3. a 6.

(+) ÷2

c

Chapter 12, SE 1.

=

=

CHAPTER 12—Solutions

The Statement of Cash Flows

Chapter 12, SE 2.

=

Free Cash Flow

= 2.0 Times

$275,000

Net Cash Flows from Operating Activities – Dividends –

$250,000

34.3%

$45,000

=

Purchases of Plant Assets + Sales of Plant Assets

() ÷2

– + $30,000

Chapter 12, SE 3.

$1,185,000

=

$180,000$270,000

$825,000 +

–

$60,000

=

=Free Cash Flow Net Cash Flows from Operating Activities – Dividends –

Purchases of Plant Assets + Sales of Plant Assets

$750,000

=

= $60,000

34.3%

= 22.8%

573

$66,000

$28,000

( 22,000)

10,000 16,000

$82,000

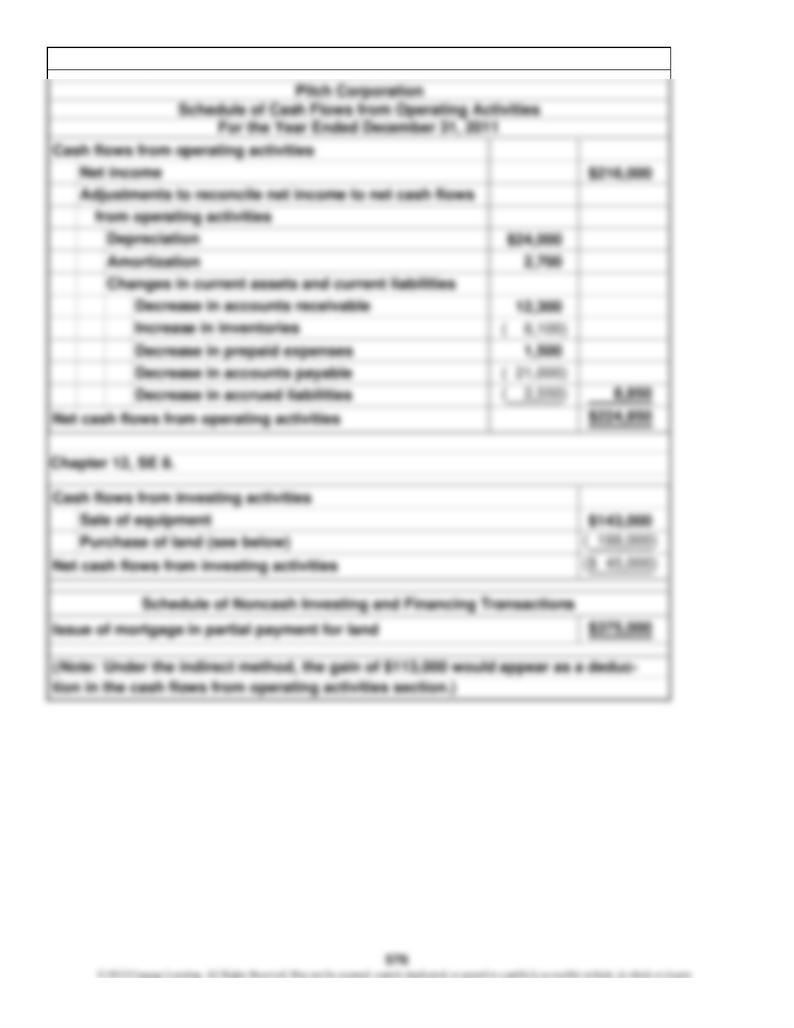

Changes in current assets and current liabilities

flows from operating activities

Increase in accounts receivable

Net cash flows from operating activities

Increase in accounts payable

Depreciation

Adjustments to reconcile net income to net cash

to improving all three efficiency ratios is better management of inventory, ac-

Cash flows from operating activities

Net income

erations. Free cash flow is positive, which indicates that the company was able

For the Year Ended December 31, 2011

Chapter 12, SE 5.

Chapter 12, SE 4.

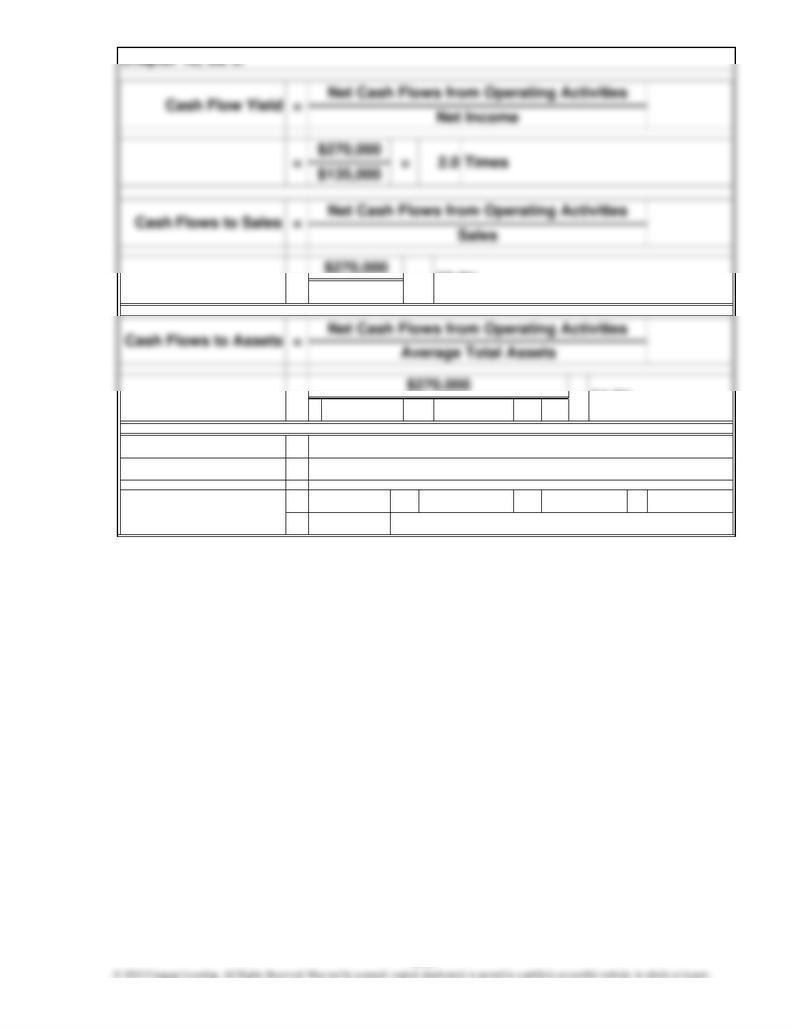

$50,000 decrease in accounts payable. The cash flows to assets is slightly larger

than cash flows to sales because the asset turnover is slightly more than 1. Be-

Titan Corporation experienced this unfavorable yield primarily because of a

are only 70 percent of earnings. A yield of less than 1 signals potential problems.

did reduce liabilities by approximately 25 percent. Overall, the company improved

The cash flow yield is 0.7 times, which indicates that cash flows from operations

preciable assets, as indicated by a decline in the gross amount of equipment, it

to finance its net expenditures for land and equipment from its cash flows from

operations after paying dividends. Although the company did not replace its de-

counts payable, and accounts receivable, all of which affect cash flows from op-

its liquidity and its ability to borrow for possible future expansion.

