Chapter 10

Stockholders’ Equity

Ethics Check

(5-10 min.) EC 10-1

a. Integrity

b. Objectivity and independence

c. Due care

d. Objectivity and independence

Short Exercises

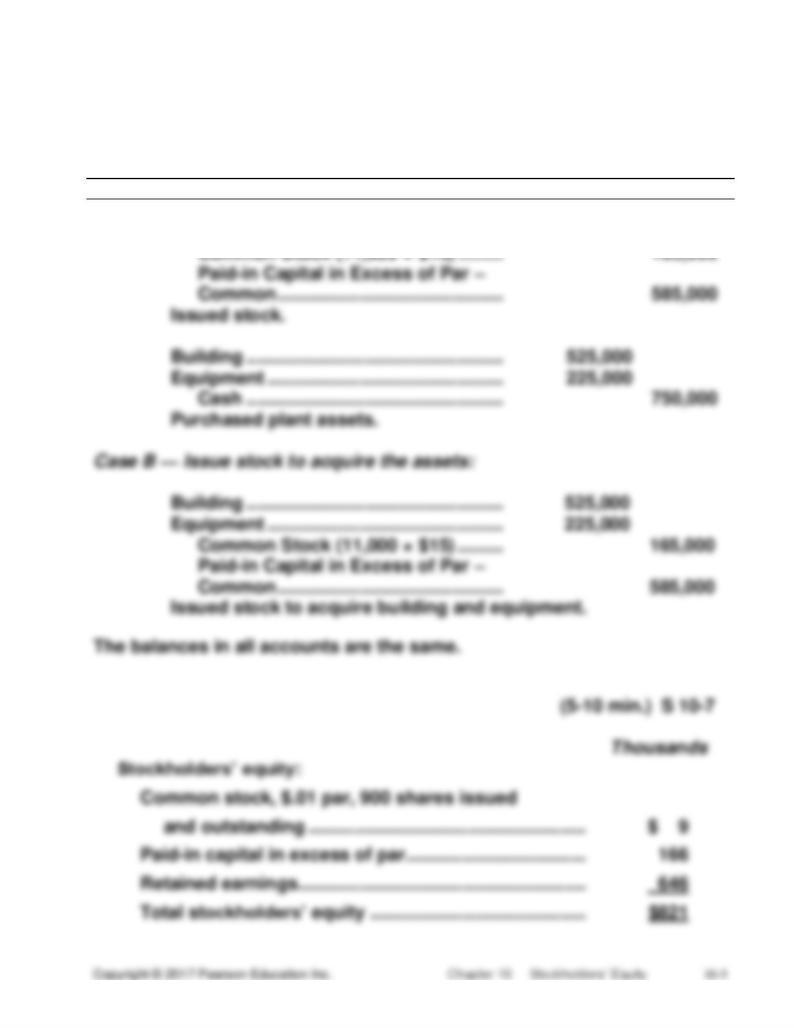

(5-10 min.) S 10-1

Corporation’s advantages:

• Continuous life

(5-10 min.) S 10-2

3. Common stockholders benefit more from a successful corporation

because the preferred stockholders’ dividends are limited to a

specified amount. The common stockholders take more risk so their

potential for gains through higher dividends and an increase in the

value of the company’s stock is unlimited.

(5-10 min.) S 10-3

The $11,488,500 was paid-in capital in excess of par – common. It was

not a profit and therefore had no effect on net income.

The par value per share of stock has no effect on total paid-in capital.

Total paid-in capital is the total amount that stockholders have invested

in (paid into) a corporation, including the par value of stock issued plus

any additional paid-in capital.

(5 min.) S 10-4

Millions

Martin Legal Services:

Cash ....................................................................

17,721

Common Stock ..............................................

21

Additional Paid-in Capital .............................

17,700

Kramer Doughnuts:

Cash ....................................................................

294

Common Stock ..............................................

294

(5-10 min.) S 10-5

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

Jan

14

Cash ........................................................

1,350,000

Common Stock (100,000 × $0.01) .....

1,000

Paid-in Capital in Excess of Par –

Common ............................................

1,349,000

Issued stock.

Jan

29

Legal Expense (2,000 × $13.70) .............

27,400

Common Stock (2,000 × $0.01) .........

20

Paid-in Capital in Excess of Par –

Common ............................................

27,380

Issued stock for services.

(5-10 min.) S 10-6

Case A — Issue stock and buy the assets in separate transactions:

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

Cash ........................................................

750,000

(10-15 min.) S 10-8

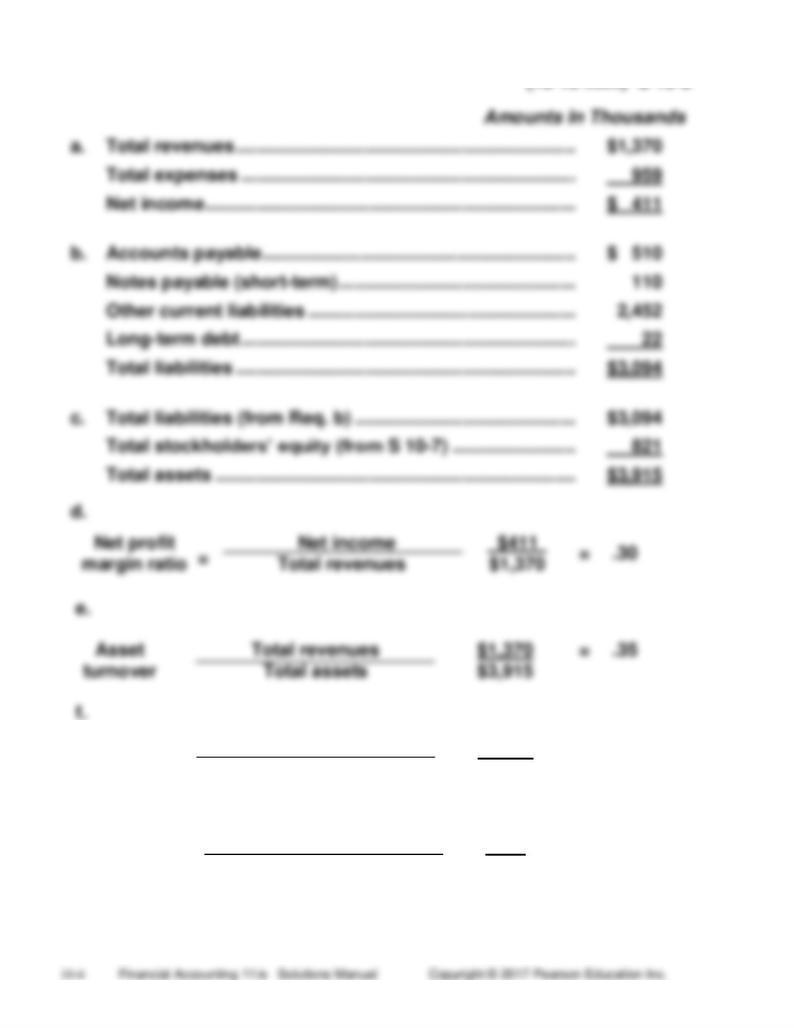

Leverage

ratio

Total assets

Total stockholders’ equity

$3,915

$821

=

4.77

g.

