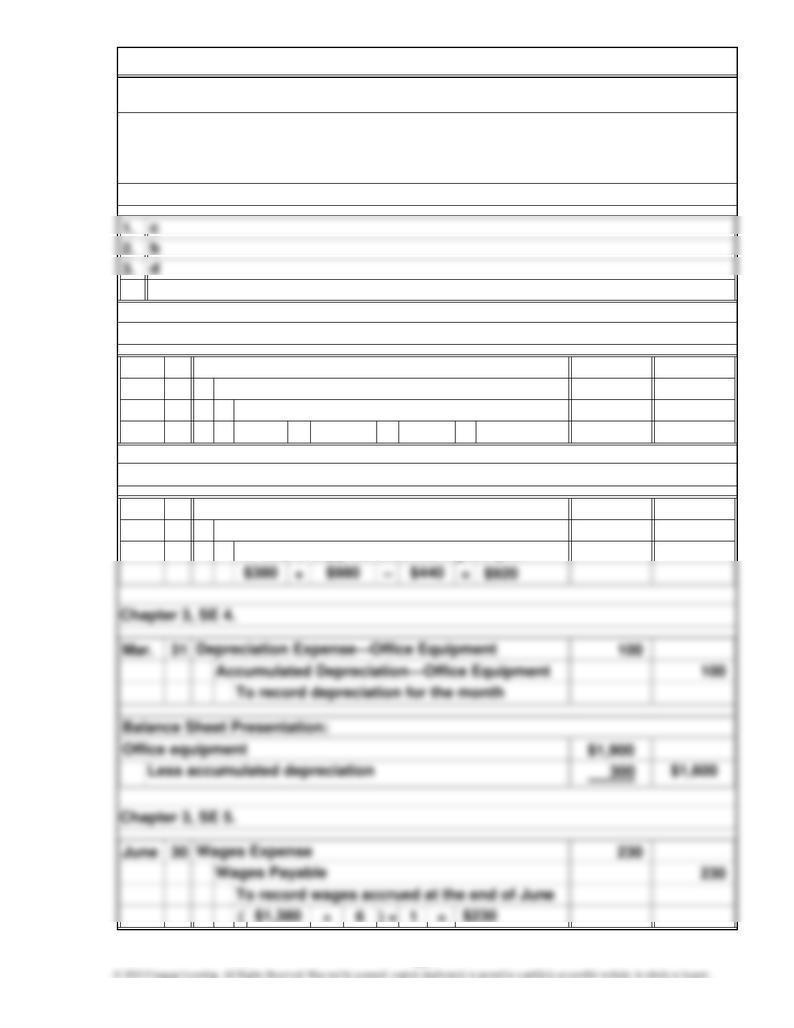

4.

31 800 800

+ – = $800

Dec. 31 920 920

(÷6) ×1=

Supplies Expense

To record supplies used during the year

Insurance ExpenseDec.

$700

Prepaid Insurance

Supplies

a

$1,040

Chapter 3, SE 2.

$460

Chapter 3, SE 1.

Chapter 3, SE 3.

CHAPTER 3—Solutions

MEASURING BUSINESS INCOME

To record insurance expired during the year

101

31 760 760

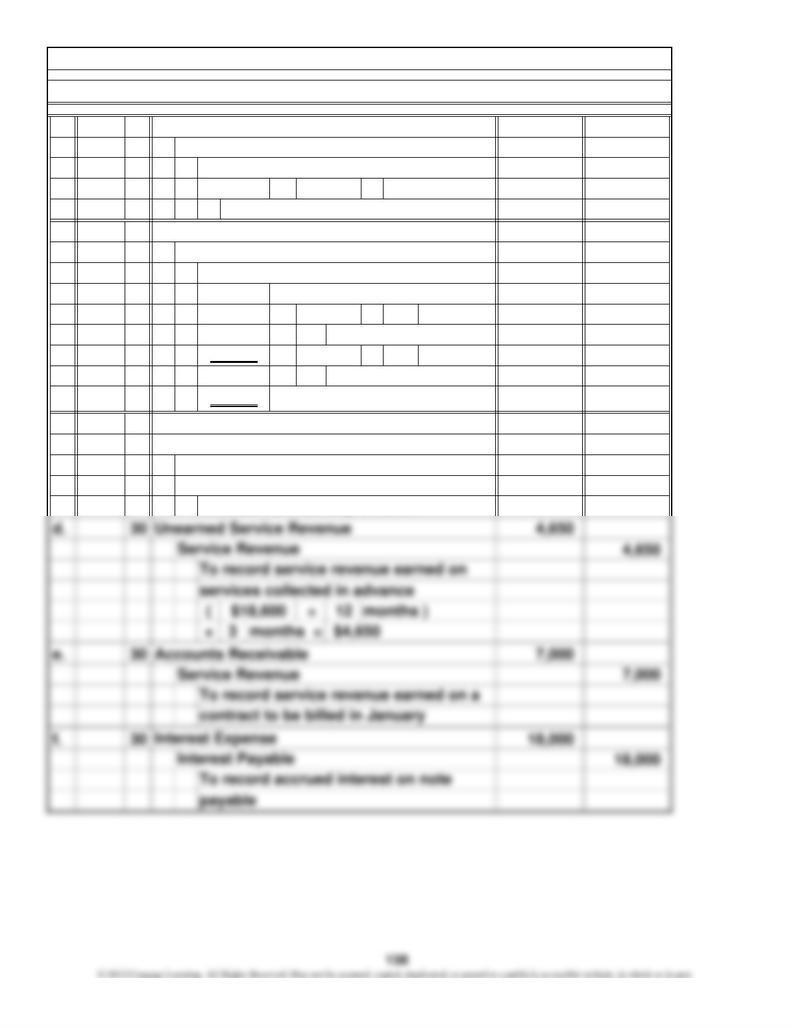

To record service revenue earned during

August on which advance deposits had

been received

$1,300

$450

200

175

100

25 950

$ 350

$4,300

350

$4,650

175

$4,475

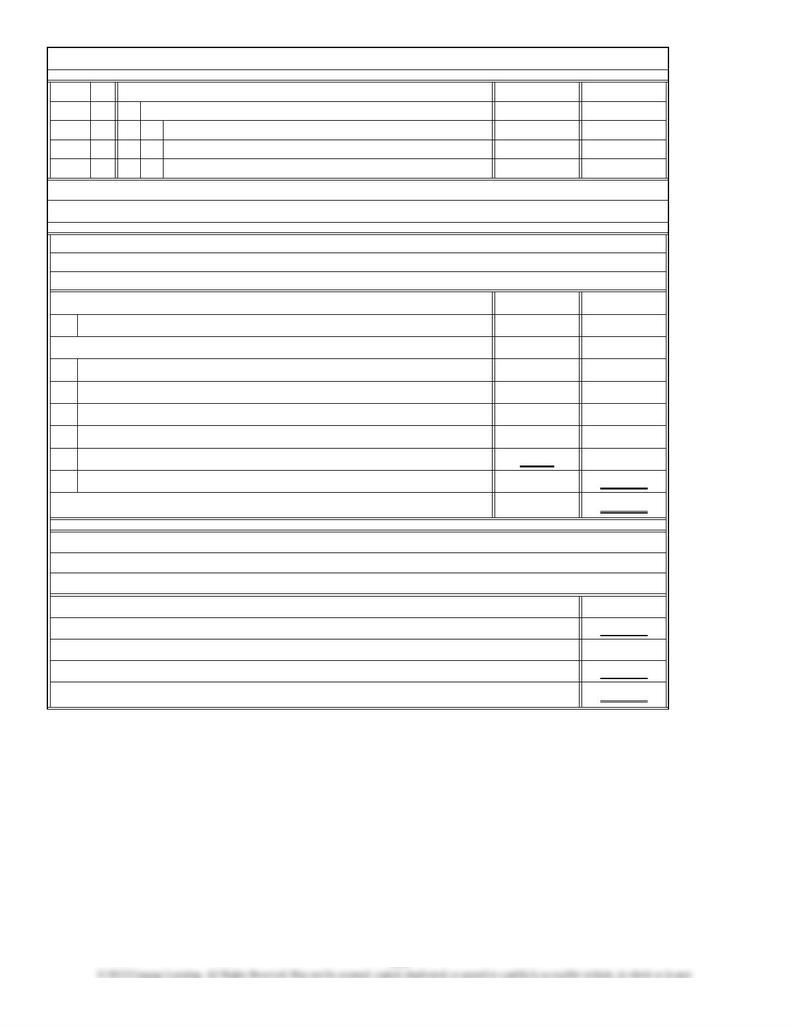

Shimura Company

Statement of Retained Earnings

For the Month Ended December 31, 2011

Less dividends

Retained earnings, December 31, 2011

Unearned Service Revenue

Retained earnings, November 30, 2011

Net income

Subtotal

Net income

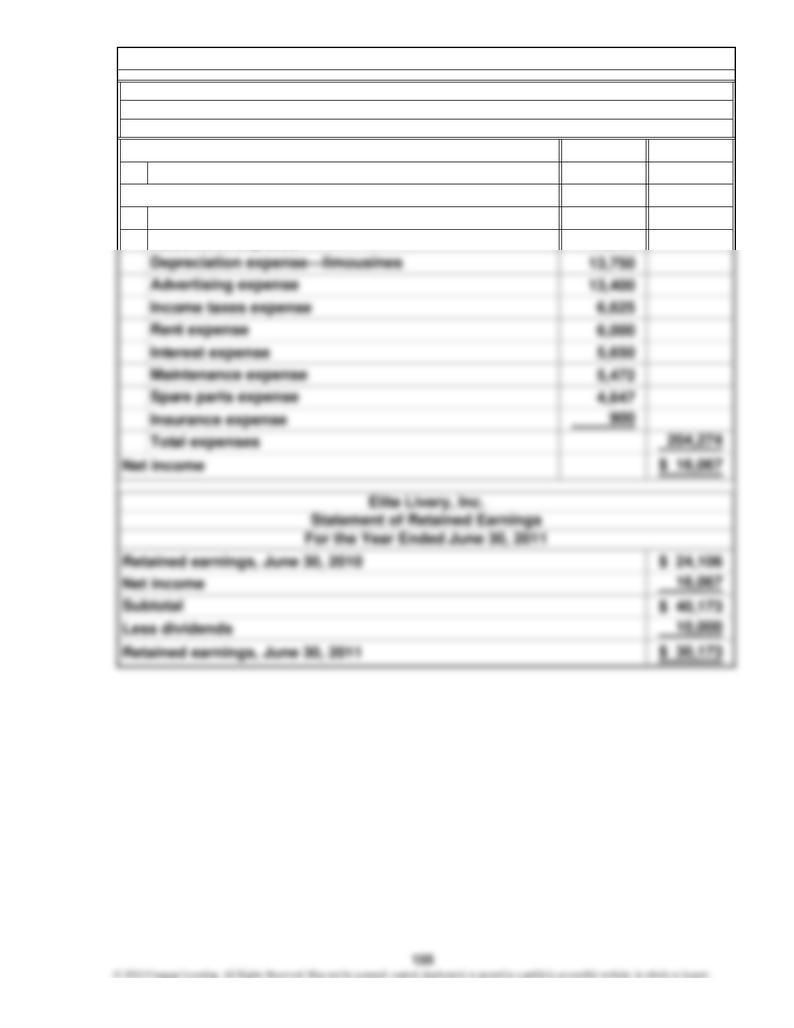

Total expenses

Rent expense

Chapter 3, SE 6.

