4.

Times

a.

Receivable Turnover

$720,000

d

Average Accounts Receivable

9.0

CASH AND RECEIVABLES

CHAPTER 7—Solutions

=

Chapter 7, SE 2.

Net Sales

Chapter 7, SE 1.

353

Times

$ 250

4,543.33

12.96

Add interest income

Less outstanding checks

9.2

9.2

Chapter 7, SE 3.

=

Chapter 7, SE 4.

Currency and coins on hand

$117,500

a.

b.

=

3,028.89

8.64

$2,488.12

31 7,500 7,500

$750,000 × 0.01 = $7,500

30 102,000 102,000

$129,000 – $27,000 = $102,000

30 150,000 150,000

$129,000 + $21,000 = $150,000

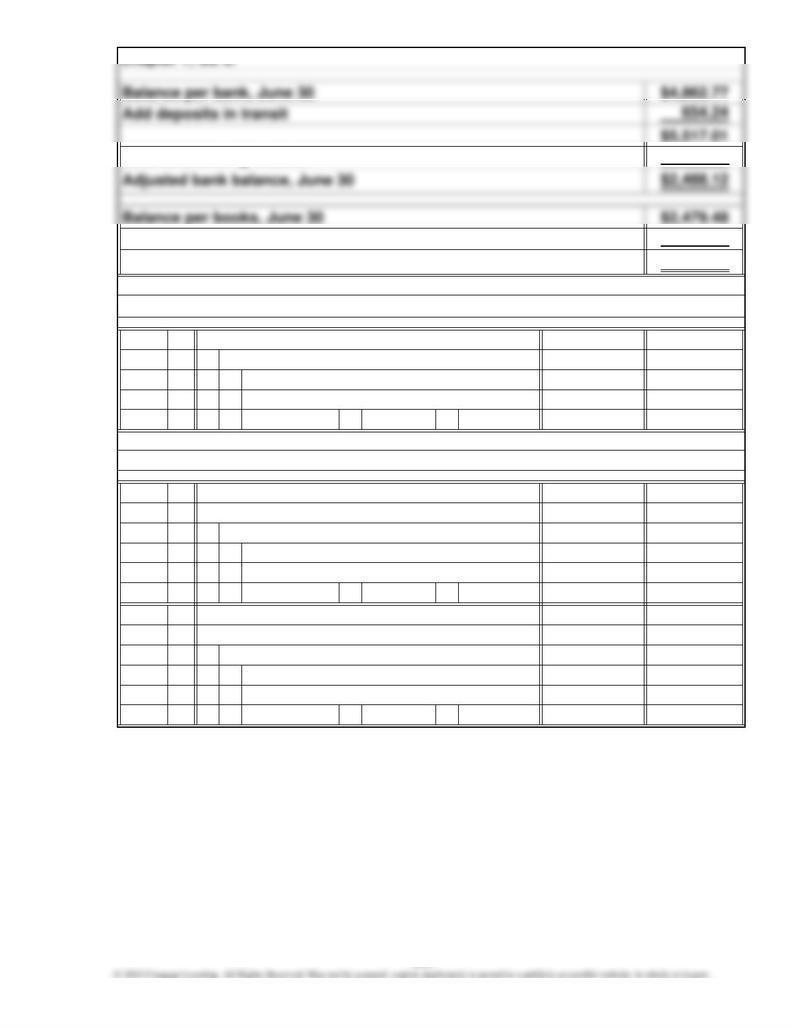

Chapter 7, SE 6.

Less outstanding checks

Add interest income

Adjusted book balance, June 30

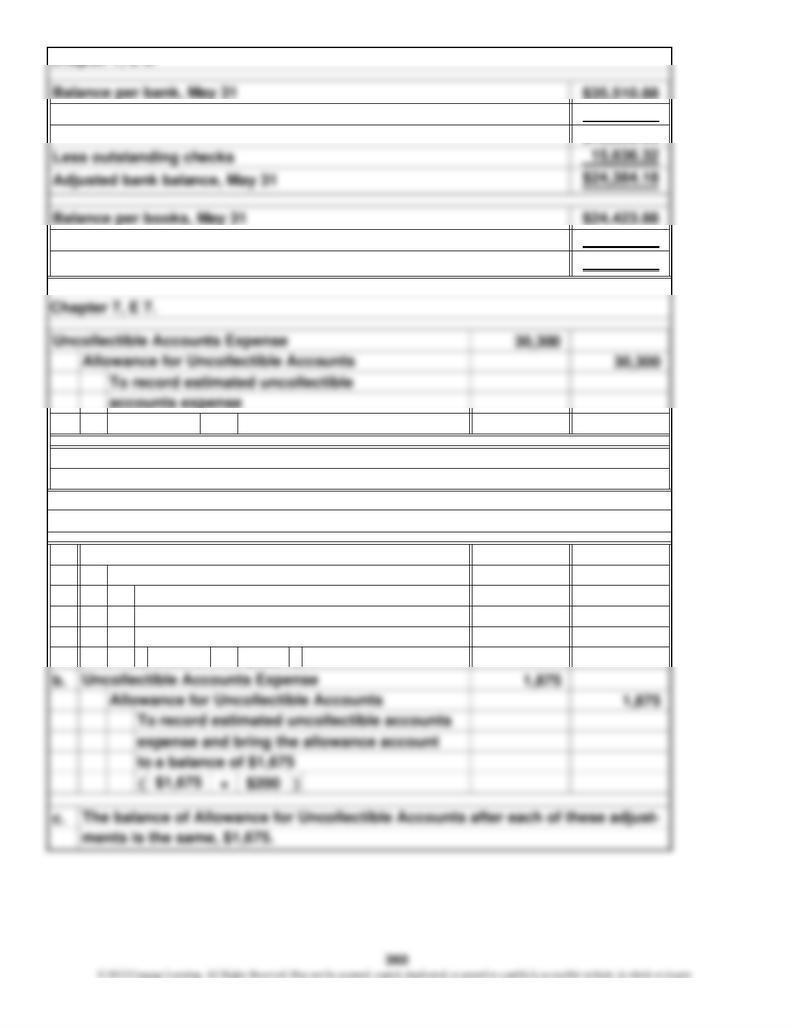

Chapter 7, SE 7.

Allowance for Uncollectible Accounts

To record estimated uncollectible

accounts expense

Oct. Uncollectible Accounts Expense

Chapter 7, SE 8.

b.

a.

Sept. Uncollectible Accounts Expense

Allowance for Uncollectible Accounts

To record estimated uncollectible

To record estimated uncollectible

accounts expense

accounts expense

Sept. Uncollectible Accounts Expense

Allowance for Uncollectible Accounts

355

30 68,000 68,000

$86,000 – $18,000 = $68,000

b.

Chapter 7, SE 9.

Uncollectible Accounts Expense

accounts expense

To record estimated uncollectible

a.

Allowance for Uncollectible Accounts

June

+=

$20,000.00

$20,443.84

$443.84

+

Chapter 7, SE 11.

Chapter 7, SE 12.

$517.81

a. Maturity date:

June 19

Rate of

=

1.

3.

4.

1.

2.

3.