Schedule of Cash Flows from Operating Activities

Express Corporation

cause cash flow yield is less than 1, we know that profit margin and return on

assets are higher than the cash flows to sales and cash flows to assets. The key

574

$144,000

$16,000

1,800

8,200

( 5,400)

1,000

( 14,000)

( 1,700) 5,900

$149,900

Increase in inventories

Decrease in prepaid expenses

Decrease in accrued liabilities

Net cash flows from operating activities

Decrease in accounts payable

Adjustments to reconcile net income to net cash flows

from operating activities

Schedule of Cash Flows from Operating Activities

For the Year Ended December 31, 2011

Cash flows from operating activities

Net income

Minh Corporation

Chapter 12, SE 6.

Depreciation

Amortization

Changes in current assets and current liabilities

Decrease in accounts receivable

575

Chapter 12, SE 7.

Chapter 12, SE 9.

4. 8.

a

b

Chapter 12, SE 11.

1.

2.

3.

1.

3.

5. b and a 10. d

c

and return on assets, respectively, because a cash flow yield of less than 1.0

from the comparative balance sheets. What is important from the statement of

Chapter 12, E 1.

579

) ÷ 2

=

=–+

=

=$525,000$600,000

+

=

=

$825,000

17.4%

=

11.9%

(

1.4 Times

$70,000

$98,000 $125,000 $23,000

($34,000)

Free Cash Flow

$30,000–

Net Cash Flows from Operating Activities – Dividends –

Purchases of Plant Assets + Sales of Plant Assets

580

$1,200,000

$820,000

( 700,000)

180,000

( 80,000)

( 900) 11,700

$93,700

Net cash flows from operating activities

Cash flows from operating activities

Net income

Adjustments to reconcile net income to net cash

Depreciation

Changes in current assets and current liabilities

Increase in accounts receivable

flows from operating activities

Decrease in inventory

Increase in prepaid expenses

Chapter 12, E 5.

Schedule of Cash Flows from Operating Activities

For the Year Ended December 31, 2011

Decrease in accrued liabilities

Sunderland Chemical Company

581

$14,800

$ 4,000

( 8,800)

( 14,000)

2,800

28,000

2,000

( 1,200) 12,800

$27,600

($116,000)

65,000

a.

b.

$78,000

13,000

$65,000

Increase in accounts receivable

(b)

(a)

Changes in current assets and current liabilities

Cash flows from operating activities

For the Year Ended June 30, 2011

Decrease in prepaid rent

Decrease in income taxes payable

Depreciation

Net cash flows from operating activities

Chapter 12, E 7.

Schedule of Cash Flows from Operating Activities

Freed Corporation

Net income

Adjustments to reconcile net income to net cash flows

from operating activities

Increase in inventories

Increase in salaries payable

Increase in accounts payable

Book value of investment sold

Chapter 12, E 8.

of cash.

T account shows $78,000 of investments sold. There was a $13,000 loss on the

T account shows purchases of investments to be $116,000, which is an outflow

Less loss on sale

Net cash inflow from sale

sale. The net cash flow from the sale is computed as follows:

Purchase of investments

Cash flows from investing activities

Sale of investments

582

Chapter 12, E 9.

( 600) 27,100

$45,000

11,700

($20,000)

25,000

( 4,300) 700

Chapter 12, E 11.

Net cash flows from operating activities

Decrease in income taxes payable

Sale of furniture*

Cash flows from investing activities

Cash flows from financing activities

Repayment of notes payable

Issue of common stock

Payment of dividends

Net cash flows from financing activities

585

1.

2.

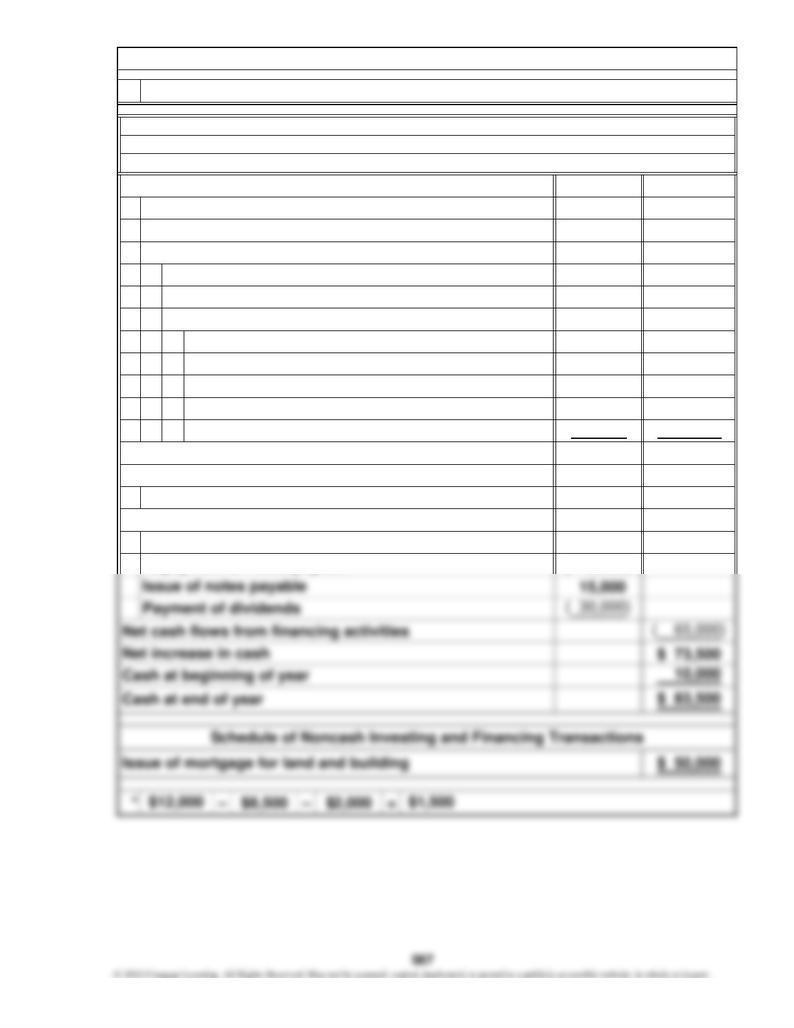

2010: ($ 71,446) – $39,640 – $60,890 =

2011: $364,300 – $45,400 – $31,200 =

3.