Service Revenue

Shimura Company

Income Statement

Aug.

Chapter 3, SE 7.

Service revenue

For the Month Ended December 31, 2011

Revenue

Expenses

Income taxes expense

Utilities expense

Telephone expense

Wages expense

102

Dec. 31 1,300 1,300

950 450

200

175

100

25

350 350

175 175

Dividends

To close the Dividends account

Retained Earnings

Retained Earnings

To close the Income Summary account

To close the expense accounts

Income Summary

Income Summary

To close the revenue account

Wages Expense

Rent Expense

Telephone Expense

Income Summary

Income Taxes Expense

Utilities Expense

Service Revenue

Chapter 3, SE 8.

Closing entries prepared

103

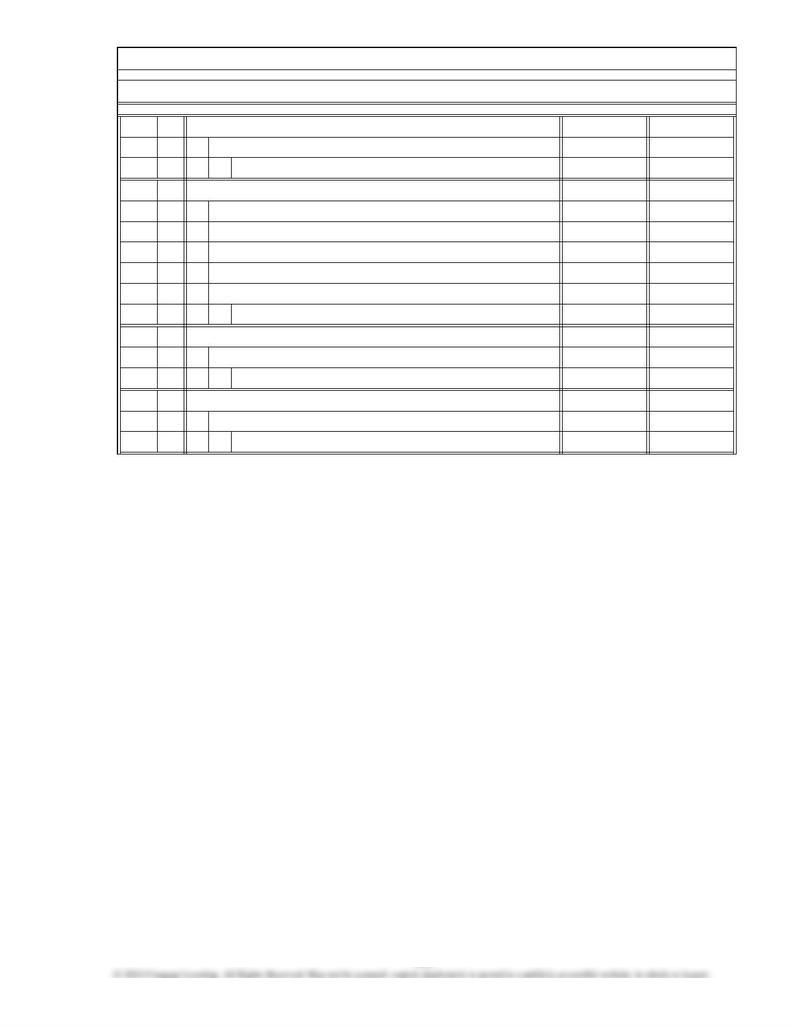

For the Month Ended October 31, 2011

Cloud Company

Income Statement

Chapter 3, SE 9.

Chapter 3, SE 10.

Chapter 3, SE 11.

2.

3.

4.

1.

2.

3.

3. 6.

in relation to its net income.

of liquidity. It tells how much cash is generated by the company's operations

c

e

the Supplies T account. The amount expended in cash to purchase supplies

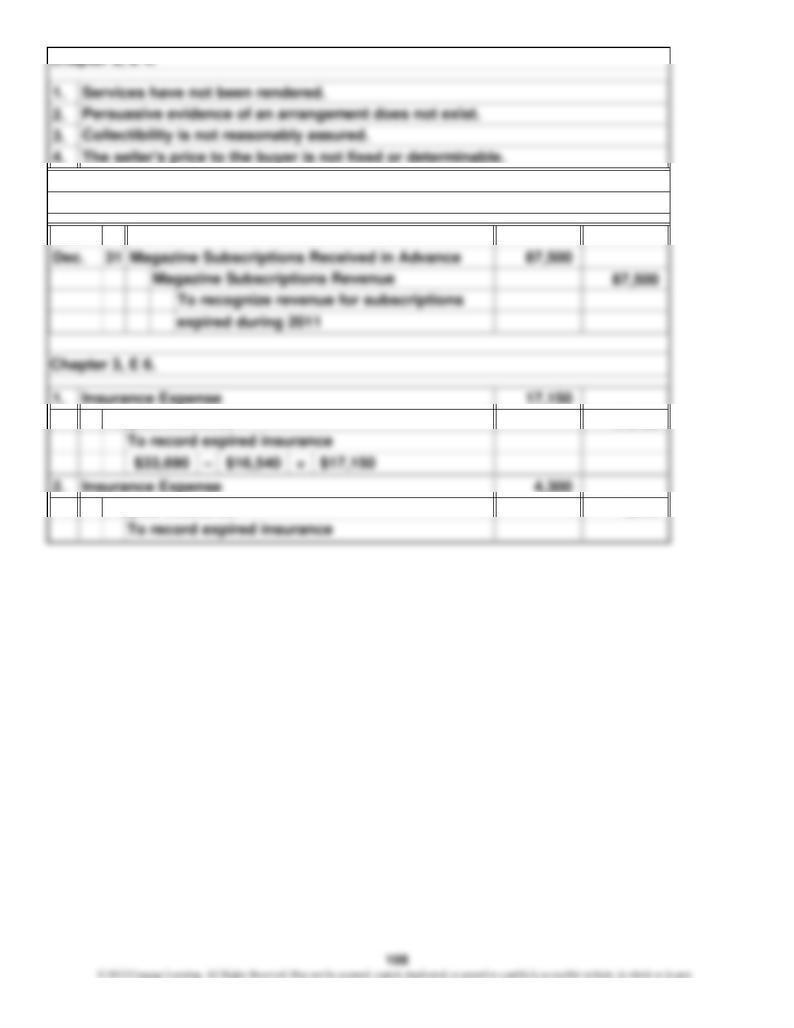

Chapter 3, E 1.

4.

1. 17,150 17,150

2. 4,300 4,300

Chapter 3, E 5.

Chapter 3, E 4.

2011

Prepaid Insurance

Prepaid Insurance

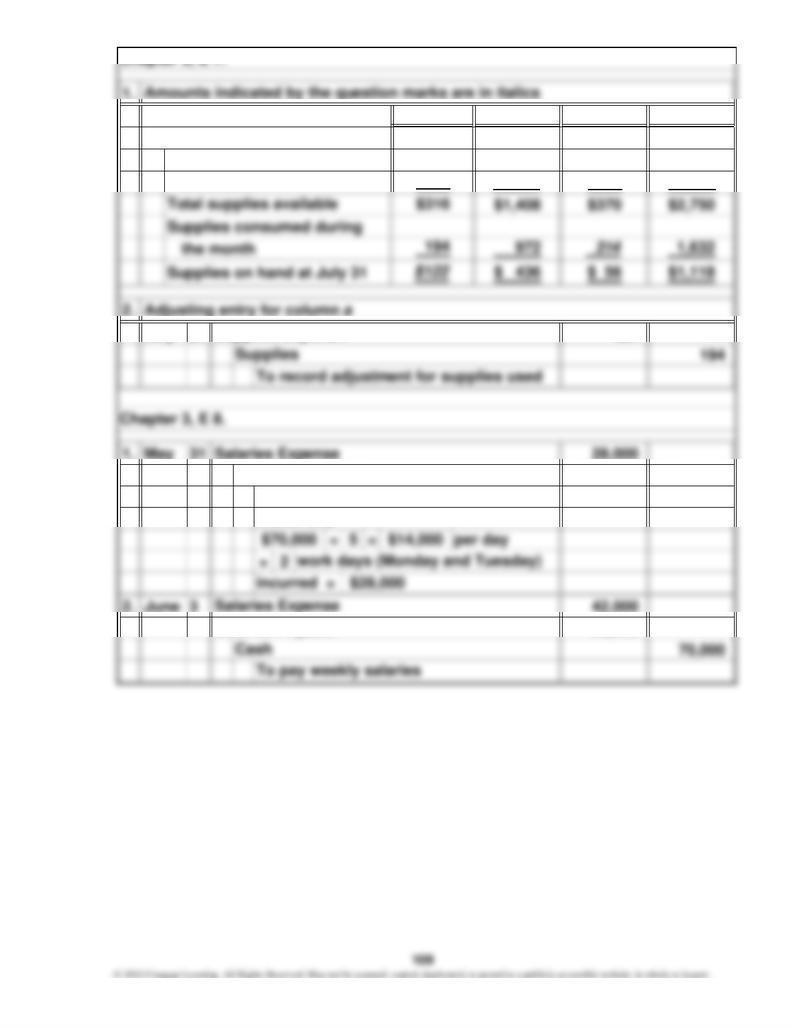

1. bcd

$ 217 $196 $ 822

1,191 174 1,928

2. 31 194 194

1. 31 28,000 28,000

2. June 3 42,000

28,000 70,000

$264

52

To accrue salaries owed but not paid at

month end $14,000 per day

Salaries Payable

Chapter 3, E 7.

a

Salaries Payable

Supplies on hand at July 1

Supplies purchased during

the month

July Supplies Expense

$20,000

31 64,500 64,500

31 64,500 64,500

1. Royalty expense and royalty income calculated

2. Adjusting entries recorded

To record royalties owed for the last half of

Royalty Expense

Royalty Payable

Dec.