Chapter 7, E 1.

contra-asset accounts, but their purposes are different. Allowance for Uncol-

from period to period, especially in the absence of changes in credit policies

able turnover and more average days to collect. These changes occur because

or economic conditions, might mean that management is underestimating the

include toy companies, college textbook publishers, amusement parks, con-

9.

Times

$ 5,600

10,000

Chapter 7, E 4.

8.4

Currency and coins on hand

Money orders from customers

Chapter 7, E 3.

b

$380,000

Key Ratios:

Chapter 7, E 5.

8.4

4,509.62

$40,020.50

39.70

$24,384.18

a. 1,475 1,475

( – $200 )

Chapter 7, E 6.

Adjusted book balance, May 31

0.008

$3,787,500 ×

to a balance of $1,675

$36,750 ($30,300 + $6,450).

Chapter 7, E 8.

To record estimated uncollectible accounts

The balance of Allowance for Uncollectible Accounts after this adjustment is

expense and bring the allowance account

$1,675

Uncollectible Accounts Expense

Allowance for Uncollectible Accounts

Add deposits in transit

Less bank service charge

× 0.014 =

Adjusting entry:

1. T accounts prepared to determine ending balances:

Collections 1,475,000

Accounts Receivable

Chapter 7, E 9.

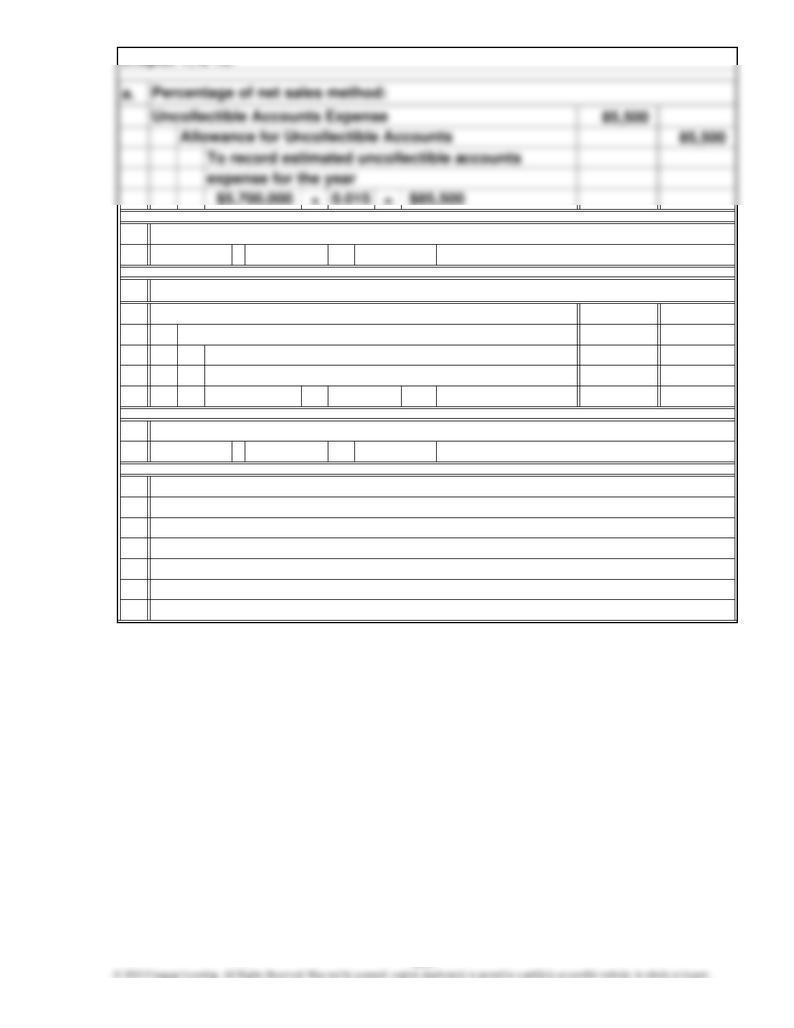

2. a. Percentage of net sales method applied

215,000

Bal.

361

$322,500

21,150 21,150

$19,350

1,800

$21,150

$322,500

Uncollectible Accounts

Estimated uncollectible accounts

Balance sheet presentation:

Accounts receivable

Chapter 7, E 9. (Continued)

Balance sheet presentation:

Accounts receivable

2. b. Aging of accounts receivable method applied

Debit balance in Allowance for

Adjusting entry:

Uncollectible Accounts Expense

Allowance for Uncollectible Accounts

To record estimated uncollectible

accounts expense

Uncollectible accounts expense

×=

The balance of Allowance for Uncollectible Accounts after this adjustment is

(–

b. 94,000 94,000

+=

The balance of Allowance for Uncollectible Accounts after this adjustment is

(–

c.

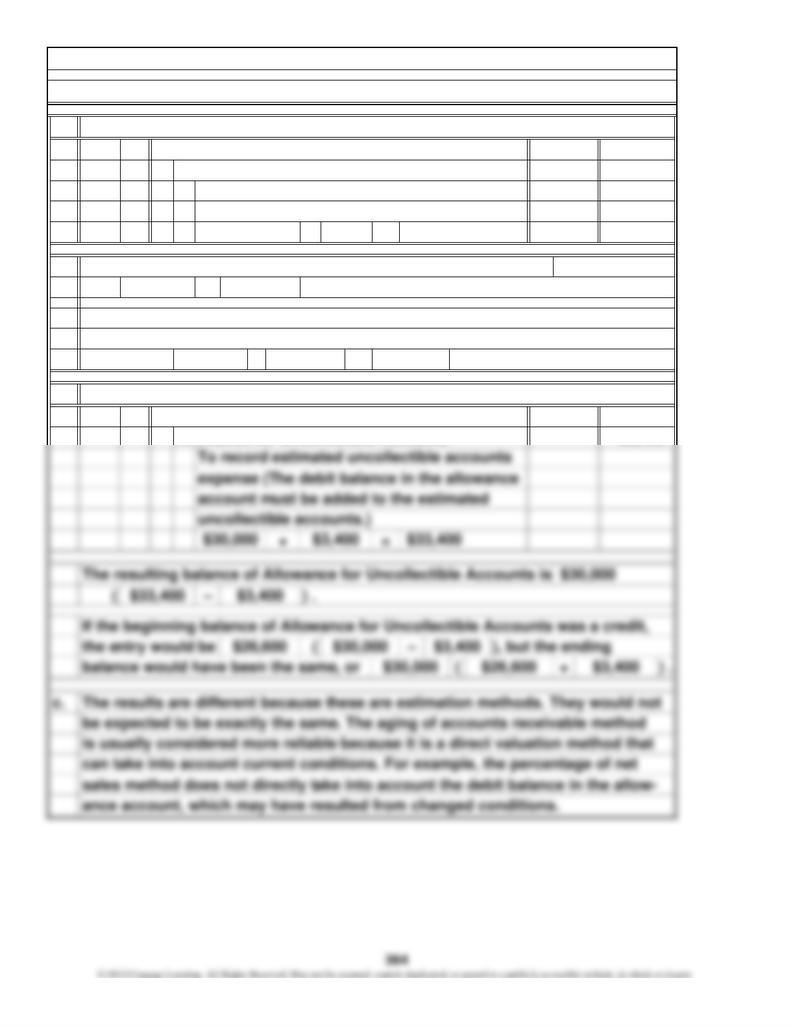

Chapter 7, E 10.

