Chapter 8

Long-Term Investments &

the Time Value of Money

Ethics Check

(5-10 min.) EC 8-1

a. Due care

b. Objectivity and independence

c. Integrity

d. Integrity

Short Exercises

(5-10 min.) S 8-1

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

2016

Jan.

1

Held-to-Maturity Investment in Bonds .........

10,000

Cash ..........................................................

10,000

July

1

Cash ($10,000 × .05 × 6/12) ...........................

250

Interest Revenue ......................................

250

(5-10 min.) S 8-2

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

2016

Jan.

1

Held-to-Maturity Investment in Bonds

($100,000 × .90) .............................................

90,000

Cash ..........................................................

90,000

July

1

Cash ($100,000 × .055 × 6/12) .......................

2,750

Interest Revenue ......................................

2,750

(5-10 min.) S 8-3

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

2016

July

1

Held-to-Maturity Investment in Bonds

($100,000 – $90,000)/10 interest periods)....

1,000

Interest Revenue ......................................

1,000

Total interest revenue = $2,750 + $1,000 = $3,750

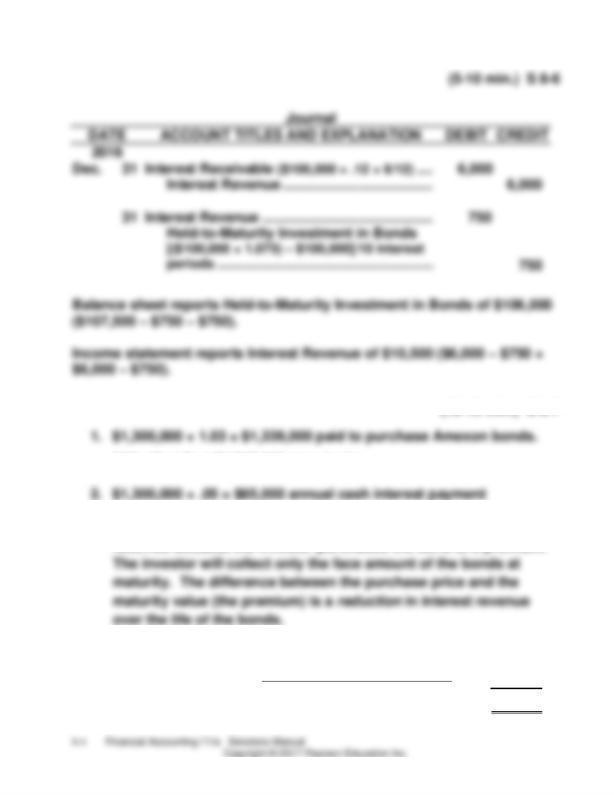

(5-10 min.) S 8-4

(5-10 min.) S 8-6

3. Interest Revenue will be less than the amount of cash interest

received because the investor purchased the bond at a premium.

4.

Cash interest received each year ..............................

$65,000

− Amortization Amortization

$1,339,000 − $1,300,000

=

(7,800)

5 years

= Annual interest revenue ............................................

$57,200

(10-15 min) S 8-8

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

2016

a.

June

30

Held-to-Maturity Investment in Bonds

($1,300,000 × 1.03) ........................................

1,339,000

Cash ..........................................................

1,339,000

b.

Dec.

31

Cash ($1,300,000 × .05 × 6/12) ......................

32,500

Interest Revenue ......................................

32,500

c.

31

Interest Revenue ...........................................

3,900

Held-to-Maturity Investment in Bonds

[($1,339,000 – $1,300,000) / 5 × 6/12] ...........

3,900

2021

d.

June 30

Cash ...............................................................

1,300,000

Held-to-Maturity Investment in Bonds ....

1,300,000

(5-10 min) S 8-9

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

2016

Mar.

23

Investment in AFSS (1,000 × $81.34) ............

81,340

Cash ..........................................................

81,340

June

22

Cash (1,000 × $0.29) .......................................

290

Dividend Revenue ....................................

290

(5-10 min) S 8-10

(15-20 min.) S 8-12

Unrealized (loss) on investment in AFSS……………

(200)

(5-10 min.) S 8-13

Req. 1

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

2017

May

21

Allowance to Adjust Investment in AFSS to

Market ........................................................