2011

Dec.

Chapter 3, E 9.

In Bit Comp, Inc.'s records:

In Regina Company's records:

2011 Royalty Receivable

January to June 2011 (payment on November 1)

2011, to be paid on May 1, 2011

Royalty Income

To record royalties earned for the last half

of 2011, to be received on May 1, 2011

110

$14,620

$5,680

2,920

1,200

800

720

580

380

320 12,600

$ 2,020

$11,034

2,020

$13,054

2,000

$11,054

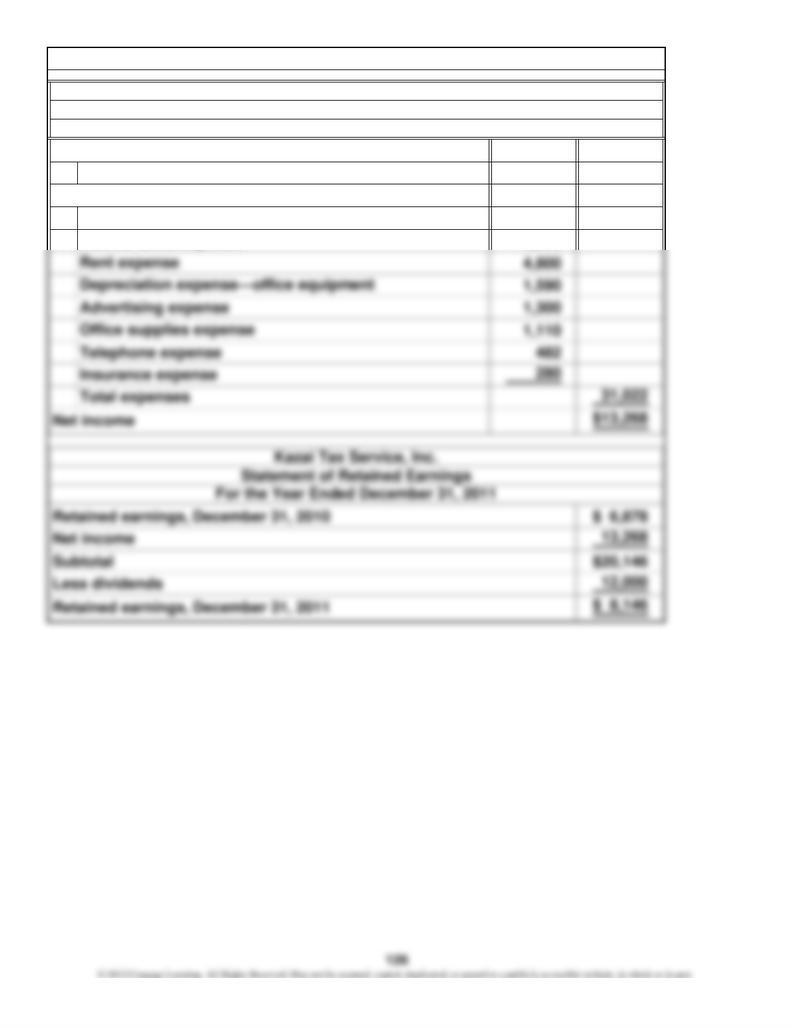

Retained earnings, August 31, 2011

Net income

Income taxes expense

Total expenses

Less dividends

For the Month Ended August 31, 2011

Retained earnings, July 31, 2011

Spark Cleaning Company, Inc.

Statement of Retained Earnings

Subtotal

Janitorial revenue

Wages expense

Rent expense

Chapter 3, E 10.

For the Month Ended August 31, 2011

Spark Cleaning Company, Inc.

Income Statement

Expenses

Net income

Depreciation expense—cleaning equipment

Depreciation expense—truck

Revenue

Gas, oil, and other truck expenses

Insurance expense

Supplies expense

111

$ 4,590

2,592

Accounts receivable

Cash

Chapter 3, E 10. (Continued)

Spark Cleaning Company, Inc.

Assets

Balance Sheet

August 31, 2011

Chapter 3, E 11.

1. 428 428

2. 1,065 1,065

3. 900 900

4. 425 425

5. 375 375

6. 400 400

To record service revenue earned but not billed

Chapter 3, E 12.

Office Supplies

To record supplies consumed during the year

Service Revenue

Beginning balance

$168

114

1 42,000 42,000

2.

31 31,700 31,700

31 23,275 13,500

3,000

2,650

2,525

1,600

31 8,425 8,425

31 7,000 7,000

Dec. Consulting Fees Earned

Office Salaries Expense

Income Summary

Retained Earnings

To close the expense accounts

Advertising Expense

To close the Dividends account

Income Summary

Retained Earnings

Dividends

To close the Income Summary account

Income Summary

Rent Expense

Income Taxes Expense

Cash

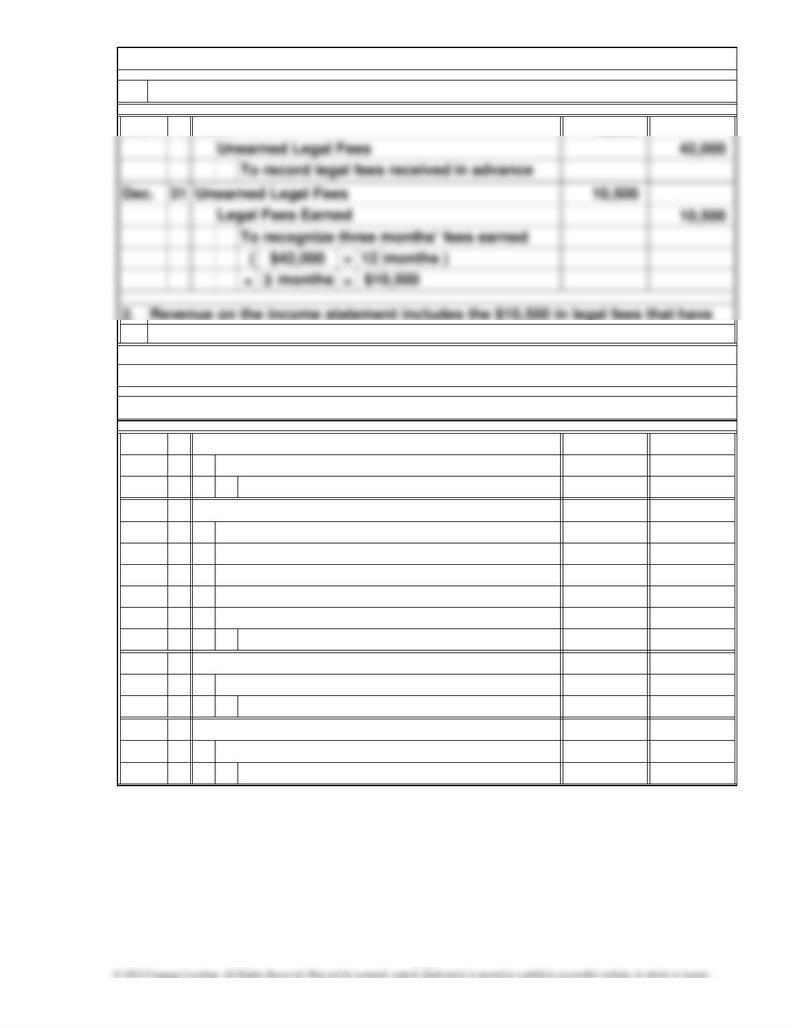

been earned. Unearned Legal Fees is a liability of $31,500 on the balance sheet.

Chapter 3, E 14.

Closing entries recorded

Telephone Expense

To close the revenue account

Chapter 3, E 13.

Entries recorded1.

Oct.

115

$52,000

44,000

Retained earnings, December 31, 2010

Statement of retained earnings prepared

Chapter 3, E 15.

Statement of Retained Earnings

For the Year Ended December 31, 2011

Cindy's Beauty Salon, Inc.

Net income

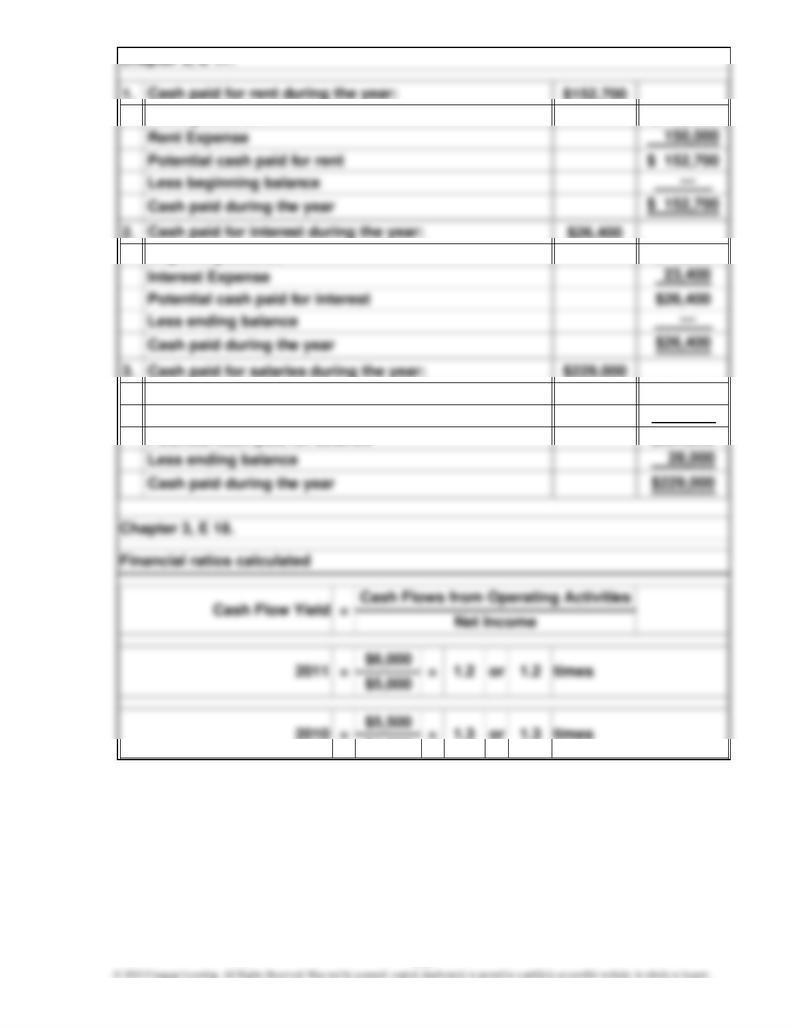

1. $152,700

2. $26,400

3. $229,000

$4,300

$ 3,000

$257,000

242,000

$ 15,000

2010

times1.3

Salaries Expense

Potential cash paid for salaries

$ 2,700

Beginning balance

Ending balance

Beginning balance

Chapter 3, E 17.