$94,000

0.015 $85,500

$85,500 $24,000 ) .

tions or the quality of the accounts receivable.

ance in the allowance account, which may have resulted from changed condi-

not be expected to be exactly the same. The aging of accounts receivable

$24,000 ) .

method that can take into account current conditions. For example, the per-

centage of net sales method does not directly take into account the debit bal-

Accounts receivable aging method:

Uncollectible Accounts Expense

Allowance for Uncollectible Accounts

$70,000

$70,000

method is usually considered more reliable because it is a direct valuation

The results are different because these are estimation methods. They would

$24,000 $94,000

To record estimated uncollectible accounts

expense for the year

$61,500

363

a. July 31

×=

(–

(+

b. July 31

accounts expense0.014

have been $35,600 $32,200 $3,400

$3,400

Uncollectible Accounts Expense 33,400Allowance for Uncollectible Accounts 33,400

$32,200 ) .

To record estimated uncollectible

$28,800

$32,200

32,200 32,200

$2,300,000

Uncollectible Accounts Expense

Allowance for Uncollectible Accounts

Chapter 7, E 11.

Journal entries for uncollectible accounts prepared

Percentage of net sales method:

If the beginning balance of Allowance for Uncollectible Accounts had been a

credit, the entry would have been the same, but the resulting balance would

The resulting balance of Allowance for Uncollectible Accounts is

) .

Accounts receivable aging method:

e. × 6 / 100 × 60 / =

365

$18,360

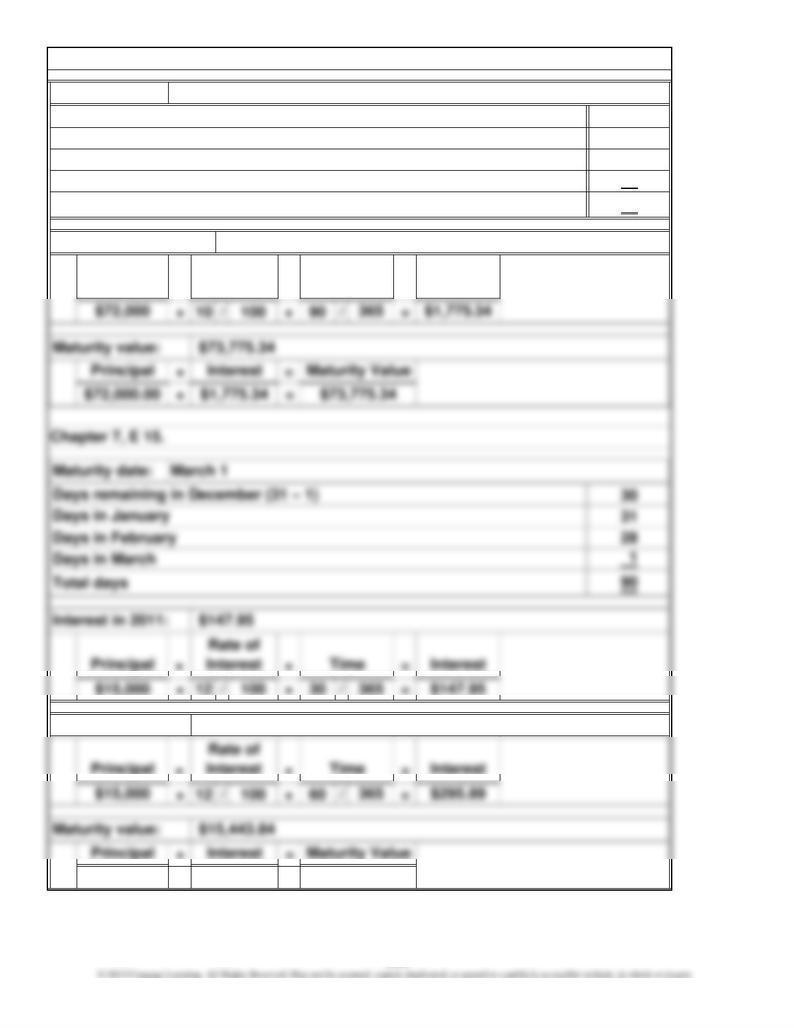

Chapter 7, E 12.

$181.08

365

13

31

30

16

90

+=

Interest in 2012:

$295.89

×× Time

Rate of

InterestPrincipal

= Interest

Interest at maturity: $1,775.34

Total days

Chapter 7, E 14.

Days in April

Days in May

Maturity date: May 16

Days remaining in February (28 – 15)

Days in March

$443.84 $15,443.84$15,000.00

+

=

=

366

a.

× 10 / 100 × 60 / =

$39.45

×

Time

=

Principal

×

$2,400 $39.45365

Chapter 7, E 16.

January 5, accepted a 60-day, 10% note for $2,400

Rate of

Interest

Maturity value:

×

Interest at maturity:

Interest

$29.59

×Rate of

Interest

$2,439.45

Principal Time

= Interest

1,400.00 30,099.68

$311,533.84

14,605.28

2,280.00 3,142.00

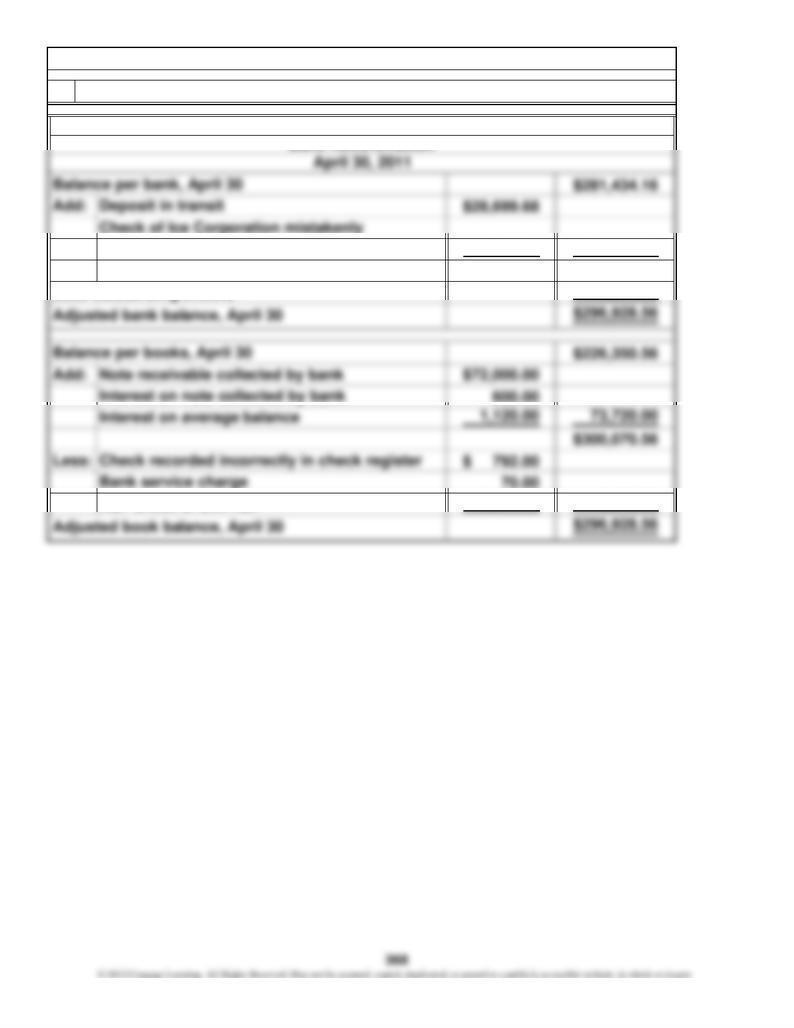

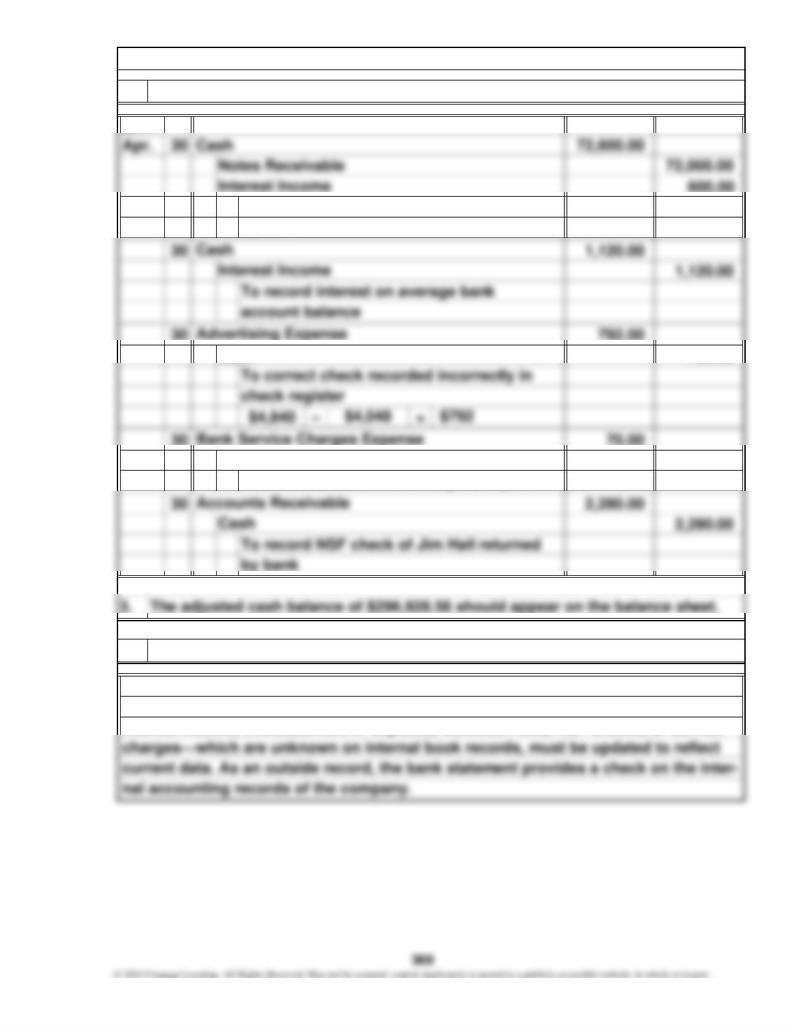

1. Bank reconciliation prepared

Merry Corporation

Chapter 7, P 1.

Bank Reconciliation

Less outstanding checks

deducted by bank

NSF check of Jim Hall

600.00

30 792.00 792.00

30 70.00 70.00

To record bank service charge for April

Cash

A bank reconciliation is a necessary internal control because certain events and

items—for example, a note receivable collected by a bank, interest income on a note,

interest income, overstatement of deposits, collection fees, NSF checks, or service

Journal entries prepared

by bank

To record note and interest collected

4. User Insight: Importance of bank reconciliation discussed

Chapter 7, P 1. (Continued)

Cash

2011

2.

74,500

= ( – ) × 0.016

=

=+

=

=–

Bal.

1.

Sales returns and allowances

Chapter 7, P 2.

T accounts prepared and data entered

2. Uncollectible accounts expense and ending balance of Allowance for

Accounts Receivable 18,250

$18,250

Allowance for Uncollectible Accounts $4,488

$5,563

$298,750

Accounts Receivable, net

1.6 percent

$63,500

$1,075

$5,563

$4,488

4.

Because the percentage of net sales method and the accounts receivable aging

method are both estimates and are based on different assumptions, it is expected

that they would differ in their effects. Also, the amount of uncollectible accounts

expense under the accounts receivable aging method depends partially on how

Chapter 7, P 2. (Continued)

$18,250

3. Receivable turnover and days' sales uncollected calculated

–

$298,750

good the estimates of losses were in the prior year because the amount of expense

is affected by the current balance of Allowance for Uncollectible Accounts, which

