3. 6.

3. 6.

28,000 28,000

28,000 28,000

$40,000

24,000

$64,000

($64,000)

($24,000)

24,000

16,000

( 64,000)

Payment of dividends

6/1

6/15

Cash

Common Stock

Additional Paid-In Capital

Retained Earnings

Start-up and organization costs

Balance Sheet Effect:

Start-up and organization costs:

Legal services, 24,000 shares of $1 par value common stock

Incorporation fees

Total start-up and organization costs

Income Statement Effect:

Chapter 11, SE 4.

Dividends

Declaration of dividends: 140,000 shares

outstanding × $0.20 per share

b

Dividends Payable

5/15 Dividends Payable

No entry necessary on record date

Cash

CHAPTER 11—Solutions

STOCKHOLDERS’ EQUITY

Chapter 11, SE 1.

Chapter 11, SE 3.

a

518

Chapter 11, SE 5.

Fina Corporation

Balance Sheet

December 31, 2011

Stockholders’ Equity

Contributed capital

1. 30,000 12,500

2. 30,000 2,500

1. 112,000 16,000

96,000

2. 100,000 16,000

84,000

Common Stock

Additional Paid-In Capital

Common Stock

Common Stock

Chapter 11, SE 7.

Common Stock

Additional Paid-In Capital

Issued 16,000 shares of $1 par value common

stock for land; market value of land used to

value transaction

520

Oct. 1 40,000 40,000

(×

17 12,500 10,000

2,500

(×

( × $20

Oct. 28 3,000

4,500

Chapter 11, SE 9.

Cash

Treasury Stock, Common

$20

Cash

Paid-In Capital, Treasury Stock

per share); $25500$12,500

cost was

2,000 per share )

Sold 500 shares of treasury stock for

Treasury Stock, Common

Common Stock

Additional Paid-In Capital

Acquired 2,000 shares of company’s common

stock for $40,000

$10,000 500

per share)

Chapter 11, SE 10.

× 224,400 =

Common stock, $3 par value, 400,000 shares authorized,

375,000 shares issued and outstanding

Contributed capital

Chapter 11, SE 12.

August 10, 2011

$1,125,000

3,000,000

Additional paid-in capital

Stockholders’ Equity

Chapter 11, SE 11.

After Stock Split Pearl International

$0.50

shares

4. $48 per share (

4.

* ( × $100 ) =

×

=

Chapter 11, SE 15.

Chapter 11, SE 13.

per share

80,000

0.08

$8,000

shares1,000

=

$29.58

*

1.

2.

3.

4.

1.

2.

3.

4.

sense that an outside investor does. For instance, no dividends are paid on

treasury stock because the company would be paying itself. By buying and

holding its own stock, the company is in effect reducing its stockholders’

been issued and then reacquired. The company does not own the stock in the

record, the seller will not receive the dividend because the date of record is the

date at which ownership of the stock of a company and the right to receive a

Chapter 11, E 1.

$66.00

$4.40

6/5 17,500 17,500

6/15

6/25 17,500 17,500

10/15 90,000 90,000

11/1

11/15 90,000 90,000

Dividends

Payment of dividends

Cash

Declaration of dividends

Dividends Payable

Dividends Payable

Cash

Payment of dividends

Chapter 11, E 5.

180,000 shares outstanding × $0.50 per share

Record date: No entry necessary

Chapter 11, E 3.

Chapter 11, E 4.

Dividends

Dividends Payable

Declaration of dividends

70,000 shares outstanding × $0.25 per share

Record date: No entry necessary

Dividends Payable

525

3. 6. 9.

Chapter 11, E 6.

$400,000

450,000

$850,000

—

$850,000

authorized, 30,000 shares issued and

Total contributed capital

2. Stockholders’ equity section of the balance sheet prepared

300,000

Cash Preferred Stock

$150,000outstanding

Rich Supply Corporation

Stockholders’ Equity

Additional paid-in capital

Retained earnings

Preferred stock, $100 par value, 6 percent

Contributed capital

March 1, 2011

Balance Sheet

1.

Chapter 11, E 8.

Transactions recorded in T accounts

4,000 shares issued and outstanding

Common stock, $5 stated value, 100,000 shares

Total stockholders’ equity

noncumulative, 20,000 shares authorized,

527

Total

Per Per Dividends

Amount Share Amount Share Allocated

Dividends

Chapter 11, E 9.

Preferred Stock Common Stock

Dividends

1. $40,000 —$40,000

(× $35,000

(– $ 5,000 $40,000

$30,000 —$30,000

( $35,000 – $ 5,000

Chapter 11, E 10.

2011 dividends

$500,000

$40,000

)

$35,000

0.07

2010 dividends

2011

)

)

2010 dividends in arrears

$30,000

1 125,000 50,000

1 125,000 5,000

120,000

Chapter 11, E 11.

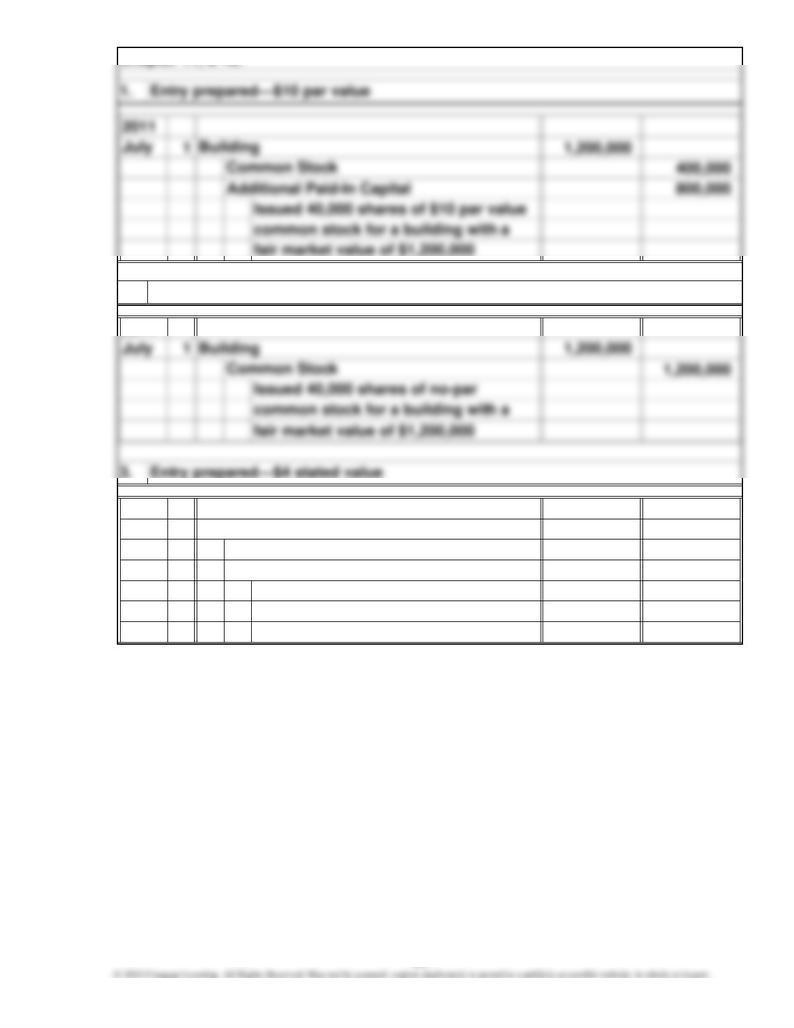

Common Stock

Aug.

2. Entry prepared—$10 par value

Cash

Additional Paid-In Capital

Issued 5,000 shares of $1 stated value

common stock for $25 per share

Aug. Cash

3.