4.

Chapter 12, P 2.

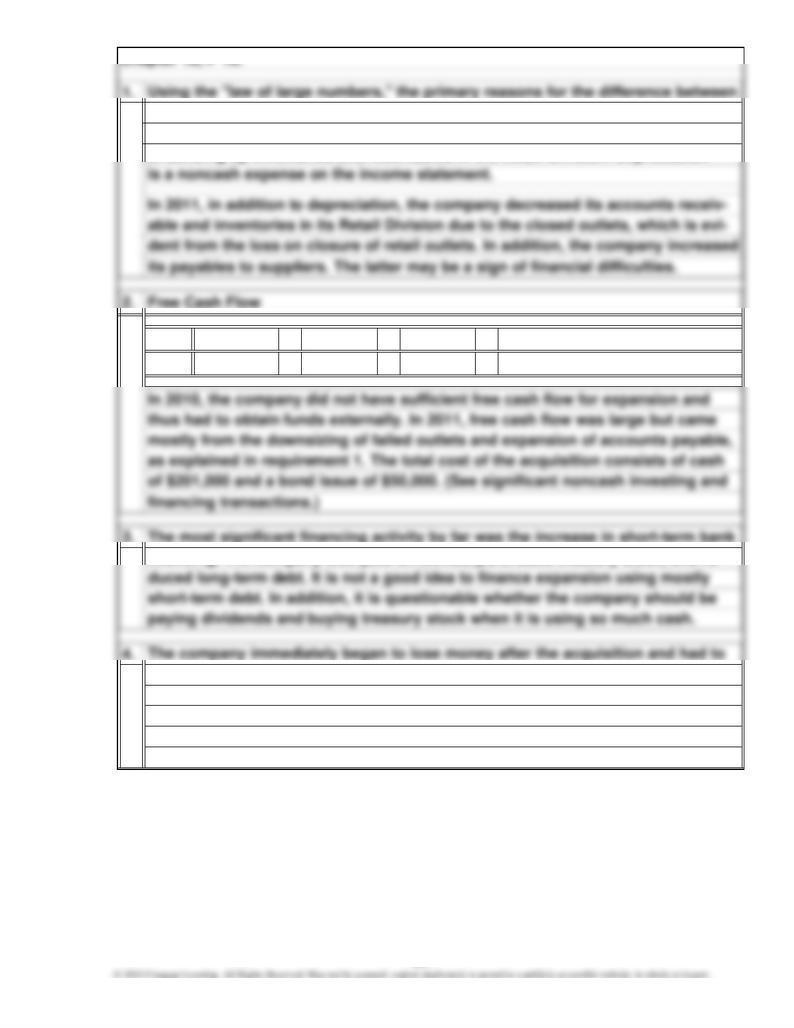

net income and cash flows from operating activities in 2010 are depreciation

and increases in inventory and accounts receivable. The last two are the result

close outlets to reduce inventory and receivables to raise cash to pay off the

financing. The company also paid dividends, purchased treasury stock, and re-

of building up inventories and receivables in the Retail Division. Depreciation

($171,976)

$287,700

short-term bank notes. The entire strategy of diversification was not well thought

$ 59,800

$30,000

2,000

10,000

20,000

200

11,000

4,000 77,200

$137,000

1,500

($10,000)

( 40,000)

from operating activities

Cash flows from operating activities

Net income

Adjustments to reconcile net income to net cash flows

Repayment of notes payable

Depreciation

Loss on sale of equipment

Changes in current assets and current liabilities

Increase in accounts payable

Net cash flows from operating activities

Cash flows from investing activities

Sale of equipment*

Cash flows from financing activities

Repayment of mortgage

Decrease in accounts receivable

Decrease in inventory

Decrease in prepaid expenses

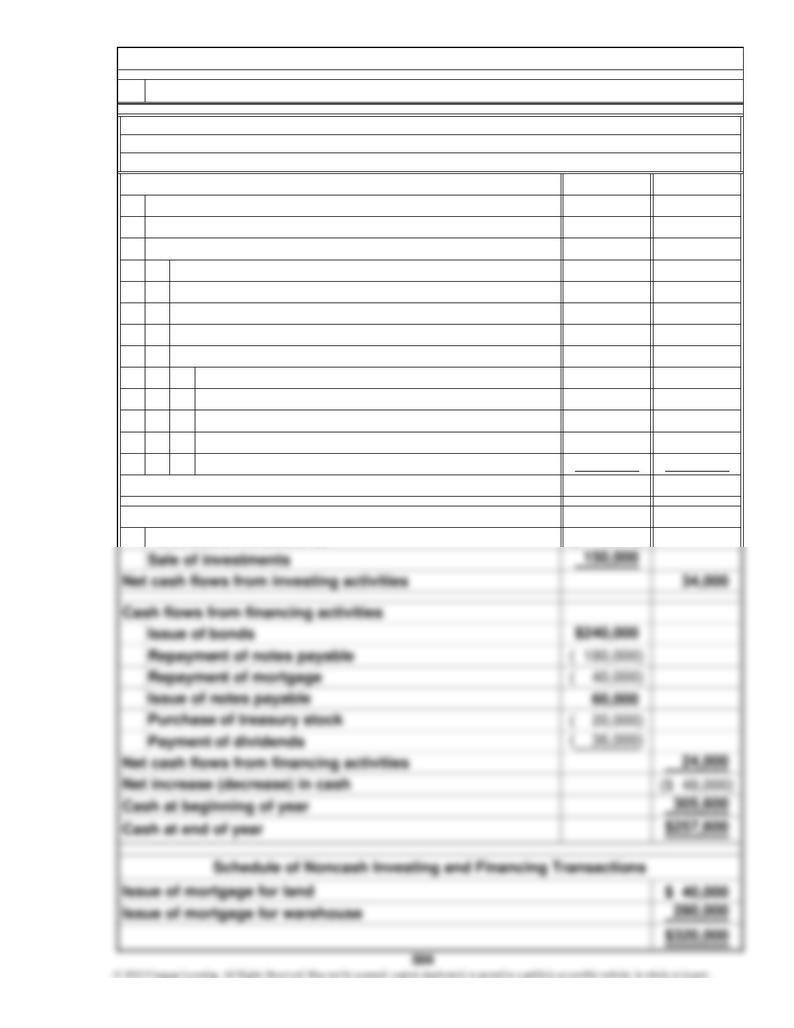

1.