User Insight: Difference in methods and rationales discussed

4.4

Times Days

1–30 31–60 61–90 Over

Not Yet Days Days Days 90 Days

Total Due Past Due Past Due Past Due Past Due

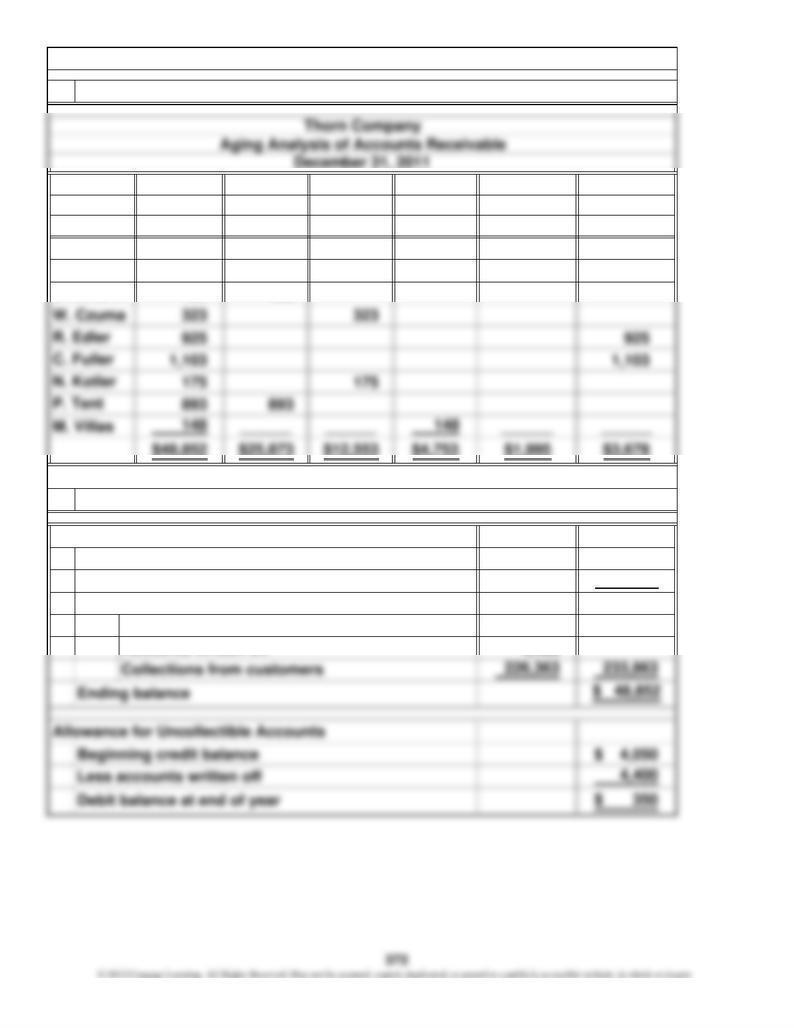

$44,820 $24,515 $12,055 $4,605 $1,995 $1,650

465 465

$ 45,215

237,500

$282,715

Less: $ 3,100

4,400

Sales returns and allowances

Accounts Receivable

Beginning balance

Credit sales

Subtotal

Account

Accounts written off

Balance

S. Ballarin

Customer

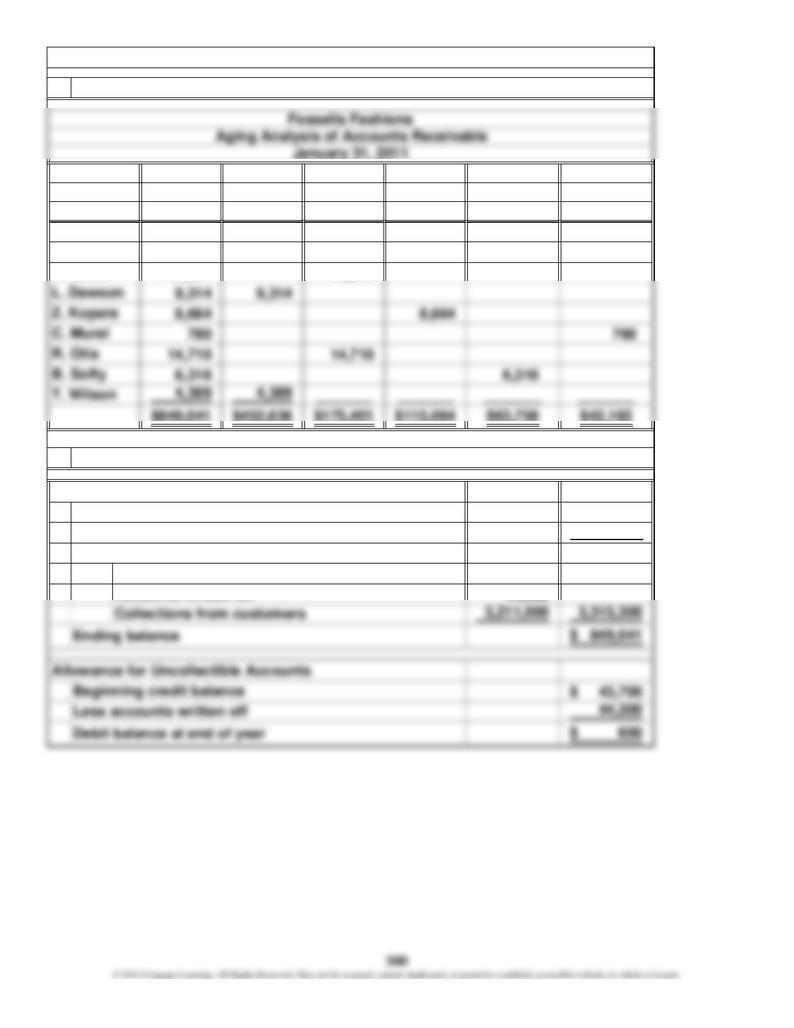

Chapter 7, P 3.

1. Aging analysis completed

Forward

2. End-of-year balances computed

analyze their accounts receivable history to determine the estimated percentage

uncollectible in each category. These percentages are multiplied by the amount in

5. User Insight: Role of estimates discussed

Estimates play an important role in applying the aging analysis method. Businesses

Estimated Uncollectible Accounts

Thorn Company

Chapter 7, P 3. (Continued)

3. Analysis of estimated uncollectible accounts prepared

Uncollectible accounts expense calculated

4.

28

30

31

+=

15

30

15

60

× 13 / 100 × 60 / = $170.96

$15,000.00

$443.84

Rate of

Interest ×Time

=

May 16, accepted $8,000, 60-day, 13% note receivable

Principal

Interest at maturity: $170.96

Chapter 7, P 4.

Days in June

Days in July

1. Maturity date, interest on the note, and maturity value for each note determined

May 3, accepted $15,000, 90-day, 12% note receivable

Days remaining in May (31 – 3)

$8,000 365

×

Interest

Days remaining in May (31 – 16)

Days in June

Days in July

Total days

July 15

August 1Maturity date:

Maturity date:

2. Interest income on June 30 reported

Since interest income on these notes receivable will not be received until maturity,

3. User Insight: Cash flow effect discussed

Date of

Accrued interest income as of June 30

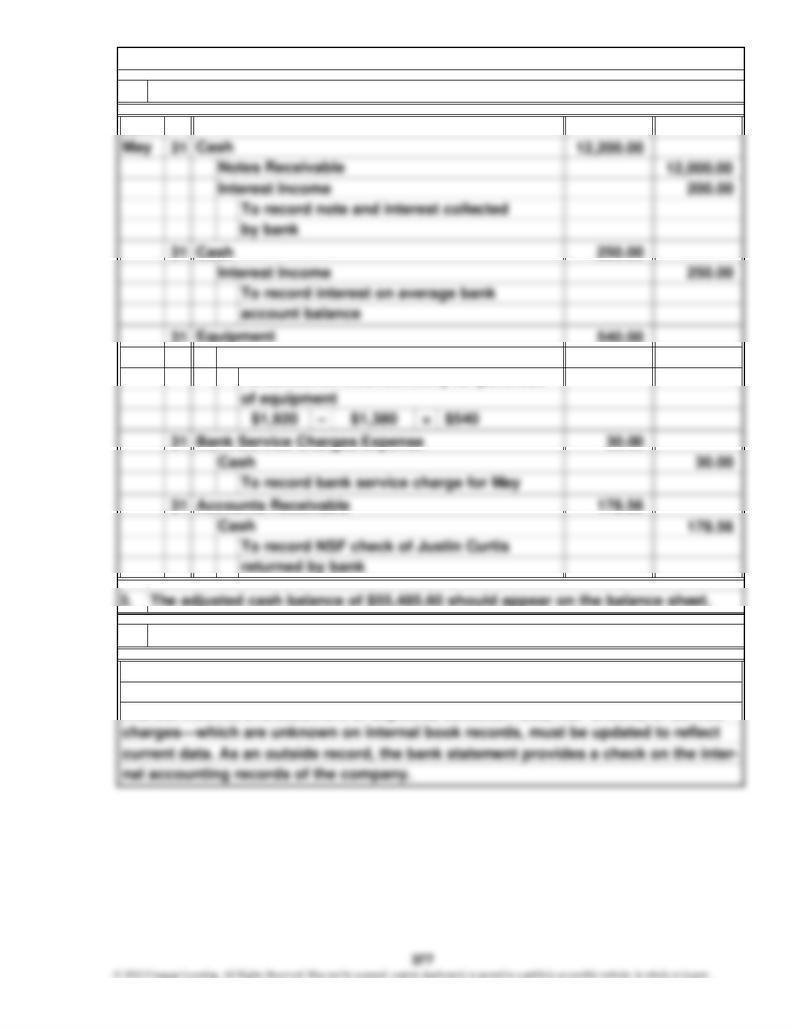

Chapter 7, P 4. (Continued)

Rate of

$203.42Interest at maturity:

3,936.80

178.56 748.56

NSF check of Justin Curtis

Less outstanding checks

1. Bank reconciliation prepared

Lotus Lake, Inc.