Unrealized Loss on Investment in AFSS

200

200

Cash (300 × $30) .......................................

9,000

Investment in AFSS ............................

6,000

Gain on Sale of Investment in AFSS ..

3,000

Req. 2

This gain on sale of investment is a realized gain. The loss recorded at

December 31, 2016, was unrealized because it resulted from a change in

the investment’s market value, not from the sale of the investment.

(10-15 min.) S 8-14

Req. 1

Equity method is appropriate because the investor (Eastern Motors)

(5 min.) S 8-15

2. Consolidated financial statements combine the balance sheets,

3. The parent company’s name appears on the consolidated financial

(10 min.) S 8-17

1. Goodwill is an intangible asset. Goodwill is the excess of the

purchase price to acquire a subsidiary company over the sum of the

2. Noncontrolling interest arises when a parent company owns less than

100% of a subsidiary’s stock. The noncontrolling interest represents

2. Purchase of investment (or acquisition of other companies)

Sale of investment (or sale of other companies)

(10 min.) S 8-19

DATE: Early in 2017

TO: The Ink Spot Company Stockholders

FROM: Chief Executive Officer

RE: Investing Activities During 2016

Ink Spot Company’s investing activities used more cash than the

previous year principally due to the increase in purchases of property,

(5-10 min.) S 8-20

2. $10,871.63 EXCEL formula = PV(1%,60,-150,-7500)

Exercises

(15-20 min.) E8-22A

Req. 1

Rentex, Inc., should use the amortized-cost method to account for the

long-term investment in bonds.

Req. 2

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

2016

Sept.

30

Held-to-Maturity Investment in Bonds

($30,000 × .97) ................................................

29,100

Cash ..........................................................

To purchase bond investment.

29,100

Dec.

31

Interest Receivable ($30,000 × .06 × 3/12) ......

450

Interest Revenue ......................................

To accrue interest revenue.

450

31

Held-to-Maturity Investment in Bonds

[($30,000 – $29,100) / 5 × 3/12) ......................

45

Interest Revenue ......................................

45

To amortize discount on bond investment.

Req. 3

Balance sheet (partial)

ASSETS

Current assets:

Interest receivable ...........................................................

$ 450

Long-term assets:

Held-to-maturity investment in bonds

($29,100 + $45) ................................................................

$29,145

(10-15 min.) E 8-23A

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

a.

Investment in AFSS (400 × $35).......................

14,000

Cash .............................................................

14,000

b.

Cash (400 × $1.60) ............................................

640

Dividend Revenue .......................................

640

c.

Allowance to Adjust Investment in AFSS

to Market [400 × ($42 − $35)] ............................

2,800

Unrealized Gain on Investment in AFSS ....

2,800

d.

Unrealized Gain on Investment in AFSS .........

2,800

Allowance to Adjust Investment in AFSS

to Market ......................................................

2,800

Cash (400 × $25) ...............................................

10,000

Loss on Sale of Investment in AFSS ...............

4,000

Investment in AFSS ....................................

14,000

(15-25 min.) E 8-24A

Req. 1

Stock

Cost

Fair Value

Canada

(3,800 × $38.00)

=

$144,400

(3,800 × $29.125)

=

$110,675

Brazil

(640 × $47.25)

=

30,240

(640 × $49.25)

=

31,520

Russian

(1,500 × $77.00)

=

115,500

(1,500 × $69.50)

=

104,250

Total ............................................

$290,140

...............................

$246,445

Req. 2

Dec. 31

Unrealized Loss on Investments in

AFSS ($290,140 − $246,445)....................

43,695

Allowance to Adjust Investments

in AFSS to Market ...........................

43,695

Req. 3

Statement of Comprehensive Income (partial):

Other comprehensive income:

Unrealized (loss) on investments in AFSS ............