Return on

equity

Net income

Total stockholders’ equity

$411

$821

=

.50

Prior year returns from the company and comparative data for competitors

would also be helpful to make decisions.

(5 min.) S 10-9

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

Millions

Jan.

10

Treasury Stock..........................................

21

Cash .....................................................

21

July

3

Cash .........................................................

12

Treasury Stock ....................................

4

Paid-in Capital from Treasury Stock

Transactions ...................................

8

Overall, stockholders’ equity decreased by $9 million ($21 million paid

out minus $12 million received).

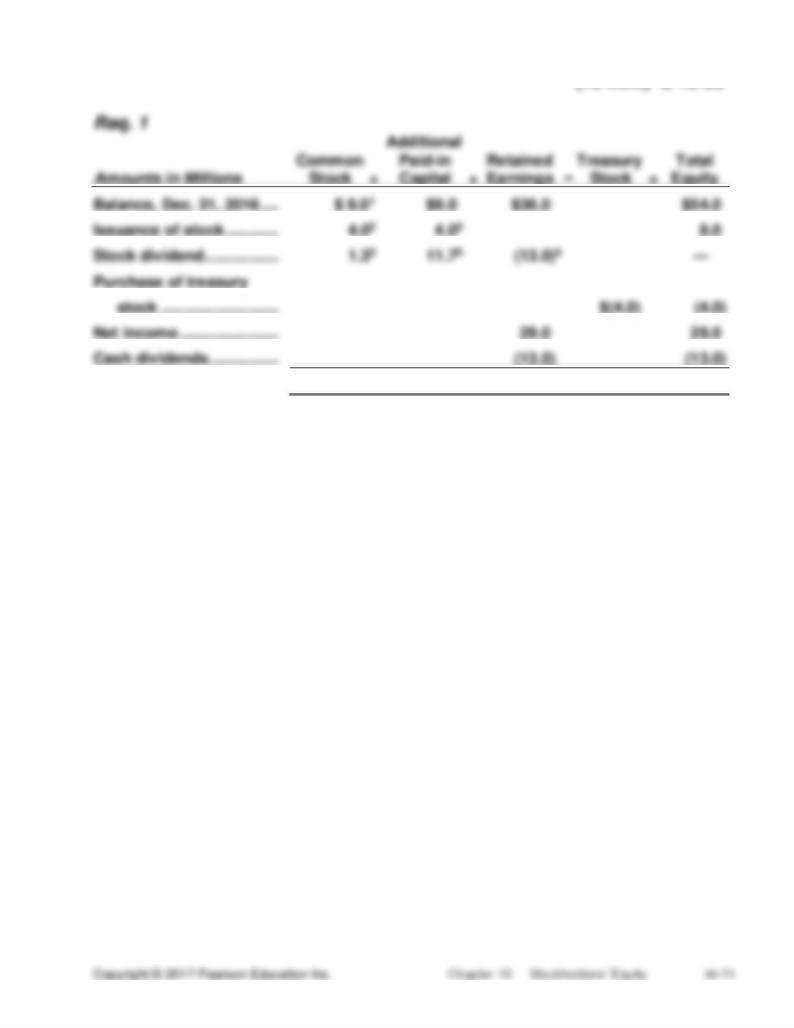

(15-20 min.) S 10-10

Req. 1

MEMORANDUM

TO: Lucinda Lowery Exports, Inc., Board of Directors

FROM: Student Name

RE: How the purchase of treasury stock will make it more difficult

for outsiders to take over the company

Purchasing treasury stock decreases the amount of stock outstanding. If

Lucinda Lowery Exports holds a sufficient quantity of company stock in

the treasury, outsiders, such as the Alberton investor group, may not be

able to acquire a controlling interest (50+ percent) of the outstanding

stock from the remaining stockholders. Because it takes cash to buy

treasury stock, the purchase decreases the size of the corporation.

Reducing the company’s cash position may make the company

sufficiently unattractive to cause the outside investors to abandon their

(10 min.) S 10-11

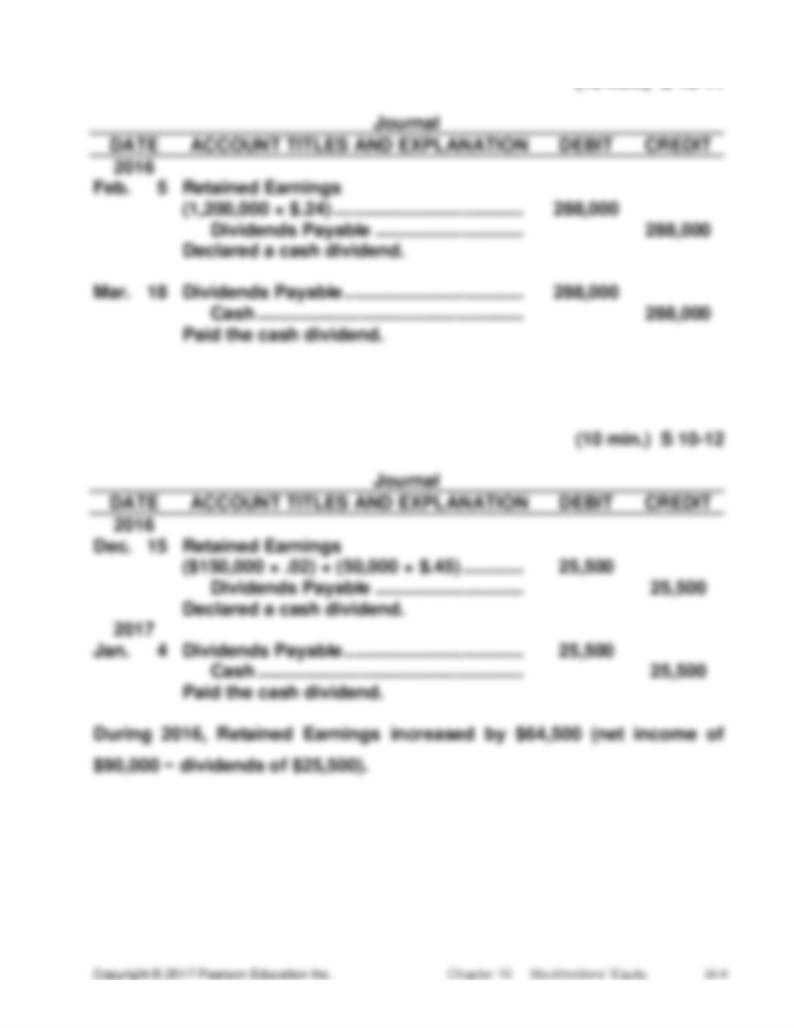

(5-10 min.) S 10-13

4. Preferred: $101,250 ($33,750 × 3)

Common: $1,198,750 ($1,300,000 − $101,250)

(5-10 min.) S 10-14

Req. 1

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

May

11

Retained Earnings (40,000 × .16 × $20) ...........

