to a

location he controls.

Separate

purchasing,

approval, and

check-signing

duties.

b.

Assignment of

responsibility

Lost revenue, because

too many employees

are managing the office

and neglecting their

duties.

Assign a single

employee to

manage the office

when the owner is

absent.

c.

Separation of

duties

Theft of cash.

Separate

accounting and

cash-handling

duties.

(continued) P 4-48A

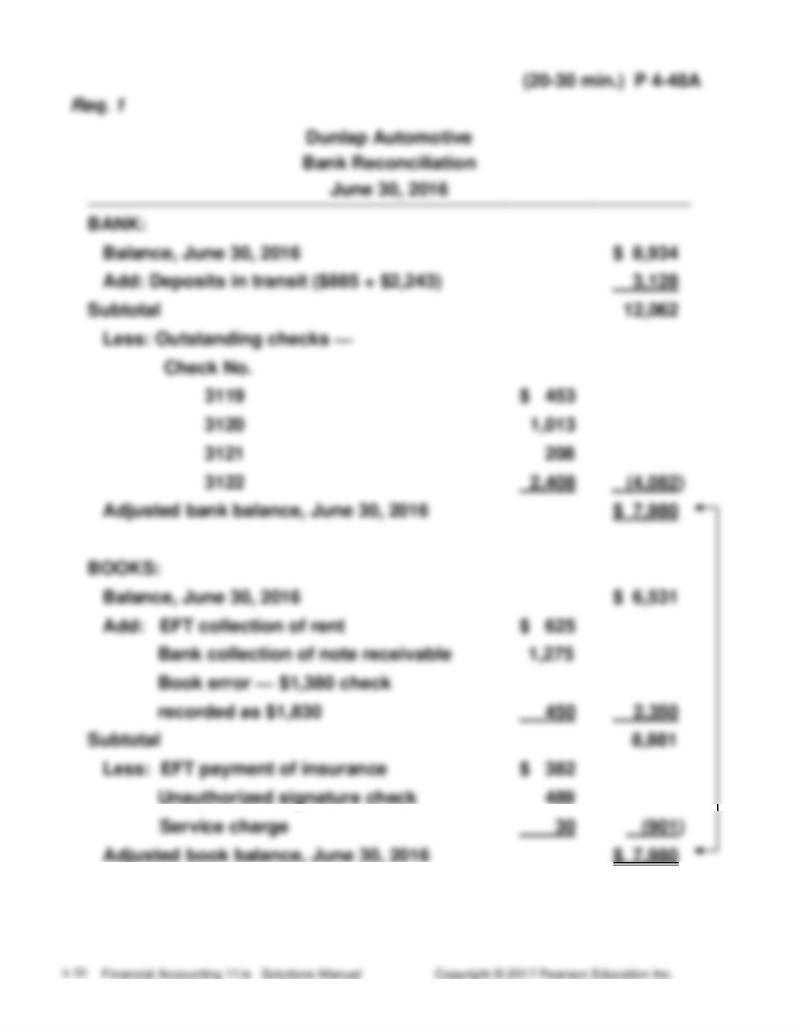

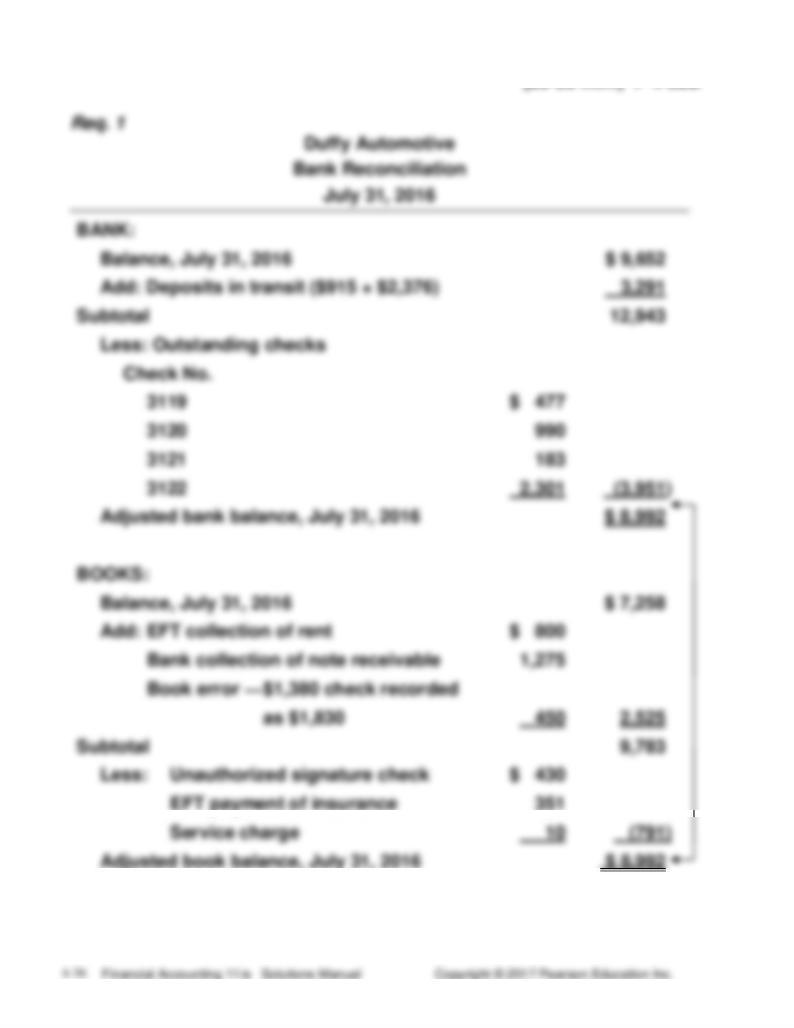

Req. 2 (entries based on the reconciliation)

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

June

30

Cash ...................................................................

625

Rent Revenue ..............................................

625

EFT deposit for rent revenue earned.

30

Cash ...................................................................

1,275

Note Receivable ..........................................

1,275

Note receivable collected by bank.

30

Cash ...................................................................

450

Accounts Payable .......................................

450

Correction for check #3115 recorded

incorrectly.

30

Insurance Expense ...........................................