Chapter 12, P 3.

Statement of cash flows prepared

Bronek Corporation

For the Year Ended June 30, 2011

Statement of Cash Flows

Increase in income taxes payable

Chapter 12, P 3. (Continued)

$59,800

=

3. User Insight: Computation and assessment of cash flow yield and free cash flow

= 2.3

Times

Free Cash Flow

Chapter 12, P 3. (Continued)

Net Cash Flows from Operating Activities – Dividends –

Purchases of Plant Assets + Sales of Plant Assets

=

$ 11,000

$ 46,800

( 7,000)

34,800

100,000

1,000

( 57,000)

( 3,000) 115,600

$126,600

$ 13,800

Cash flows from investing activities

1. Statement of cash flows prepared

Depreciation

Gain on sale of furniture and fixtures

Changes in current assets and current liabilities

Decrease in merchandise inventory

Decrease in prepaid rent

Net cash flows from operating activities

Decrease in accounts receivable

Decrease in accounts payable

Decrease in income taxes payable

Cash flows from operating activities

Net income

Adjustments to reconcile net income to net cash flows

from operating activities

Sale of furniture and fixtures*

Brick Corporation

Chapter 12, P 4.

Statement of Cash Flows

For the Year Ended December 31, 2011

$11,000

=

Chapter 12, P 4. (Continued)

Free Cash Flow

Times

3. User Insight: Computation and assessment of cash flow yield and free cash flow

11.5

2011

Net Cash Flows from Operating Activities – Dividends –

==

Purchases of Plant Assets + Sales of Plant Assets

$24,000

$20,000

15,000

5,000

( 8,500)

5,000

( 40,000)

3,000

( 47,500)

( 2,500) ( 50,500)

($26,500)

($29,000)

37,500 8,500

Cash flows from operating activities

Carmelita Vases, Inc.

Chapter 12, P 5.

Statement of Cash Flows

1. Statement of cash flows prepared

Decrease in accounts payable

Decrease in accrued liabilities

Purchase of investments

Depreciation—building

Decrease in accounts receivable

Net income

Adjustments to reconcile net income to net cash flows

Depreciation—equipment

Amortization—intangibles

from operating activities

Increase in inventory

Gain on sale of investments

Changes in current assets and current liabilities

For the Year Ended December 31, 2011

Cash flows from investing activities

Sale of investments

Decrease in prepaid expenses

Net cash flows from operating activities

($26,500)

$24,000

=

=($26,500) – – $0 +

=

Net Income

= not meaningful

3.

Purchases of Plant Assets + Sales of Plant Assets

Net Cash Flows from Operating Activities – Dividends –

$0

Net Cash Flows from Operating Activities

and issued bonds. Overall, the situation warrants investigation. Why did inventory

and pay accounts payable. Further, this contributed to the company's negative free

divided into negative cash flow. The major uses of cash were to increase inventory

negative. The cash flow yield was not meaningful because a positive net income is

grow so rapidly? Are the company's suppliers requiring faster payment? The focus

Despite a net income in 2011, Carmelita Vase's cash flows from operations were

cash flow of $35,500. To bolster its cash balance, the company sold investments

$9,000

($35,500)

=

Chapter 12, P 5. (Continued)

Cash Flow Yield =

Free Cash Flow

594

$ 28,000

$15,000

3,000

3,000

( 5,300)

( 27,000)

25,000

20,000

( 26,000)

( 12,300) ( 4,600)

$ 23,400

($12,500)

6,300

Cash flows from operating activities

Net income

Zagloba Materials, Inc.

Chapter 12, P 7.

Statement of Cash Flows

For the Year Ended December 31, 2011

Depreciation—building

Gain on sale of equipment

Changes in current assets and current liabilities

Increase in accounts receivable

Decrease in inventory

Sale of equipment*

Decrease in accounts payable

Decrease in accrued liabilities

1. Statement of cash flows prepared

Adjustments to reconcile net income to net cash flows

from operating activities

Purchase of equipment

Amortization—patent

Depreciation—equipment

Decrease in prepaid expenses

Net cash flows from operating activities

Cash flows from investing activities

$28,000

=

= $23,400 – – $12,500 + $6,300

=

$9,000

$8,200

Purchases of Plant Assets + Sales of Plant Assets

==

3. User Insight: Computation and assessment of cash flow yield and free cash flow

0.8 Times

Net Cash Flows from Operating Activities – Dividends –

Chapter 12, P 7. (Continued)

Free Cash Flow

$ 56,000

$ 30,000

6,000

6,000

( 10,600)

( 54,000)

50,000

40,000

( 52,000)

( 24,600) ( 9,200)

$ 46,800

($ 25,000)

