Chapter 7

Plant Assets, Natural Resources, &

Intangibles

Ethics Check

(5-10 min.) EC 7-1

a. Integrity

Short Exercises

1. Red Rock reported Buildings and leasehold improvements of

$2,219,767 (thousand) and Fixtures and equipment of $1,674,089

2.

Cost = $4,048,650 thousand

Book value = $2,194,687 thousand

Book value is less than cost because accumulated depreciation is

subtracted from cost to compute book value.

(5 min) S 7-2

(10-15 min.) S 7-4

1. First-year depreciation:

Straight-line ($56,700,000 − $4,700,000) / 5 years .............

$ 10,400,000

Units-of-production $10.40/mile* × 775,000 miles ............

$ 8,060,000

Double-declining-balance ($56,700,000 × 40%) ................

$22,680,000

2. Book value:

Straight-

Line

Units-of-

Production

Double-

Declining-

Balance

(10 min.) S 7-5

1. Double-declining-balance (DDB) depreciation offers the tax

2.

DDB depreciation .....................................................

$22,680,000

(5-10 min.) S7-6

$25,000 / 4 years = $6,250 / year, straight-line depreciation

Depreciation Accumulated Book

Expense Depreciation Value

2015: $6,250 $ 6,250 $18,750

2016: 6,250 12,500 12,500

2017: 6,250 18,750 6,250

2018: 6,250 25,000 -0-

(5-10 min.) S 7-7

$25,000 / 200,000 miles = $.125 / mile, units-of-production depreciation

Depreciation Accumulated Book

Miles Expense Depreciation Value

2015: 60,000 $7,500 $ 7,500 $17,500

2016: 65,000 8,125 15,625 9,375

2017: 40,000 5,000 20,625 4,375

2018: 35,000 4,375 25,000 -0-

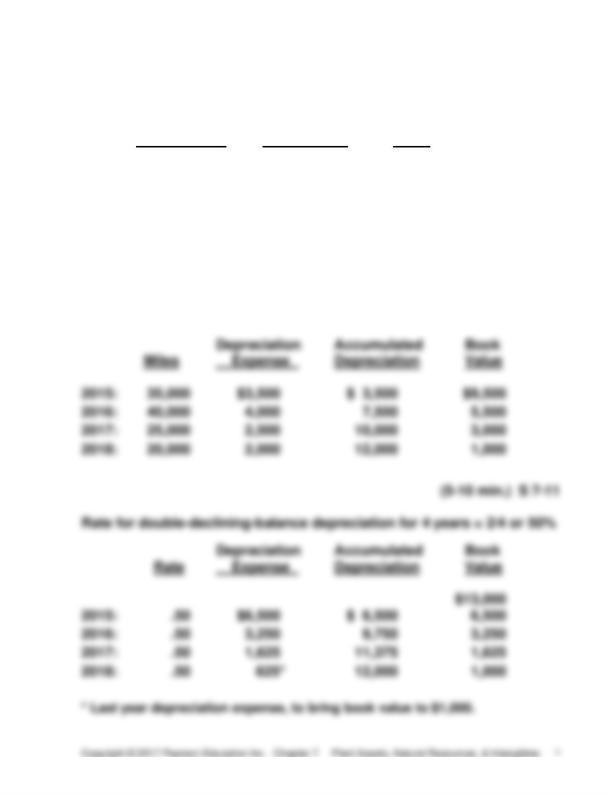

(5-10 min.) S 7-8

Rate for double-declining-balance depreciation for 4 years = 2/4 or 50%

Depreciation Accumulated Book

Rate Expense Depreciation Value

$25,000

2015: .50 $12,500 $12,500 12,500

2016: .50 6,250 18,750 6,250

2017: .50 3,125 21,875 3,125

2018: .50 3,125* 25,000 -0-

* Remaining book value is the last year depreciation expense, to bring book

value to -0-.

(5-10 min.) S 7-9

($13,000 — $1,000) / 4 years = $3,000 / year, straight-line depreciation

Depreciation Accumulated Book

Expense Depreciation Value

2015: $3,000 $ 3,000 $10,000

2016: 3,000 6,000 7,000

2017: 3,000 9,000 4,000

2018: 3,000 12,000 1,000

(5-10 min.) S 7-10

($13,000 — $1,000) / 120,000 miles = $.10 / mile, units-of-production

depreciation

(5-10 min.) S 7-12

(5-10 min.) S 7-14

1. ($920,000 − $70,000) / 5 years × 2 = $340,000

Loss on sale of machinery:

Sale price of machinery .........................................

$ 250,000

2.

2017

Oil Inventory .........................................................

11.7

(5-10 min.) S 7-16

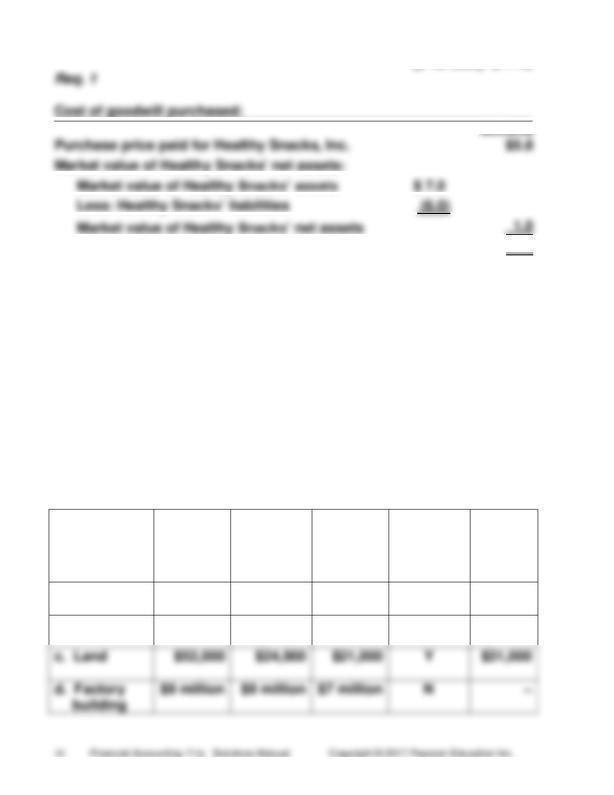

Cost of goodwill

$4.8

Req. 2

In future years Crunchies, Inc. will determine whether its goodwill has

been impaired. If the goodwill’s value has not been impaired, there is

nothing to record. But if goodwill’s value has been impaired,

Crunchies, Inc. will record a loss and write down the book value of the

goodwill.

(5-10 min.) S 7-17

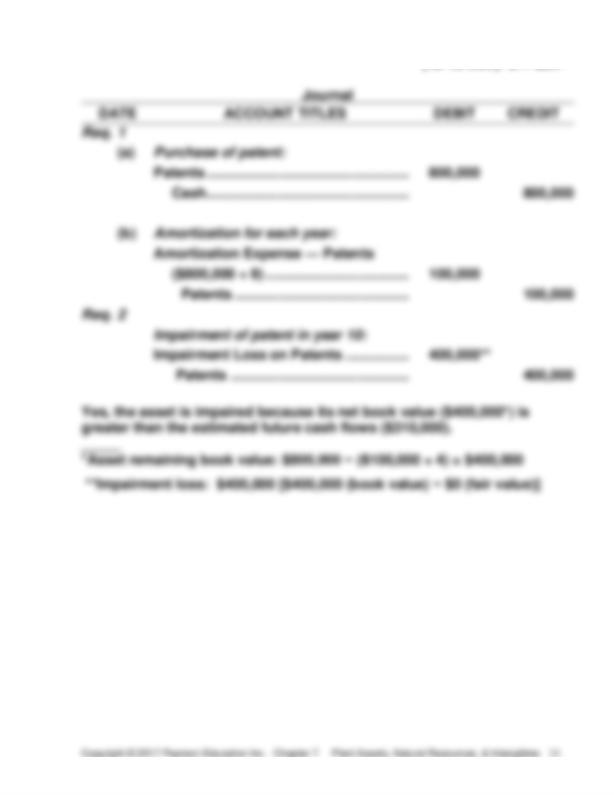

Asset

Book

Value

Estimated

Future

Cash

Flows

Fair

Value

Impaired?