Chapter 7, P 5.

Bank Reconciliation

31 250.00 250.00

31 540.00 540.00

31 30.00 30.00

31 178.56 178.56

items—for example, a note receivable collected by a bank, interest income on a note,

interest income, overstatement of deposits, collection fees, NSF checks, or service

A bank reconciliation is a necessary internal control because certain events and

4. User Insight: Importance of bank reconciliation discussed

2. Journal entries prepared

2011

Chapter 7, P 5. (Continued)

Cash

To correct an incorrect entry for purchase

640,000

2,104,000

(

= $567,870

$49,930

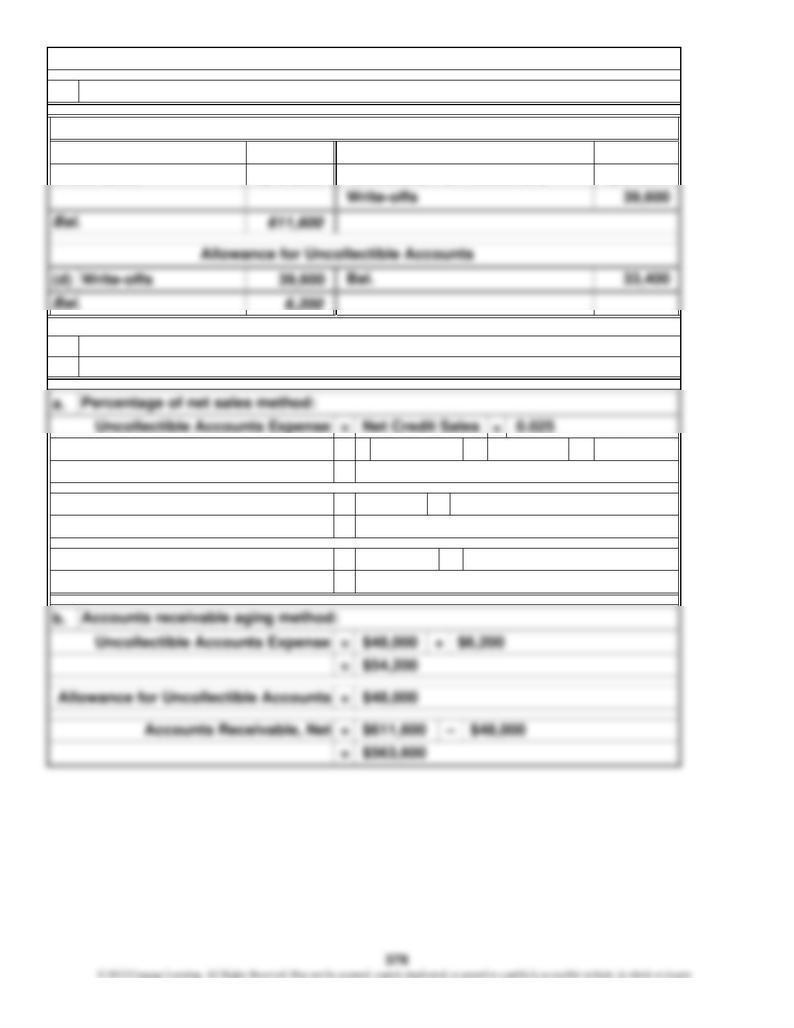

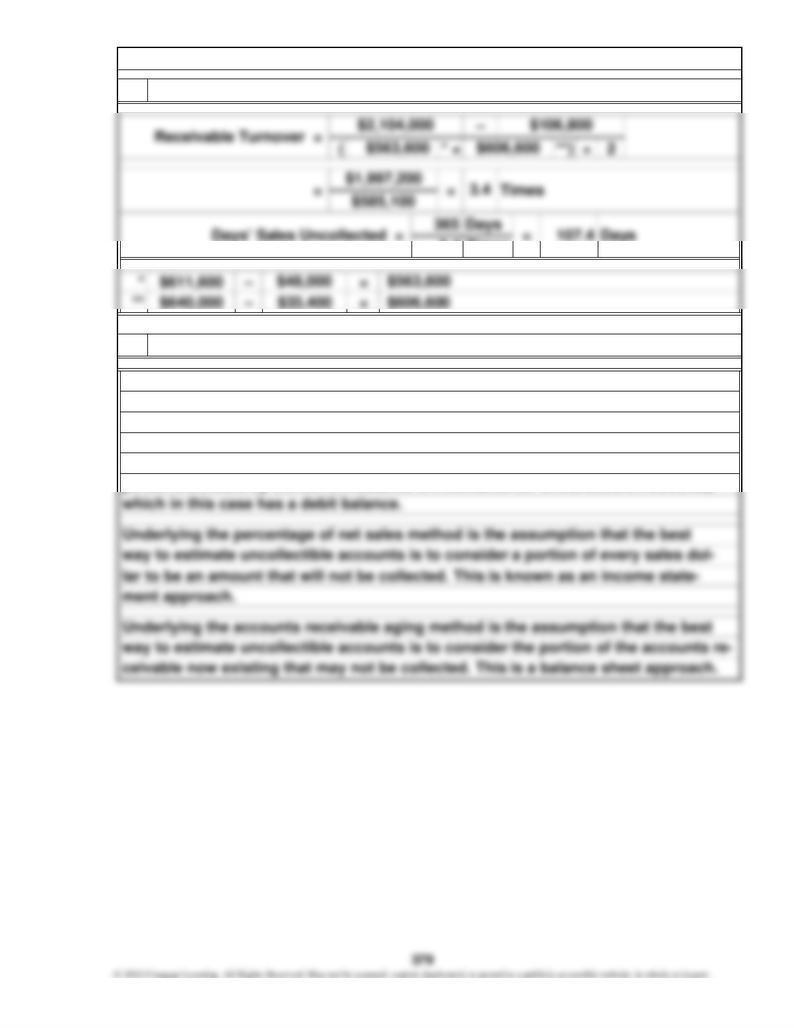

Accounts Receivable, Net

$43,730

Allowance for Uncollectible Accounts = –

Uncollectible accounts expense and ending balance of Allowance for

Bal.

Chapter 7, P 6.