4. Entry prepared—$1 stated value

530

1 1,200,000 160,000

1,040,000

2011

2011

with a fair market value of $1,200,000

Additional Paid-In Capital

Issued 40,000 shares of $4 stated

value common stock for a building

Common Stock

July

3.

2. Entry prepared—no par value

Building

Chapter 11, E 12.

531

May 17 2 May 5 1May 5 128,000 May 17 48,000 3

21 5 21 32,000

28 628 48,000 7

Bal. —

May 28 2,400 8 May 17 4,800 4

Bal. 2,400

1=

2=

3=

4=

5=

6=

7=

8=

$40

($38 – $40)

$40

$44

$40

($44 – $40)

1,200

3,200

$32,000

$45,600

800

shares ×

shares ×

$128,000

shares × $48,000

shares ×

1,200

$2,400

52,800

32,000

45,600

128,000

Chapter 11, E 13.

Cash Treasury Stock, Common

1,200

1,200 shares ×

1,200

1,200 $52,800

$48,000

$40

$38

shares ×

shares × $4,800

shares ×

Paid-In Capital, Treasury Stock

532

10 21

1 35,000 June 10 8,750 3

20 520 12,250 6

30 14,000 8

—

20 720 1,250 June 10 1,250 4

Bal. —

Chapter 11, E 14.

Treasury Stock, Common

Paid-In Capital, Treasury Stock

30 5,600 11

10,000

10,150

June

June Retained Earnings

850

35,000 June 1

Cash

Bal.

June

June

shares × = $33,000

$0.50

Chapter 11, E 15.

66,000

534

$100,000

10,000

$110,000

350,000

$460,000

$100,000

10,000

$110,000

350,000

$460,000

Contributed capital

Chapter 11, E 16.

May 15, 2011

Retained earnings

Additional paid-in capital

Total contributed capital

Retained earnings

No entry is required, but a memorandum entry for informational purposes should

be prepared.

Common stock, $1 par value, 250,000 shares authorized,

Contributed capital

Total stockholders’ equity

Common stock, $0.50 par value, 250,000 shares authorized,

100,000 shares issued and outstanding

200,000 shares issued and outstanding

Agat Company

Stockholders’ Equity

Total contributed capital

Before Stock Split

May 15, 2011

After Stock Split Agat Company

Additional paid-in capital

Stockholders’ Equity

Total stockholders’ equity

535

January 15, 2011

Mendoza International

Stockholders’ Equity

Chapter 11, E 17.

Contributed capital

Before Stock Split

Other

0.02 per share

( 400 × ) +

400 =

$44,400 per Share

Chapter 11, E 19.

$2,400

Preferred Stock

Book Value per Share =$105

$111=

400 Shares

*

Sept. 1 500,000 Sept. 1 32,000 Sept. 1 100,000

Oct. 2 960,000 Oct. 15 150,000 Oct. 2 320,000

1,460,000 182,000 Bal. 420,000

Bal. 1,278,000

Sept. 1 400,000 Nov. 30 48,000

1. T accounts set up and transactions recorded in the accounts

Additional Paid-In Capital

Common Stock

Cash

Dividends Payable

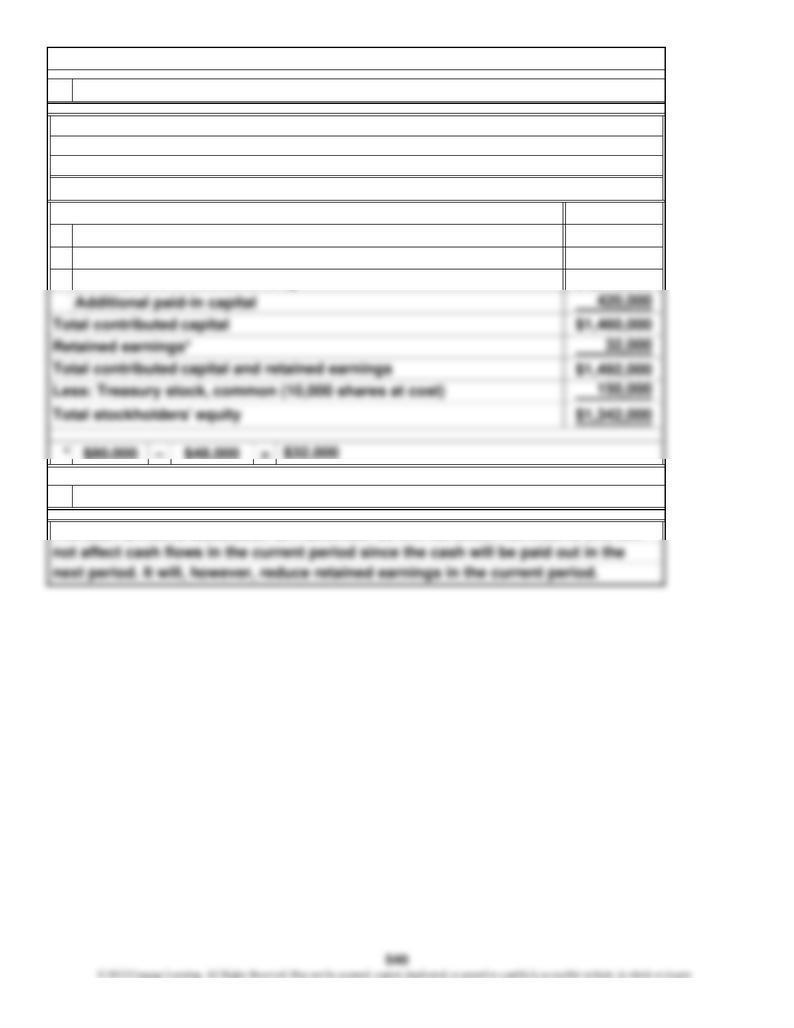

Chapter 11, P 1.

*

$1,040,000

Dewey Corporation

Contributed capital

Common stock, $8 par value, 300,000 shares

authorized, 130,000 shares issued and

120,000 shares outstanding

Balance Sheet

Stockholders’ Equity

November 30, 2011

Chapter 11, P 1. (Continued)