$(43,695)

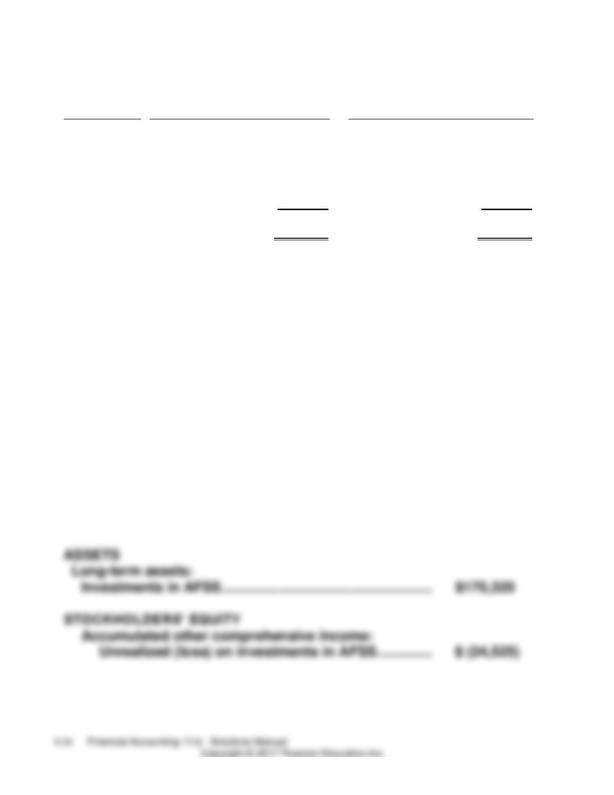

Balance Sheet (partial):

ASSETS

Long-term assets:

Investments in AFFS ....................................................

$246,445

STOCKHOLDERS’ EQUITY

Accumulated other comprehensive income:

Unrealized (loss) on investments in AFSS ............

$(43,695)

(10-15 min.) E 8-25A

(10-15 min.) E 8-26A

(15-20 min.) E 8-27A

(20-25 min.) E 8-28A

8-21

(10-15 min.) E 8-29A

Retained earnings

295,000

1.19

351,050

Accumulated other

comprehensive income:

(15-20 min.) E 8-30A

Net cash (used) in investing activities .......................

$(10.3)

Based on Honey Bakery’s investing activities, it appears that the

company is growing. Acquisitions of long-term assets and

investments are greater than the sales of long-term assets and other

businesses. Capital expenditures of $10.0 million exceed the sale of

PPE of $7.3 million.

8-23

(20-25 min.) E 8-31A

Req. 1

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

(15-20 min.) E 8-33B

Req. 1

Baytex should use the amortized-cost method to account for the long-

term investment in bonds.

Req. 2

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

2016

Sept.

30

Held-to-Maturity Investment in Bonds

($46,000 × .97) ..............................................

44,620

Cash .........................................................

44,620

To purchase bond investment.

Dec.

31

Interest Receivable ($46,000 × .05 × 3/12) ......

575

Interest Revenue .....................................

575

To accrue interest revenue.

31

Held-to-Maturity Investment in Bonds

[($46,000 − $44,620) / 60 mo. × 3 mo.] .........

69

Interest Revenue .....................................

69

To amortize discount on bond investment.

Req. 3

8-25

(10-15 min.) E 8-34B

(15-25 min.) E 8-35B

Req. 1

Stock

Cost

Fair Value

Dublin

(2,800 × $35)

=

$ 98,000

(2,800 × $28.125)

=

$ 78,750

Chile

(590 × $45.50)

=

26,845

(590 × $48.00)

=

28,320

Russian

(1,000 × $70)

=

70,000

(1,000 × $63.25)

=

63,250

Total ............................................

$194,845

..............................

$170,320

Req. 2

Dec. 31

Unrealized Loss on Investments in

AFSS ($194,845 − $170,320) ....................

24,525

Allowance to Adjust Investments in

AFSS to Market ................................

24,525

Req. 3

Statement of Comprehensive Income (partial):

Other comprehensive income:

Unrealized (loss) on investments in AFSS ..............

$ (24,525)

Balance Sheet (partial):

8-27

(10-15 min.) E 8-36B

(10-15 min.) E 8-37B

Equity-Method Investment

a.

Purchase

1,300,000

c.

Dividends

135,000

b.