128,000

Common Stock (40,000 × .16 × $8) ..............

51,200

Paid-in Capital in Excess of Par-Common ...

76,800

Req. 2

(10 min.) S 10-15

Book value per share of common stock ............................

$ 64.26

(5-10 min.) S 10-16

(a)

Rate of return on

total assets (ROA)

=

Net profit margin ratio x Asset turnover

(b)

Rate of return on

common

=

ROA x Leverage ratio

stockholders'

equity (ROE)

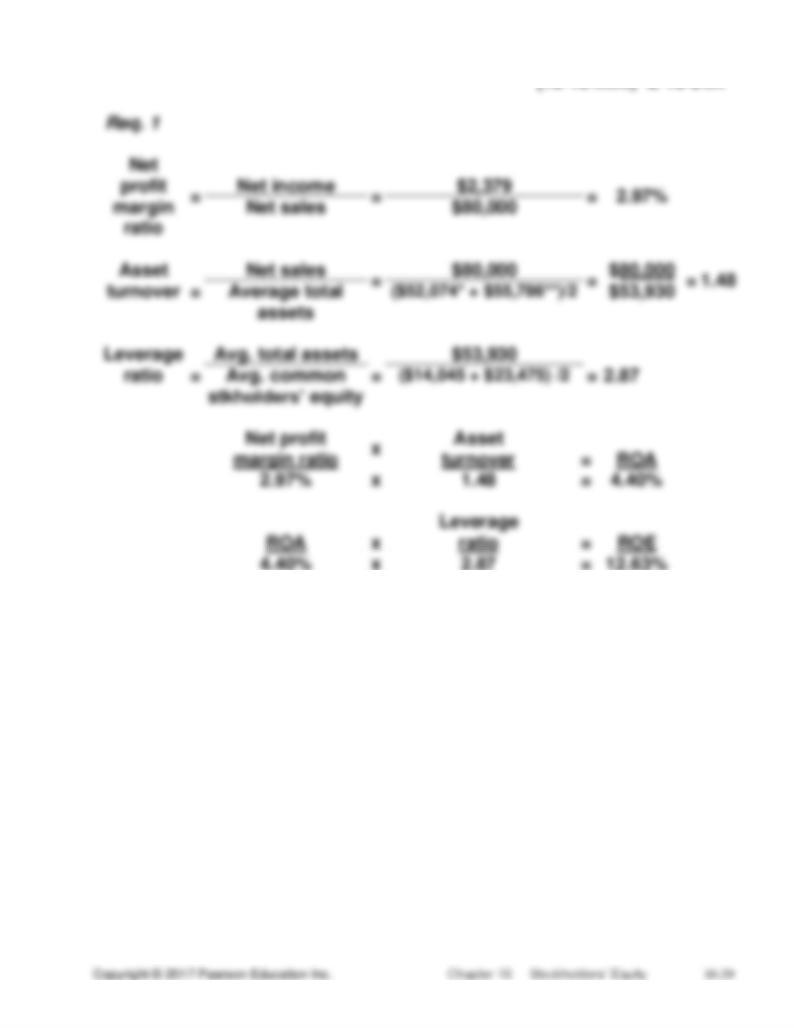

Req. 1

The components of ROA are net profit margin ratio and asset turnover.

Net profit margin ratio [(net income minus preferred dividends)/net sales]

is a measure of operational effectiveness. It measures the percentage net

profit generated for each dollar of sales. Generally, companies that can

differentiate a highly desirable product can sell the product for more,

generating a higher profit. Asset turnover (net sales/average total assets)

is a measure of efficiency in the use of assets. Generally, companies that

can cut costs by reducing the amount invested in fixed assets and

(3.6%)

The company’s rate of return on total assets for 2016 is weak. The

company’s rate of return on common stockholders’ equity for 2016 is

(20-30 min.) S 10-18

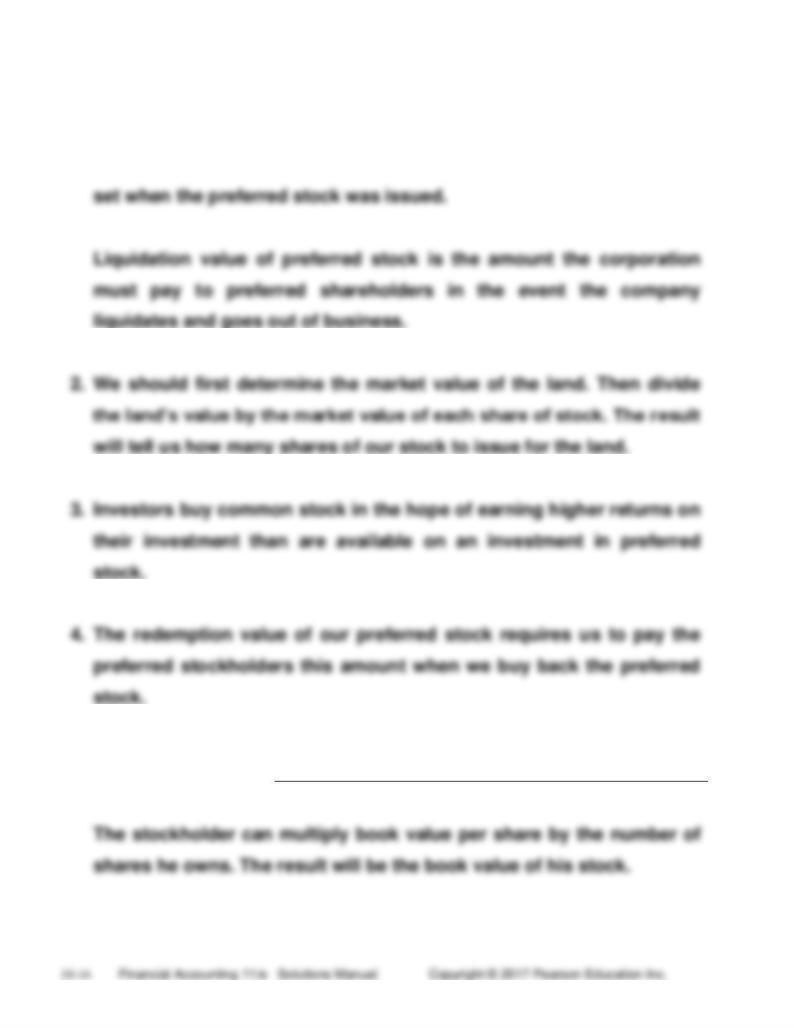

1. Redemption value of preferred stock is the price the corporation

agrees to pay to retire its redeemable preferred stock; that price was

5.

Book value

per share of

=

Total stockholders’ equity − Preferred equity

common stock

Number of shares of common stock outstanding

(5-10 min.) S 10-19

(10 min.) S 10-20

3. The dividend:

(10 min.) S 10-21

2. The stock dividend:

4. Comprehensive income is $96,500 ($84,500 + $9,000 + $3,000).

Addition to Accumulated Other Comprehensive Income is $12,000.