2. Stockholders’ equity section of the balance sheet prepared

The cash dividend declaration on November 30 will not affect net income and will

3. User Insight: Effects of cash dividend declaration discussed

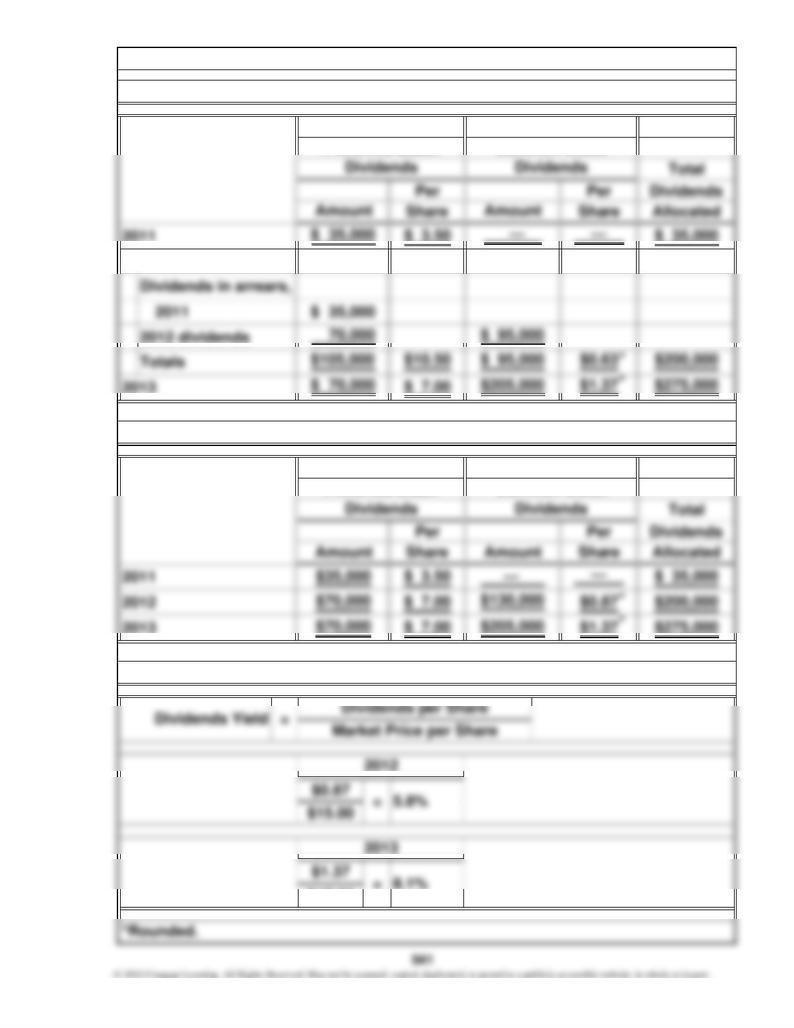

$ 3.50 —$ 35,000

$17.00

=

Common Stock

Noncumulative

Chapter 11, P 2.

Preferred Stock Total

2012

Common Stock

Preferred Stock

1. Dividends calculated for cumulative preferred stock and common stock

2. Dividends calculated for noncumulative preferred stock and common stock

3. The 2012 and 2013 dividends yield for common stock calculated

Cumulative

2011

Chapter 11, P 2. (Continued)

4. User Insight: Preferred stock compared to long-term bonds

Both cumulative and noncumulative preferred stock have a fixed level of dividends

bonds in the sense that if dividends are declared in any given year, past dividends

not paid must be made up. Likewise, any past interest missed on long-term bonds

would have to be made up. The difference is that with noncumulative preferred

and are thus similar in this way to long-term bonds, which have a fixed level of in-

terest. However, cumulative preferred stock would be more similar to long-term

Jan. 19 310 $ 15,000

$ 31,500 312 16,500

21 310 5,000

11,000 312 6,000

Feb. 7 310 30,000

78,000 312 48,000

Mar. 22 30,000 110 30,000

July 15 310 5,000

15,000 312 10,000

Aug. 1 350 7,500

Credited

Account

Number

Debited

Dollar

Amount Dollar

Amount

Account

Account

Number

110

Chapter 11, P 3.

1. Account numbers and dollar amounts provided

110

350

510

121

2. User Insight: Stockholders’ equity section of balance sheet discussed

The stockholders’ equity section of the balance sheet is an important factor in ana-

lyzing a company’s performance because it represents the ownership interest of

Chapter 11, P 3. (Continued)

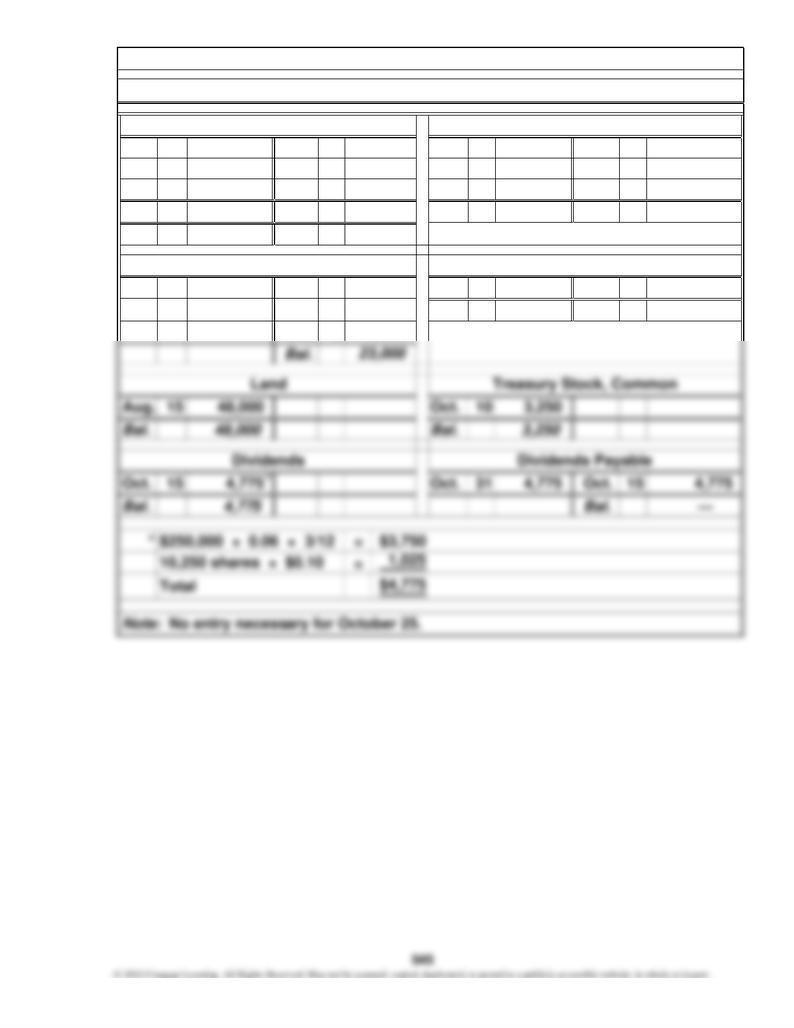

Aug. 3 110,000 Oct. 10 Aug. 3 100,000

22 250,000 31 15 40,000

Oct. 4 30,000 Oct. 4 25,000

390,000 Bal. 165,000

Bal. 381,975

Aug

.

3 Aug. 22 250,000

Bal. 250,000

Oct. 4

10,000 Preferred Stock

Cash 3,250

4,775

15

Additional Paid-In Capital

Common Stock

Chapter 11, P 4.