117

Income Adjustment

Amount of

(+ or –)Statement Account

a. June 30 26,000 26,000

b. 30 22,440 22,440

( ÷ 5 3 days

=

c.

d. 30 8,824 8,824

+ – = $8,824

e. 30 6,514 6,514

[( ÷

×6

1. Adjusting entries recorded

Interest Expense

$37,400

Interest Payable

To record accrued interest on mortgage

Chapter 3, P 2.

Insurance Expense

$8,230

months ]

$5,800

To record expired insurance

Prepaid Insurance

$3,230 $2,636

12 months )2,900

$3,240

To record supplies used

Salaries Payable

Salaries Expense

To record accrued salaries

days )

Supplies

No entry

Supplies Expense

$22,440 ×

2. User Insight: Revenue recognition discussed

In transaction c, no revenue is recognized because even though a contract has

Chapter 3, P 2. (Continued)

been signed, no services have yet been provided or earned. In transaction h, the

Bal. 9,250 Bal. 1,331 (a) 1,181

(g) 1,550 Bal. 150

Bal. 5,675

Bal. 660 (b) 305 Bal. 4,620

Bal. 355 (c) 263

Bal. 1,033

Bal. 2,970 Bal. 5,500 (f) 902 Bal. 1,485

Bal. 583

Accounts Payable

Accumulated Depreciation—

Income Taxes Payable

Notes Payable

770

Prepaid Rent Office Equipment Office Equipment

Bal. 4,125

2. Adjusting entries posted to the accounts

Bal.

Chapter 3, P 3.

Cash Accounts Receivable Office Supplies

Unearned Service Revenue

Interest Payable Salaries Payable

$ 9,250

5,675

150

355

4,620 $ 1,033

2,970

5,500

583

285

165

Adjusted Trial Balance

Office Supplies

Chapter 3, P 3. (Continued)

3. Adjusted trial balance prepared

Prepaid Rent

December 31, 2011

Financial Service, Inc.

Accounts Receivable

Accumulated Depreciation—Office Equipment

Accounts Payable

Cash

Interest Payable

Unearned Service Revenue

Notes Payable

Office Equipment

Salaries Payable

a.

b.

c.

d.

Balance sheet, income statement, statement of retained earnings

Balance sheet, income statement, statement of retained earnings

Balance sheet, income statement, statement of retained earnings

Balance sheet, income statement, statement of retained earnings

Chapter 3, P 3. (Continued)

4. User Insight: The following financial statements are affected by the adjustments:

Bal. 480 (b) 280

Bal. 200

Bal. 1,560 (a) 1,110 Bal. 14,200 Bal. 1,540

Bal. 450 Bal. 3,130

(e) 438 Bal. 438 (f) 4,860

(d) 42 Bal. —

2. Adjusting entries posted to the accounts

Unearned Tax Fees Revenue

Bal.

Accounts Payable

2,198

Office Supplies

7,400

Office Equipment

Chapter 3, P 4.

Cash Accounts Receivable Prepaid Insurance

Bal.

1,270 Income Taxes Payable

Bal.

1,590(c)

Office Equipment Accumulated Depreciation—

$ 7,400

2,198

200

450

14,200 $ 3,130

1,312

4,860

7,000

6,878

12,000 44,290

16,600

1,300

4,800

482

280

1,110

1,590

4,860

$67,470 $67,470

Note: Unearned Tax Fees Revenue does not appear on the adjusted trial balance

because it now has a zero balance.

Office Supplies Expense

Depreciation Expense—Office Equipment

Income Taxes Expense

Rent Expense

Accumulated Depreciation—Office Equipment

Cash

Income Taxes Payable

Common Stock

Telephone Expense

Tax Fees Revenue

Insurance Expense

3. Adjusted trial balance, income statement, statement of retained earnings,

Prepaid Insurance

and balance sheet prepared

Chapter 3, P 4. (Continued)

Office Supplies

December 31, 2011

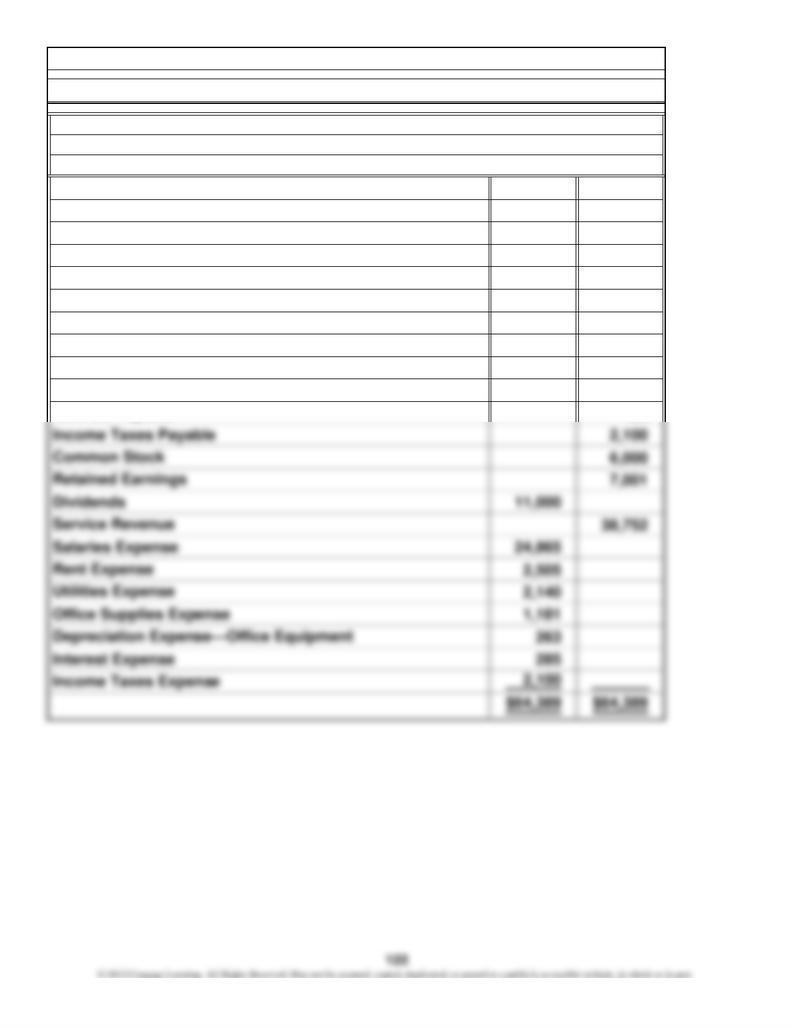

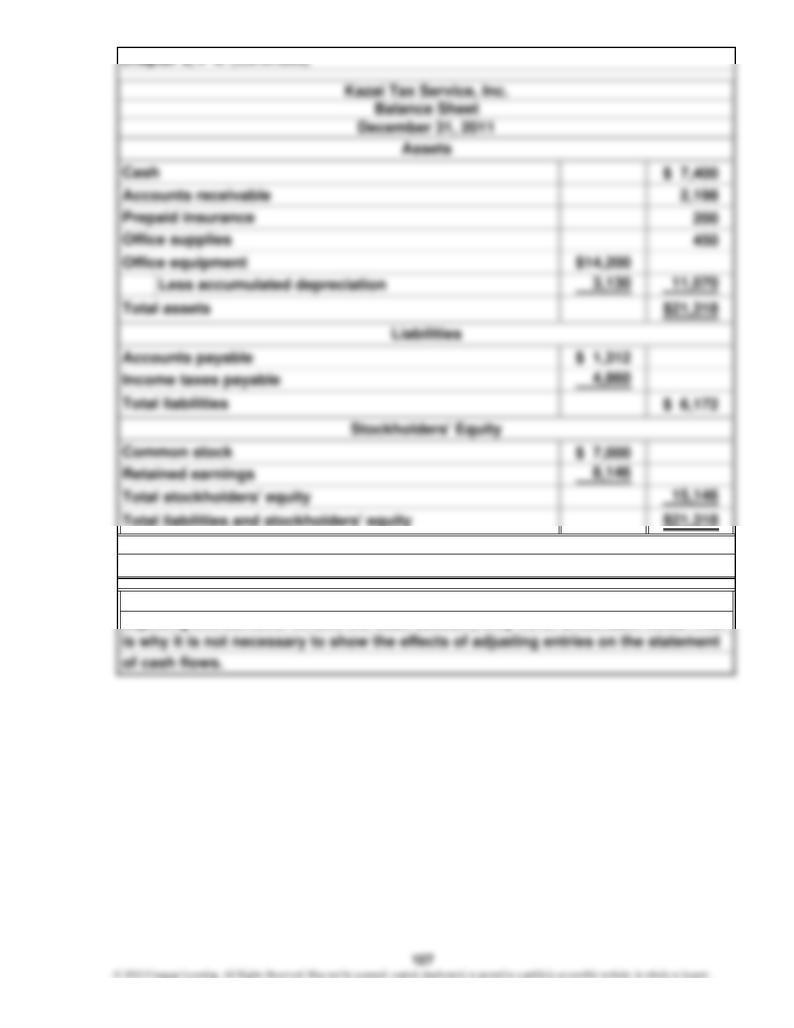

Kazai Tax Service, Inc.

Accounts Receivable

Adjusted Trial Balance

Advertising Expense

Retained Earnings

Dividends

Office Equipment

Office Salaries Expense

Accounts Payable

125

$44,290

$16,600

4,860

Revenue

Expenses

Tax fees revenue

Office salaries expense

Income taxes expense

Kazai Tax Service, Inc.

Chapter 3, P 4. (Continued)

Income Statement

For the Year Ended December 31, 2011

Chapter 3, P 4. (Continued)

4. User Insight: The effect of adjusting entries discussed

By definition, adjusting entries cannot include a debit or a credit to Cash. Because

adjusting entries never involve the Cash account, they never affect cash flows. That

Page 14

Post.