Accumulated Other Comprehensive Income is reported as a part of

Stockholders’ Equity, and is not included in net income.

Exercises

(10-15 min.) E 10-22A

Req. 1

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

Mar.

23

Cash .............................................................

46,500

Common Stock .......................................

18,000

Paid-in Capital in Excess of Par –

Common ...............................................

28,500*

Apr.

12

Inventory ......................................................

20,000

Equipment ...................................................

39,000

Common Stock .......................................

18,600

Paid-in Capital in Excess of Par --

Common ................................................

40,400*

Req. 2

(10 min.) E 10-23A

4.

36,000 (18,000 × $2)

$1,119,000 = Total paid-in capital

Other stockholders’ equity ...................................................

(22)

Total stockholders’ equity ...............................................

$821

(10-15 min.) E 10-25A

Accumulated other comprehensive income (loss) .............

(730)

Total stockholders’ equity ...............................................

$1,127

Req. 2

Alistair Software paid a higher price to acquire treasury stock than the

price Alistair received when it issued its stock. This explains why

Treasury Stock has a greater balance than the sum of Common Stock

plus Paid-in Capital in Excess of Par.

(5-10 min) E 10-26A

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

Millions

Treasury Stock ......................................................

28

Cash ...................................................................

28

Cash .......................................................................

9

Treasury Stock ..................................................

3

Paid-in Capital from Treasury Stock

Transactions ..................................................

6

Overall, stockholders’ equity decreased by $19 million (decrease of

$28 million and increase of $9 million).

(10 min.) E 10-27A

Req. 1

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

Millions

(10 min.) E 10-28A

Treasury stock, at cost ($40 + $121 − $55) ........................

(106)

Total stockholders’ equity .............................................

$ 771

(20-30 min.) E 10-29A

Req. 1

Possible causes for preferred stock decrease:

• Conversion of preferred stock into common stock

Less: Treasury stock, number of shares......................

(38)

Common shares outstanding ........................................

162

Req. 4

Retained Earnings (Millions)

Dec. 31, 2016

Bal.

5,025

treasury stock purchased during 2017 .........

$24.07

(15 min.) E 10-30A

Req. 1

Preferred

Common

Total

2016

Total dividend

$120,000

Preferred dividends in arrears:

2014: 65,000 shares × $4.00 (par)

per share × .07 =

$18,200

2015: 65,000 shares × $4.00 (par)

per share × .07 =

18,200

Preferred dividends, current year :

2016: 65,000 shares × $4.00 (par)

per share × .07 =

18,200

Total to preferred

$54,600

Remainder to common

$65,400

2017

Total dividend

$204,000

Preferred dividends, current year:

2017: 65,000 shares × $4.00 (par)

per share × .07 =

$18,200

Remainder to common

$185,800

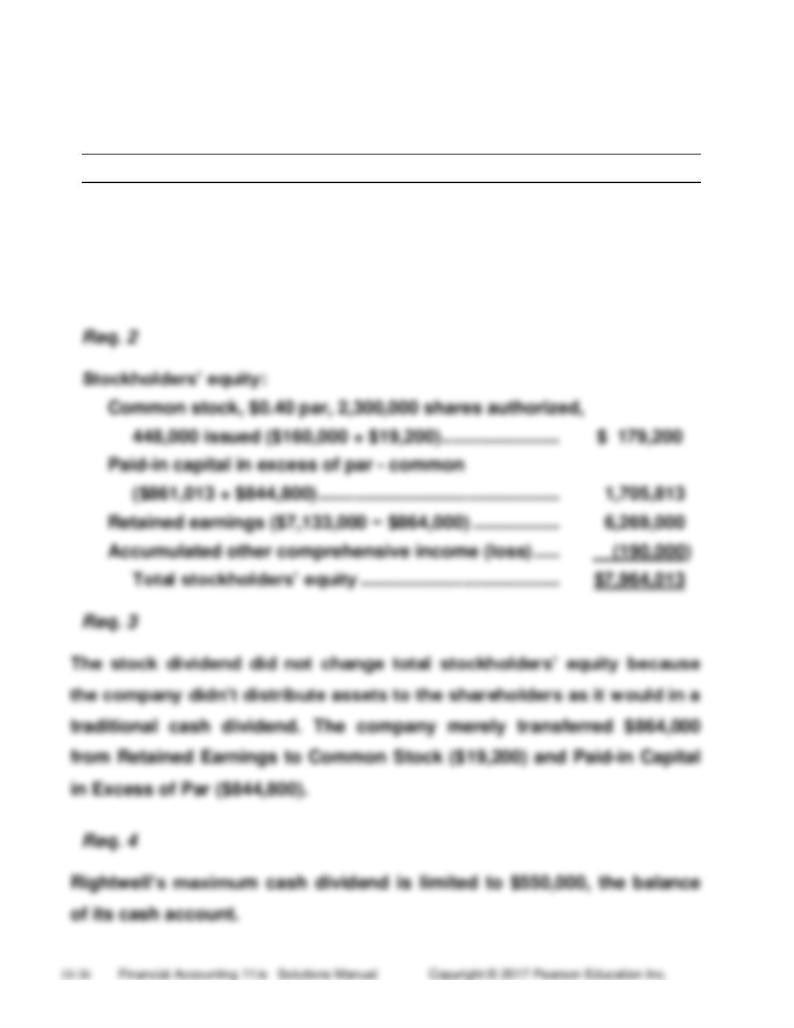

(15-20 min.) E 10-31A

Req. 1

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

June

16

Retained Earnings (400,000 × .12 × $18) .........

864,000

Common Stock (400,000 × .12 × $0.40) ......

19,200

Paid-in Capital in Excess of

Par – Common ..........................................

844,800

To declare and distribute a common stock dividend.

(15-20 min.) E 10-32A

(10-15 min.) E 10-33A

Book value per share ($65,000 / 4,000 shares) ..............

$ 16.25

Req. 2

Book value per share ($60,200 / 4,000 shares) ................

$ 15.05

Req. 3

Eclectic Rug’s stock is not necessarily a good buy. Investment

(10-15 min.) E 10-34A

(12.6%)

_____

Total assets = Total liabilities + Stockholders’ equity

*Beginning of year = $52,074 ($38,029 + $14,045)

**End of year = $55,786 ($32,311 + $23,475)

(continued) E 10-34A

Req. 2

These rates of return suggest relative weakness. The company is

generating a 2.97% net profit margin ratio (moderate effectiveness). The

Dividends paid .................................................................

(205)

Net cash used for financing activities $ (2,275)

(20-25 min.) E 10-36A

$1.00 Par

Common

Stock

Additional

Paid In

Capital

Retained

Earnings

Accum. Other

Comprehensive

Income

Total

Shareholders’

Equity

Balance, Dec. 31, 2015 ..