1. T accounts prepared and data entered

106,800

1,986,000

Accounts Receivable

Credit sales

=

2. Uncollectible Accounts determined

Sales returns and allowances

Collections from customers

=

=

= $2,104,000 –

0.025

$49,930 $6,200

) ×

$611,600

$106,800

$43,730–

=

method are both estimates and are based on different assumptions, it is expected

Chapter 7, P 6. (Continued)

3. Receivable turnover and days' sales uncollected calculated

that they would differ in their effects. Also, the amount of uncollectible accounts

good the estimates of losses were in the prior year because the amount of ex-

User Insight: Difference in methods and rationales discussed

pense is affected by the current balance of Allowance for Uncollectible Accounts,

3.4

expense under the accounts receivable aging method depends partially on how

Because the percentage of net sales method and the accounts receivable aging

4.

1–30 31–60 61–90 Over

Not Yet Days Days Days 90 Days

Total Due Past Due Past Due Past Due Past Due

$793,791 $438,933 $149,614 $106,400 $57,442 $41,402

11,077 11,077

$ 442,341

3,722,000

$4,164,341

Less: $ 60,000

44,300

Account

Forward

2. End-of-year balances computed

Customer

Chapter 7, P 7.

1. Aging analysis completed

K. Baker

Accounts written off

Balance

Sales returns and allowances

Accounts Receivable

Beginning balance

Credit sales

Subtotal

4. Uncollectible accounts expense calculated

Fossella Fashions

Chapter 7, P 7. (Continued)

3. Analysis of estimated uncollectible accounts prepared

Estimated Uncollectible Accounts

5. User insight: Role of estimates discussed

January 31, 2011

Estimates play an important role in applying the aging analysis method. Businesses

analyze their accounts receivable history to determine the estimated percentage

uncollectible in each category. These percentages are multiplied by the amount in

28

30

31

1

90

× 10 / 100 × 90 / = $1,479.45

+=

Interest at maturity:

$61,479.45

March 3, accepted $60,000, 90-day, 10% note receivable

Interest Maturity Value

×Time

$61,479.45

May 15Maturity date:

×

= Interest

$1,479.45

June 1

$60,000 365

Rate of

Interest

Chapter 7, P 8.

Days remaining in March (31 – 3)

Maturity date:

1. Maturity date, interest on the note, and maturity value for each note determined

Days in April

Days in May

Days in June

Principal

Principal

March 16, accepted $32,000, 60-day, 11% note receivable

Total days

$60,000.00 $1,479.45

+=

Maturity value:

$665.75Interest at maturity:

×Time

×

Rate of

Interest

Chapter 7, P 8. (Continued)

= InterestPrincipal

2. Interest income on April 30 reported

cash flow impact on June 30 is zero.

Accrued interest income as of April 30

Since interest income on these notes receivable will not be paid until maturity, the

3. User Insight: Cash flow effect discussed

383

3.

cash situation by offering more attractive terms for early payment, such as a sales

discount (for example, 2/10, n/60).

Since Gerard sells its appliances to large, established customers, the accounts

and notes receivable, which total $12 million, should provide adequate security to

raise the needed $10 million in cash. Gerard might also be able to improve its

billing operation are needed to handle the new credit customers. The small fee

the matching rule, each year Mitsubishi will need to estimate the amount of un-

lectible accounts that will arise from these credit sales and record it as an ad-

Chapter 7, C 1.

and payments because management felt that such terms would increase sales

September. Third, there is the cost of uncollectible accounts. In accordance with

Mitsubishi established the generous credit terms of 14 months without interest

dramatically. Customers could make large purchases without emptying their

pockets. There are three main costs to Mitsubishi. First, a credit department and

charged to the dealer will help cover that cost. Second, there is an implicit inter-

est cost associated with carrying the no-interest receivables until the following

Chapter 7, C 4.

is 54.5 and 59.8 days for 2008 and 2009, respectively. Although days' sales uncol-

lected for Fosters are decreasing, it takes Fosters longer to collect a receivable

than it does Heineken. Thus, proportionately, Fosters has more capital tied up in

its receivables. However, it is not possible to determine which company has the

$1,046,000 $1,048,000 $1,008,000

== 3.2%

3.1%

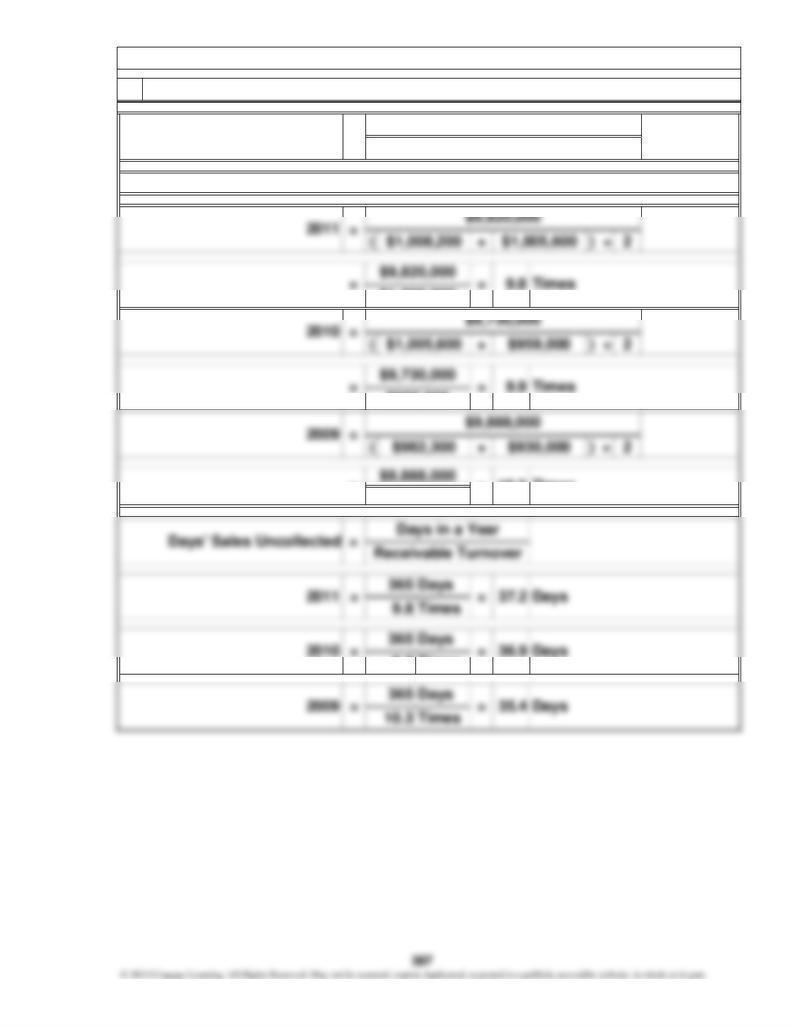

Chapter 7, C 5.

1. Financial ratios computed (dollar amounts in thousands)

2011 2010

2009

Receivable

9.9

10.3 Times

Times

9.9

=

9.8=

=

=

=

(Note: The net accounts receivable needs to be calculated for 2011, 2010, and 2009.)