382

(continued) P 4-48A

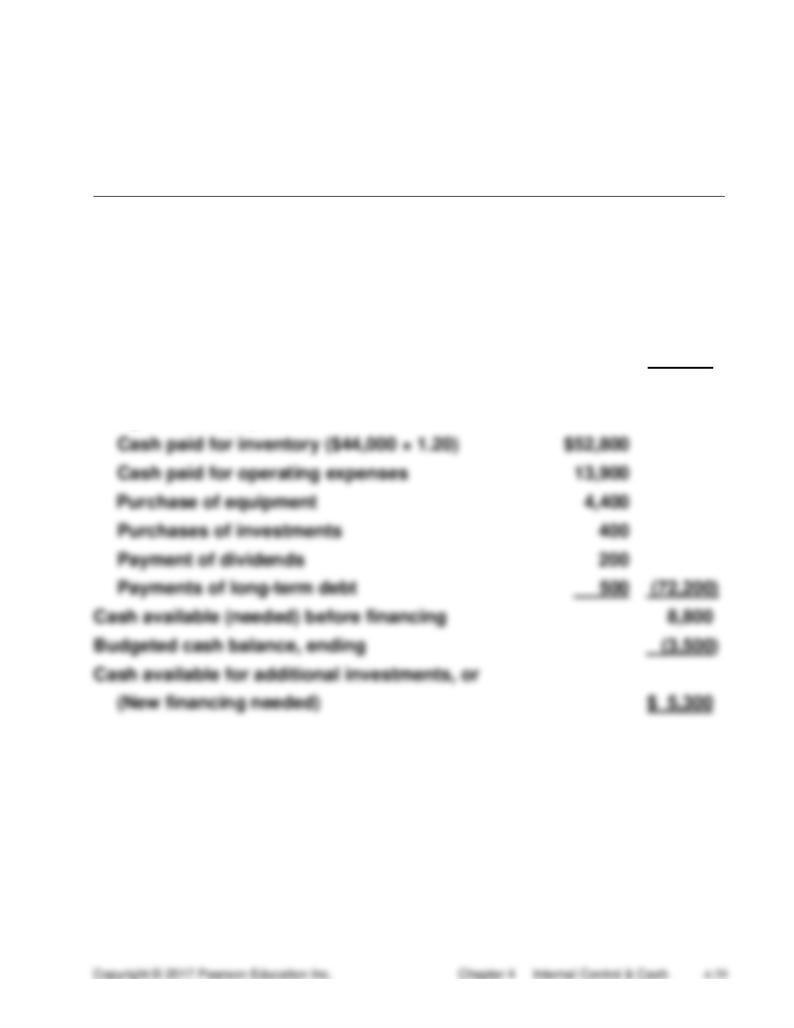

(30-45 min.) P 4-49A

Keller Wireless

Cash Budget

2017

Thousands

Cash balance, beginning

$ 8,100

Budgeted cash receipts:

Collections from customers ($66,000 × 1.14)

75,240

Receipt of interest

600

83,940

(15-20 min.) P 4-50B

1. Martin controls the content of the invoices. With no supervision of her

3. Moore prepares the bank reconciliation. Moore has cash handling

2. Gustafson could assign either cash handling or accounting duties to

(10-20 min.) P 4-51B

Requirement 1

Requirement 2

Requirement 3

Missing Internal

Control

Characteristic

Possible Problem

Solution

a.

Separation of duties

Theft of cash or

diamonds by the

purchasing agent.

Have a manager, not

the purchasing agent,

approve invoices for

payment and sign the

checks.

b.

Assignment of

responsibilities

Lost revenue due to

delay of architectural

drawings.

Assign one senior

architect to fulfill

management duties

while Hixson is absent.

Other senior architect

should focus on

producing architectural

drawings.

c.

Separation of duties

Theft of cash.

Keep accounting and

cash handling duties

separate.

(20-30 min.) P 4-52B

(continued) P 4-52B

Req. 2 (entries based on the reconciliation)

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

July

31

Cash ...................................................................

800

Rent Revenue ...............................................

800

EFT deposit for rent revenue.

31

Cash ...................................................................

1,275

Note Receivable ...........................................

1,275

Note receivable collected by bank.

31

Cash ...................................................................

450

Accounts Payable ........................................

450

Correction for check #3115 recorded

incorrectly.

31

Accounts Receivable ........................................