1. T accounts set up and transactions recorded in the accounts

5,000

8,000

8,025

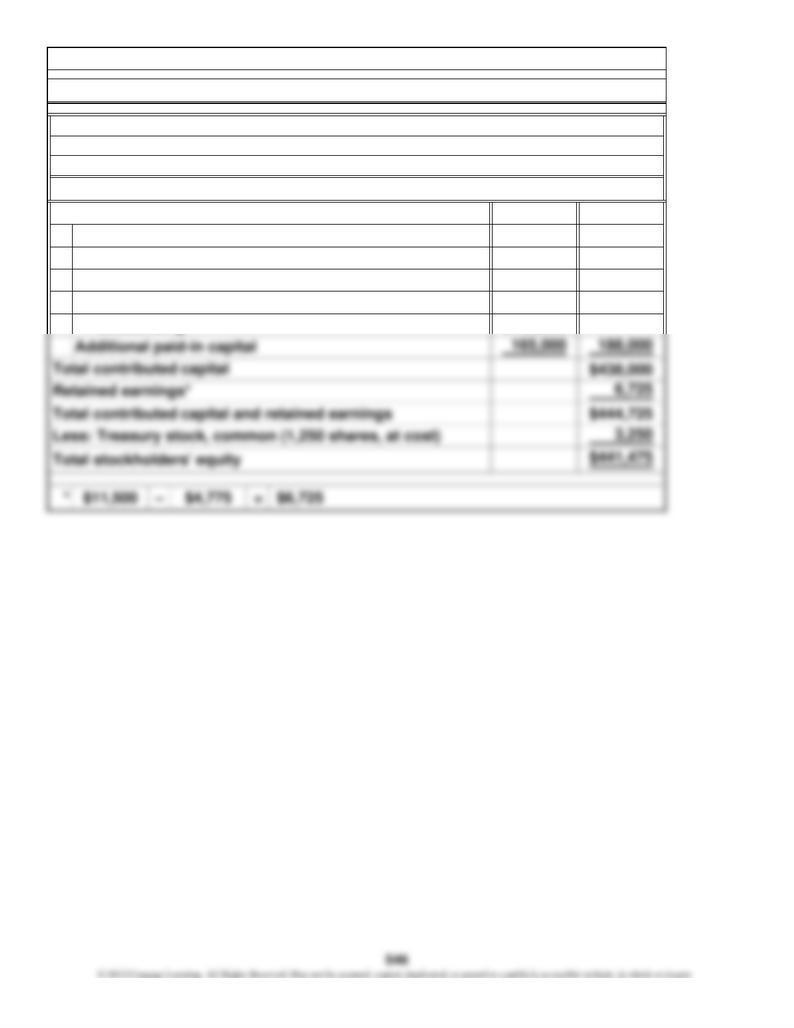

$250,000

$ 23,000

2. Stockholders’ equity section of the balance sheet prepared

Balance Sheet

October 31, 2011

Stas Corporation

authorized, 2,500 shares issued and outstanding

authorized, 11,500 shares issued, and 10,250 shares

outstanding

Chapter 11, P 4. (Continued)

Stockholders’ Equity

Contributed capital

Preferred stock, $100 par value, 6 percent, 5,000 shares

Common stock, $2 stated value, 25,000 shares

Average Stockholders’ Equity

$1.97

$25.00

Chapter 11, P 4. (Continued)

3. User Insight: Performance ratios computed for the quarter

Return on Equity

Net Income

=

must also consider changes in the price of the company’s stock. A return on equity

Stas Corporation’s dividends yield is only 0.4 percent, which means that investors

4. User Insight: Investors’ return discussed

3/25 12,000

12/15 25,200

Bal. 25,200

2×× =

+=

240,000

$21

$9

80,000

80,000 $226,800

$84,000

0.05

Shares outstanding before split: 84,000

252,000 0.10

Common Stock

252,000

1. Transactions recorded in T accounts

Common Stock Distributable

Bal.

Bal.

5/1

12,000

Chapter 11, P 5.

Additional Paid-In Capital Retained Earnings

5/1 12,000

$ 252,000

2,000

3. User insight: Effect of stock transactions determined

shares

receive the same proportionate distributions.

Your proportionate share would be the same because other shareholders would

Mar. 1, 2012:

252,000 shares issued and outstanding

Chapter 11, P 5. (Continued)

If you owned 2,000 shares of Rigby Storage stock on March 1, 2012, you would own

6,930 shares on February 15, 2013 (calculation below).

2. Stockholders’ equity section of the balance sheet prepared

Rigby Storage, Inc.

Stockholders’ Equity

December 31, 2012

Contributed capital

Common stock, $1 par value, 1,000,000 shares authorized,

Original holding

1 Mar. 2 Mar. 1 60,000 1

10 Apr. 15 Apr. 10 26,000 2

Bal. 86,000

Mar. 1 Mar. 2 12,000

Bal. 12,000

Bal.

Dividends Payable

Apr.

128,000Bal.

Start-up and Organization Costs

40,000

79,000

25,000

165,000 37,000

Chapter 11, P 6.

Common Stock

1. Transactions recorded in T accounts

Cash

Additional Paid-In Capital

Mar. 12,000

100,000

65,000

Treasury Stock, Common

Apr. 10

39,000

$ 86,000

Contributed capital

Common stock, $4 par value, 50,000 shares authorized,

21,500 shares issued and 19,000 shares outstanding

Algae Corporation

Balance Sheet

May 31, 2011

2. Stockholders’ equity section of balance sheet prepared

Stockholders’ Equity

Chapter 11, P 6. (Continued)

3. User Insight: Effects of cash dividend declaration discussed

The cash dividend declaration on May 31 will not affect net income and will not

Per Per Dividends

Amount Share Amount Share Allocated

$ 30,000 $ 6.00 — — $ 30,000

Per Per Dividends

Amount Share Amount Share Allocated

1. Dividends calculated for cumulative preferred stock and common stock

2. Dividends calculated for noncumulative preferred stock and common stock

Total

Noncumulative

Common Stock

Dividends

Preferred Stock

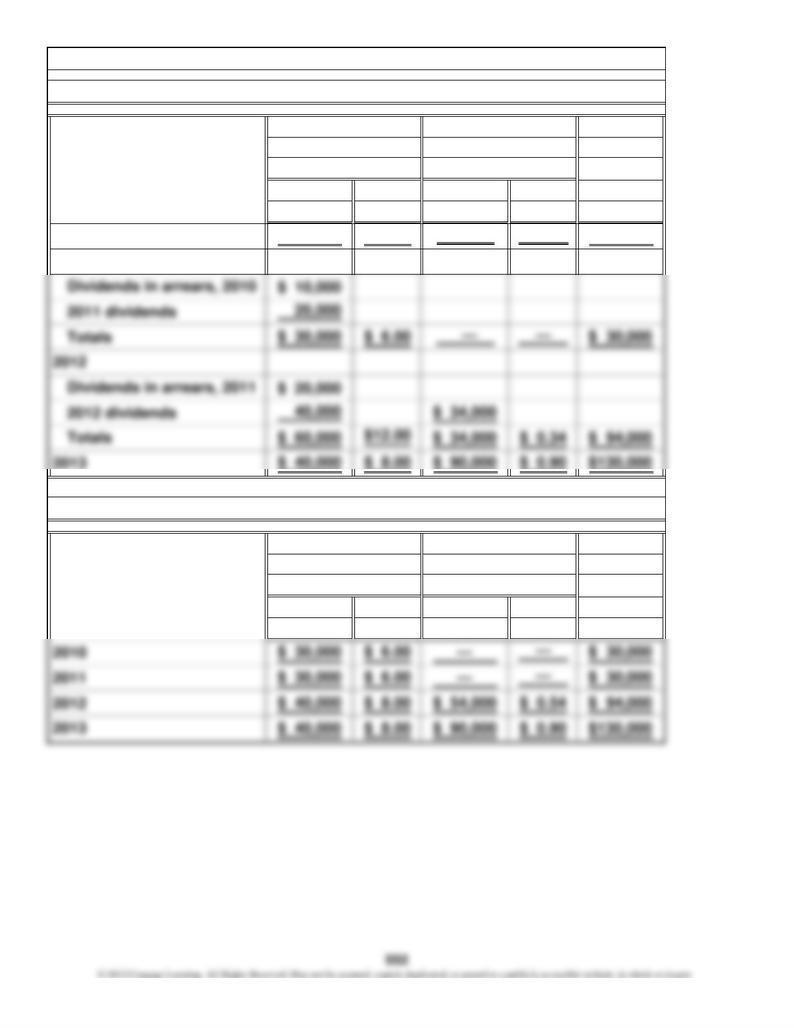

Chapter 11, P 7.

Dividends Total

2010

2011

Dividends

Preferred Stock Common Stock

Cumulative

Dividends

Chapter 11, P 7. (Continued)

4.