(Y or N)

Amount

of Loss

a. Equipment

$180,000

$140,000

$100,000

Y

$80,000

b. Trademark

$320,000

$460,000

$375,000

N

–

(5 min.) S7-18

.077

X

1.955

=

15.1%

The net profit margin ratio improved slightly over 2015, and the asset

turnover improved from 2015 to 2016; these improvements caused the

ROA to increase.

(5 min.) S 7-20

Net cash (used in) investing activities ...........................

$(12.9)

Exercises

(5-10 min.) E 7-21A

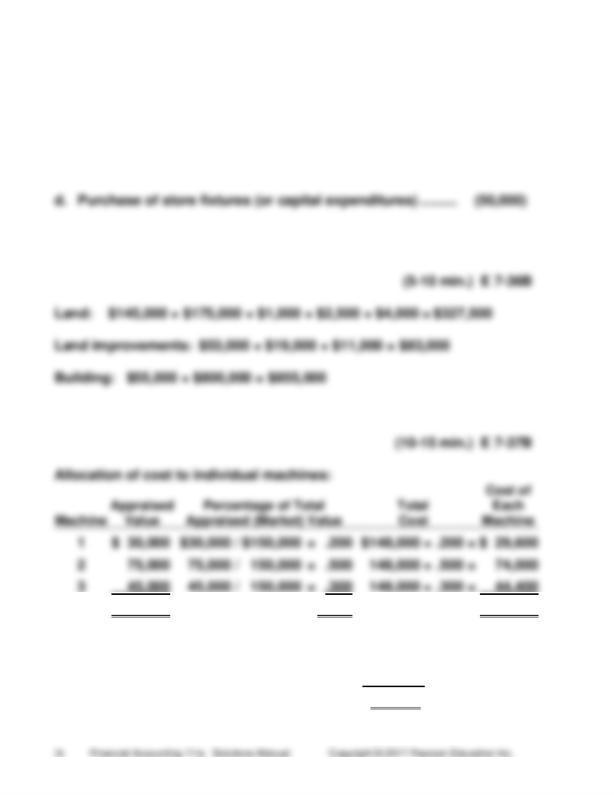

Land: $150,000 + $170,000 + $3,000 + $4,500 + $7,000 = $334,500

Land improvements: $48,000 + $19,000 + $10,000 = $77,000

Totals

$215,000

1.000

$209,000

Sale price of machine No. 3 ..........................

$21,500

Cost ................................................................

20,900

Gain on sale of machine ...............................

$ 600

(5-10 min.) E 7-23A

(a) Major overhaul

(b) Periodic lubrication

(c) Purchase price

(d) Training of personnel

Capital Expenditure

Immediate Expense

Capital Expenditure

Capital Expenditure

(e) Reinforcement to platform

(f) Transportation and insurance

(g) Ordinary recurring repairs

Capital Expenditure

Capital Expenditure

Immediate Expense

(h) Lubrication before machine is placed in

service

(i) Sales tax

Capital Expenditure

Capital Expenditure

(j) Installation

Capital Expenditure

(k) Income tax

Immediate Expense

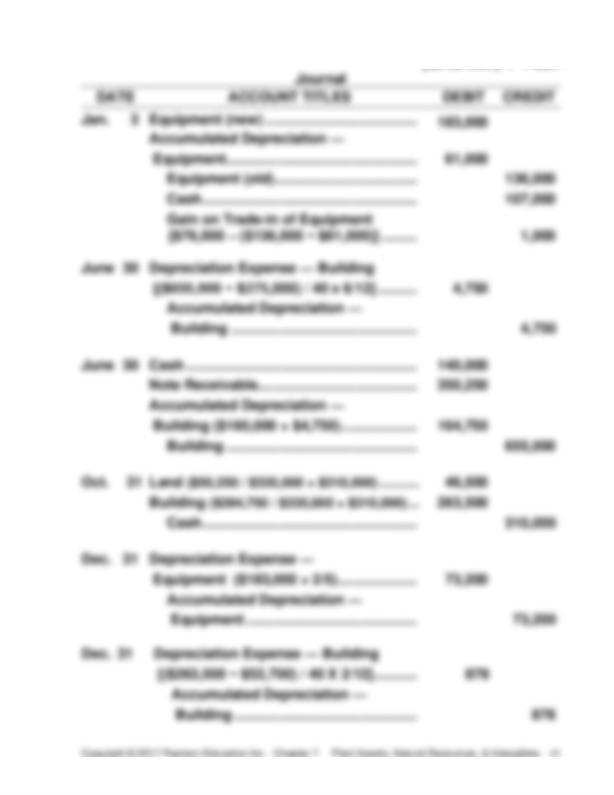

(15 min.) E 7-24A

Req. 1

Journal

ACCOUNT TITLES

DEBIT

CREDIT

a.

Land ....................................................................

485,000

Cash ..............................................................

485,000

b.

Building

($1,400 + $15,320 + $690,000 + $28,300) ...........

735,020

Note Payable .................................................

690,000

Cash ($1,400 + $15,320 + $28,300) ...............

45,020

c.

Depreciation Expense – Building .....................

5,686

Accumulated Depreciation – Building

($735,020 − $337,000) / 35 × 6/12 .................

5,686

Req. 2

BALANCE SHEET

Plant assets:

Land ..............................................................

$485,000

Building .........................................................

$735,020

Less Accumulated depreciation..................

(5,686)

Building, net .................................................

729,334

Req. 3

INCOME STATEMENT

Expense:

Depreciation expense ..................................