Ref. Debit Credit

2011

a. June 30 514 6,000

117 6,000

b. 30 515 900

118 900

c. 30 518 5,472

119 5,472

d. 30 516 4,647

141 4,647

advance

To record spare parts used during

1. Adjusting entries recorded in the general journal

Date

during the year

Spare Parts Expense

Spare Parts

during the year

Insurance Expense

Prepaid Maintenance

Maintenance Expense

Prepaid Insurance

General Journal

To record insurance that expired

Description

Prepaid Rent

Rent Expense

To expense one year's rent paid in

To record amount of deposit used

Chapter 3, P 5.

Ref. Debit Credit Debit Credit

30 4,906

Ref. Debit Credit Debit Credit

30 7,114

Ref. Debit Credit Debit Credit

30 6,000

30 J14 6,000 —

Ref. Debit Credit Debit Credit

30 2,450

30 J14 900 1,550

Ref. Debit Credit Debit Credit

30 6,000

30 J14 5,472 528

3. Adjusting entries posted from the general journal

Account No. 118

Adjustment

June Balance

2011

Balance

Post.

Adjustment

Date Item

Post.

2011

June Balance

Balance

Date Item

Prepaid Maintenance

Prepaid Insurance

Account No. 119

BalanceJune

Date Post.

Balance

Chapter 3, P 5. (Continued)

Cash

2011

Account No. 111

Post.

2011

June

Balance

Item

Account No. 112

Balance

June

2011

Balance

Account No. 117

Balance

Post.

Accounts Receivable

Date

Item

Prepaid Rent

Item

Adjustment

Date

129

Ref. Debit Credit Debit Credit

30 5,655

30 J14 4,647 1,008

Ref. Debit Credit Debit Credit

30 110,000

Ref. Debit Credit Debit Credit

30 17,500

30 J14 13,750 31,250

Ref. Debit Credit Debit Credit

30 22,500

Ref. Debit Credit Debit Credit

30 15,000

30 J14 6,092 8,908

Ref. Debit Credit Debit Credit

30 J14 5,650 5,650

Balance

2011

June Balance

2011

June Balance

Date Item Post.

Post.

Date Item

Accumulated Depreciation—Limousines

Limousines Account No. 142

Date

Adjustment

2011 Item Balance

Item

Adjustment

Balance

Post.

June

Interest Payable

Date

Unearned Passenger Service Revenue Account No. 212

Balance

Balance

Spare Parts Account No. 141

2011

Post.

Date Item

Account No. 143

Chapter 3, P 5. (Continued)

June Balance

Notes Payable Account No. 211

Balance

Post.

ItemDate

June Balance

2011

2011

Adjustment

Account No. 213

June

Post.

Adjustment

Balance

130

Ref. Debit Credit Debit Credit

Income Taxes Payable Account No. 214

Date Item Balance

Chapter 3, P 5. (Continued)

Post.

2011

Chapter 3, P 5. (Continued)

Chapter 3, P 5. (Continued)

$ 4,906

7,114

1,550

528

1,008

110,000

$ 31,250

22,500

8,908

5,650

6,625

20,000

24,106

10,000 220,341

44,650

103,180

13,400

6,000

900

4,647

13,750

5,472

5,650

6,625

$339,380 $339,380

Gas and Oil Expense

Common Stock

Retained Earnings

Interest Payable

Maintenance Expense

Cash

Adjusted Trial Balance

Prepaid Maintenance

June 30, 2011

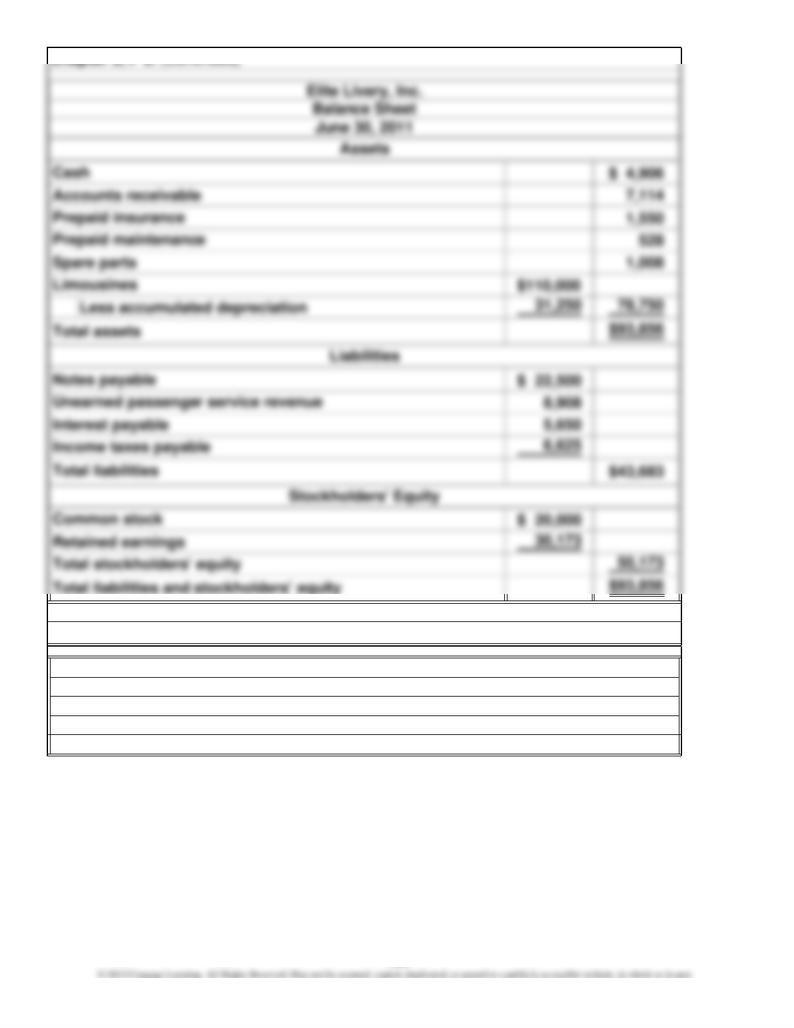

Elite Livery, Inc.

Interest Expense

and balance sheet prepared

Notes Payable

4. Adjusted trial balance, income statement, statement of retained earnings,

Chapter 3, P 5. (Continued)

Note: Prepaid Rent does not appear on the adjusted trial balance because it now has

Accounts Receivable

Income Taxes Payable

Advertising Expense

Salaries Expense

Limousines

Accumulated Depreciation—Limousines

Passenger Service Revenue

Insurance Expense

Spare Parts Expense

Depreciation Expense—Limousines

Income Taxes Expense

Unearned Passenger Service Revenue

Prepaid Insurance

a zero balance.

Spare Parts

Dividends

Rent Expense

134

$220,341

$103,180

44,650

Chapter 3, P 5. (Continued)

Elite Livery, Inc.

Income Statement

For the Year Ended June 30, 2011

Revenue

Expenses

Salaries expense

Passenger service revenue

Gas and oil expense

5. User Insight: The effect of adjustments discussed

Chapter 3, P 5. (Continued)

Adjusting entries affect net income on the income statement, and therefore they

to decrease.

affect the cash flow yield. After the adjustments have been posted in the previous

parts of the problem, the cash flow yield for the year has increased because the

additional expenses recorded exceed the additional revenues, causing net income

136

Amount of

Adjustment

(+ or –)

a. 30 5,171 5,171

+–

=

b. 30 6,874 6,874

[ ( ÷ 12

×5

[ ( ÷ 36

×2

c. 30 16,000

40,000 16,000

40,000

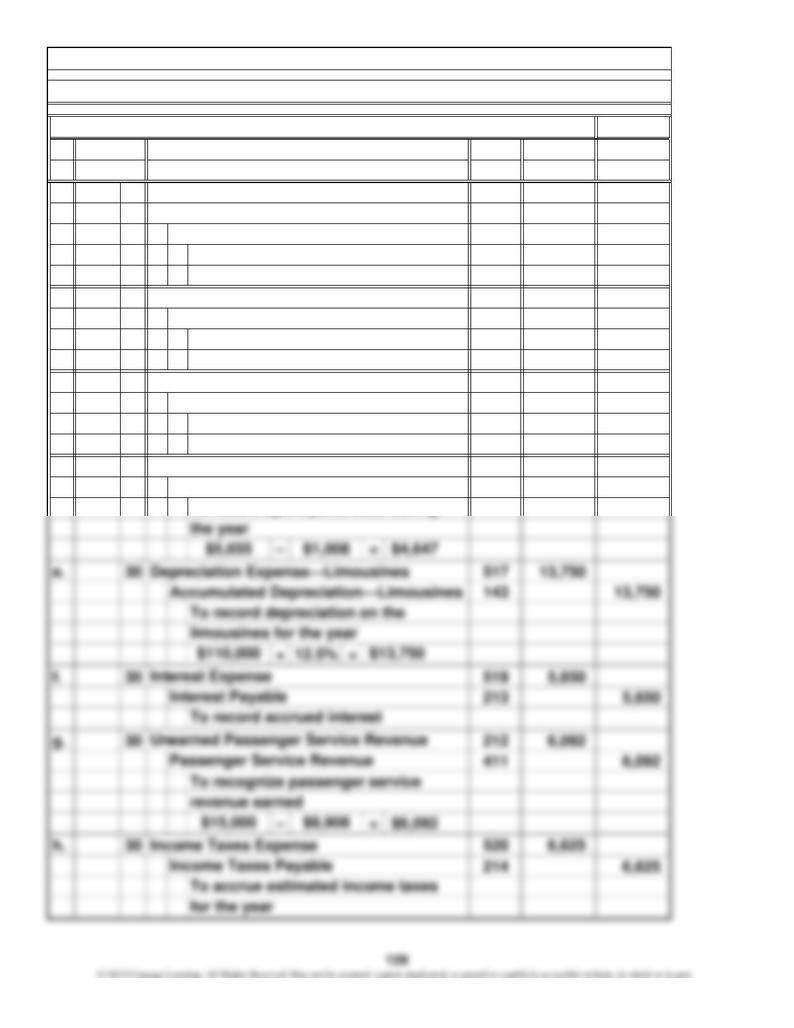

Chapter 3, P 7.

1. Adjusting entries recorded

Nov.