12,600

Cash flows from investing activities

Purchase of equipment

Sale of equipment*

Cash flows from operating activities

Depreciation—building

Net cash flows from operating activities

Decrease in inventory

Amortization—patent

Depreciation—equipment

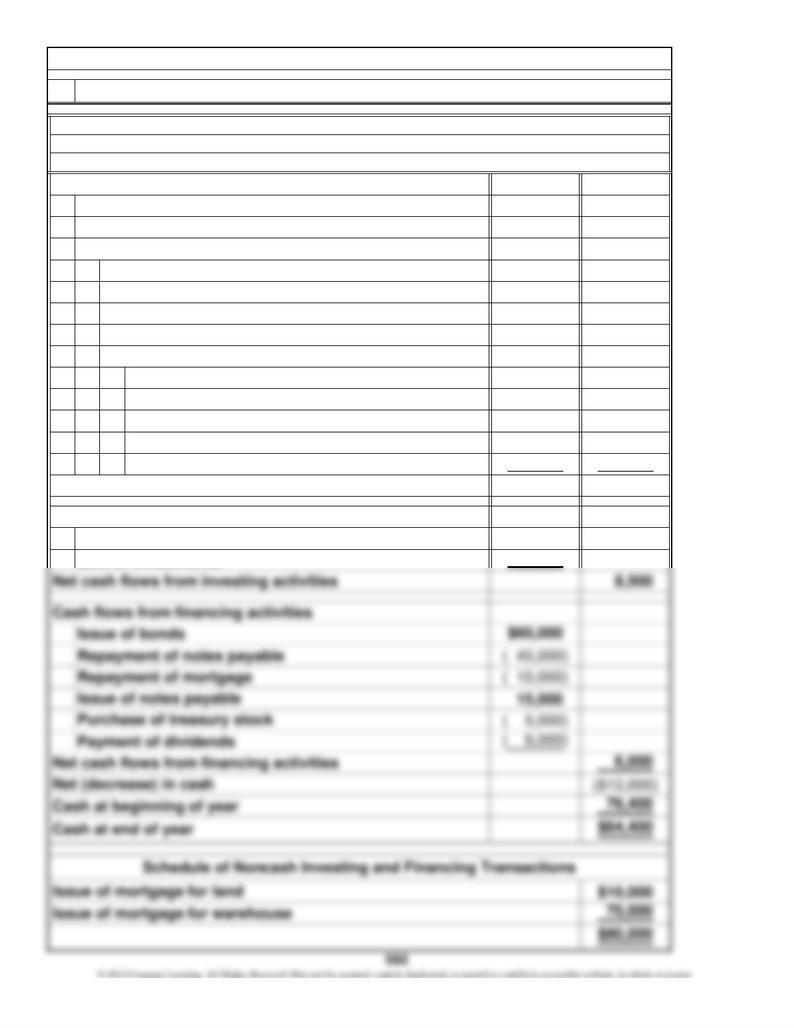

Sharma Fabrics, Inc.

Chapter 12, P 8.

1. Statement of cash flows prepared

For the Year Ended December 31, 2011

Decrease in accounts payable

Decrease in accrued liabilities

Net income

Adjustments to reconcile net income to net cash flows

from operating activities

Gain on sale of equipment

Changes in current assets and current liabilities

Increase in accounts receivable

Decrease in prepaid expenses

Statement of Cash Flows

$56,000

=

= $46,800 – – $25,000 + $12,600

Chapter 12, P 8. (Continued)

Free Cash Flow

Times=

3. User Insight: Computation and assessment of cash flow yield and free cash flow

Net Cash Flows from Operating Activities – Dividends –

$18,000

Purchases of Plant Assets + Sales of Plant Assets

0.8

=

$ 96,000

$ 80,000

60,000

20,000

( 34,000)

20,000

( 160,000)

12,000

( 190,000)

( 10,000) ( 202,000)

($106,000)

($116,000)

