7–3 What does the term reciprocal mean in the context of departmental cost allocation?

7-4 There are three methods for departmental cost allocation: the direct method, the

step method, and the reciprocal method.

The direct method of cost allocation is done by taking the service department

3. The allocation of costs of production departments to products

The first phase in departmental cost allocation has two parts: to trace the direct

manufacturing costs in the plant to each service and production department that used

7-6 There are a number of possible answers here. The chapter gives an example of

the use of departmental cost allocation in the banking industry. Other examples

would include cost allocation in an electric utility company to provide a basis for

3. The allocation of costs of production departments to products

The first phase in departmental cost allocation has two parts: to trace the direct

manufacturing costs in the plant to each service and production department that used

7-7 There are four methods for by-product costing:

The two asset recognition methods are:

Method 1 - Net Realizable Value Method. This method shows the net realizable

value of by-products in the income statement as a deduction from the total

manufacturing cost in the period in which the by-product is produced.

Method 2 - Other Income at Production Point Method. This method shows the

net realizable value of by-products in the income statement as an other income or

other sales revenue item in the period in which the by-product is produced.

The two revenue methods are:

Method 3 - Other Income at Selling Point Method. The net sales revenue from a

7–8 What are the limitations of joint product cost allocation?

7–9 What are the implementation issues of departmental cost allocation?

7–10 What are some of the ethical issues of cost allocation?

7-10 A number ethical issues are important when implementing cost allocation

methods. First, there are ethical issues when cost allocation is used in a situation

where the products or services are produced for both a competitive market and for

a public agency or government which is paying on a cost-plus basis. There is an

incentive for the provider to allocate an unfairly high portion of joint costs to the

cost-plus customer.

A second issue is the equity or “fair share” issue that arises when a government

reimburses costs of a private institution, or when government provides a service for

7-9 There are a number of implementation issues to consider when using either joint cost

allocation or departmental cost allocation.

One implementation issue is that it is often difficult to determine an appropriate

allocation base to allocate the joint product costs or to determine a figure for percentage

7-7 There are four methods for by-product costing:

The two asset recognition methods are:

Method 1 - Net Realizable Value Method. This method shows the net realizable

value of by-products in the income statement as a deduction from the total

manufacturing cost in the period in which the by-product is produced.

Method 2 - Other Income at Production Point Method. This method shows the

net realizable value of by-products in the income statement as an other income or

other sales revenue item in the period in which the by-product is produced.

The two revenue methods are:

Method 3 - Other Income at Selling Point Method. The net sales revenue from a

Brief Exercises 7-11 through 7-19

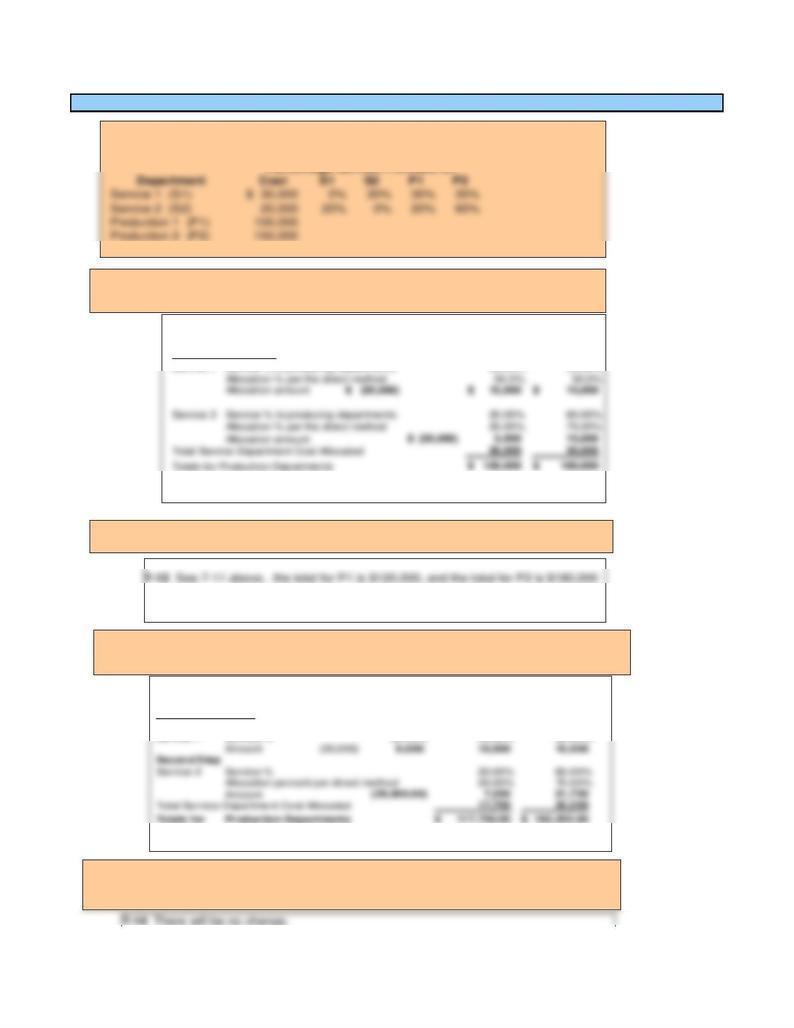

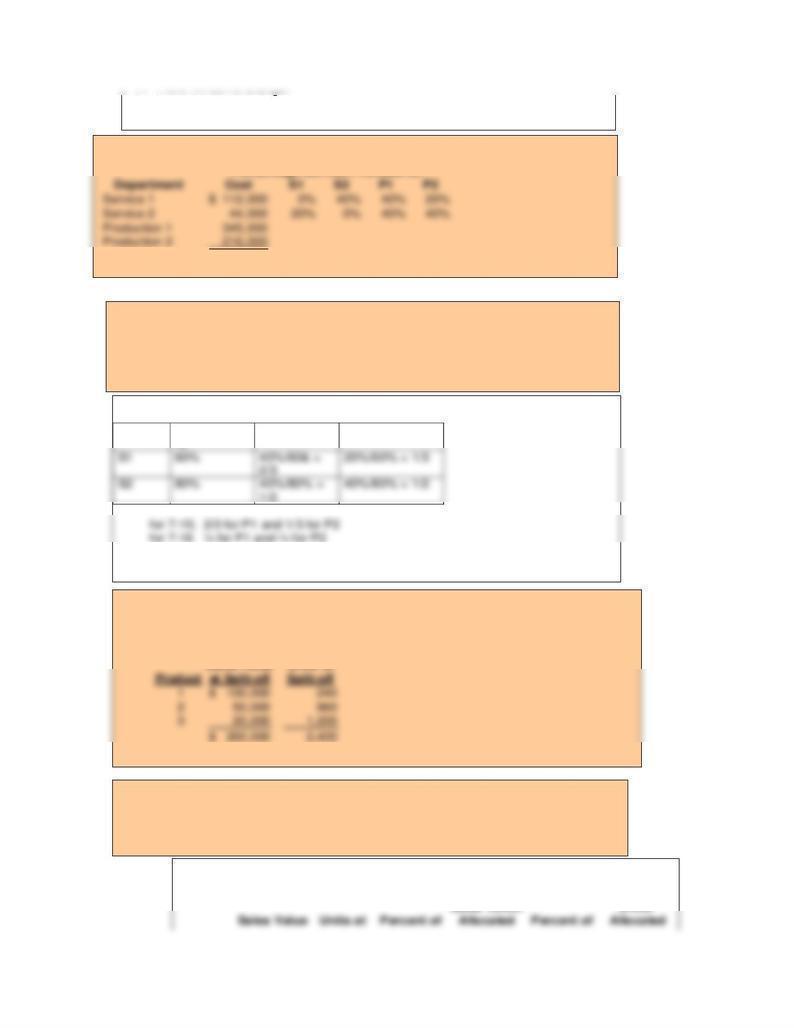

7-11 through 7-14 Involve departmental cost allocation with two service departments

and two production departments.

Percentage Service Provided to:

7-11 What is the amount of service department cost allocated to P1 and P2 using the

direct method?

7-12 What is the total cost in P1 and in P2 after allocation?

7-13

Total cost allocated to P1 is $17,500 and to P2 is $32,500

The Step Method

First Step

Service 1 Service % 30.00% 35.00% 35.00%

7-13 What is the amount of service department cost allocated to P1 and P2 using the step

method with S1 going first?

7-14 How does your answer to 12-11 change if the cost in Production 1 is changed from

$100,000 to $120,000?