$ 5,686

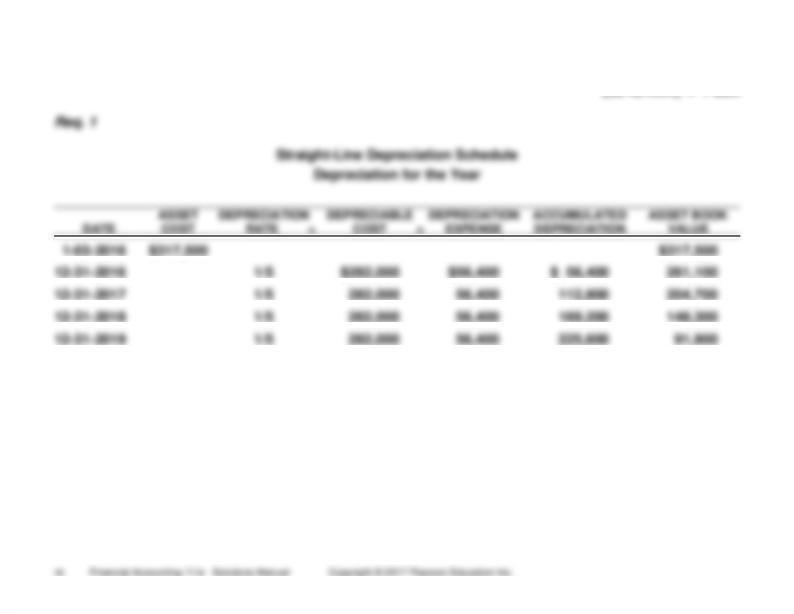

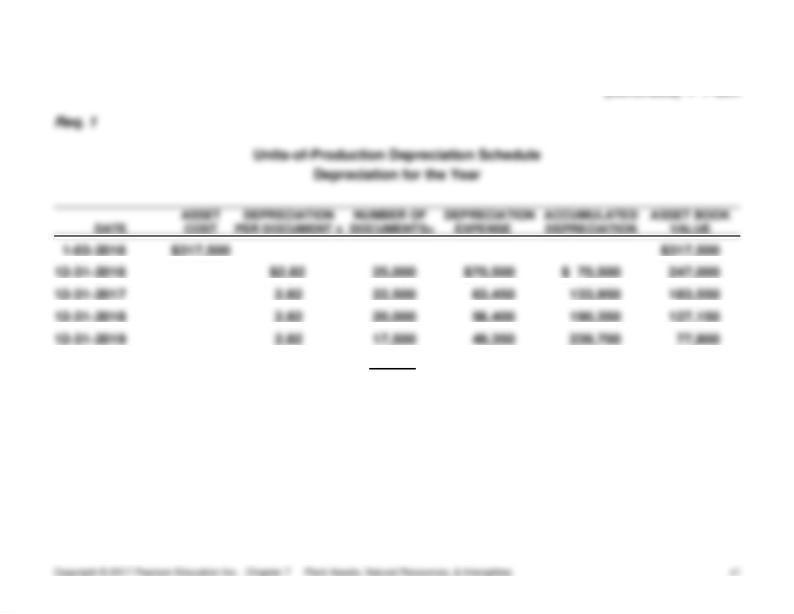

(15-20 min.) E 7-25A

Req. 1

Year

Straight-Line

Units-of-

Production

Double-Declining-

Balance

2016

$ 4,450

$ 7,000

$ 9,600

2017

4,450

5,125

4,800

2018

4,450

4,625

2,400

2019

4,450

1,050

1,000

$17,800

$17,800

$17,800

_____

Computations:

Straight-line: ($19,200 − $1,400) ÷ 4 = $4,450 per year.

Units-of-production: ($19,200 − $1,400) ÷ 71,200 miles = $.25 per mile:

2016

28,000

×

$.25

=

$7,000

2017

20,500

×

.25

=

5,125

2018

18,500

×

.25

=

4,625

(continued) E 7-25A

(15 min.) E 7-26A

(10-15 min.) E 7-27A

2. The journal entry on January 1, 2019 to record the sale:

Cash ..........................................................................................

400,000

Accumulated Depreciation – Machine ....................................

425,000

Loss on the Sale of Machine....................................................

95,000

Machine ...............................................................................

920,000

(15-20 min.) E 7-29A

Journal

DATE

ACCOUNT TITLES

DEBIT

CREDIT

2017

Depreciation for 8 months:

Aug.

31

Depreciation Expense – Fixtures ............

1,312*

Accumulated Depreciation —

Fixtures ..............................................

1,312

Sale of fixtures:

31

Cash ..........................................................

2,200

Accumulated Depreciation —

Fixtures ($3,280 + $1,312)......................

4,592

Loss on Sale of Fixtures .........................

1,408**

Fixtures ...............................................

8,200

_____

*2016 depreciation: $8,200 × 2/5 = $3,280

2017 depreciation: ($8,200 − $3,280) × 2/5 × 8/12 = $1,312

**Loss on sale of fixtures:

Sale price of old fixtures ........................................

$ 2,200

Book value of old fixtures:

Cost .....................................................................

$8,200

Less: Accumulated depreciation ($3,280 +

$1,312) ......................................................

(4,592)

(3,608)

Loss on sale ............................................................

$ (1,408)

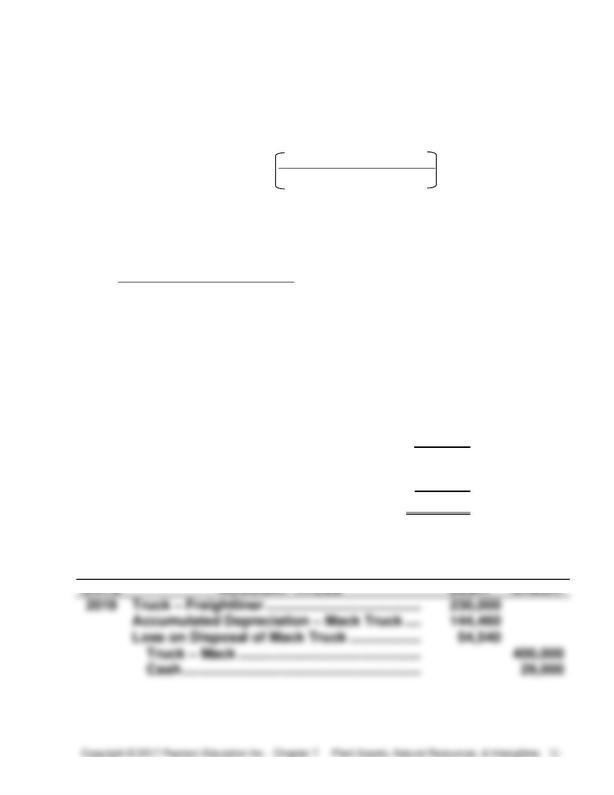

(10-15 min.) E 7-30A

Cost of old truck ............................................................

$400,000

Less: Accumulated depreciation:

($400,000 − $90,000) ×

85 + 165 + 175 + 41

(144,460)*

1,000

_______

Book value of old truck ................................................

$255,540

_____

aAlternate solution setup for accumulated depreciation:

($400,000 − $90,000)

=

$.31 per mile

1,000,000 miles

85,000 + 165,000 + 175,000 + 41,000 = 466,000 miles driven

Accumulated depreciation

=

466,000 miles × $.31

=

$144,460

Calculation of gain or loss:

Purchase price of Freightliner truck $230,000

Cash paid for Freightliner truck (29,000)

Trade-in value of Mack truck 201,000

Book value of Mack truck (255,540)

Net loss on disposal of Mack truck $ (54,540)

Journal

DATE

ACCOUNT TITLES

DEBIT

CREDIT

(10-15 min.) E 7-31A

(10-15 min.) E 7-32A

(5-10 min.) E 7-33A

Less: Burton Industries’ liabilities .........................

(29)

Market value of Burton Industries’ net assets ......

3

Cost of goodwill ..........................................................

$16

Req. 2

Journal

DATE

ACCOUNT TITLES

DEBIT

CREDIT

Current Assets ................................................

15

Long-Term Assets ..........................................

17

Goodwill ..........................................................

16

Liabilities ..................................................

29

(5-10 min.) E 7-34A

=

4.80%

=

4.48%

Net sales

$75,000

$73,600

=

1.25

=

1.24

Average total assets

$60,000

$59,400

or

4.80% x 1.25

=

6.00%*

4.48% x 1.24

=

5.56%*

The return on assets improved from 2014 to 2015; the increase in the

net profit margin ratio was mostly responsible for this.

_____

*difference due to rounding

(10 min.) E 7-35A

a.

Proceeds from sale of building (or disposal of building) ..

$650,000

b.

Insurance proceeds from fire (or disposal of building) .....

180,000

c.

Renovation of store (or capital expenditures) ....................

(190,000)

Totals

$150,000

1.000

$148,000

Sale price of machine no. 3 ..........................

$ 45,000

Cost ................................................................

(44,400)

Gain on sale of machine ...............................

$ 600

(5-10 min.) E 7-38B

(a) Major overhaul

(b) Periodic lubrication

(c) Purchase price

(d) Installation

Capital Expenditure

Immediate Expense

Capital Expenditure

Capital Expenditure

(e) Lubrication before machine is placed in

service

(f) Training of personnel

(g) Reinforcement to platform

Capital Expenditure

Capital Expenditure

Capital Expenditure

(h) Ordinary recurring repairs

(i) Transportation and insurance

Immediate Expense

Capital Expenditure

(j) Sales tax

Capital Expenditure

(k) Income tax

Immediate Expense

(15 min.) E 7-39B

Req. 1

Journal

ACCOUNT TITLES

DEBIT

CREDIT

a.