Net cash flows from operating activities

Decrease in prepaid expenses

Net income

Adjustments to reconcile net income to net cash flows

Depreciation—building

Gain on sale of investments

Depreciation—equipment

Amortization—intangibles

Cash flows from investing activities

Purchase of investments

1. Statement of cash flows prepared

from operating activities

Cash flows from operating activities

Changes in current assets and current liabilities

Decrease in accounts receivable

Increase in inventory

Decrease in accounts payable

Decrease in accrued liabilities

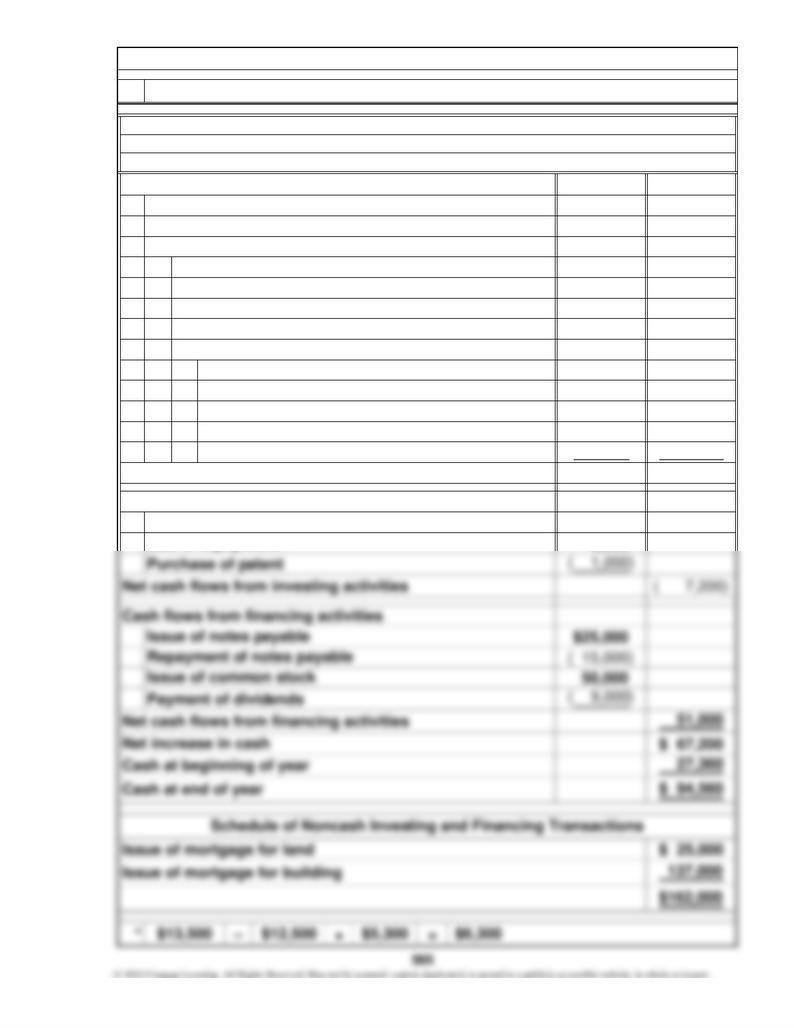

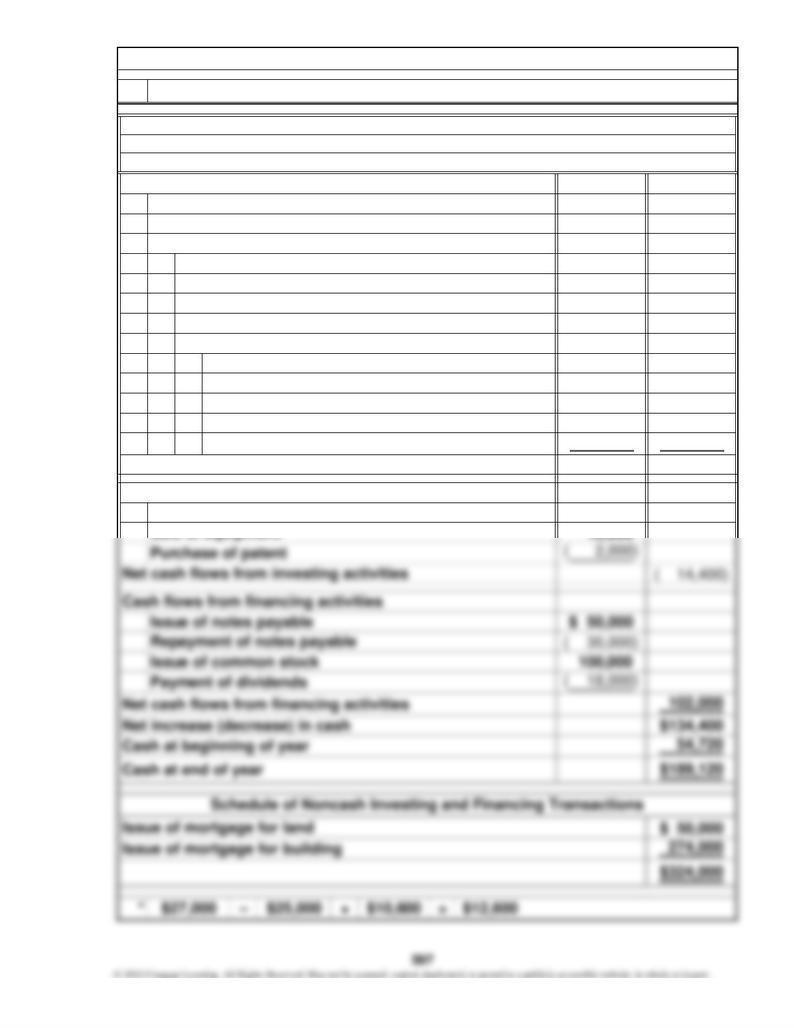

Karidis Ceramics, Inc.

Chapter 12, P 9.

Statement of Cash Flows

For the Year Ended December 31, 2012

($106,000)

$96,000

=

=($106,000) – – $0 + $0

=

Chapter 12, P 9. (Continued)

3.

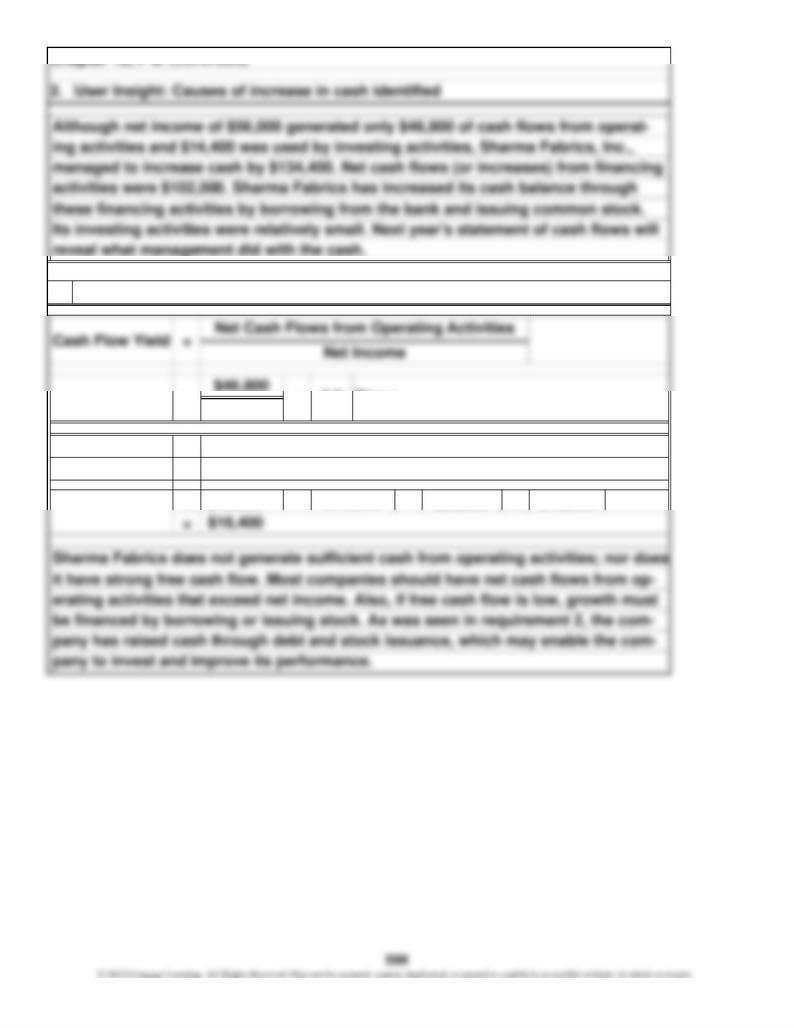

User Insight: Computation and assessment of cash flow yield and free cash flow

not meaningful

Cash Flow Yield

and issued bonds. Overall, the situation warrants investigation. Why did inventory

and pay accounts payable. Further, this contributed to the company's negative free

divided into negative cash flow. The major uses of cash were to increase inventory

=

grow so rapidly? Are the company's suppliers requiring faster payment? The focus

Despite a net income in 2012, Karidis Ceramics' cash flows from operations were

cash flow of $142,000. To bolster its cash balance, the company sold investments

Net Cash Flows from Operating Activities – Dividends –

$36,000

($142,000)

negative. The cash flow yield was not meaningful because a positive net income is

Net Cash Flows from Operating Activities

Net Income

Purchases of Plant Assets + Sales of Plant Assets

==

Free Cash Flow

1.

2.