Net income

204,000

Balance

1,369,000

Proceeds from sale of investment .............

$1,000,000

Carrying amount of investment ..................

(1,369,000)

(Loss) on sale of investment ......................

$ (369,000)

8-29

(15-20 min.) E 8-38B

Req. 1

The equity method is appropriate for a 45% investment in another

(20-25 min.) E 8-39B

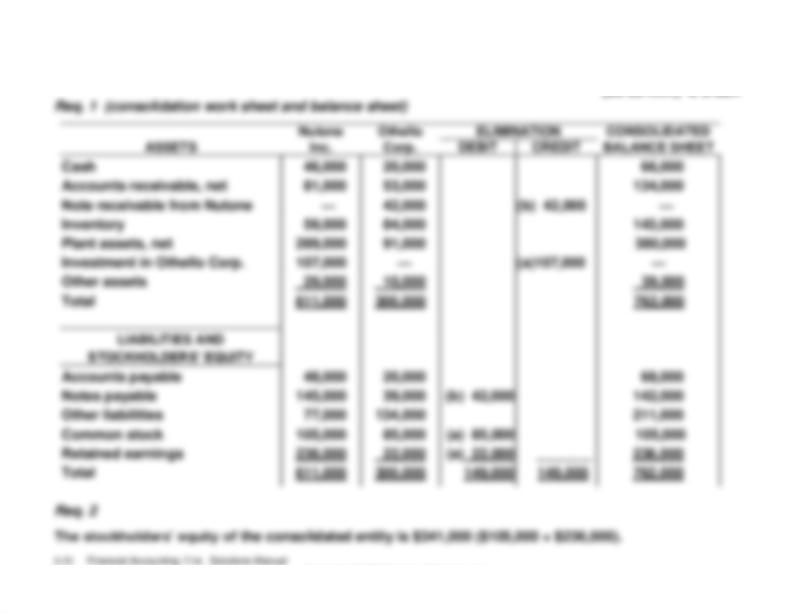

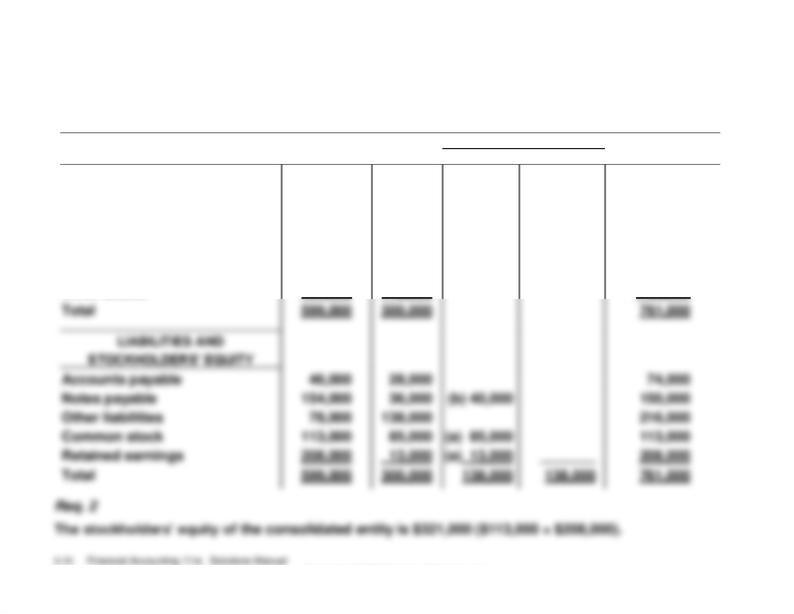

Req. 1 (consolidation work sheet and balance sheet)

Gamma,

Cressida

ELIMINATION

CONSOLIDATED

ASSETS

Inc.

Corp.

DEBIT

CREDIT

BALANCE SHEET

Cash

54,000

14,000

68,000

Accounts receivable, net

80,000

55,000

135,000

Note receivable from Gamma

—

40,000

(b) 40,000

—

Inventory

53,000

84,000

137,000

Plant assets, net

290,000

99,000

389,000

Investment in Cressida Corp.