Land ....................................................................

484,000

Cash ..............................................................

484,000

b.

Building

($1,300 + $15,300 + $685,000 + $28,220) ...........

729,820

Note Payable .................................................

685,000

Cash ($1,300 + $15,300 + $28,220) ...............

44,820

c.

Depreciation Expense – Building .....................

5,626

Accumulated Depreciation – Building

($729,820 − $336,000) / 35 × 6/12 .................

5,626

Req. 2

BALANCE SHEET

Plant assets:

Land ..............................................................

$484,000

Building ........................................................

$729,820

Less: Accumulated depreciation ................

(5,626)

Building, net .................................................

724,194

Req. 3

INCOME STATEMENT

Expense:

Depreciation expense – Building ................

$ 5,626

(15-20 min.) E 7-40B

Req. 1

Year

Straight-Line

Units-of-

Production

Double-Declining-

Balance

2016

$ 4,275

$ 6,150

$ 9,300

2017

4,275

4,800

4,650

2018

4,275

4,620

2,325

2019

4,275

1,530

825

$17,100

$17,100

$17,100

_____

Computations:

Straight-line: ($18,600 − $1,500) ÷ 4 = $4,275 per year.

Units-of-production: ($18,600 − $1,500) ÷ 57,000 miles = $.30 per mile:

(continued) E 7-40B

(15 min.) E 7-41B

(10-15 min.) E 7-42B

2. The journal entry on January 1, 2020 to record the sale:

Cash ..........................................................................................

325,000

Accumulated Depreciation – Machine ....................................

506,250

Loss on the Sale of Machine ....................................................

18,750

Machine ...............................................................................

850,000

(15-20 min.) E 7-44B

Journal

DATE

ACCOUNT TITLES

DEBIT

CREDIT

2017

Depreciation for 9 months:

Sept.

30

Depreciation Expense – Fixtures ............

1,440*

Accumulated Depreciation —

Fixtures ............................................

1,440

Sale of fixtures:

30

Cash ..........................................................

2,200

Accumulated Depreciation —

Fixtures ($3,200 + $1,440) .....................

4,640

Loss on Sale of Fixtures .........................

1,160**

Fixtures ...............................................

8,000

_____

*2016 depreciation: $8,000 × 2/5 = $3,200

2017 depreciation: ($8,000 − $3,200) × 2/5 × 9/12 = $1,440

**Loss on sale of fixtures:

Sale price of old fixtures ........................................

$ 2,200

Book value of old fixtures:

Cost .....................................................................

$8,000

Less: Accumulated depreciation ($3,200 +

$1,440) ............................................................

(4,640)

(3,360)

Loss on sale ............................................................

$ (1,160)

(10-15 min.) E 7-45B

Cost of old truck ...........................................................

$390,000

Less: Accumulated depreciation:

($390,000 − $70,000) ×

79+ 159 + 189 + 36

(148,160)*

1,000

_______

Book value of old truck ...............................................

$241,840

_____

*Alternate solution setup for accumulated depreciation:

($390,000 − $70,000)

=

$.32 per mile

1,000,000 miles

79,000 + 159,000 + 189,000 + 36,000 = 463,000 miles driven

Accumulated depreciation

=

463,000 miles × $.32

=

$148,160

Calculation of gain or loss:

Purchase price of Freightliner truck ........... $240,000

Cash paid for Freightliner truck .................. (24,000)

Trade-in value of Mack truck ....................... 216,000

Book value of Mack truck ............................ (241,840)

Net loss on disposal of Mack truck ............. $ (25,840)

Journal

DATE

ACCOUNT TITLES

DEBIT

CREDIT

(10-15 min.) E 7-46B

(10-15 min.) E 7-47B

(5-10 min.) E 7-48B

Less: Bailey Industries’ liabilities ..................................

(24)

Market value of Bailey Industries’ net assets ...............

14

Cost of goodwill ...................................................................

$ 4

Req. 2

Journal

DATE

ACCOUNT TITLES

DEBIT

CREDIT

Current Assets .......................................................

17

Long-Term Assets .................................................

21

Goodwill .................................................................

4

Liabilities .........................................................

24

(5-10 min.) E 7-49B

=

4.80%

=

4.69%

Net sales

$75,000

$73,600

=

1.25

=

1.24

Average total assets

$60,000

$59,300

or

4.80% x 1.25

=

6.00%*

4.69% x 1.24

=

5.82%

The return on assets improved from 2014 to 2015; the increase in the

net profit margin ratio was mostly responsible for this.

_____

*difference due to rounding

(10 min.) E 7-50B

Q7-65

d

$36,000 / $300,000

Problems

(20-30 min.) P 7-66A

Req. 1

ITEM

LAND

LAND

IMPROVEMENTS

SALES

BUILDING

GARAGE

BUILDING

FURNITURE

(a)

$283,500

$ 76,500

(b)

8,800

(c)

$ 31,100

(d)

600

(e)

5,500

(f)

1,000

(g)

$ 300

(h)

45,220

(i)

510,000

(j)

32,980

(k)

9,200

(l)

6,700*

(m)

52,100

(n)

7,300

(o)

4,200

35,280

2,520

(p)

$79,600

(q)

800

Totals

$298,400

$102,400

$600,000

$112,000

$80,400

Computations:

(a) Land: $315,000 / $400,000 × $360,000 = $283,500

Garage building: $ 85,000 / $400,000 × $360,000 = $76,500

(o) Land improvements: $ 42,000 × .10 = $4,200

Sales building: $ 42,000 × .84 = $35,280

Garage building: $ 42,000 × .06 = $2,520

_____

*Some accountants would debit this cost to the Land account.

(continued) P 7-66A

Req. 2

Journal

DATE

ACCOUNT TITLES

DEBIT

CREDIT

Dec.

31

Depreciation Expense — Land

Improvements ($102,400 / 15 × 9/12) ...........

5,120*

Accumulated Depreciation —

Land Improvements ..............................

5,120

31

Depreciation Expense — Sales Building

($600,000 / 30 × 9/12) ....................................

15,000

Accumulated Depreciation —

Sales Building .......................................

15,000

31

Depreciation Expense — Garage

Building ($112,000 / 30 × 9/12) .....................

2,800

Accumulated Depreciation —

Garage Building ....................................

2,800

31

Depreciation Expense — Furniture

($80,400 / 12 × 9/12) ......................................

5,025

Accumulated Depreciation —

Furniture ................................................

5,025

____

*$4,785 ($95,700 / 15 × 9/12) if $6,700 (l in Req. 1) is debited to Land.