Receivable Turnover Average Accounts Receivable

Net Sales

Chapter 7, C 5. (Continued)

2. Receivable turnover and days' sales uncollected calculated

$956,150

$982,300

$1,006,900

Ratios interpreted

2011. Thus, the ratio of allowance for uncollectible accounts to accounts receivable

pense. However, perhaps management has been underestimating the amounts that

for the three years exceed the total provisions made for uncollectible accounts ex-

This opinion is also supported by the fact that the net accounts written off in total

has decreased from 4.9 percent in 2009 to 3.6 percent in 2011.

Chapter 7, C 5. (Continued)

3.

1.

2.

3.

needed in the last quarter.

have excess cash from operations after the fourth quarter (which is also the bal-

ance sheet date) and in the first half of the year. More cash for operations will be

be fairly steady during the course of the year. However, there is some variation.

In Note 15, it may be observed that the sales are lowest in the first and third

quarters (January to March and July to September) of the year. The fourth quar-

ter (October to December) has the most sales. Thus, the company is likely to

Chapter 7, C 6.

makes few sales to consumers on credit, its note on accounts receivable states

389

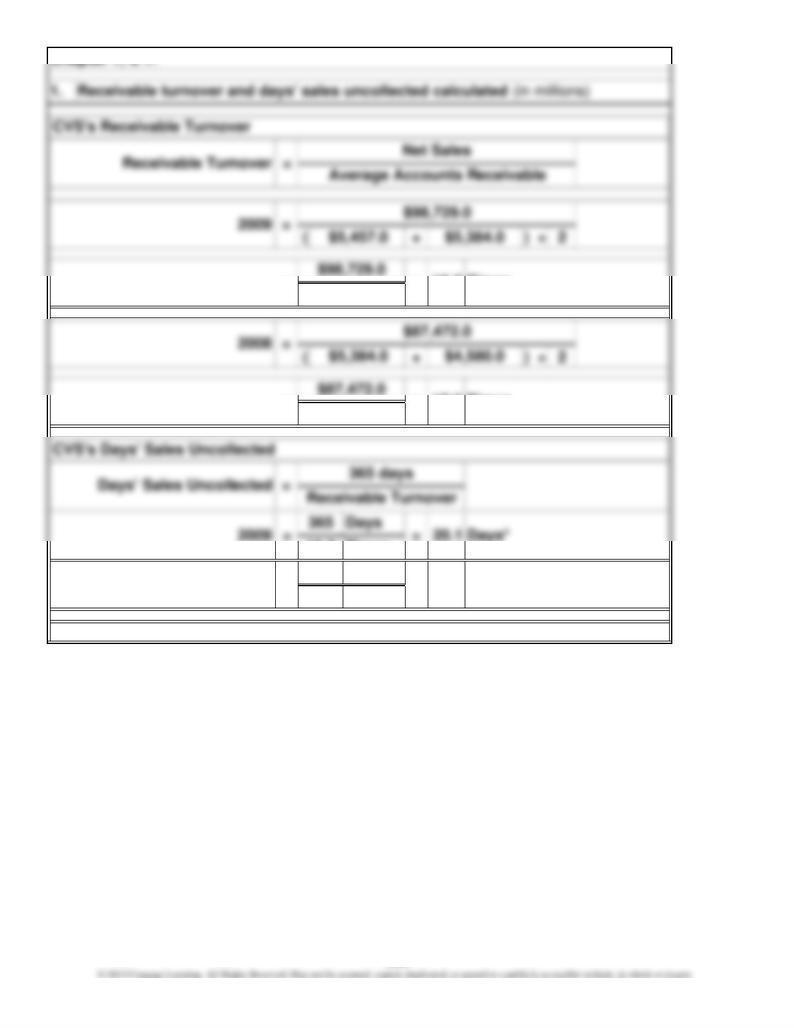

365 = Days*20.72008 17.6

$4,982.0

Times

=

18.2

=

18.2

Chapter 7, C 7.

$5,420.5 =

=

17.6

Times

Times

*Rounded

=

Days

390

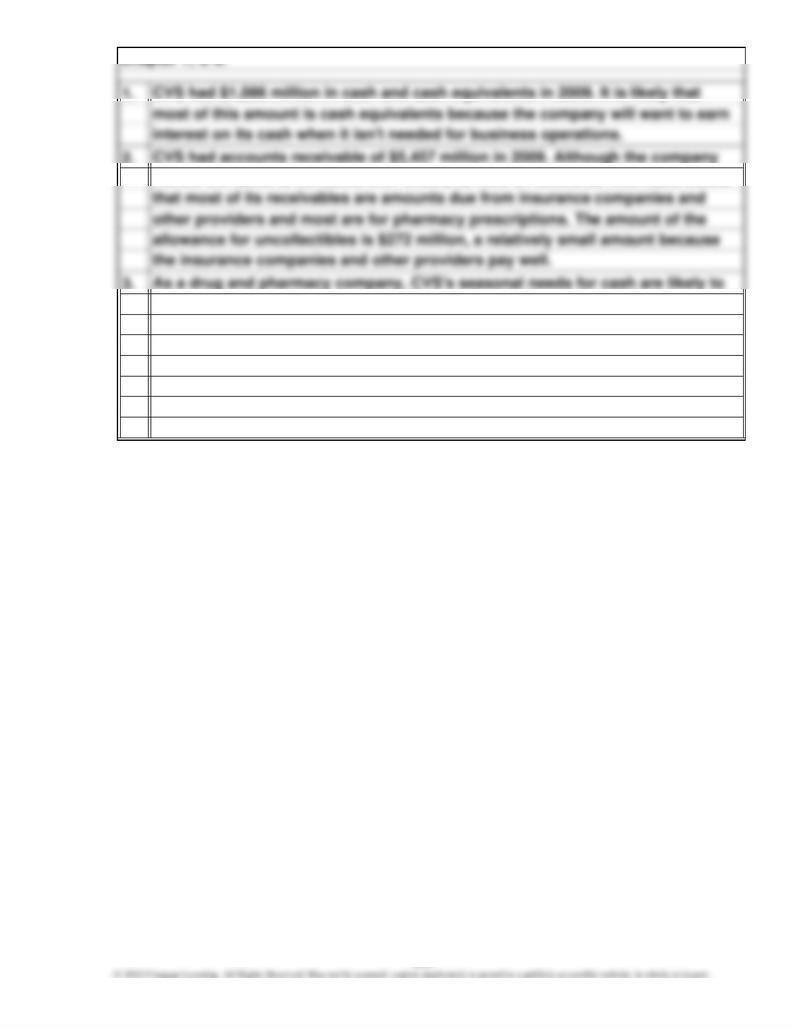

2.

is expected because both CVS and Walgreens sell mostly to retail customers who

pay with cash or credit cards or to insurance companies (for prescriptions) that

that CVS has some insurance accounts for its pharmacy items.

denced by the high receivable turnovers and short days' sales uncollected. This

Walgreens does, as shown by the receivables turnovers. This probably means

$2,382.0

=

pay quickly. On a basis relative to sales, CVS has about as many receivables as

Walgreens' Days' Sales Uncollected

=

25.2

= $2,511.5

Times

24.8

391

This case addresses several issues that get at the heart of the question, does ac-

counting matter? The main issue is whether accounting should be used to accom-

Chapter 7, C 8.