430

(continued) P 4-52B

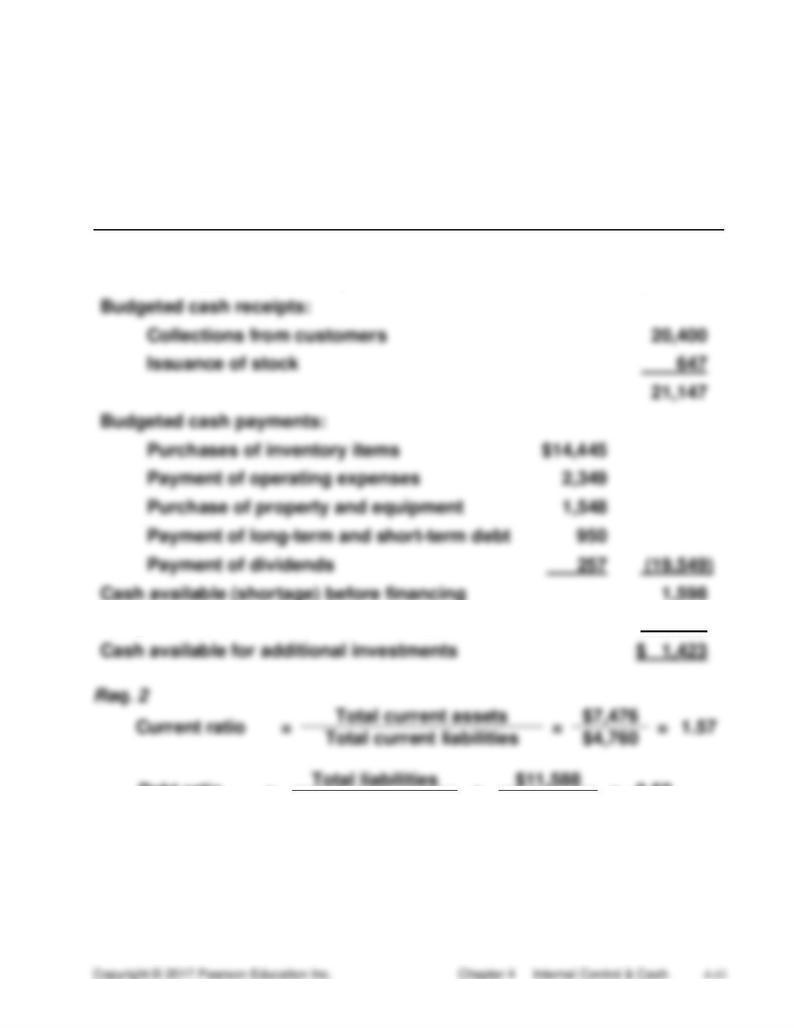

(30-45 min.) P 4-53B

Carvel Wireless

Cash Budget

2017

Cash balance, beginning

$ 7,900

Budgeted cash receipts:

Collections from customers ($65,000 × 1.12)

72,800

Receipt of interest

300

81,000

Budgeted cash payments:

Challenge Exercises and Problem

2.

Submitting purchase invoices a

second time for duplicate

payment, perhaps altering the

2.

authenticity and comparing

invoices to receiving reports to

3.

Paying suppliers excess

3.

Comparing the business’s ratio

(20-30 min.) E 4-55

Req. 1

Dollar Depot, Inc.

Cash Budget

Year Ended December 31, 2017

Thousands

Cash balance, December 31, 2016

$ 100

Budgeted cash balance, December 31, 2017

(175)

Debt ratio

=

=

=

0.52

Total assets

$22,177

Req. 3

Dollar Depot will have cash available for additional investments and

should not need to borrow.

(20-30 min.) P 4-56

The Parkview Company

Bank Reconciliation

December 31

BANK:

Balance, December 31

$ 3,936

Add: Deposit in transit

Actual amount of December 30 deposit

670

Subtotal

4,606

(continued) P 4-56

Checks No. 1880, 1882, and 1883 were outstanding in November so

should not also be deducted from Cash in December. The unexplained

difference of $3,638* consists of: $1,138 erroneous November

outstanding checks and the $2,500 difference between deposit in transit

listed on the original reconciliation and the amount of the deposit in

transit listed on the books. It is possible that the $4,000 difference

between the December 23 deposit on the books and the December 24

receipt on the bank statement was intentional and used to cover up the

missing cash.

Decision Cases

(20-30 min.) Decision Case 1

NSF check

36

(44)

Adjusted book balance, September 30

$10,558

(continued) Decision Case 1

1. The bookkeeper should not handle incoming mail. The mailroom

2. The bookkeeper should not make bank deposits. The treasurer

should have the cashier deposit the checks in the bank.

(15-30 min.) Decision Case 2

(continued) Decision Case 2

3. Don’t allow Pickins to pass out paychecks. Have employees pick up

6. Have a home-office employee go to the construction site occasionally

7. Have employees deliver or mail time sheets to home office.

Ethical Issues

2. What are the alternatives? Require the client to record the loss, or

3. Identify the stakeholders. The auditor, the bank, and the public at

large can be affected. The auditor’s reputation is on the line. The

bank’s financial statements are in question. The public, including

creditors and investors, can be affected if the bank issues financial

statements that include erroneous amounts.

Assess the possible outcomes. If the auditors require the bank to

record the loss, the auditor will keep his or her reputation intact. But

(continued) Ethical Issue 1

4. Make the decision. The auditor should require the bank to record the

loss even if that means losing the bank as a client. By sticking to his

or her belief that the bank should record the loss, the auditors’

Ethical Issue 2

1. Identify the ethical issue. Galvin’s ethical issue is whether to use his

knowledge of The Salvation Army’s plans and of Nadar’s situation to

either party’s advantage (or disadvantage). Should Galvin help The

Salvation Army buy the land at the lowest price? Should he help

Nadar sell the land at the highest price? Galvin’s position presents

2. What are the alternatives? There are several:

(a) Let other members of the Salvation Army board of directors

know of Nadar’s situation in order to help The Salvation Army

buy the land at a bargain price.