(continued) P 7-66A

Req. 3

This problem shows how to determine the cost of a plant asset. It also

demonstrates the computation of depreciation for a variety of plant

assets. Because virtually all businesses use plant assets, a manager

needs to understand how those assets’ costs and depreciation

amounts are determined. Depreciation affects net income. Managers

(15 min.) P 7-67A

(25-35 min.) P 7-68A

(30-40 min.) P 7-69A

12-31-2020

1/5

282,000

56,400

282,000

35,500

Asset cost: $280,000 + $1,900 + $7,000 + $28,600 = $317,500

Depreciation for each year: ($317,500 − $35,500) / 5 years = $56,400

(continued) P 7-69A

12-31-2020

2.82

15,000

42,300

282,000

35,500

Total documents

100,000

Depreciation per document: ($317,500 − $35,500) / 100,000 documents = $2.82

(continued) P 7-69A

12-31-2020

41,148

5,648**

282,000

35,500

*DDB rate = (1/5 years × 2) = 2/5 = .40

**Depreciation for 2020: $41,148 − $35,500 = $5,648

(continued) P 7-69A

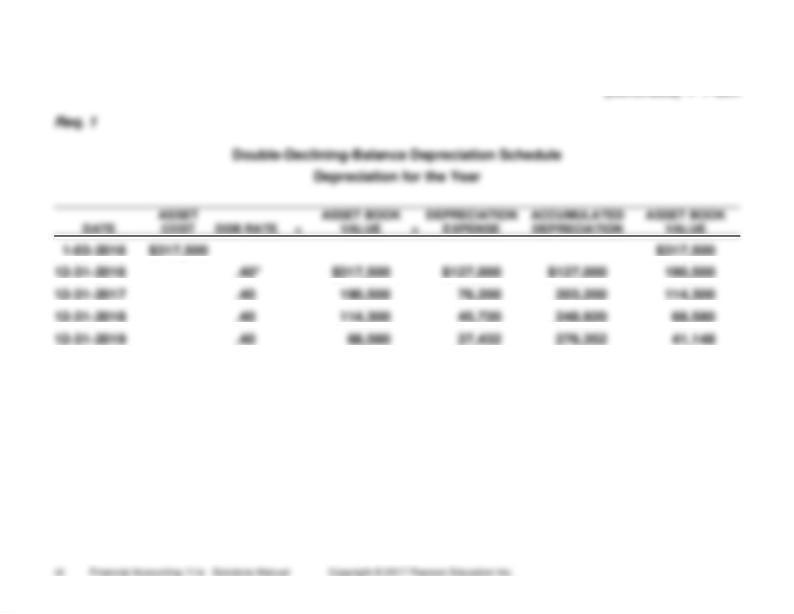

Req. 2

The depreciation method that maximizes reported income in the first

year of the computer’s life is the straight-line method. Straight-line

produces the lowest depreciation for that year ($56,400).

The method that maximizes cash flow by minimizing income tax

payments in the first year is the double-declining-balance method (or

MACRS depreciation when used for tax purposes), which produces the

highest depreciation amount for that year ($127,000).

Req. 3

DEPRECIATION METHOD

THAT IN THE EARLY

YEARS

MAXIMIZES

REPORTED

INCOME

MINIMIZES

INCOME TAX

PAYMENTS

(20-25 min.) P 7-70A

3. Statement of cash flows reports “Additions to property, plant, and

equipment.”

Req. 3

Property, Plant, and Equipment

Accumulated Depreciation

3/31/15 Bal.

4,194

Cost of

Accum. depr.

3/31/15 Bal.

1,726

Purchased

assets sold

of assets sold

Depr. during

during 2016

720

in 2016

78

in 2016

64

2016

459

3/31/16 Bal.

4,836

3/31/16 Bal.

2,121

Goodwill

3/31/15 Bal.

515

Purchased

during 2016

38*

3/31/16 Bal.

553

_____

*Determined by deduction, since there was no loss on goodwill.

(continued) P 7-70A

Req. 4

2016

Cash .......................................................

145

Accumulated Depreciation—Property,

Plant and Equipment ............................

Gain on Sale of Property, Plant and

Equipment .......................................

Property, Plant & Equipment ..........

64

131

78

(20-30 min.) P 7-71A

Req. 1

Journal

DATE

ACCOUNT TITLES

DEBIT

CREDIT

Iron Ore Rights .............................................

2,200,000

Cash .........................................................

2,200,000

Iron Ore Rights .............................................

61,000

Cash .........................................................

61,000

Iron Ore Rights .............................................

71,000

Cash .........................................................

71,000

Iron Ore Rights .............................................

24,000

(continued) P 7-71A

(30-40 min.) P 7-72A

Property, plant, and equipment, net (book value) .....................

$ 1.8

Sales of property, plant, and equipment .....................................

0.3

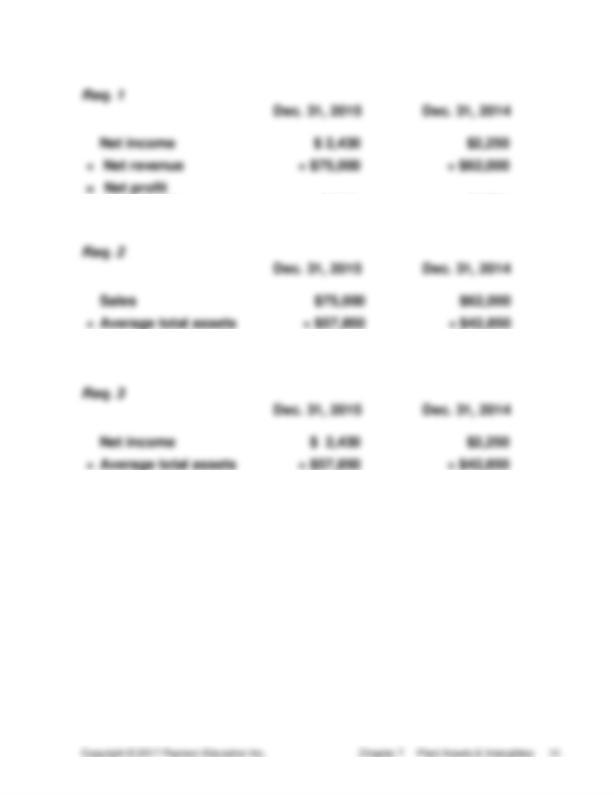

(20-30 min.) P 7-73A

margin ratio

= 3.24%

= 3.63%

= Asset turnover

= 1.30

= 1.45

= Return on assets

= 4.20%

= 5.25%

Req. 4

The following contributed to the decrease in ROA during the most

recent year.

• Cost of goods sold (as a percent of sales) increased, causing

gross profit (as a percent of sales) to decrease. Net profit margin

ratio decreased.

• Cost of goods sold grew faster than sales.

• Total asset turnover decreased.

- Acc. Depr.

-310

= Loss on sale

$(257)

There is a loss because the sales price (proceeds) is less than the book

value.

(continued) P 7-74A

Req. 3

Cash ..........................................................................................

43

Accumulated Depreciation – Prop. & Equipment ...................

310

Loss on the Sale of Prop. & Equipment ..................................

257

Property & Equipment .........................................................

610

Assets decrease, liabilities unaffected, and stockholders’ equity

decreases; revenues unaffected, expenses (losses) increase, and net

income decreases.

The total book value of $300 ($610− $310) is $257 more than the sales

price of $43. This is the same calculation as in Req. 2.

Req. 4

Property & Equipment, net

12/31/15 Bal.

9,010

300

Book value, assets sold

Purchases

2,820

1,145

Depreciation

12/31/16 Bal.

10,385

(20-30 min.) P 7-75B

Req. 1

ITEM

LAND

LAND

IMPROVEMENTS

SALES

BUILDING

GARAGE

FURNITURE

(a)

$283,500

$ 76,500

(b)

8,100

(c)

$ 31,900

(d)

700

(e)

5,100

(f)

1,100

(g)

$ 500

(h)

26,050

(i)

513,000

(j)

31,650

(k)

9,000

(l)

6,600*

(m)

52,300

(n)

7,000

(o)

3,700

31,450

1,850

(p)

$79,800

(q)

2,600

Totals

$297,400

$102,600

$580,000

$110,000

$82,400

Computations:

(a) Land: $315,000 / $400,000 × $360,000 = $283,500

Garage: $85,000 / $400,000 × $360,000 = $76,500

(o) Land improvements: $37,000 × .10 = $3,700

Sales building: $37,000 × .85 = $31,450

Garage: $37,000 × .05 = $1,850

_____

*Some accountants would debit this cost to the Land account.