$395

$1,630

$4,500

$7

$6,532

(75)

(75)

Debt ratio

=

=

=

49.5%

Total assets

$7,800 + $7,958

Issue price

=

=

=

$3.90 per

share

Number of shares issued

100*

*$100/$1.00 par = 100 shares issued

(10-15 min.) E 10-37B

Req. 1

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

Feb.

23

Cash .............................................................

25,500

Common Stock .......................................

3,400

Paid-in Capital in Excess of Par –

Common .................................................

22,100*

Mar.

12

Inventory ......................................................

19,000

Equipment ...................................................

46,000

Common Stock .......................................

6,400

Paid-in Capital in Excess of Par –

Common ..................................................

58,600*

Req. 2

(10 min.) E 10-38B

4.

136,000 (17,000 × $8)

$946,000 = Total paid-in capital

Other stockholders’ equity ...................................................

(27)

Total stockholders’ equity ...............................................

$832

(10-15 min.) E 10-40B

Accumulated other comprehensive income (loss) ............

(730)

Total stockholders’ equity ...............................................

$1,369

Req. 2

Treasury Stock has a larger balance than the sum of Common Stock

and Paid-in Capital in Excess of Par because Patterson Software paid a

higher price to acquire treasury stock than the price Patterson received

when it issued its stock.

(5-10 min.) E 10-41B

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

Millions

Treasury Stock ......................................................

34

Cash ...................................................................

34

Cash .......................................................................

15

Treasury Stock ..................................................

6

Paid-in Capital from Treasury Stock

Transactions ..................................................

9

Overall, stockholders’ equity decreased by $19 million (decrease of

$34 million and increase of $15 million).

(10 min.) E 10-42B

Req. 1

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

Millions

(10 min.) E 10-43B

Treasury stock, at cost ($100 + $65 − $52) ......................

(113)

Total stockholders’ equity ...........................................

$794

(20-30 min.) E 10-44B

Req. 1

Possible causes for preferred stock decrease:

• Conversion of preferred stock into common stock

• Retirement of preferred stock

Req. 2

Less: Treasury stock, number of shares………

(57)

Common shares outstanding……………………....

243

(continued) E 10-44B

Req. 4

Retained Earnings (Millions)

treasury stock purchased during 2017 ..........

$22.80

(15 min.) E 10-45B

Req. 1

Preferred

Common

Total

2016

Total dividend

$90,000

Preferred dividends in arrears:

2014: 55,000 shares × $2.50 (par)

per share × .04 =

$ 5,500

2015: 55,000 shares × $2.50 (par)

per share × .04 =

5,500

Preferred dividends, current year :

2016: 55,000 shares × $2.50 (par)

per share × .04 =

5,500

Total to preferred

$16,500

Remainder to common

$73,500

2017

Total dividend

$225,000

Preferred dividends, current year:

2017: 55,000 shares × $2.50 (par)

per share × .04 =

$ 5,500

Remainder to common

$219,500

(15-20 min.) E 10-46B

Req. 1

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

Aug.

13

Retained Earnings (700,000 × .25 × $20) .....

3,500,000

Common Stock (700,000 × .25 × $0.60) ...

105,000

Paid-in Capital in Excess of Par -

Common ..............................................

3,395,000

To declare and distribute a common stock dividend.

(15-20 min.) E 10-47B

(10-15 min.) E 10-48B

Book value per share ($53,000 / 4,000 shares) .............

$13.25

Req. 2

Book value per share ($49,760 / 4,000 shares) ..............

$12.44

Req. 3

Walton Wallcoverings’ stock is not necessarily a good buy. Investment

(10-15 min.) E 10-49B

11.99%

x

2.87

=

34.41%

_____

Total assets = Total liabilities + Stockholders’ equity

*Beginning of year = $52,064 ($38,025 + $14,039)

**End of year = $55,794 ($32,311 + $23,483)

(continued) E 10-49B

Req. 2

These rates of return suggest relative strength. The company is

generating a 10.8% net profit margin ratio. The company is generating

an asset turnover of 1.11 meaning $1.11 in sales for each dollar of assets

Dividends paid ................................................................

Net cash used for financing activities ................................

(195)

$ (2,325)

(20-25 min.) E 10-51B

$2.00 Par

Common

Stock

Additional

Paid In

Capital

Retained

Earnings

Accum. Other

Comprehensive

Income

Total

Shareholders’

Equity

Balance, Dec. 31, 2015 ..

$370

$1,730

$4,500

$9

$6,609

(85)

(85)

Debt ratio

=

=

=

46.0%

Total assets

$7,000 + $8,225

Quiz

Q10-71

a ($25,000 / $120,000 = 20.8%)

Problems

(30-45 min.) P 10-72A

Req. 1

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

Mar.

6

Organization Expense ...................................

27,000

Common Stock (1,000 × $6) ....................

6,000

Paid-in Capital in Excess of

Par – Common .....................................

21,000

Issued stock to promoter for assisting

with issuance of stock.

9

Cash (30,000 × $10 per share) ......................

300,000

Common Stock (30,000 × $6) ..................

180,000

Paid-in Capital in Excess of

Par – Common .....................................

120,000

Issued common stock for cash.

26

Cash (1,500 × $22) .........................................

33,000

Common Stock (1,500 × $6) ....................

9,000

Paid-in Capital in Excess of

Par – Common .....................................

24,000

Issued common stock for cash.

(continued) P 10-72A

Req. 2

Lane Rafts, Inc.

Balance Sheet (partial)

March 31, 2017

Stockholders’ equity:

Common stock, $6 par, 160,000 shares authorized,

32,500* shares issued and outstanding ....................

$195,000

Paid-in capital in excess of par – common** ...................

165,000

Retained earnings ..............................................................

90,000

Total stockholders’ equity............................................

$450,000

_____

*1,000 + 30,000 + 1,500 = 32,500 shares

**$21,000 + $120,000 + $24,000 = $165,000

(10-15 min.) P 10-73A

Rollo Corp.

Balance Sheet (partial)

December 31, 2016

Stockholders’ equity:

Preferred stock, 7%, $110 par, 5,000 shares authorized,

2,500 shares issued and outstanding ................................

$275,000

Common stock, no-par, 650,000 shares authorized,

65,000 shares issued and outstanding ..............................

511,000

Total paid-in capital ...............................................................

786,000

Retained earnings ....................................................................

96,500

Total stockholders’ equity ..................................................

$882,500

_____

Computations:

Preferred stock: 2,500 × $110 = $275,000

Retained earnings: $79,000 + $95,000 − ($275,000 ×.07 × 2) −

(65,000 × $.60) = $96,500

(25-35 min.) P 10-74A

Req. 1

Yoder Outdoor Furniture Company has Class A cumulative preferred

stock, Class B cumulative preferred stock, and common stock

outstanding.

Req. 2

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

Cash ...................................................

2,520,000

Class A Preferred Stock ................

2,520,000

Cash ...................................................

3,115,000

Class B Preferred Stock ................

3,115,000

Cash ($1,860,000 + $5,570,000) .........