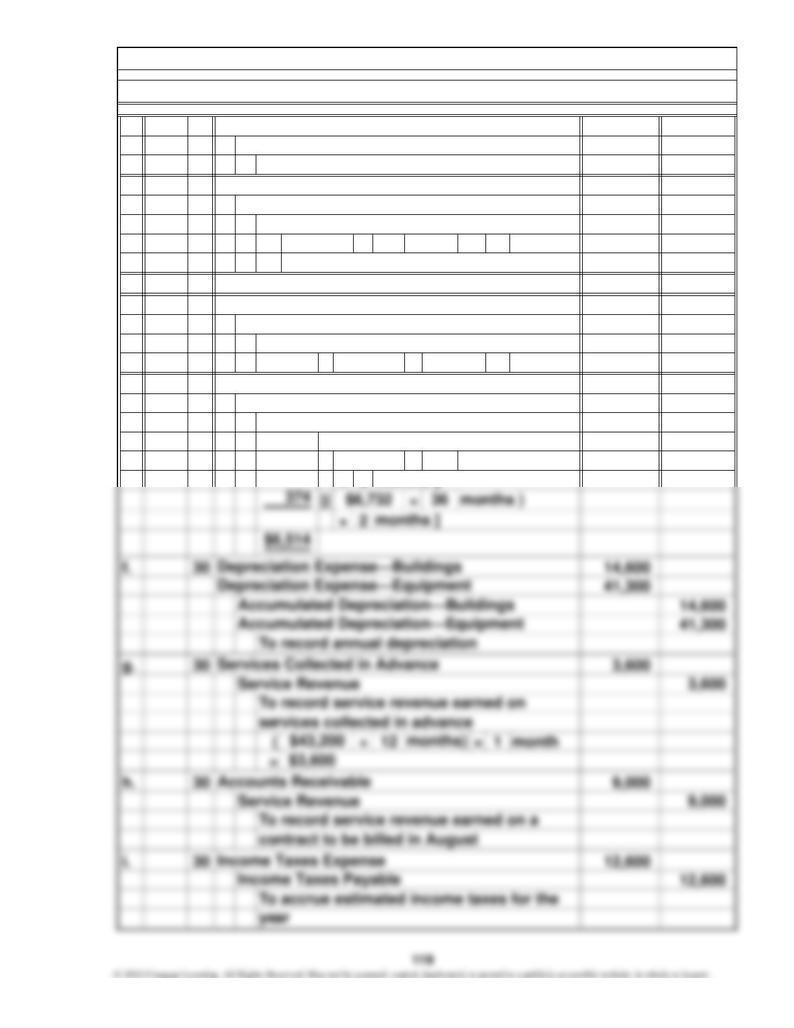

Depreciation Expense—Buildings

Depreciation Expense—Equipment

months )

Supplies Expense

Supplies

To record supplies used

Prepaid Insurance

$1,397$2,350 $4,218

$5,171

Insurance Expense

To record expired insurance

months ]

$7,272

$4,200

$4,720

1,750

404

$6,874

To record annual depreciation

Accumulated Depreciation—Equipment

Accumulated Depreciation—Buildings

months )

months ]

2. User Insight: Revenue recognition discussed

In transaction e, $7,000 has to be recognized as revenue because services have

Chapter 3, P 7. (Continued)

already been provided and there is an obligation to pay for them. In transaction h,

Bal. 13,786 Bal. 991 (a) 894

(g) 915 Bal. 97

Bal. 25,755

Bal. 1,400 (b) 500 Bal. 7,300

Bal. 900 (c) 720

Bal. 3,320

Bal. 1,820 Bal. 10,000 (d) 600

Accounts Payable

Office Equipment

2. Adjusting entries posted to the accounts

Accumulated Depreciation—

Chapter 3, P 8.

Cash Accounts Receivable Office Supplies

Prepaid Rent Bal.

Unearned Service RevenueSalaries Payable

Interest Payable

Income Taxes Payable

2,600

Notes Payable

24,840

Office Equipment

Bal.

$ 13,786

25,755

97

900

7,300 $ 3,320

1,820

10,000

600

230

1,410

Notes Payable

Office Equipment

Interest Payable

Unearned Service Revenue

Salaries Payable

Accumulated Depreciation—Office Equipment

Accounts Payable

Cash

Chapter 3, P 8. (Continued)

3. Adjusted trial balance prepared

Prepaid Rent

December 31, 2011

Sigma Consultants Corporation

Accounts Receivable

Adjusted Trial Balance

Office Supplies

a.

b.

c.

d.

Chapter 3, P 8. (Continued)

4. User Insight: The following financial statements are affected by the adjustments:

Balance sheet, income statement, statement of retained earnings

Balance sheet, income statement, statement of retained earnings

Balance sheet, income statement, statement of retained earnings

Balance sheet, income statement, statement of retained earnings

Bal. 195 (b) 130

Bal. 65

Bal. 610 (a) 430 Bal. 6,800 Bal. 670

Bal. 180 Bal. 1,320

(e) 315 Bal. 315 (f) 2,385

(d) 45 Bal. —

650(c)

970

Office EquipmentOffice Supplies Office Equipment

Income Taxes Payable

Bal. Bal.3,650

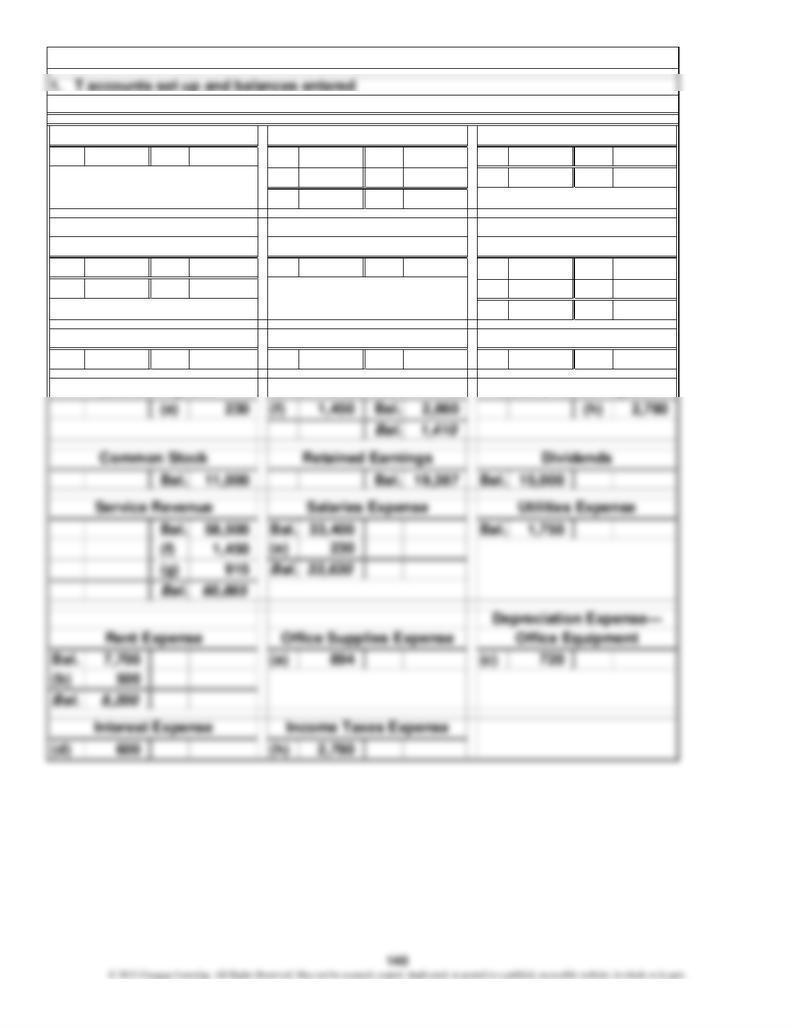

Chapter 3, P 9.

Cash Accounts Receivable Prepaid Insurance

2. Adjusting entries posted to the accounts

Travel Fees RevenueAccounts Payable

Accumulated Depreciation—

590

Unearned

Bal

.

$ 3,650

970

65

180

6,800 $ 1,320

635

2,385

3,300

3,117

4,200 20,394

8,300

585

2,350

456

130

430

650

2,385

$31,151 $31,151

Advertising Expense

Retained Earnings

Dividends

Office Equipment

Office Salaries Expense

Accounts Payable

Chapter 3, P 9. (Continued)