3. The 2012 and 2013 dividends yield for common stock calculated

Both cumulative and noncumulative preferred stock have a fixed level of dividends

and are thus similar in this way to long-term bonds, which have a fixed level of in-

terest. However, cumulative preferred stock would be more similar to long-term

would have to be made up. The difference is that with noncumulative preferred

bonds in the sense that if dividends are declared in any given year, past dividends

not paid must be made up. Likewise, any past interest missed on long-term bonds

1 110,000 50,000

60,000

1 5,500 2,500

3,000

2 100,000 100,000

×=

12

No entry required

Common Stock

stated shares of

Cash

$11

July

1.

10,000

Start-up and Organization Costs

value common stock at

Issued

Total $980

$5

Chapter 11, P 8.

Journal entries prepared

$0.02

legal services to organize the corporation

value common stock at $11 per share for

Common Stock

stated $5500

Additional Paid-In Capital

Issued per share

Cash

Additional Paid-In Capital

shares of

$100,000

$65,000

outstanding

Chapter 11, P 8. (Continued)

Contributed capital

Common stock, no-par $5 stated value, 50,000 shares

Preferred stock, $100 par value, 9 percent, 5,000 shares

authorized, 13,000 shares issued, and 11,500 shares

Stockholders’ equity section of the balance sheet prepared

2.

Stockholders’ Equity

Java, Inc.

Balance Sheet

August 31, 2011

authorized, 1,000 shares issued and outstanding

4.8 percent is low and will not encourage a rise in the company’s stock or an ex-

=

$1.00

$20.00

3. User Insight: Performance ratios computed

Chapter 11, P 8. (Continued)

2012

Jan. 4

14 960,000 960,000

14 160,000 160,000

Mar. 8

Apr. 20 72,000 72,000

May 4 32,000 24,000

8,000

July 15 206,400 206,400

+ $94,400 =

25

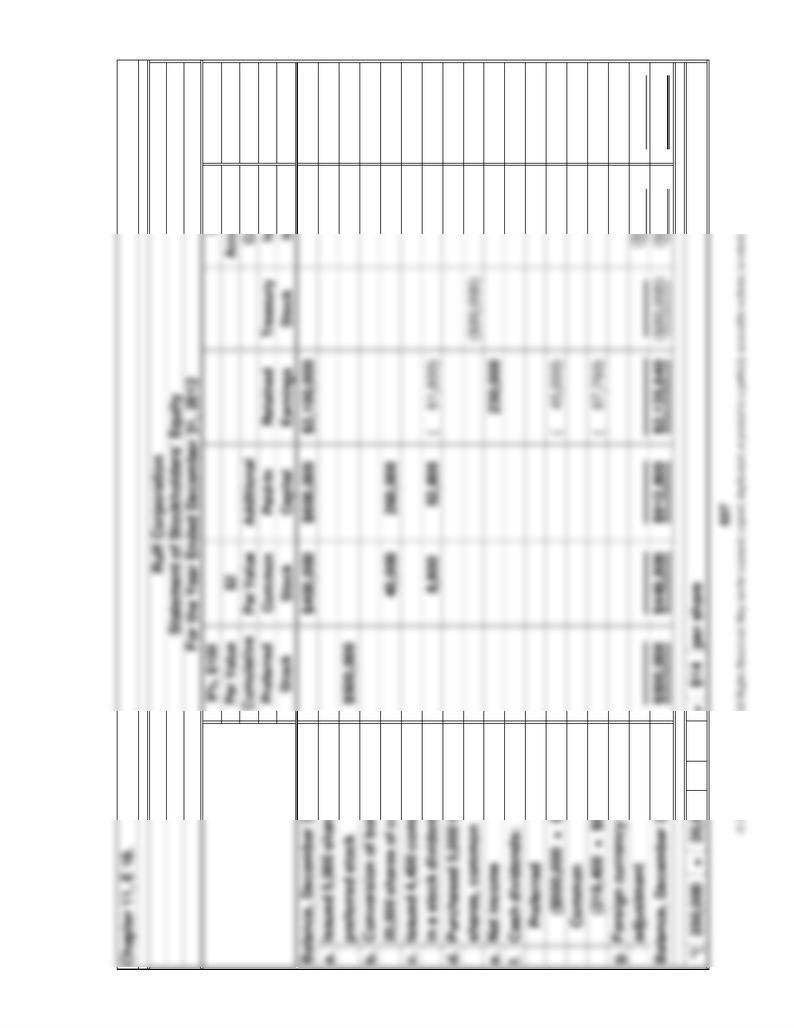

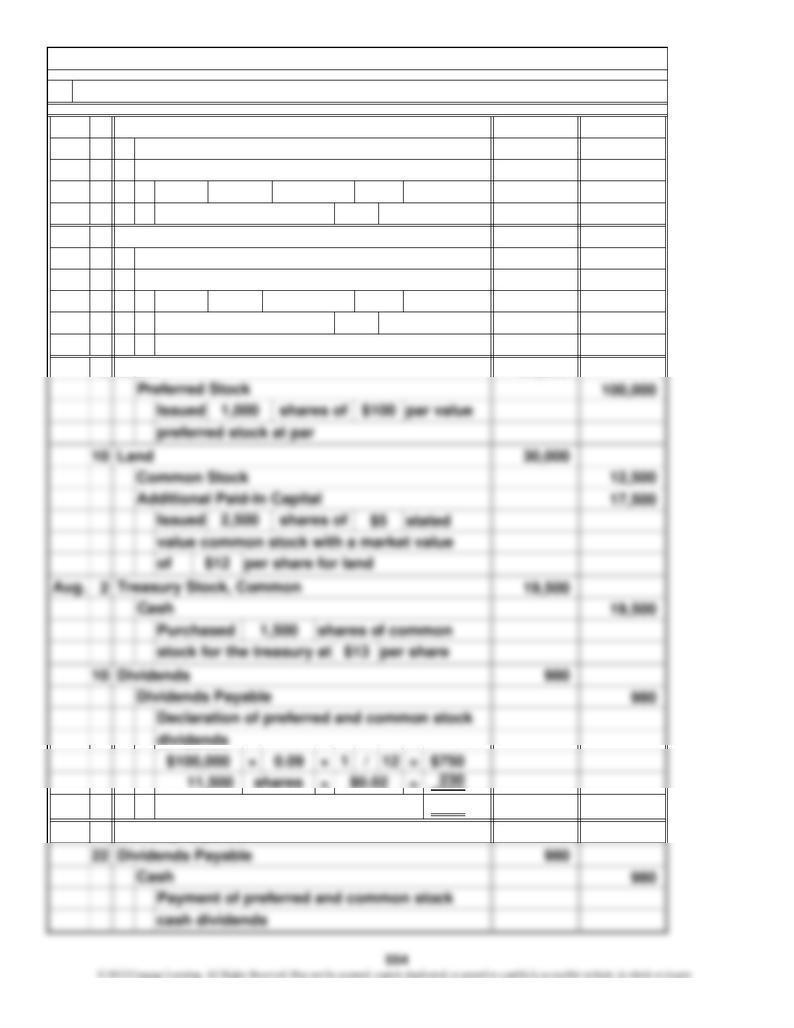

Chapter 11, P 9.

No entry required

Preferred Stock

Issued 4,000 shares of preferred stock in

Preferred Stock

exchange for a building valued at $160,000

Paid-In Capital, Treasury Stock

value common stock issued and outstanding.