7,430,000

Common Stock ..............................

1,860,000

Additional Paid-in Capital –

(continued) P 10-74A

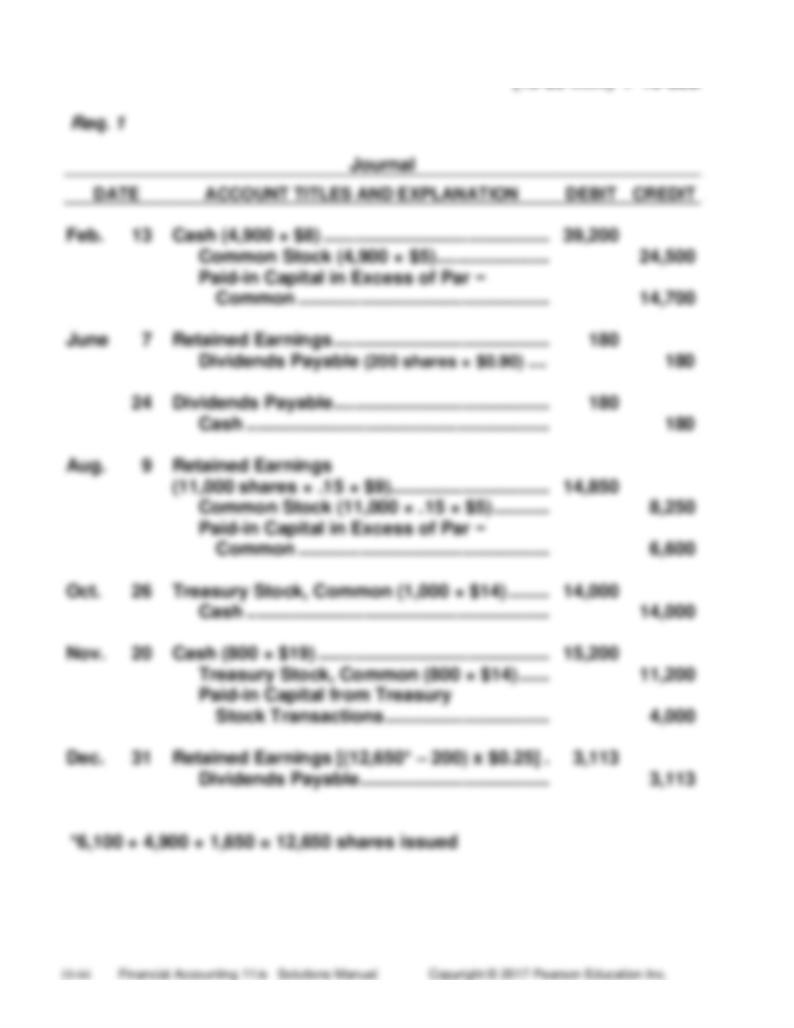

(15-20 min.) P 10-75A

(continued) P 10-75A

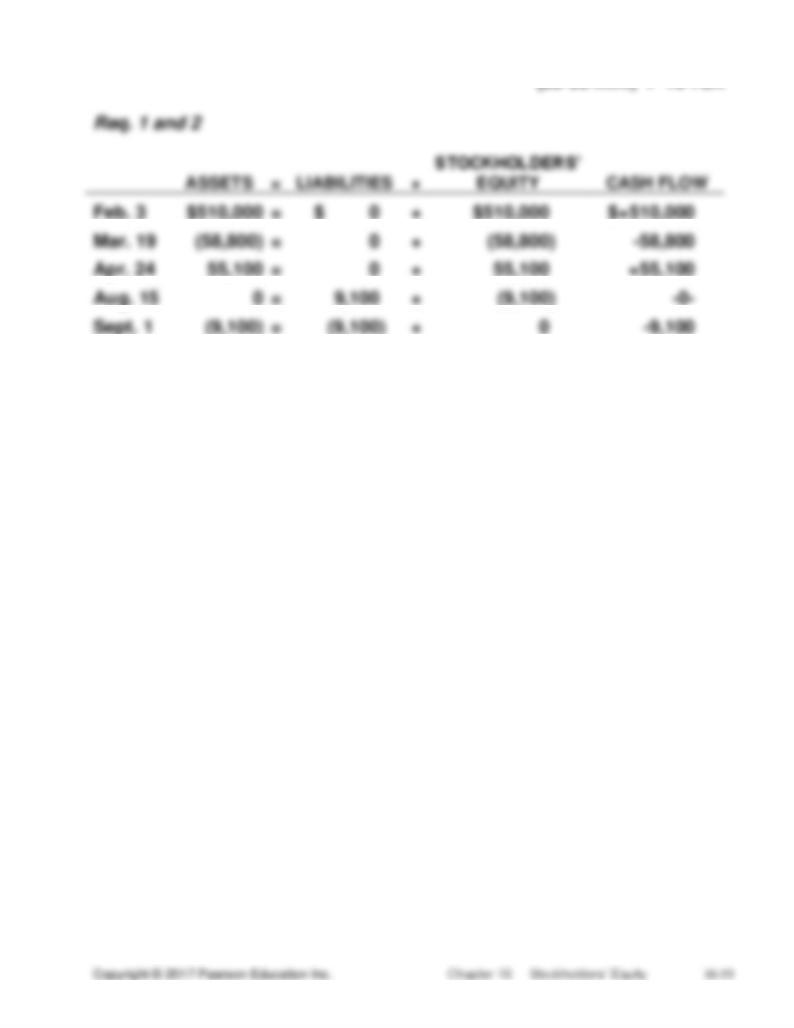

(20-30 min.) P 10-76A

Nov. 22

0

=

0

+

0

-0-

(40-50 min.) P 10-77A

Req. 1

Seagull Designers, Inc.

Balance Sheet

December 31, 2016

ASSETS

LIABILITIES

Current:

Current:

Cash ...........................

$ 42,000

Accounts payable ...............

$145,000

Accounts rec.,

Accrued liabilities ..............

25,000

net ...........................

20,000

Dividends payable ..............

11,000

Inventory ....................

89,000

Total current liabilities ..........

181,000

Prepaid

expenses ................

22,000

Long-term note payable .........

98,000

Total current assets ....

173,000

Total liabilities ........................

279,000

Property, plant,

STOCKHOLDERS’

EQUITY

(continued) P 10-77A

17.2%

x

2.092

=

36.0%

(continued) P 10-77A

9.47% (9.5%) net profit margin ratio indicating great effectiveness in

achieving profit goals and most likely some product differentiation. The

company is generating an asset turnover of 1.813, meaning $1.81 in

sales for each dollar of assets invested, indicating excellent efficiency.

Finally, the company has relatively moderate leverage, meaning they are

utilizing debt effectively. This magnifies ROA to a 36% ROE, which is

(15-20 min.) P 10-78A

Price per share of stock issuance:

=

$4.00 per share

100 million shares

issued

Req. 3

Cost of treasury stock sold: $ 5 million

Selling price of treasury stock sold: $ 22 million

Increase in total stockholders’ equity: $ 22 million

Req. 4

Stock dividend percentage:

$112 million

=

20%

$460 million + $100 million

(30-45 min.) P 10-79B

Req. 1

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

Jan.