(b) Disclose Nadar’s situation to fellow board members and insist

3. Identify the stakeholders involved. Galvin, The Salvation Army,

(continued) Ethical Issue 2

fellow board members. This would help The Salvation Army and hurt

Nadar, relative to her ability to sell the land at market value of $3.6

million. Insisting that The Salvation Army offer market price for the

land would seem fair to both parties, but that would betray the trust of

Nadar. And it may or may not sway the board to go along with a $3.6

million offer for the land.

4. Make the decision. The authors would take the leave of absence and

hope other Salvation Army board members do not probe Galvin’s

Ethical Issue 3

2. What are the alternatives?

3. Identify the stakeholders involved. IMS, Snicker Foods, Community

Bank, and everyone connected to these organizations — owners,

4. Make the decision. French should not tell IMS of Snicker’s financial

difficulties (after all, Snicker isn’t bankrupt yet). French should let

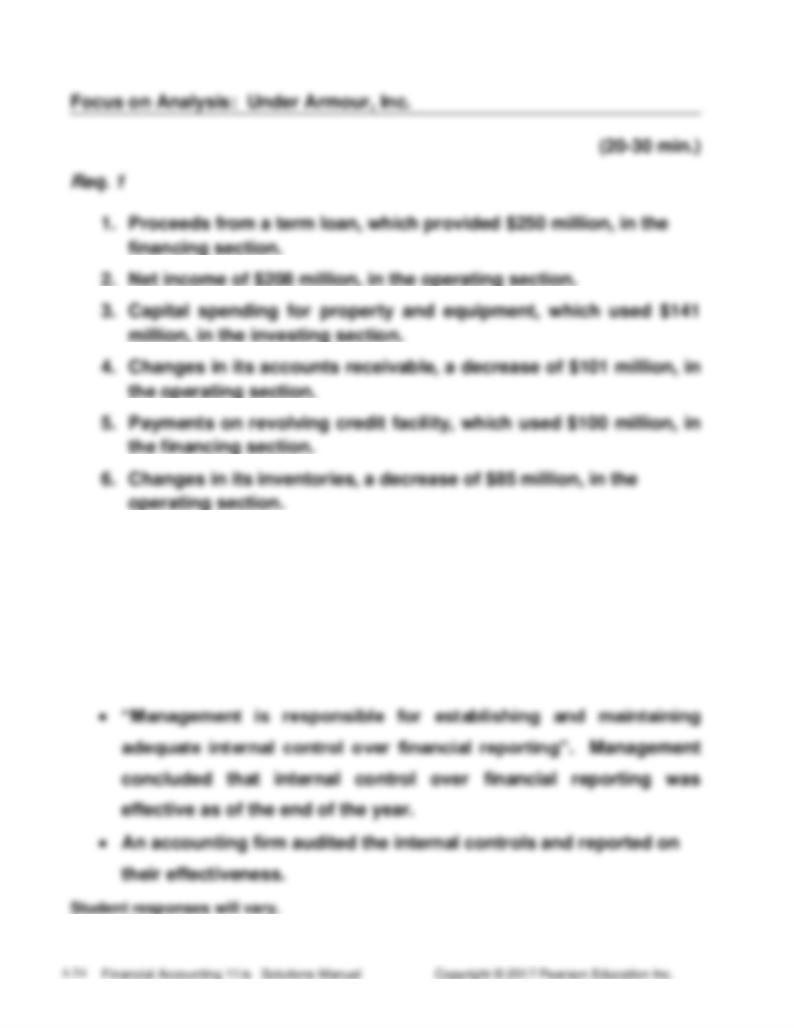

Focus on Financials: Apple Inc.

(20-30 min.)

Req. 1

Cash equivalents include assets that are slightly less liquid than cash,

but similar enough to be reported together. Cash equivalents must be

readily convertible to known amounts of cash and close to maturity (with

an original maturity of three months or less at the time of purchase).

Req. 2

Apple Inc. includes in its cash equivalents highly liquid instruments with

an original maturity of three months or less at the time of purchase.

7. Depreciation and amortization, which provided $72

million. Actually, these expenses do not use cash, so they are

added back to income to arrive at cash provided by operations.

Req. 2

The following items from the report are also mentioned in the chapter:

Group Project