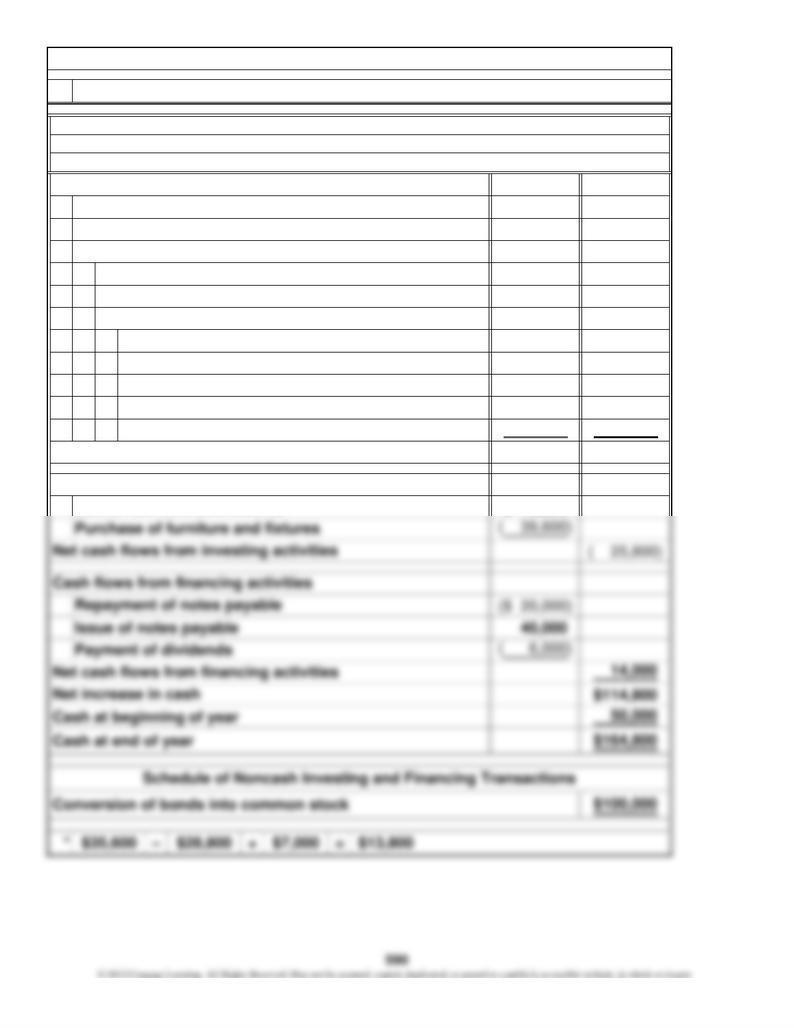

2010: ($ 38,472) – $19,973 – $33,112 =

2011: $184,227 – $22,924 – $16,145 =

3.

4.

net income and cash flows from operating activities in 2010 are depreciation

and increases in inventory and accounts receivable. The last two are the result

of building up inventories and receivables in the Retail Division. Depreciation

short-term bank notes. The entire strategy of diversification was not well thought

out. The company's regular sales probably declined due to its traditional cus-

tomers resenting the competition from one of their suppliers. The company had

no experience running a retail business.

close outlets to reduce inventory and receivables to raise cash to pay off the

$145,158

Chapter 12, P 10.

financing. The company also paid dividends, purchased treasury stock, and re-

($ 91,557)

601

EBITDA (earnings before interest, taxes, depreciation, and amortization) is often

used in the financial press as a shortcut for cash flows from operating activities on

Chapter 12, C 1.

=

($753)

0.2%

1.

Chapter 12, C 2.

Make required computations and label the document "Attachment"

2000 =

Net Cash Flows from Operating Activities – Dividends –

Purchases of Plant Assets + Sales of Plant Assets

Free Cash Flow

$64,926

2001.

cash flows. Enron's statement of cash flows and the computation on which this

Re:

At your request, I have prepared an analysis of Enron Corporation's statement of

Today's Date

Investment Analyst

StudentFrom:

ferent story.

negative cash flows in 2001 were the net margin deposit activity (in connection

Chapter 12, C 2. (Continued)

In fact, the net income, or "bottom line," decreased from $797 million in 2000 to $225

million in 2001 (nine-month period). Also, the statement of cash flows tells a very dif-

Memorandum

Date:

To:

Mr. Lay, Chairman of Enron, referred to a 26 percent increase in recurring earnings.

Assessment of Enron's Statements of Cash Flows

analysis is based are presented in attachments.

First, net cash provided by operating activities was only $127 million in 2000 and

declined to a negative $753 million in 2001. The largest items accounting for the

with derivatives trading—$2,349 million) and the decline in payables ($1,764 mil-

2. Prepare a memorandum to the investment analyst

604

2009: 407 – 43 – 496 + 153 = 21 117 – 83 – 522 + 40 =

2008: 758 – 25 – 475 + 145 = 403 466 – 69 – 419 + 151 =

Chapter 12, C 3.

129

(448)

$120,000

$20,000

( 32,000)

( 60,000)

Increase in accounts receivable

Statement of Cash Flows

For the Year Ended December 31, 2011

Changes in current assets and current liabilities

Adjustments to reconcile net income to net cash

Net income

Chapter 12, C 4.

1. Statement of cash flows prepared

Increase in inventory

Roll Print Gallery, Inc.

Cash flows from operating activities

flows from operating activities

Depreciation

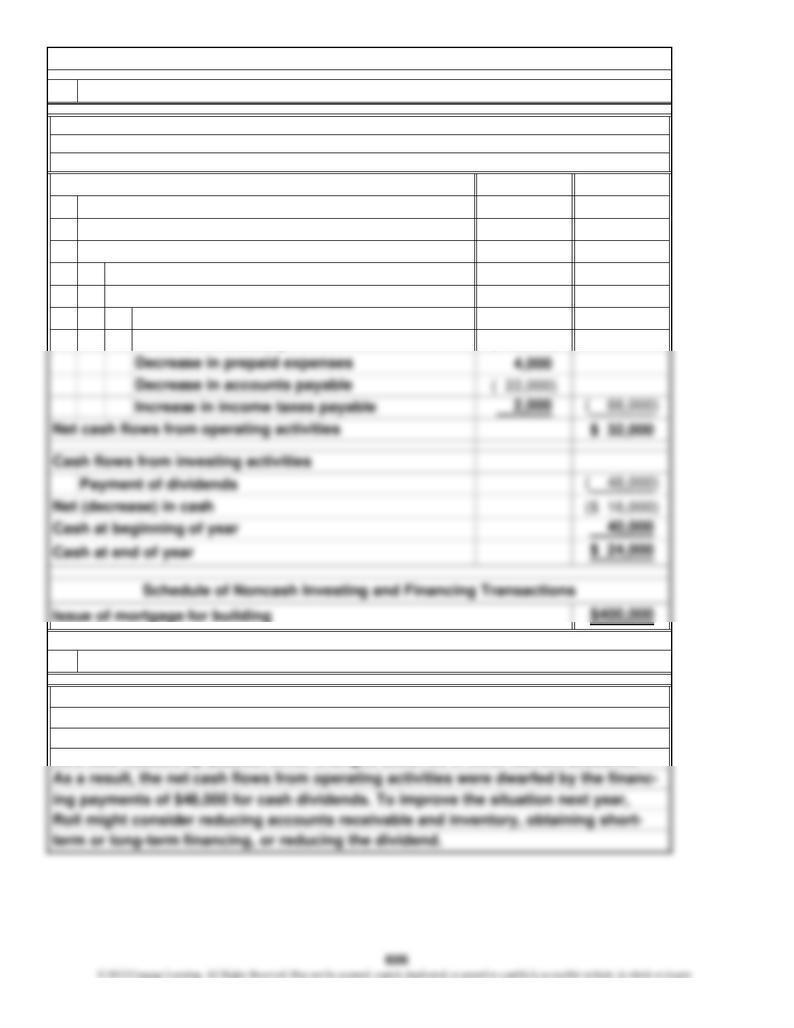

2. Cash problem explained

Although Roll earned $120,000 and had $20,000 of depreciation during the year,

operating activities generated only $32,000 in cash because of the large increases

in accounts receivable ($32,000) and inventory ($60,000). In addition, accounts pay-

able was reduced by $22,000. Minor changes occurred in other current accounts.