6

Organization Expense .....................................

1,800

Common Stock (100 × $15) ........................

1,500

Paid-in Capital in Excess of

Par – Common ........................................

300

Issued stock to promoter for assistance in

Issuing common stock.

9

Cash (26,000 × $22) .........................................

572,000

Common Stock (26,000 × $15) ...................

390,000

Paid-in Capital in Excess of

Par – Common ........................................

182,000

Issued common stock for cash.

26

Cash (1,400 × $22) ...........................................

30,800

Common Stock (1,400 × $15) .....................

21,000

Paid-in Capital in Excess of

Par – Common ........................................

9,800

Issued common stock for cash.

Req. 2

Canal Kayaks, Inc.

Balance Sheet (partial)

January 31, 2017

Stockholders’ equity:

Common stock, $15 par, 125,000 shares

authorized, 27,500* shares issued and outstanding .....

$412,500

Paid-in capital in excess of par – common ........................

192,100**

Retained earnings ................................................................

65,000

Total stockholders’ equity ...............................................

$669,600

_____

*100 + 26,000 + 1,400 = 27,500 shares

**$300 + $182,000 + $9,800 = $192,100

(10-15 min.) P 10-80B

Req. 1

Jackson Corp.

Balance Sheet (partial)

December 31, 2016

Stockholders’ equity:

Preferred stock, 6%, $110 par, 9,000 shares authorized,

2,250 shares issued and outstanding ............................

$247,500

Common stock, no-par, 450,000 shares authorized,

112,500 shares issued and outstanding ........................

515,000

Total paid-in capital .............................................................

762,500

Retained earnings ................................................................

94,300

Total stockholders’ equity ..............................................

$856,800

_____

Computations:

Preferred stock: 2,250 × $110 = $247,500

Retained earnings: $73,000 + $96,000 − ($247,500 × 0.06 x 2) –

(112,500 x $0.40) = $94,300

(25-35 min.) P 10-81B

Req. 1

(continued) P 10-81B

(15-20 min.) P 10-82B

(continued) P 10-82B

$0.90 cumulative preferred stock, $20 par, 200 shares

issued and outstanding ...........................................................

$ 4,000

Common stock, $5 par, 12,650 shares issued ($30,500 +

$24,500 + $8,250) and 12,450 shares outstanding .................

63,250

Paid-in capital in excess of par – common

($17,300 + $14,700 + $6,600) ....................................................

38,600

Paid-in capital from treasury stock transactions .......................

Total paid-in capital ......................................................................

4,000

109,850

(20-30 min.) P 10-83B

Nov.

22

0

=

0

+

0

-0-

(40-50 min.) P 10-84B

Req. 1

Ginger Designers, Inc.

Balance Sheet

December 31, 2016

ASSETS

LIABILITIES

Current:

Current:

Cash .............................

$ 50,000

Accounts payable ....................

$130,000

Accounts receivable,

Accrued liabilities ....................

26,000

net .............................

23,000

Dividends payable ...................

5,000

Inventory .....................

89,000

Total current liabilities ................

161,000

Prepaid

expenses ..................

16,000

Long-term note payable .............

95,000

Total current assets .......

178,000

Total liabilities .............................

256,000

Property, plant,

STOCKHOLDERS’

and equipment,

EQUITY

net ................................

363,000

Common stock,

(continued) P 10-84B

Leverage

assets

=

$527,500

1.904

6.1%

1.904

=

11.6%

(continued) P 10-84B

6.1% net profit margin ratio indicating some effectiveness in achieving

profit goals and perhaps some product differentiation. The company is

generating an asset turnover of 1.23, meaning $1.23 in sales for each

dollar of assets invested, indicating some efficiency. Finally, the

company has relatively moderate leverage, meaning they are utilizing

debt somewhat effectively. This magnifies ROA to only an 11.6% ROE,

(15-20 min.) P 10-85B

Price per share of stock issuance:

=

$1.10 per share

200 million shares

issued

Req. 3

Cost of treasury stock sold: $7 million

Selling price of treasury stock sold: $18 million

Increase in total stockholders’ equity: $18 million

Req. 4

Stock dividend percentage:

$106 million

=

20%

$430 million + $100 million

Challenge Exercises and Problem

(20-25 min.) E 10-86

Req. 1

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

(a)

Cash (52,000* × $6) .......................................

312,000

Common Stock ........................................

52,000

Additional Paid-in Capital .......................

260,000

Issued stock.

(b)

Treasury Stock (1,300 × $11) ......................

14,300

Cash ........................................................

14,300

Purchased treasury stock.

(c)

Cash .............................................................

1,400

Treasury Stock ($14,300 − $13,200) ......

1,100

Additional Paid-in Capital .......................

300

Resold treasury stock.

(d)

Revenues .....................................................

171,000

Expenses ................................................

119,000

Retained Earnings ..................................

52,000

Closed net income to Retained Earnings.

(20-25 min.) E 10-87

(15 min.) E 10-89

Balance, Dec. 31, 2017 ....

$14.3

$24.7

$39.0

$(4.0)

$74.0

Computations:

1$9,000,000 ÷ $1 par = 9,000,000 shares

24,000,000 × $1 par = $4,000,000

4,000,000 × ($2 − $1) = $4,000,000

3(9,000,000 + 4,000,000) × .10 × $1 par = $1,300,000

4(9,000,000 + 4,000,000) × .10 × $10 market value = $13,000,000

5$13,000,000 market value − $1,300,000 par value = $11,700,000

(20-25 min.) P 10-90

Req. 1

$350,000 / 1,000,000 shares = $.35 per share

Req.2

960,000 (1,000,000 shares issued – 40,000 shares in treasury)

Req. 3

Common stock $ 350,000

Paid-in capital in excess of par 34,850,000

$35,200,000

÷ Number of shares ÷ 1,000,000

= Average price $35.20

Req. 4

Journal

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

Cash ................................................................ 4,770,000

Common Stock ($350,000 – $315,000) ... 35,000

Paid-in Capital in Excess of Par

($34,850,000 – $30,115,000) ................ 4,735,000

Req. 5

Proceeds from issuance of stock $4,770,000

÷ Number of shares ÷ 100,000

= Average price $47.70

(continued) P 10-90

Req. 6

Cost of treasury stock $1,528,000

÷ Number of shares ÷ 40,000

= Average price $38.20

Req. 7

Journal

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

Cash ($191,000 + $3,000)……………………….. 194,000

Treasury Stock ($1,719,000 – $1,528,000)…… 191,000

Paid-in Capital from Treasury Stock

Transactions ($53,000 – $50,000)………… 3,000

Req. 8

Journal

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

Retained Earnings………………………….. 1,500,000

Dividends Payable ................................ 1,500,000

($55,000,000 + $11,000,000 – X = $64,500,000)

X = $1,500,000

Decision Cases

(30-45 min.) Decision Case 1

Req. 1

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

Smith, Capital ...................................................