Office Supplies

December 31, 2011

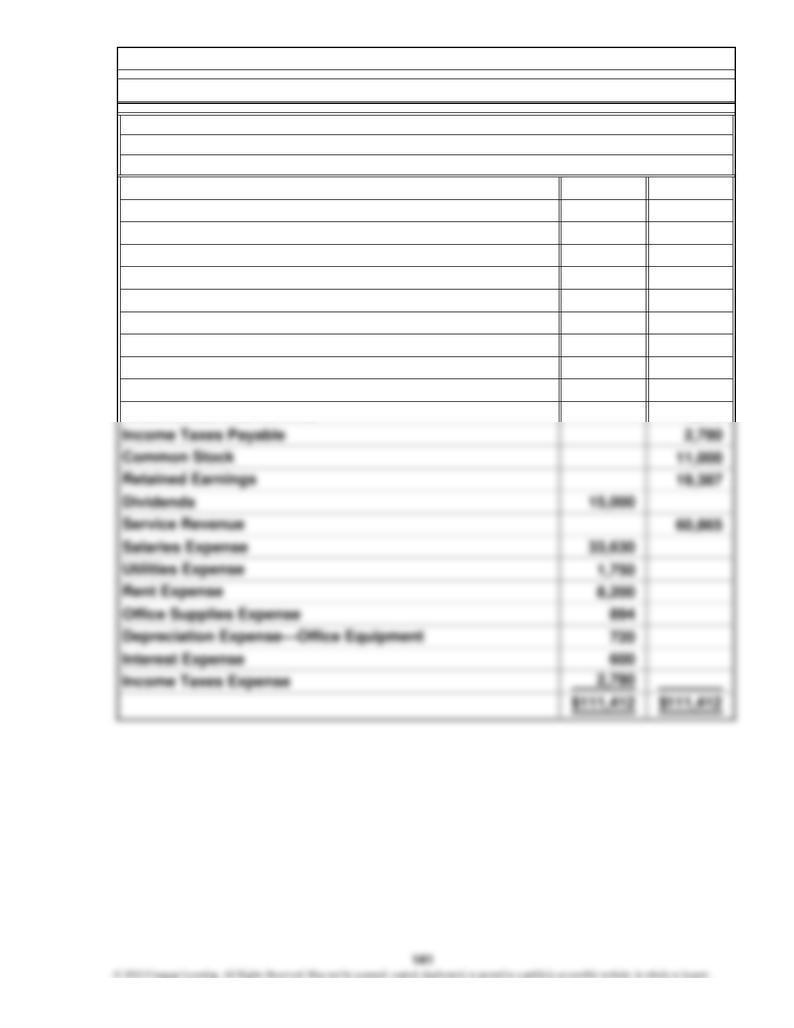

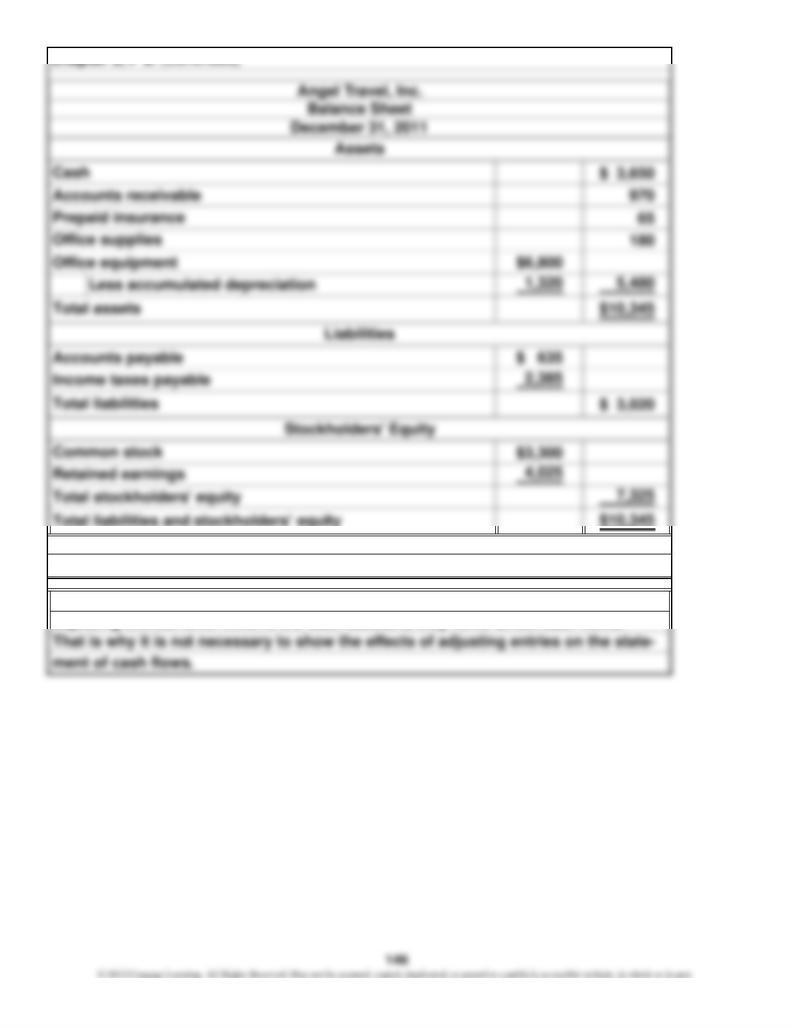

Angel Travel, Inc.

Accounts Receivable

Adjusted Trial Balance

3. Adjusted trial balance, income statement, statement of retained earnings,

Prepaid Insurance

and balance sheet prepared

Common Stock

Telephone Expense

Travel Fees Revenue

Insurance Expense

Note: Unearned Travel Fees Revenue does not appear on the adjusted trial balance

because it now has a zero balance.

Office Supplies Expense

Depreciation Expense—Office Equipment

Income Taxes Expense

Rent Expense

Accumulated Depreciation—Office Equipment

Cash

Income Taxes Payable

144

$20,394

$8,300

2,385

Chapter 3, P 9. (Continued)

Angel Travel, Inc.

Income Statement

For the Year Ended December 31, 2011

Income taxes expense

Expenses

Office salaries expense

Revenue

Travel fees revenue

4. User Insight: The effect of adjusting entries discussed

By definition, adjusting entries cannot include a debit or a credit to Cash. Because

adjusting entries never involve the Cash account, they never affect cash flows.

Chapter 3, P 9. (Continued)

Page 14

Post.

Ref. Debit Credit

2011

a. June 30 514 11,000

117 11,000

b. 30 515 1,400

118 1,400

c. 30 518 9,879

119 9,879

d. 30 516 12,520

141 12,520

1. Adjusting entries recorded in the general journal

Spare Parts Expense

during the year

To record insurance that expired

General Journal

Prepaid Insurance

during the year

To record amount of deposit used

Date

Maintenance Expense

Spare Parts

Prepaid Maintenance

Description

Insurance Expense

Chapter 3, P 10.

Prepaid Rent

Rent Expense

To expense one year's rent paid in

advance

Ref. Debit Credit Debit Credit

30 8,120

Ref. Debit Credit Debit Credit

30 13,270

Ref. Debit Credit Debit Credit

30 11,000

30 J14 11,000 —

Ref. Debit Credit Debit Credit

30 3,700

30 J14 1,400 2,300

Ref. Debit Credit Debit Credit

30 11,000

30 J14 9,879 1,121

3. Adjusting entries posted from the general journal

Date

Adjustment

Balance

Date

June

Prepaid Rent

Accounts Receivable

ItemDate

Post.

Balance

BalanceJune

2011

Balance

Account No. 117

Balance

Item

Account No. 112

Balance

Post.

Post.

2011

June

Chapter 3, P 10. (Continued)

Cash

2011

Account No. 111

Post.

Item

Account No. 119

Item

Date Item

Prepaid Maintenance Balance

Date

2011

June Balance

Adjustment

Account No. 118

June Balance

2011

Adjustment

Balance

Post.

Prepaid Insurance

148

Ref. Debit Credit Debit Credit

30 15,100

30 J14 12,520 2,580

Ref. Debit Credit Debit Credit

30 190,000

Ref. Debit Credit Debit Credit

30 25,000

30 J14 23,750 48,750

Ref. Debit Credit Debit Credit

30 48,000

Ref. Debit Credit Debit Credit

30 29,500

30 J14 15,965 13,535

Ref. Debit Credit Debit Credit

30 J14 11,800 11,800

Spare Parts Account No. 141

Balance

Date Balance

Post.

June Balance

2011

Notes Payable Account No. 211

Item

Adjustment

Post.

Date Item Balance

2011

June Balance

Account No. 143

Chapter 3, P 10. (Continued)

Balance

Account No. 213

Post.

June

2011

June

Interest Payable

Unearned Service Revenue Account No. 212

Balance

Balance

Accumulated Depreciation—Vehicles

Post.

Adjustment

2011 ItemDate

Date Item

Adjustment

Adjustment

Account No. 142Vehicles

Post.

Date Item Balance

Post.

2011

2011

June Balance

June

Date Item

Balance

149

Ref. Debit Credit Debit Credit

30 J14 12,980 12,980

2011

June Adjustment

Post.

Common Stock Account No. 311

Chapter 3, P 10. (Continued)

Income Taxes Payable Account No. 214

Date Item Balance

Chapter 3, P 10. (Continued)

Chapter 3, P 10. (Continued)

$ 8,120

13,270

2,300

1,121

2,580

190,000 $ 48,750

48,000

13,535

11,800

12,980

27,000

53,650

19,000 435,125

95,600

214,320

21,200

11,000

1,400

12,520

23,750

9,879

11,800

12,980

$650,840 $650,840

Dividends

Rent Expense

Income Taxes Expense

Service Revenue

Insurance Expense

Spare Parts Expense

Depreciation Expense—Vehicles

Note: Prepaid Rent does not appear on the adjusted trial balance because it now has

a zero balance.

Unearned Service Revenue

Accumulated Depreciation—Vehicles

4. Adjusted trial balance, income statement, statement of retained earnings,

Notes Payable

Spare Parts

Cash

Chapter 3, P 10. (Continued)

Income Taxes Payable

Advertising Expense

Salaries Expense

Vehicles

and balance sheet prepared

Prepaid Maintenance

June 30, 2011

Ray Heating & Cooling, Inc.

Accounts Receivable

Adjusted Trial Balance

Prepaid Insurance

Gas and Oil Expense

Common Stock

Retained Earnings

Maintenance Expense

Interest Expense

Interest Payable

153

$435,125

$214,320

95,600

Revenue

Expenses

Salaries expense

Service revenue

Gas and oil expense

Ray Heating & Cooling, Inc.

Income Statement

For the Year Ended June 30, 2011

Chapter 3, P 10. (Continued)

affect the cash flow yield. After the adjustments have been posted in the previous

parts of the problem, the cash flow yield for the year has increased because the

come and thus increasing cash flow yield.

additional expenses recorded exceed the additional revenues, decreasing net in-

Adjusting entries affect net income on the income statement, and therefore they

5. User Insight: The effect of adjustments discussed

Chapter 3, P 10. (Continued)

155

a.

b.

America Online (AOL) recognized advertising as an asset. However, advertising

Chapter 3, C 1.

Lucent Technologies recognized revenue. However, collectibility was not rea-

decisions. In other words, whenever Never Flake sold a rust-prevention coating,

there was an associated warranty expense that the company could expect to pay in

According to the concepts of accrual accounting and the matching rule, the ac-

countant must estimate and record (accrue) the expenses associated with a sale

expense undoubtedly led to poor management decisions and, eventually, to the

sonably assured. Therefore, Lucent Technologies violated the matching rule.