(continued) P 7-75B

Req. 2

Journal

DATE

ACCOUNT TITLES

DEBIT

CREDIT

Dec.

31

Depreciation Expense — Land

Improvements ($102,600 / 25 × 9/12) ............

3,078*

Accumulated Depreciation —

Land Improvements ..................................

3,078

31

Depreciation Expense —Sales

Building ($580,000 / 50 × 9/12) ......................

8,700

Accumulated Depreciation —

Sales Building ...........................................

8,700

31

Depreciation Expense — Garage

($110,000 / 50 × 9/12) .....................................

1,650

Accumulated Depreciation —

Garage .......................................................

1,650

31

Depreciation Expense — Furniture

($82,400 / 12 × 9/12) .......................................

5,150

Accumulated Depreciation —

Furniture ....................................................

5,150

_____

*$2,880 ($96,000 / 25 × 9/12) if $6,600 (l in Req. 1) is debited to Land.

(15 min.) P7-76B

(25-35 min.) P 7-77B

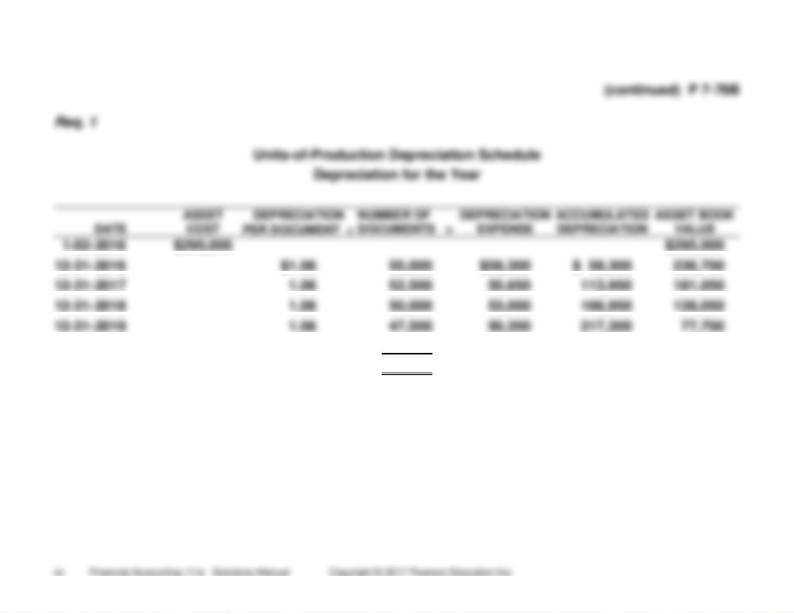

(30-40 min.) P 7-78B

12-31-2020

1/5

265,000

53,000

265,000

30,000

Asset cost: $255,000 + $1,500 + $6,600 + $31,900 = $295,000

Depreciation for each year: ($295,000 − $30,000) / 5 years = $53,000

12-31-2020

1.06

45,000

47,700

265,000

30,000

Total documents

250,000

Depreciation per document: ($295,000 − $30,000) / 250,000 documents = $1.06 per document

(continued) P 7-78B

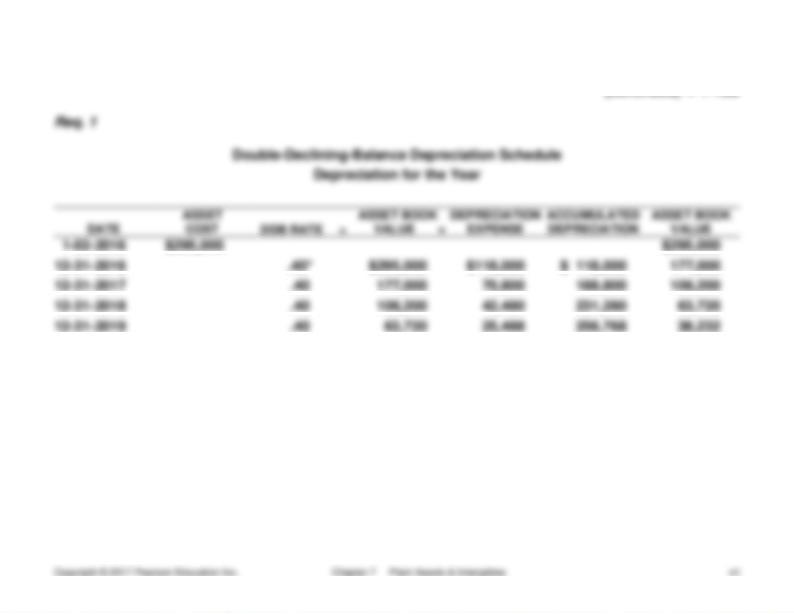

12-31-2020

38,232

8,232**

265,000

30,000

* DDB rate: (1/5 years × 2) = 2/5 = .40

** Depreciation for 2020: $38,232 − $30,000 = $8,232

(continued) P 7-78B

Req. 2

The depreciation method that maximizes reported income in the first

year of the computer’s life is the straight-line method, which produces

the lowest depreciation for that year ($53,000). The method that

maximizes cash flow by minimizing income tax payments in the first

year is the double-declining-balance method (or MACRS depreciation

when used for tax purposes) which produces the highest depreciation

amount for that year ($118,000).

Req. 3

DEPRECIATION METHOD THAT

IN THE EARLY YEARS

MAXIMIZES

REPORTED

INCOME

MINIMIZES

INCOME TAX

PAYMENTS

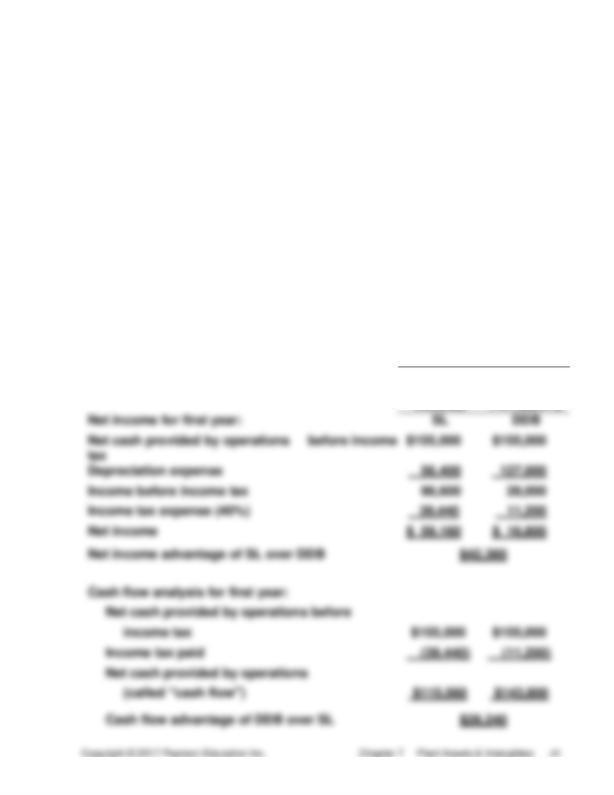

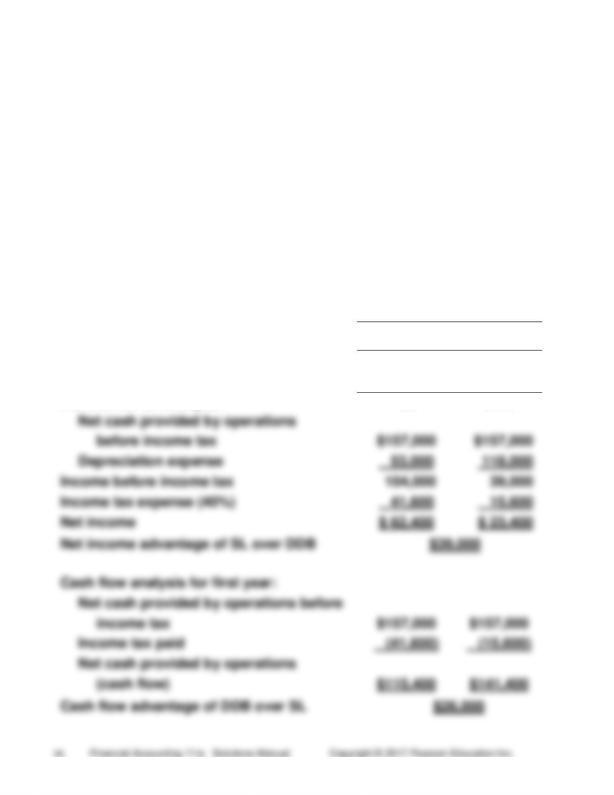

Net income for first year:

SL

DDB

(20-25 min.) P 7-79B

3. Statement of cash flows reports “Additions to property, plant and

equipment.”