25,000

Jones, Capital ..................................................

25,000

Common Stock ............................................

50,000

To incorporate the business, close the capital

accounts of Smith and Jones, and issue

common stock to them.

Req. 2

Journal

DATE

ACCOUNT TITLES AND EXPLANATION

DEBIT

CREDIT

Plan 1:

Cash..................................................................

80,000

Preferred Stock (800 × $100).......................

80,000

To issue preferred stock to outside investors.

Plan 2:

Cash..................................................................

55,000

Preferred Stock ............................................

55,000

To issue preferred stock to outside investors.

Cash..................................................................

35,000

Common Stock ............................................

35,000

To issue common stock to outside investors.

(continued) Decision Case 1

Req. 3

Plan 1:

Stockholders’ Equity

Preferred stock, 6%, $100 par, nonvoting,

10,000 shares authorized, 800 shares issued and

outstanding ....................................................................

$ 80,000

Common stock, $1 par, 500,000 shares authorized,

50,000 shares issued and outstanding .........................

50,000

Retained earnings ($120,000 − $30,000) ............................

90,000

Total stockholders’ equity .............................................

$220,000

Plan 2:

Stockholders’ Equity

Preferred stock, $5, no-par, 10,000 shares authorized,

500 shares issued and outstanding ..............................

$ 55,000

Common stock, $1 par, 500,000 shares authorized,

85,000 shares issued and outstanding .........................

85,000

Retained earnings ($120,000 − $30,000) ............................

90,000

Total stockholders’ equity .............................................

$230,000

(continued) Decision Case 1

Req. 4

Plan 1 appears to fit the plans of Smith and Jones better than Plan 2

because:

• Their primary goal is to raise as much capital as possible without

giving up control of the business. Under Plan 2, the outside

stockholders would have 60,000 votes [35,000 common votes +

25,000 preferred votes (500 shares × 50 votes per share)]. Smith

and Jones would lose control of the business because they would

have only 50,000 votes.

• Under Plan 1 preferred stockholders have no votes. Smith and

Jones would have complete control since they would hold all the

voting shares.

• Plan 2 would raise only $10,000 more than Plan 1.

(15-20 min.) Decision Case 2

Req. 1

The stock dividend does not affect your proportionate ownership in the

company because all the stockholders receive 10% new shares. All

stockholders are in the same relative position after the dividends as they

were before.

Req. 2

Cash dividends received last year were $7,150 (10,000 shares × $0.715

per share). Cash dividends after the dividend will be $7,150 (11,000

shares × $0.65 per share). Thus, there is no change in cash dividends.

Req. 3

You incur no loss in value because the market value of your investment

Ethical Issue 1

(continued) Ethical Issue 1

Ethical Issue 2

(continued) Ethical Issue 2

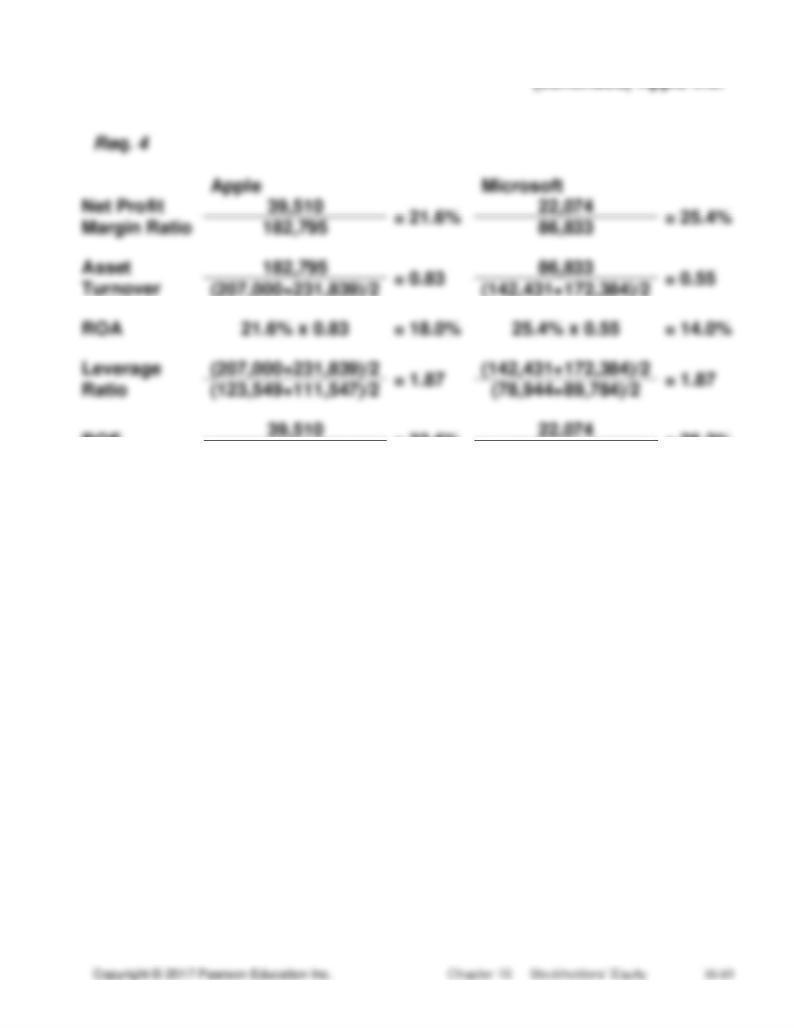

Focus on Financials: Apple Inc.

(continued) Apple Inc.

ROE

= 33.6%

= 26.2%

(123,549+111,547)/2

(78,944+89,784)/2

Apple has positive ROA and ROE ratios in 2014. While both companies

have a similar leverage ratio, Microsoft has a higher net profit margin

ratio. Apple has a higher asset turnover than Microsoft. Apple is

obviously more profitable based on ROA and ROE than Microsoft, but

Microsoft does a better job at managing its costs relative to its revenues

(higher net profit margin ratio).

Student answers may vary if another company is chosen for

comparison.

Focus on Analysis: Under Armour, Inc.

(20-30 min.)

Req. 1

2014. If you multiply 5,667,280 by the par value of $0.00033, this equals

$1,870.20, which approximates $2,000 (increase in Common Stock

account in balance sheet).

(continued) Under Armour, Inc.

Req. 4

Retained Earnings

653,842 Beg. Balance

208,042 Net Income

Shares withheld 5,197

856,687 End. Balance

Group Project in Ethics

(1-3 hours, including discussion)

Req. 1

Stakeholders in a corporation vary widely with the nature of the

corporation. In the case of the corporations included in this case (GM,

Chrysler, AIG, Citibank, Bank of America) because of their size and the

scope of their operations, stakeholders include the shareholders,

bondholders, other creditors, employees, suppliers, customers, local,

regional, national and international economies, federal, state and local

governments—just about everyone in the broadest sense of the term.

(continued) Group Project in Ethics