98,000

—

(a) 98,000

—

Other assets

24,000

8,000

32,000

8-31

(10-15 min.) E 8-40B

Retained earnings

355,000

1.17

415,350

Accumulated other

comprehensive income:

(15-20 min.) E 8-41B

Sale of long-term investments .......................................

3.1

Net cash (used) in investing activities .......................

$ (10.7)

Based on Ellis Bakery’s investing activities, it appears that the

company is growing. Acquisitions of long-term assets and

investments are greater than the sales of long-term assets and other

businesses. Capital expenditures of $10.6 million exceed the sale of

PPE of $7.5 million.

(20-25 min.) E 8-42B

Req. 1

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

Quiz

Q8-55

b

8-35

Problems

(45-60 min.) P 8-56A

Req. 1

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

2016

Jan.

1

Held-to-Maturity Investment in Bonds

($2,800,000 × 1.12) ......................................

3,136,000

Cash .......................................................

3,136,000

To purchase bond investment.

July

1

Cash ($2,800,000 × .09 × 6/12) ...................

126,000

Interest Revenue ...................................

126,000

(continued) P 8-56A

Req. 3

Balance sheet at October 31, 2016:

Current assets:

Interest receivable ....................................................

$ 84,000

Property, plant, and equipment, net ...........................

XXX,XXX

Long-term assets:

Held-to-maturity investment in bonds

8-37

(20-30 min.) P 8-57A

(continued) P 8-57A

Req. 2

Balance sheet:

ASSETS

Total current assets ...........................................................

$ XXX

Property, plant, and equipment, net .................................

XXX

Long-term assets:

Equity-method investment ..............................................

452,614*

Investment in AFSS .........................................................

30,100

STOCKHOLDERS’ EQUITY

Common stock ...................................................................

$ XXX

Retained earnings ..............................................................

XXX

Accumulated other comprehensive income:

Unrealized (loss) on investment in AFSS

[$30,100 − (1,000 × $41.50)] ............................................

(11,400)

Income statement:

Income from operations ....................................................

$ XXX

Other revenue:

Equity-method investment revenue ($540,000 × .25)....

135,000

Dividend revenue (1,000 × $.33) .....................................

330

Net income .........................................................................

XXX

Statement of comprehensive income:

Other comprehensive income:

Unrealized (loss) on investment in AFSS ......................

$ (11,400)

8-39

(45-60 min.) P 8-58A

(continued) P 8-58A

Req. 2

Equity-Method Investment

Jan.

1

Balance

610,000

Aug.

17

Dividends

90,000

Dec.

31

Net income

106,000

Dec.

31

Balance

626,000

8-41

(20-30 min.) P 8-59A

Total assets

$85.1

Req. 2

Total assets

$239.7

Consolidation of the finance subsidiary increased Spindler’s reported

(35-45 min.) P 8-60A

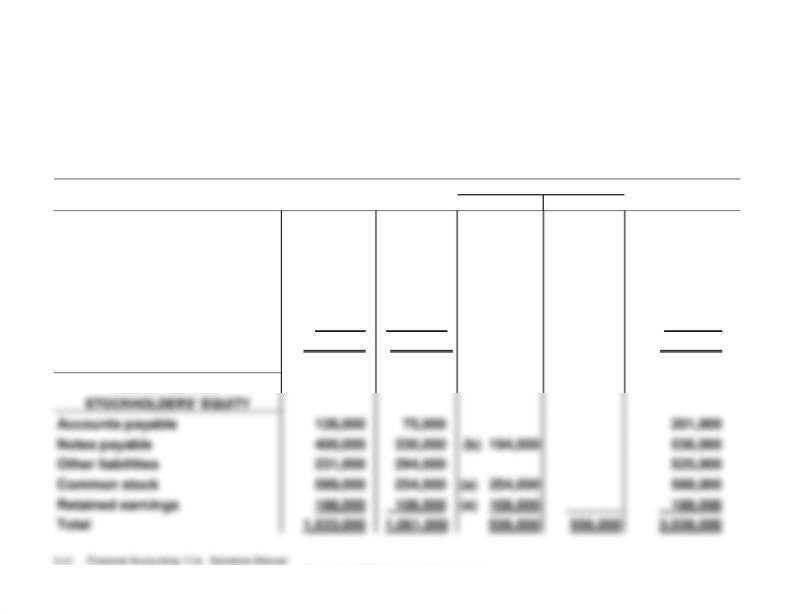

Req. 1

Ronny, Inc.