Req. 3

Property, Plant, and Equipment

Accumulated Depreciation

4/30/15 Bal.

4,198

Cost of

Accum. depr.

4/30/15 Bal.

1,725

Purchased

assets sold

of assets sold

Depr. during

during 2016

712

in 2016

77

in 2016

66

2016

462

4/30/16 Bal.

4,833

4/30/16 Bal.

2,121

Goodwill

4/30/15 Bal.

510

Purchased

during 2016

49*

4/30/16 Bal.

559

_____

*Determined by deduction, since there was no loss on goodwill.

(continued) P 7-79B

Req. 4

2016

Cash .......................................................

135

Accumulated Depreciation—Property,

Plant & Equipment ................................

Gain on Sale of Property, Plant &

Equipment ......................................

Property, Plant & Equipment ..........

66

124

77

(20-30 min.) P 7-80B

Req. 1

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

Iron Ore Rights .........................................

2,900,000

Cash.....................................................

2,900,000

Iron Ore Rights .........................................

68,000

Cash.....................................................

68,000

Iron Ore Rights .........................................

78,000

Cash.....................................................

78,000

Iron Ore Rights .........................................

38,750

(continued) P 7-80B

(30-40 min.) P 7-81B

Sales of property, plant, and equipment .................................

0.9

(20-30 min.) P 7-82B

margin ratio

= 3.24%

= 3.63%

= Asset turnover

= 1.30

= 1.49

= Return on assets

4.20%

5.41%

Req. 4

All of the following contributed to the decrease in ROA during the most

recent year:

• Net profit margin ratio decreased.

• While net income increased slightly, the gross profit percentage

decreased, thus decreasing the net profit margin ratio.

• Assets increased, decreasing the asset turnover.

- Acc. Depr.

-280

= Book value of assets sold

$360

Sales price

$ 56

Book value

360

= Loss on sale

$304

There is a loss because the sales price (proceeds) is less than the book

value.

(continued) P 7-83B

Req. 3

Cash ..........................................................................................

56

Accumulated Depreciation – Prop. & Equipment ...................

280

Loss on the Sale of Prop. & Equipment ..................................

304

Property & Equipment .........................................................

640

Assets decrease, liabilities unaffected, and stockholders’ equity

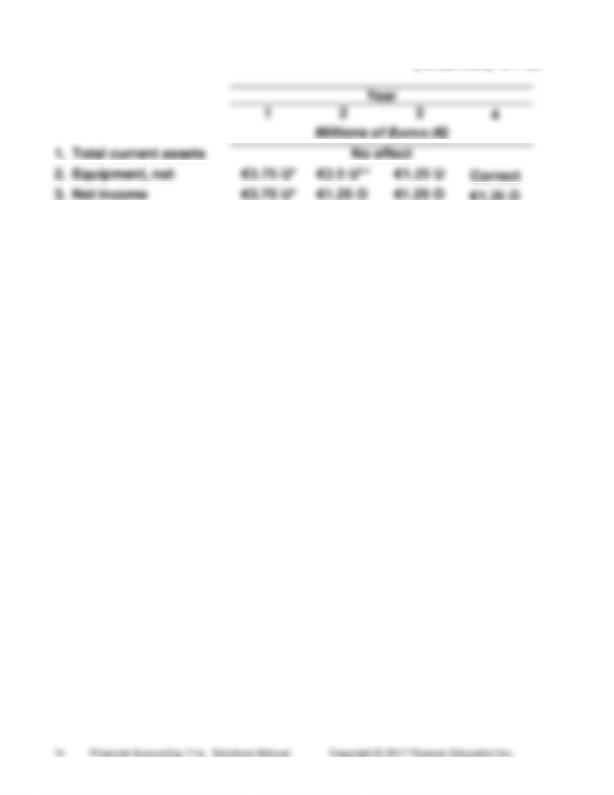

Challenge Exercises and Problem

Decrease in net income ...............................................

(14)

Net income Yentun can expect for 2017

if the company uses DDB depreciation .................

$48

DDB depreciation by year:

Millions

(15-25 min.) E 7-85

€1.25 O

_____

U = Understated

O = Overstated

* Cost (€5.0 million) − Depreciation expense (€1.25 million)

= €3.75 million

** Cost (€5.0 million) − Two years’ depreciation (€2.5 million)

= €2.5 million

(20-30 min.) P 7-86

(All amounts in millions)

Req.1

Property and Equipment

Bal 5/31/2014 (BS) 40,691

Capital expenditures (SCF) 4,347

276 Impairment loss

1,898 Original cost of plant and

equipment sold (plug)

Bal.5/31/2015 (BS) 42,864

Accumulated Depreciation

Acc. Depr. on assets sold 1,752

(plug)

21,141 Bal. 5/31/2014 (BS)

2,600 Depr. exp. (note)

21,989 Bal 5/31/2015 (BS)

Req. 2

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

Property and Equipment .......................

4,347

Cash ...................................................

4,347

Depreciation Expense—Prop. & Equip.

2,600

Accumulated Depreciation—Prop. &

Equip.

2,600

Loss on Impairment of Prop & Equip ...

276

Property and Equipment ..................

276

Cash (SCF) .............................................

24

Accumulated Depreciation—Prop. &

Equip.......................................................

1,752

Loss on Sale of Prop & Equip ...............

122

Property and Equipment ...............

1,898

Decision Cases

(30-45 min.) Decision Case 1

Req. 1

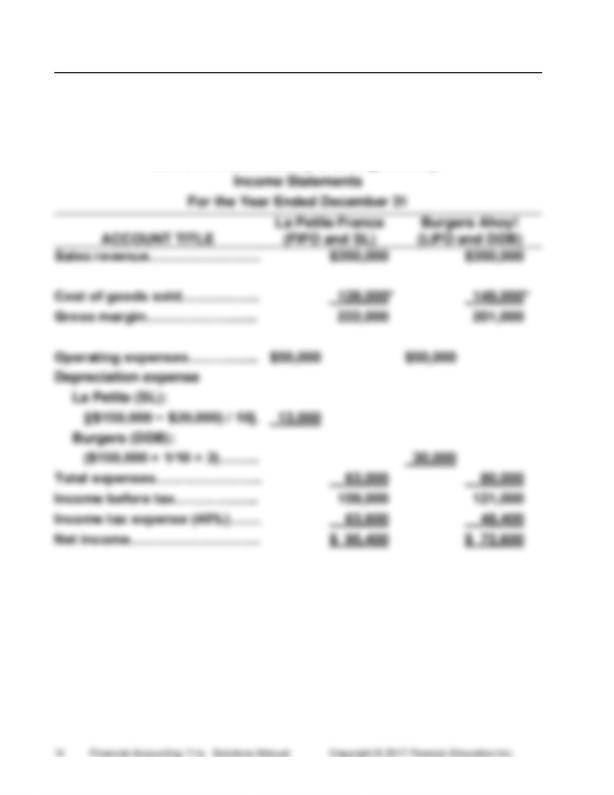

La Petite France Bakery and Burgers Ahoy!