Chapter 3, C 2.

even though cash may not be paid out until future years. This procedure enables

which sales were made, Never Flake's management would have realized that it was

management to tell whether a company is earning an income and to make informed

company's bankruptcy.

either charging too little for the rust-prevention service or being too generous in

the period covered by the warranty. The failure to properly estimate the warranty

future years. If warranty expenses had been estimated correctly in the years in

4. Matching rule discussed

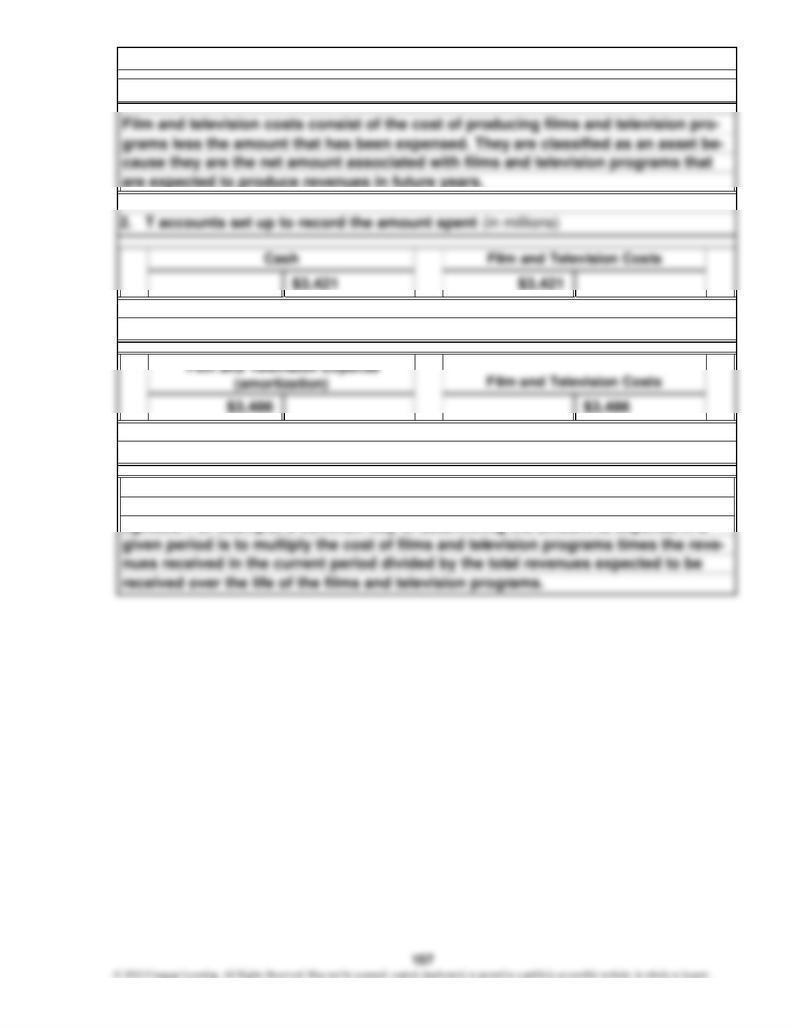

3. T accounts set up to record the amount expensed (in millions)

The matching rule attempts to allocate the costs of films and television programs

to the accounting periods in which the revenues associated with the costs are rec-

ognized. For example, a common way of determining the amount to expense in a

Chapter 3, C 4.

1. Film and television costs defined

1.

2.

3.

$3,212.0

$178

than that of Southwest in 2009. CVS is steady even though less in 2009.

CVS is steadier even though its cash flow yield decreased in 2009 and was less

flows in the lower portion of the statement where net income is reconciled to

= -8.5 or

-8.5

long-term assets like property and equipment can require adjustments to allo-

Chapter 3, C 5.

of depreciation expense depends on several estimates, such as the estimated

erally accepted accounting principles (GAAP). This means that management

has to make estimates and assumptions. For instance, determining the amount

times

1.2

158

the following year.

may receive an incorrect view of the company's progress and pay too high a price

for stock or lend too much money to the company. One must also ask what man-

agement's stake is in this issue. Is compensation tied to net income? Could man-

agers possibly lose their jobs if the financial results are not positive? The goal of

This question raises the issue of whether it would be unethical not to follow good

accounting practice. In answering this question, one must recognize who benefits

and who is harmed when good practices are not followed. If management's recom-

mendation is accepted, earnings will be overstated in 2011. Perhaps this overstate-

Students may suggest an alternative method: immediately recording the cash re-

ceived as revenue, but recording the estimated cost as an expense through an ad-

ment will hurt no one. But the likelihood is that various people with stakes in the

company will be hurt. For example, stockholders and creditors, such as banks,

is received, and because it is difficult to estimate the amount of the future expense.

To apply accrual accounting, the accountant must assume that it is possible to di-

vide the life of the business into time periods (periodicity) and that the business

will be a going concern long enough for the transactions and service contracts to

be resolved.

It is not appropriate to record the cash received for the service contracts as reve-

nues in the current year because policy coverage does not begin until the second

year of ownership. This would overstate net income in the first year when cash is

received. The expenses associated with these receipts will not be incurred for one

credit the Service Contract Revenue account for one year's worth or a portion of

a year's worth of the service contract. The remaining amount would be adjusted

actually provided, which is after the regular warranty period expires. At that time,

an entry would be made to debit the Unearned Service Revenue account and to

Chapter 3, C 7.

year or more from the date of receipt. This would cause the net income to be under-

justing entry. This method does not work as well because the service is provided

in the years in which the service contract applies, not in the year in which the cash

stated in the two years the policy actually covered—years 2 and 3 of ownership. To

give management a clear view of how the business is doing, accrual accounting

and the matching rule should be applied. This can be done by recording the cash

received as deferred revenue (a liability) until the period in which the service is

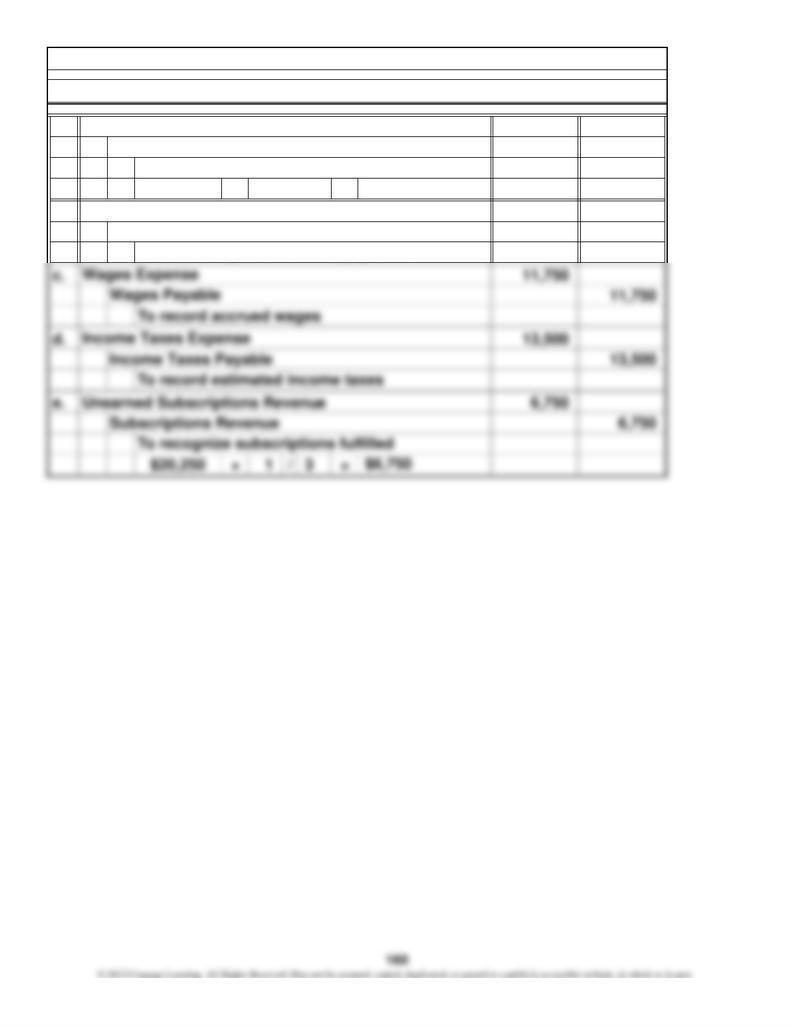

a. 22,500 22,500

$40,000 – =

b. 25,000 25,000

$17,500 $22,500

To record supplies used

Depreciation Expense—Equipment

To record depreciation on equipment

Printing Supplies

Printing Supplies Expense

Accumulated Depreciation—Equipment

Chapter 3, C 8.

1. Adjusting entries prepared

Before After

$432,500 (e) 6,750 $439,250

352,500 (a) 22,500

(b) 25,000

(c) 11,750

(d) 13,500 425,250

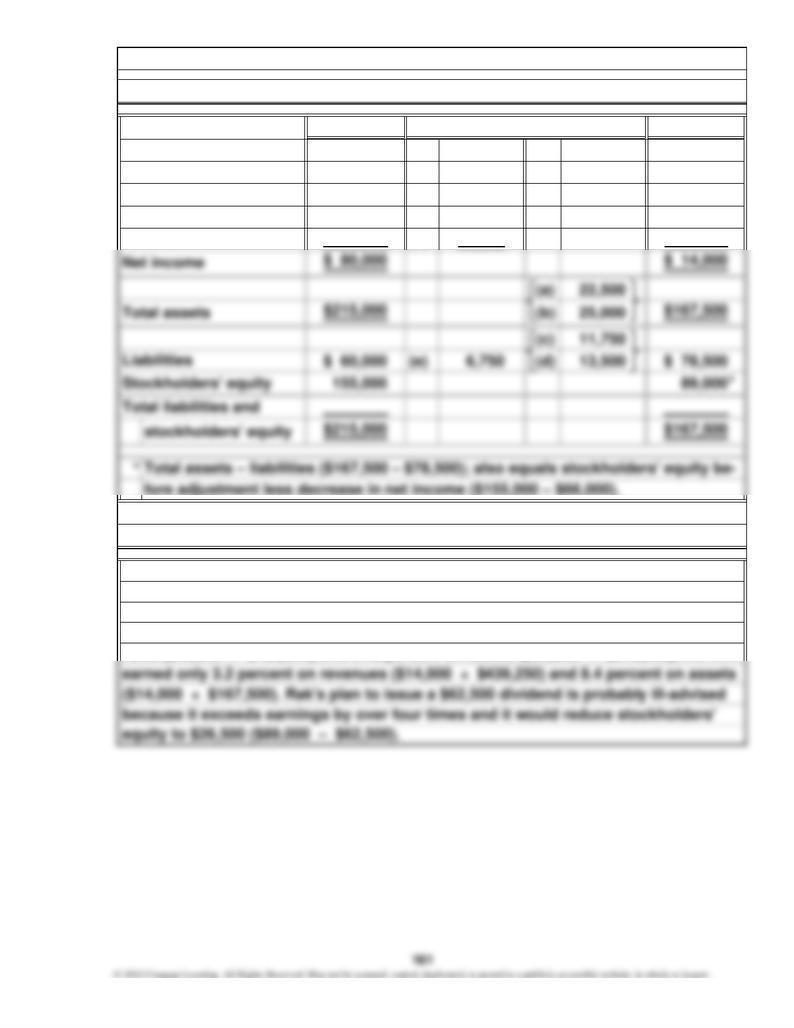

2. Financial statement amounts recast

3. Results discussed

nues ($80,000 ÷ $432,500) and 37.2 percent on assets ($80,000 ÷ $215,000), the firm

Expenses

equity is only $89,000 ($155,000 – $66,000). Instead of earning 18.5 percent on reve-

The performance of the company is much less favorable than Rak's original figures

suggest. As a result of the adjustments, net income is $66,000 ($80,000 – $14,000)

less than Rak's initial determination. The lower net income means that stockholders'

Chapter 3, C 8. (Continued)

Adjustments

Revenues

162