1.

2.

3.

Chapter 12, C 5.

bottom of the statement. This reconciliation uses the indirect method and should

be used to understand CVS's cash flows from operations. The most important

items affecting cash flows from operations other than net earnings are depreci-

ties. In order to understand the difference between net income and net cash pro-

vided by operating activities, it is necessary to look at the reconciliation at the

used in 2009.

billion in the last two years. The other large item was the repurchase of common

total. In addition, acquisitions and other investments totaled more than $2.7 bil-

totaled only $0.7 billion. Also, the increase in short-term debt totaled over $3.7

creased by a total of $4.1 billion from $0.9 billion provided in 2008 to $3.2 billion

stock of $2.5 billion in 2009. Overall, net cash used in financing activities in-

the company had additions to long-term debt of $3.2 billion, while reductions

pany has had additions to property and equipment that exceeded $4.7 billion in

607

( + ) ÷ 2

=

Chapter 12, C 6.

(dollars in millions)

CVS's cash flow yield:

$87,472

2008: =

6.6%

CVS's cash flows to assets:

4.5%

=

=

$3,947

=

– Purchases of Plant Assets + Sales of Plant Assets

=

CVS's free cash flow:

$61,301

Free Cash Flow

Net Cash Flows from Operating Activities – Dividends

$3,947

$57,841 6.8%

$60,960 $54,722

2008:

=

––+=

––+=

$923

Net Cash Flows from Operating Activities – Dividends

2008: ($2,457)

$387

$13

2009: $985 $13 $585

$0($1,521)

=

$0

Free Cash Flow

– Purchases of Plant Assets + Sales of Plant Assets

= -9.9%

7.0%

$15,420

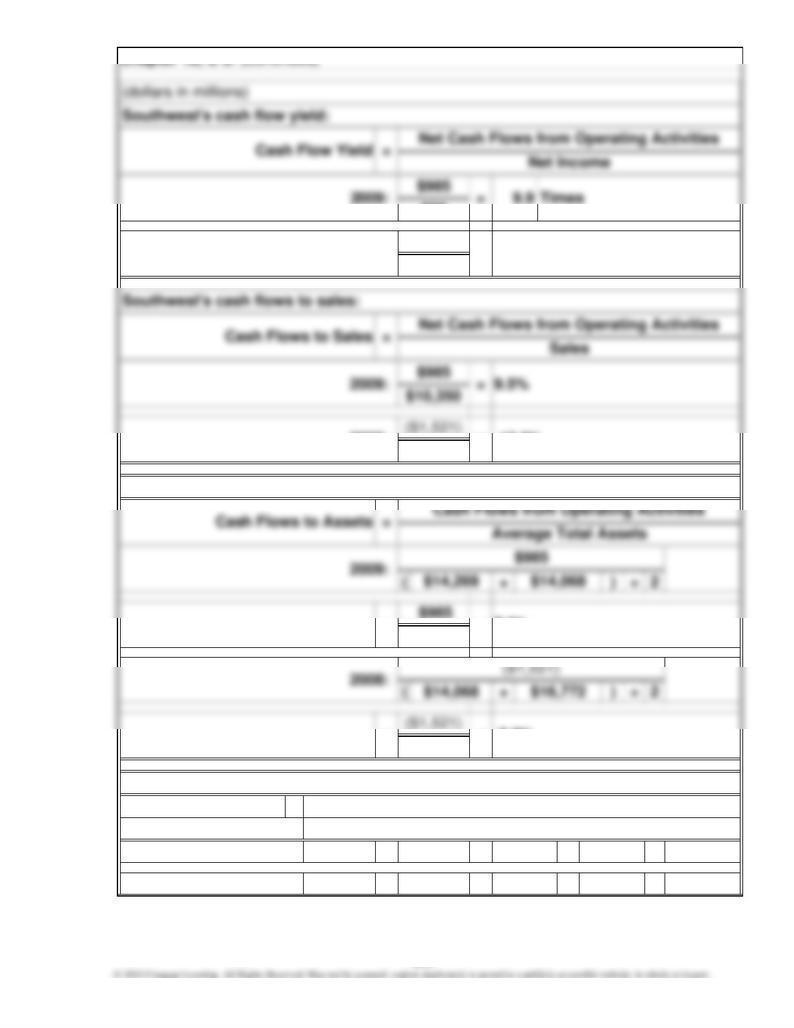

Southwest's free cash flow:

not meaningful

Southwest's cash flows to assets:

=

$11,023

2008: =

($1,521)

$178

$99 9.9 Times

Chapter 12, C 6. (Continued)

2008:

-13.8%

=

= $14,169

609

Chapter 12, C 6. (Continued)

flows.

the note is for only two years and is "close" to being a current liability. Allowances

years in relation to asset growth. The company will need to continue borrowing to

times in 2009, but the cash flow yield for 2008 is not meaningful due to negative

CVS's cash flow yield exceeds 1.0 times but is not sufficient to generate high cash

flows to sales or to assets. In addition, free cash flow was relatively low in both

high depreciation. Therefore, for 2009, Southwest has higher cash flows to sales

finance expansion. Southwest, on the other hand, had a high cash flow yield of 9.9

cash flow from operating activities, partly caused by low net income in relation to

and to assets than CVS does. These ratios are not meaningful and/or negative for

Southwest's 2008 operations. CVS had greater free cash flows in both years. Both

companies have decreased their cash balances during the year. Due to the nega-

tive ratios for Southwest in 2008, overall, it appears that CVS has stronger cash

for judgment would permit the reclassification. Also, the 3.0 ratio requirement is

Students will disagree on this case. Some will think the president's order is tanta-

mount to lying. Others will see it as the practical thing to do, especially given that

Chapter 12, C 7.

quite arbitrary. Why risk a serious situation over such a small thing? Most will argue