(continued) Decision Case 1

(continued) Decision Case 1

1. La Petite France’s income statement reports a net income of $95,400

compared to $72,600 for Burgers Ahoy!. On the surface La Petite

France appears to be more profitable. This difference is illusory,

2. Burgers Ahoy! reports a lower net income than La Petite France, but

Burgers has more cash to invest in promising projects because

Burgers pays less in income taxes. Burgers uses the LIFO method for

(continued) Decision Case 1

3. Over the long run we favor Burgers Ahoy! because Burgers will have

more cash to invest. That should result in higher real profits even if

(20-30 min.) Decision Case 2

3. We support the recording and reporting of intangible assets at cost,

less accumulated amortization, in accordance with GAAP because the

business paid a price for intangibles like any other asset. The

argument for recording intangibles at $1 or $0 is consistent with the

perspective of a lender, who might reason that, in the liquidation of a

business, most of its intangibles are worthless. However, accounting

serves other users besides lenders. Also, someone who evaluates a

company and believes its intangibles are worthless can simply

subtract the intangibles’ cost from total assets and from total owners’

equity to compute revised totals for analytical purposes. But the

reverse is not true. If intangibles were not reported on the balance

sheet, a user of the statements who believes the intangibles have

value could not add the unknown amount to compute revised total

assets and total owner equity.

Student responses will vary.

Ethical Issue

Req. 1

The ethical issue in this case is “What is the proper amount of the

purchase price to allocate to the land and the proper amount to allocate to

the building?” The taxpayer wants to allocate as much of the purchase

price as possible to the building because tax laws allow a deduction from

taxable income for depreciation expense on plant assets other than land.

The greater the allocation to the building, the greater the depreciation

deduction, and therefore the lower the tax payments because there is no

tax deduction on the land. The cost of the land is not depreciated.

Req. 2 and Req. 3

The stakeholders in this situation include Dellroy National Bank, their

management, their shareholders, the Internal Revenue Service, creditors,

and taxpayers in general. The immediate economic consequences of the

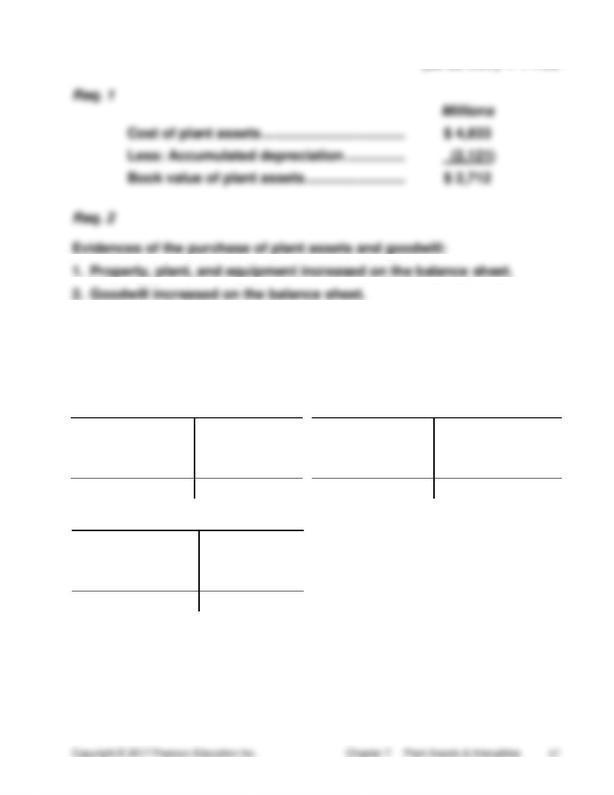

Focus on Financials: Apple Inc.

$6.9 billion includes the straight-line amount of buildings, machinery,

software, and leasehold improvement increases. Accumulated

depreciation and amortization exceeds depreciation and amortization

expense because the expense is for only the current year. Accumulated

depreciation and amortization is the sum of the depreciation and

(continued) Apple Inc.

amortization amounts for all years the company has used its property

and equipment.

Req. 4

Apple Inc. reports goodwill of $4,616 million on its 2014 balance sheet,

and acquired intangible assets on the balance sheet, of $4,142 million.

As explained in Notes 1 and 4 to the Consolidated Financial Statements,

the company does not amortize goodwill and other indefinite-lived

assets. It evaluates the assets that are not being amortized to determine

whether circumstances or events suggest impairment of the assets.

Apple Inc. performs an annual (or sooner if events suggest impairment)

impairment test for goodwill and indefinite-life intangible assets and

writes them down when their value is impaired.

Apple Inc. amortizes the cost of the other definite-life intangibles over

their estimated useful lives, usually three to seven years. The definite-

life intangibles are also reviewed for impairment.

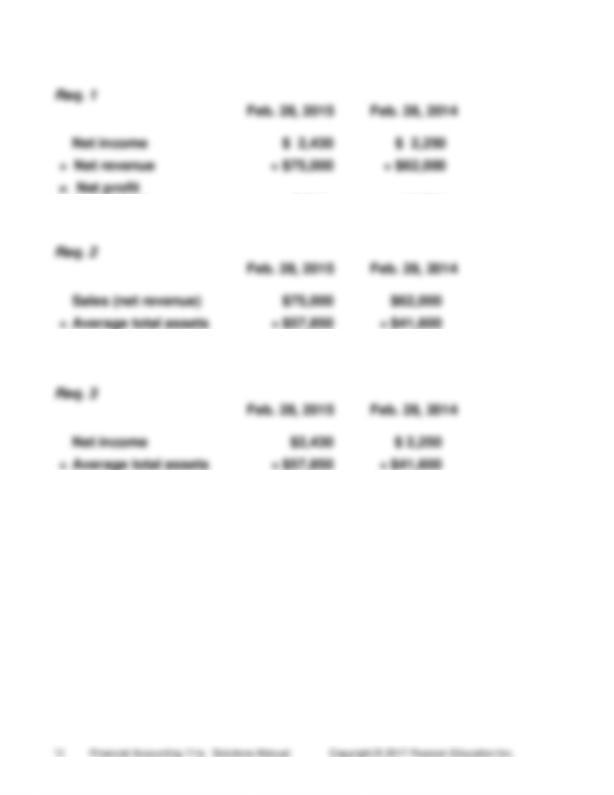

Focus on Analysis: Under Armour, Inc.

(20-30 min.)

(continued) Under Armour, Inc.

=

41.5%

=

= 43.5%

Based on this ratio, the property and equipment is slightly newer in 2014

when compared to 2013. At December 31, 2013, 43.5% of the assets are

used up. At December 31, 2014, 41.5% of the assets are used up.

Req. 4

Under Armour records intangibles when it acquires technology,

customer relationships, or another business. An increase in goodwill in

2014 came from an acquisition in other foreign countries (not North

American) of $1 million. The company lists definite-lived intangible

assets that include technology, trade name, customer relationships,

(continued) Under Armour, Inc.

=

6.74%

=

= 6.95%

Return on assets

=

6.74% x 1.68=11.32%

=

6.95% x 1.71=11.88%

From this analysis, we can see that both the net profit margin ratio and

the asset turnover ratio declined in 2014. So, both ratios are responsible

for the decrease in the return on assets of 0.56%. The company

Group Projects