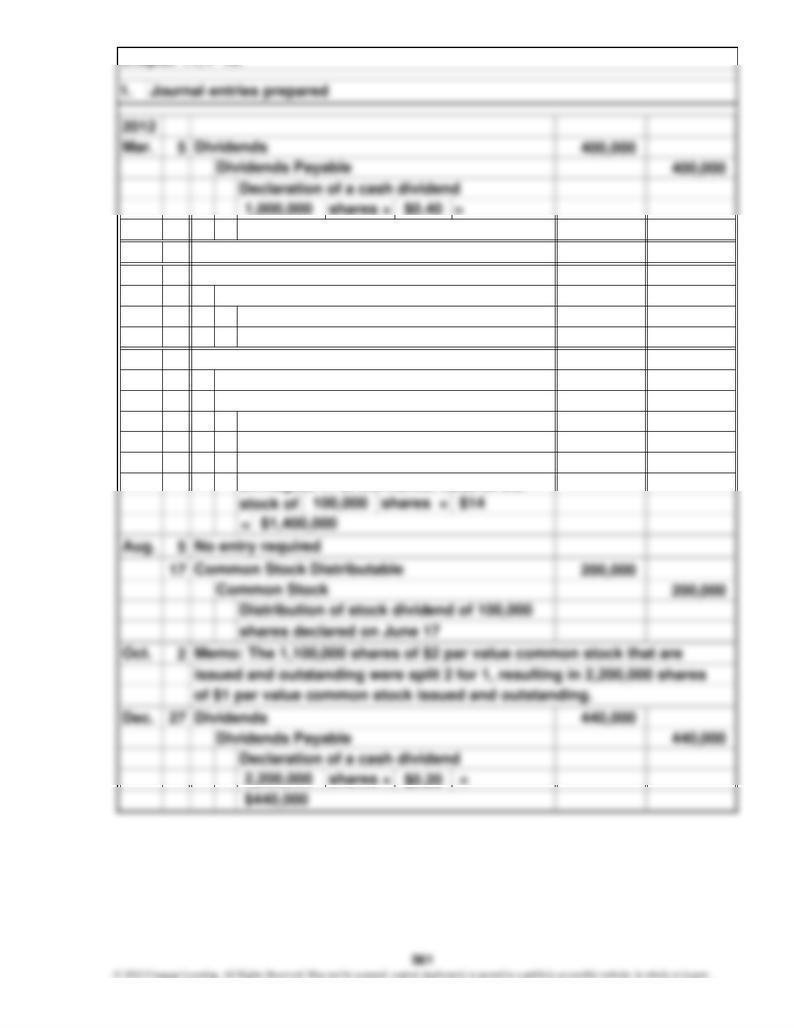

Memo: The 120,000 shares of $8 par value common stock that are issued

1. Journal entries prepared

the treasury at $12 per share

Cash

Sold 24,000 shares of $40 par value preferred

stock at $40

Building

Treasury Stock, Common

share

Cash

per share; originally purchased for $12 per

Purchased 6,000 shares of common stock for

and outstanding were split 2 for 1, resulting in 240,000 shares of $4 par

No entry required $206,400

Dividends

Dividends Payable

Declared a cash dividend of $4 per share on

28,000 shares of preferred stock and $0.40

per share on 236,000 shares of common stoc

k

$112,000

Treasury Stock, Common

Cash

Sold 2,000 shares of treasury stock for $16

557

2012

Aug. 15 206,400 206,400

Nov. 28 708,000 141,600

566,400

Additional Paid-In Capital

Paid cash dividends to preferred and

Dividends Payable

Stock Dividends

Cash

common stockholders

Common Stock Distributable

Declared a 15 percent stock dividend on

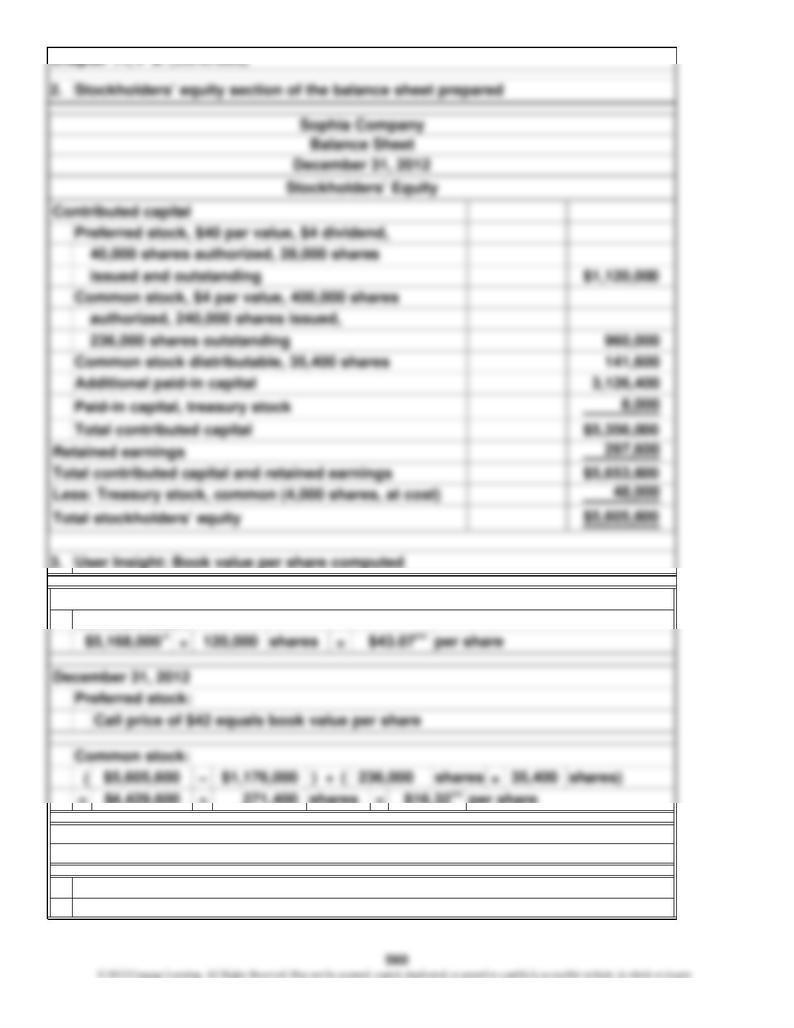

Chapter 11, P 9. (Continued)

Chapter 11, P 9. (Continued)

=÷ =

*

**

December 31, 2011

271,400 ) ÷ (

3.

per share

shares

Rounded.