Consolidation Work Sheet

September 30, 2016

ELIMINATIONS

CONSOLIDATED

ASSETS

RONNY

BIRCHER

DEBIT

CREDIT

AMOUNTS

Cash

54,000

20,000

74,000

Accounts receivable, net

196,000

88,000

284,000

Note receivable from Bircher

194,000

—

(b) 194,000

0

Inventory

346,000

469,000

815,000

Plant assets, net

381,000

484,000

865,000

Investment in Bircher

362,000

—

(a) 362,000

0

Total

1,533,000

1,061,000

2,038,000

LIABILITIES AND

8-43

(20-25 min.) P 8-61A

(20-25 min.) P 8-62A

Req. 1

This situation will generate a positive translation adjustment, which is

like a gain. The gain occurs because the yen’s current exchange rate,

which is used to translate the subsidiary’s net assets, is greater than

the historical exchange rates at which Mason Corp. invested in the

Japanese subsidiary.

YEN

EXCHANGE

RATE

DOLLARS

Assets

410,000,000

$.0090

$3,690,000

Liabilities

145,000,000

.0090

$1,305,000

Stockholders’ equity:

Common stock

25,000,000

.0075

187,500

Retained earnings

240,000,000

.0088

2,112,000

Accumulated other

comprehensive income:

Foreign-currency

translation adjustment

85,500

410,000,000

$3,690,000

The foreign currency translation adjustment is reported in accumulated

other comprehensive income in stockholders’ equity on the balance sheet

and other comprehensive income on the statement of comprehensive

income .

Req. 2

The translation adjustment “belongs” to Mason, the parent company.

Therefore, the translation adjustment will be reported on Mason’s

8-45

(45-60 min.) P 8-63B

(continued) P 8-63B

Req. 3

Balance sheet at October 31, 2016:

Current assets:

Interest receivable ...................................................

$ 52,000

Property, plant, and equipment, net ..........................

XXX,XXX

Long-term assets:

Held-to-maturity investment in bonds

8-47

(20-30 min.) P 8-64B

(continued) P 8-64B

Req. 2

Balance sheet:

ASSETS

Total current assets ............................................................

$ XXX

Property, plant, and equipment, net ..................................

XXX

Long-term assets:

Equity-method investment ...............................................

575,590*

Investment in AFSS ..........................................................

30,900

STOCKHOLDERS’ EQUITY

Common stock ....................................................................

$ XXX

Retained earnings ...............................................................

XXX

Accumulated other comprehensive income:

Unrealized (loss) on investment in AFSS

[(1,100 × $42.25) − $30,900] .............................................

(15,575)

Income statement :

Income from operations .....................................................

$ XXX

Other revenue:

Equity-method investment revenue ($580,000 × .45)….

261,000

Dividend revenue (1,100 × $.34) ......................................

374

Net income ..........................................................................

XXX

Statement of Comprehensive Income:

Other comprehensive income:

8-49

(45-60 min.) P 8-65B

(continued) P 8-65B

Req. 2

Equity-Method Investment

Jan.

1

Balance

614,000

Aug.

17

Dividends

85,000

Dec.

31

Net income

143,000

Dec.

31

Balance

672,000

8-51

(20-30 min.) P 8-66B

Total assets

$80.6

Req. 2

from 0.793 to 0.929. Companies would prefer to report a lower debt

ratio, so they would prefer not to consolidate the financial statements

(35-45 min.) P 8-67B

Req. 1

Robertson, Inc.