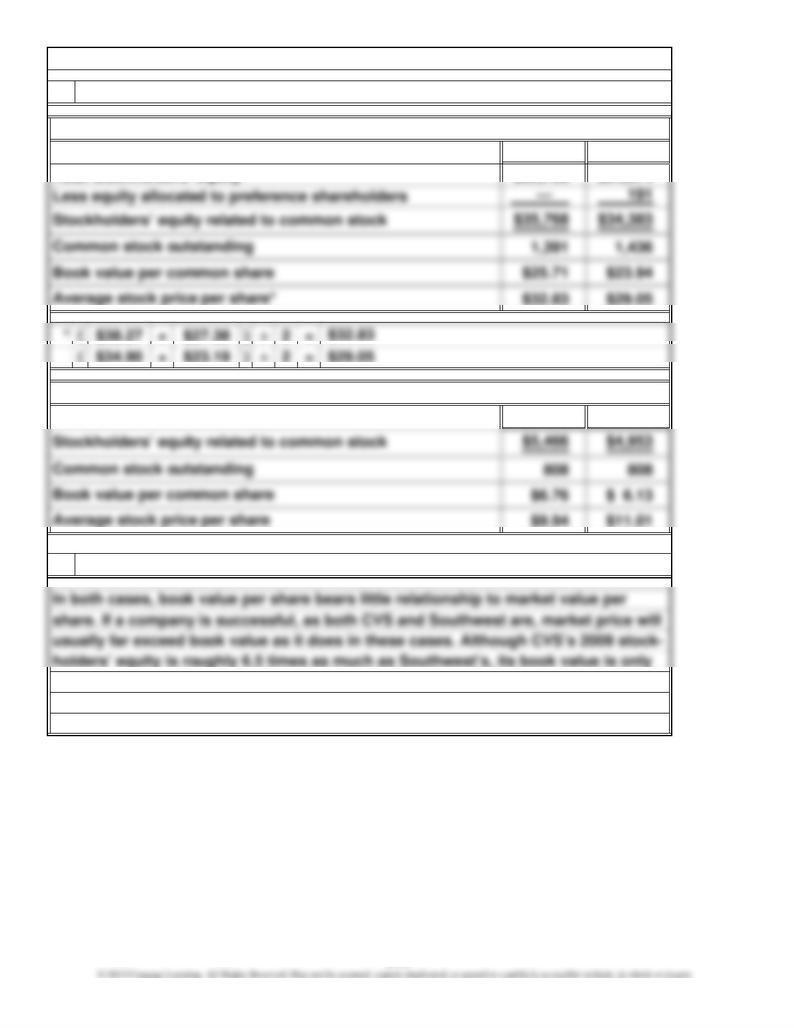

Book value per share usually does not affect market price, which is affected by

28,000 shares of preferred stock × $42 per share

$16.32

$4,429,600

many other factors.

Common stock:

Chapter 11, P 9. (Continued)

$0.40

20

6 400,000 400,000

17 1,400,000 200,000

1,200,000

on August 17 at the market value of the

$0.20

Declaration of a stock dividend of 100,000

Common Stock Distributable

June Stock Dividends

Additional Paid-In Capital

Apr.

Dividends Payable

No entry required

Chapter 11, P 10.

Cash

par value common stock, to be distributed

Payment of cash dividend declared on

March 5

shares (1,000,000 shares × 0.10) on $2

$400,000

$2,200,000

=

pany declares stock dividends or stock splits. These actions often accompany

Jet Moving Company

Contributed capital Stockholders’ Equity

Chapter 11, P 10. (Continued)

Balance Sheet

If you owned shares in Jet, you would expect the total value of your shares to re-

main about the same, although the price per share would be less because there

positive views on the part of management about the future of the company.

are more shares outstanding. An intangible that might cause the total value to in-

crease is that it is usually considered a positive sign to the market when a com-

2. Stockholders’ equity section of the balance sheet prepared

3. User Insight: Effect of stock transactions on share price

Common stock, $1 par value, 6,000,000 shares authorized,

2,200,000 shares issued and outstanding

December 31, 2012

562

Chapter 11, C 2.

terest rates decline and a company wishes to refinance the stock, it can call the

mon stock rises above the conversion price, the price of the preferred stock will

PERCs are popular with companies because they provide great flexibility. If the in-

long-term debt. Another advantage is that issuing stock is less risky than issuing

reduces the company’s ability to use financial leverage to increase the return on

ible, whereas dividends paid on common stock are not.

equity over the return on assets. Also, the interest paid on bonds is tax-deduct-

to be repaid. These are effects that could improve DreamWorks’ bond rating and

dividend rate, they are classified on the balance sheet as equity. This is very im-

portant to companies that have suffered losses resulting in decreased stockhold-

stock and retire it. If a company does not have the cash to redeem the shares, it

assets. From the investor’s standpoint, the dividend is fixed, like bond interest.

The value of the preferred stock varies with changes in the market rate of interest,

also like bond prices. If the preferred stock is convertible and the price of the com-

then rise with the common price (in which case the investor has a capital gain).

An advantage of issuing common stock is that it improves the company’s debt to

Chapter 11, C 1.

equity ratio by increasing the amount of common stock outstanding in relation to

Even though preferred stocks have some characteristics of bonds, such as a fixed

ers’ equity and to banks, which must maintain minimum ratios of capital to total

bonds because dividends do not have to be paid on stock and there is no debt

lower the interest it might pay on future bond issues. A disadvantage of issuing

ers unless they buy more shares. In addition, when the company is profitable, it

stock is that it dilutes the share of the company owned by the current stockhold-

Chapter 11, C 3.

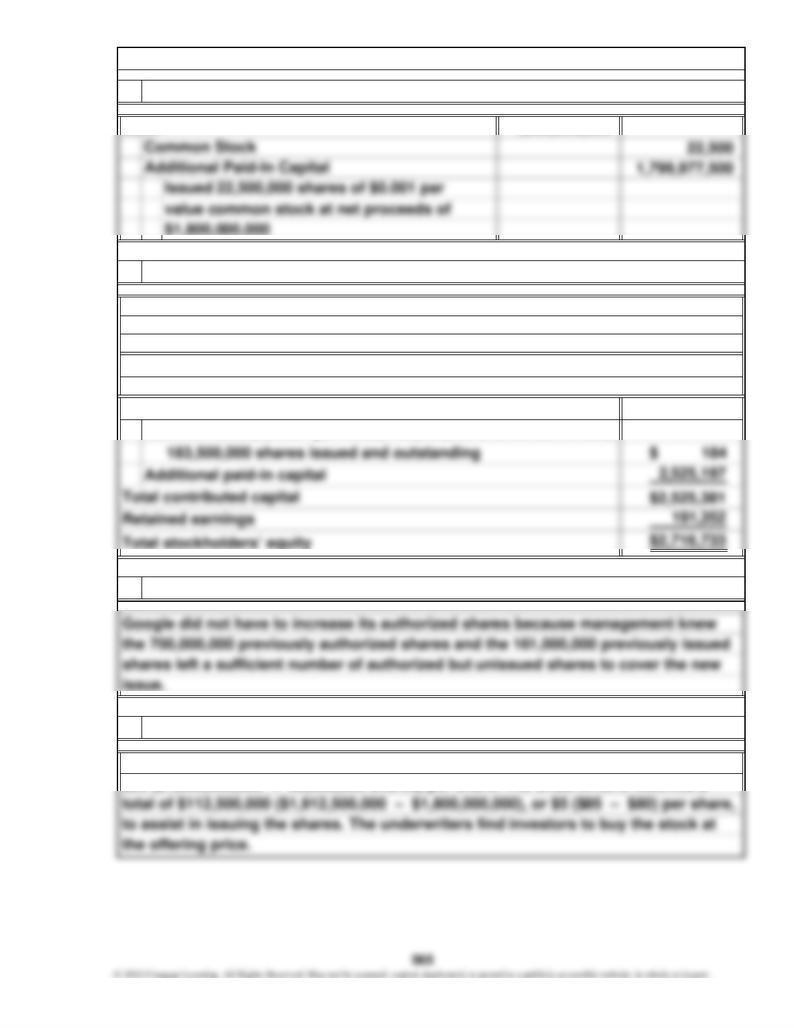

1,800,000,000 22,500

The total proceeds were $1,912,500,000 ($85 × 22,500,000 shares). Google received

$80 ($1,800,000,000 ÷ 22,500,000 shares) per share. The underwriters received a

4. Underwriters’ fee discussed

Contributed capital

Balance Sheet

After Stock Offering

Google, Inc.

Stockholders’ Equity

3. Google’s need to increase the authorized shares discussed

Common stock, $0.001 par value, 700,000,000 shares authorized,

1. Stock issue recorded as journal entry

2. Stockholders’ equity section of the balance sheet prepared

Cash

Chapter 11, C 5.