Consolidation Work Sheet

September 30, 2016

ELIMINATION

CONSOLIDATED

ASSETS

ROBERTSON

DINETTE

DEBIT

CREDIT

AMOUNTS

Cash

59,000

57,000

116,000

Accounts receivable, net

199,000

87,000

286,000

Note receivable from Dinette

197,000

—

(b) 197,000

0

Inventory

294,000

412,000

706,000

Plant assets, net

388,000

441,000

829,000

Investment in Dinette

289,000

—

(a) 289,000

0

Total

1,426,000

997,000

1,937,000

LIABILITIES AND

STOCKHOLDERS’ EQUITY

Accounts payable

121,000

77,000

198,000

Notes payable

405,000

335,000

(b) 197,000

543,000

Other liabilities

212,000

296,000

508,000

Common stock

550,000

272,000

(a) 272,000

550,000

Retained earnings

138,000

17,000

(a) 17,000

_______

138,000

(15-20 min.) P 8-68B

(20-25 min.) P 8-69B

Retained earnings

260,000,000

0.0100

2,600,000

Accumulated other

comprehensive income:

Foreign-currency

translation adjustment

312,500

Challenge Exercises and Problem

(15-20 min.) E 8-70

Req. 1

a. Consolidation

b. Available-for-sale

c. Equity

Req. 2

PlaySpace’s net income for 2016:

a. Increased by $209,000 (₤110,000 × $1.90).

b. Increased by $18,000.

c. Increased by $450,000 ($1,000,000 × .45).

Req. 3

(20 min.) E 8-71

2. Foreign-currency translation adjustments.

Req. 2

An unrealized gain (loss) on available-for-sale investments produces a

positive (negative) balance.

A foreign-currency translation adjustment is positive when the assets of

(20-25 min.) P 8-72

Req. 1

Amount of

Cash Flow

8% Factor

from Table

Present Value

of Cash Flow

$ 25,000

x

.926

=

$ 23,150

45,000

x

.857

=

38,565

35,000

x

.794

=

27,790

15,000

x

.735

=

11,025

50,000

x

.681

=

34,050

$170,000

$134,580

You should choose the option with the payments over the five years

rather than the one payment of $120,000. The present value of the

payments, $134,580, is higher than the present value of the single

payment, $120,000.

Req. 2

Amount of

Cash Flow

10% Factor

from Table

Present Value

of Cash Flow

$ 25,000

x

.909

=

$ 22,725

45,000

x

.826

=

37,170

35,000

x

.751

=

26,285

15,000

x

.683

=

10,245

50,000

x

.621

=

31,050

$170,000

$127,475

(continued) P 8-72

Decision Cases

4. These items should probably not scare you away from investing in

Infografix stock. After all, the foreign-currency translation adjustment

and the unrealized loss on investments haven’t been realized yet.

(20-30 min.) Decision Case 2

1. The Ohio Office Systems investment cannot be used to generate the

2. The bond investment cannot be used to generate the needed income

because a sale of the bonds would increase net income by only

$6,200, computed as follows:

3. The Microsoft stock can be used to generate the needed income, as

follows:

Sale price of the investment in Microsoft stock

Ethical Issue

Req. 1

The issue: Should Cohen have used his power to influence Web Talk to

pay a large cash dividend when they have to borrow to do so?

(continued) Ethical Issue

Focus on Financials: Apple Inc.

(15-20 min.)

Req. 1

From the caption Cash Equivalents and Marketable Securities in Note

1—Summary of Significant Accounting Policies—Marketable Debt

Investments for which the contractual maturity date is 12 months or less

are classified as short-term. Marketable Debt Investments for which the

contractual maturity is greater than 12 months are classified as long-

term. Marketable equity securities are classified as short-term or long-

term based on the nature of each security and its availability for use in

current operations.

Req. 2

Apple does adjust for periodic changes in fair value of their investments.

According to Cash Equivalents and Marketable Securities in Note 1—

Summary of Significant Accounting Policies—the company’s securities

(continued) Apple Inc.

Focus on Analysis: Under Armour, Inc.

(30 min.)

Req. 1

Under Armour’s three main categories are Apparel, Footwear, and

Accessories. The categories brought in the following revenue listed

from greatest to smallest for 2014.

(In Millions)

Apparel

$2,292

Footwear

$431

Accessories

$275

The apparel category brought in the most revenue in 2014.

Req. 2

Group Project