(in thousands)

(8)

2. Comprehensive income discussed

Chapter 11, C 6.

sources other than owners and includes net income, change in unrealized invest-

ment gains and losses, and other items affecting equity. Thus, Spencer’s compre-

Comprehensive income is the change in a company’s equity during a period from

1.

3.

4.

(called a stock incentive plan) described in Note 10. These options apply to

lates to the preference stock. In addition, the company has a stock option plan

Chapter 11, C 7.

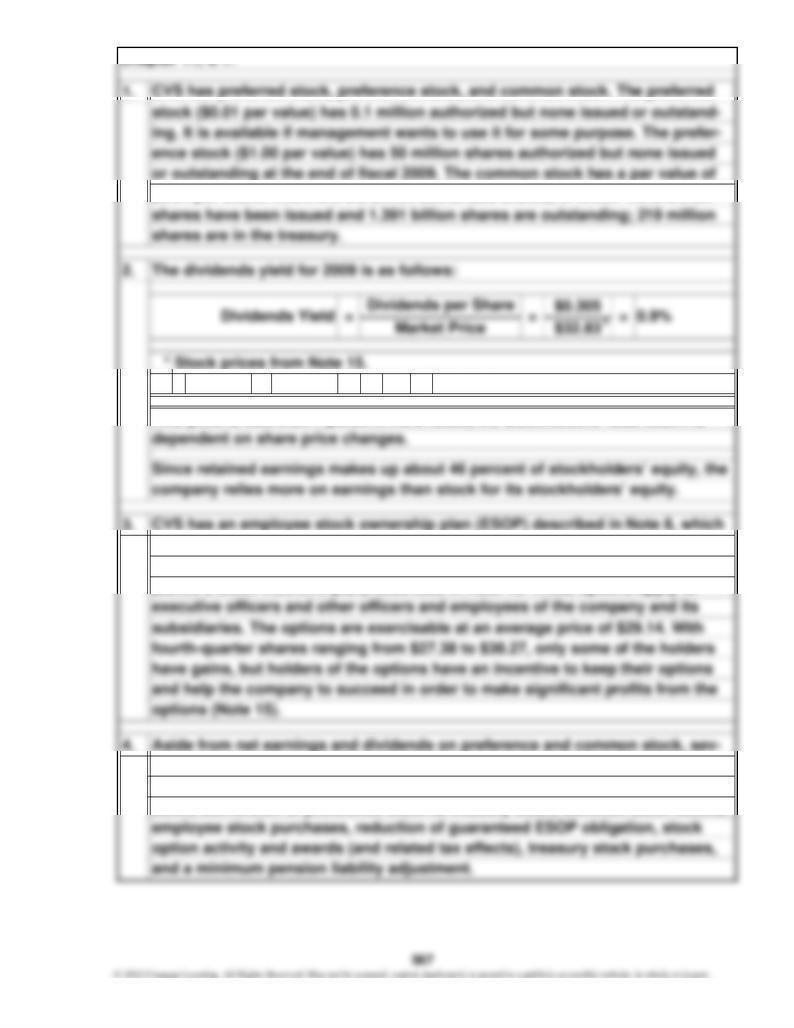

$0.01 per share. There are 3.2 billion authorized shares, of which 1.612 billion

applies to full-time employees with at least one year of service. This plan re-

$32.83

This yield is less than 1 percent. As a result, the stockholders’ total return is

eral items appear on each of the three years of CVS’s statement of sharehold-

ers’ equity. These items include conversion of preference stock to common

stock, conversion of preference stock to treasury stock, common stock issued,

=

=

=

=

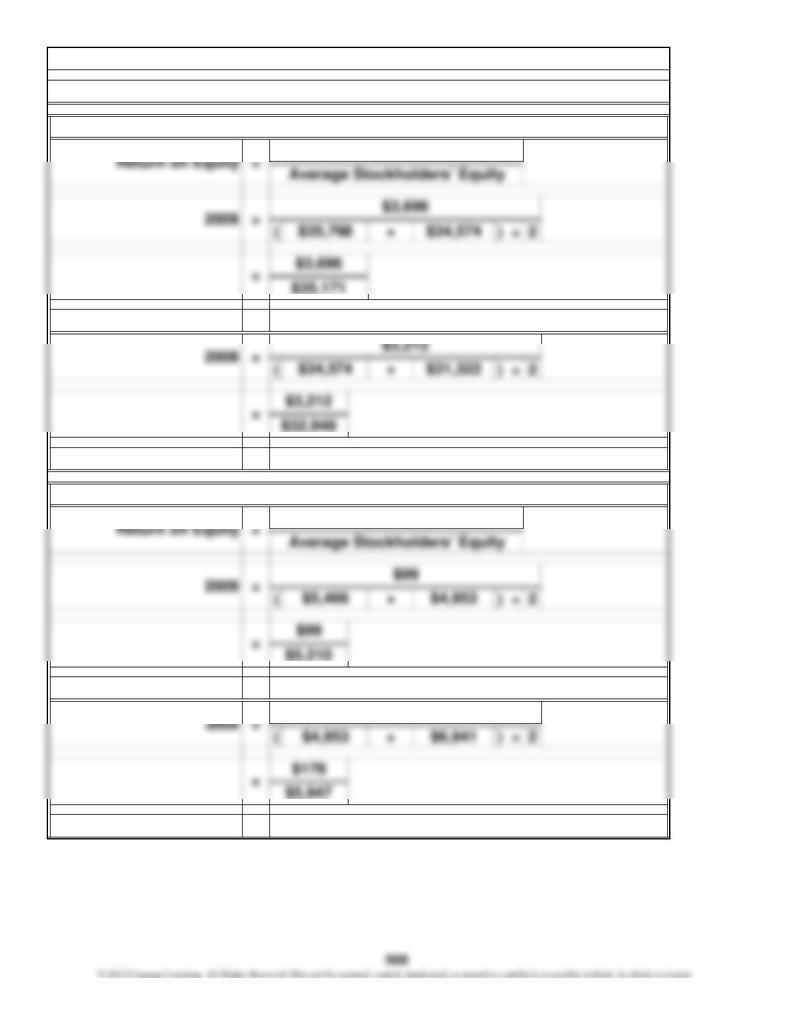

3.0%

1.9%

Southwest’s Return on Equity Ratio:

Net Income

Net Income

Chapter 11, C 8.

1. Return on equity computed (dollars in millions)

CVS’s Return on Equity Ratio:

10.5%

9.7%

$178

holders’ equity, it may be seen that both companies pay cash dividends, but the

Dividend policies discussed

From their income statements, statements of cash flows, and statements of stock-

4.

Neither company raised significant funds through stock issues. It may be seen in

According to the statement of cash flows, CVS purchased treasury stock of $2.477

billion in 2009, but about $7.87 billion over the past three years. In contrast, South-

3. Stock issues discussed

Chapter 11, C 8. (Continued)

2. Treasury stock purchases discussed

2009 2008

$35,768 $34,574

$34.90 + $23.19 ) ÷2=

2009 2008

6. Book values per share and their relationship to market prices discussed

Total stockholders’ equity

Chapter 11, C 8. (Continued)

5. Book values per share computed

of shares outstanding. CVS has roughly two times as many shares outstanding as

about 3.8 times that of Southwest. Book value per share is a function of the number

Southwest does.

CVS’s Book Value per Share (in millions except per share):

Southwest’s Book Value per Share (in millions except per share):

570

are harmed by this action in at least two ways. Buying treasury stock is not unethi-

Chapter 11, C 9.

Some may argue that if management were not prohibited from taking such action,

then its actions might be judged as acceptable. Others will clearly see that owners