7-11

Total cost allocated to P1 is $20,000 and to P2 is $30,000

The Direct Method

Service 1 Service % to producing departments 35.00% 35.00%

7-15, 16

Non Service

P1

P2

7-17,18

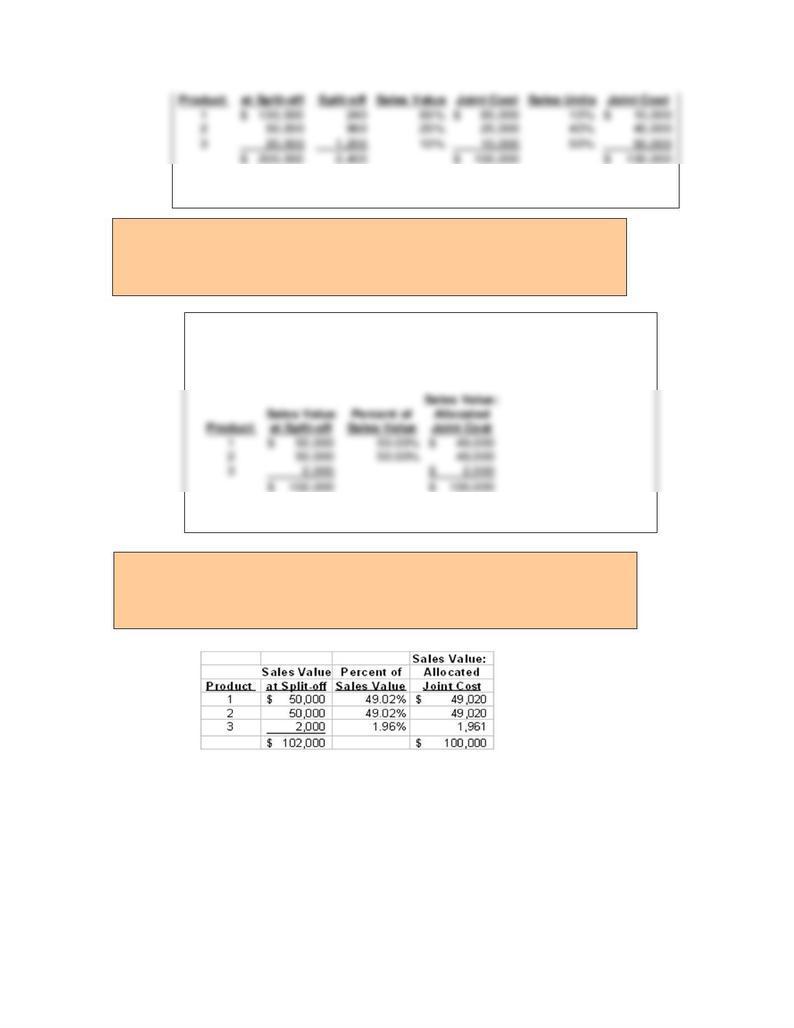

The cost allocations are shown below.

Sales Value: Units:

7-15 and 7-16 require the following information

Percentage Service Provided to:

7-15 What percentage of service department 1’s costs are allocated to P1 and to P2

under the direct method?

7-16 What percentage of service department 2’s costs are allocated to P1 and to P2

under the direct method?

7-17 through 7-20 require the following information about a joint production process

for three products, with a total joint production cost of $100,000. There are no

separable processing costs for any of the three products.

Sales Value Units at

7-17 What amount of joint cost is allocated to each of the three products using the

relative sales value method?

7-18 What amount of joint cost is allocated to each of the three products using the

physical units method?

7-17,18

The cost allocations are shown below.

Sales Value: Units:

7-19

First, the net realizable value of the by-product, $2,000 is reduced from the total joint

product cost; the by-product is inventoried at $2,000, and the remaining joint cost of

$98,000 is allocated to products 2 and 3 using the net realizable value method, as

follows:

7-19 Assume that the total sales value at the split-off point for product 1 is $50,000

instead of $130,000 and the sales value of product 3 is $2,000 instead of $20,000.

Assume also that, because of its relatively low sales value, the firm treats product 3 as

a by-product and uses the net realizable value method for accounting for joint costs.

What amount of joint cost would be allocated to the three products?

7-20 Assume the same as for 7-19 above except that product 3 is treated as a joint

product. What amount of joint costs would be allocated to the three products using

the relative sales value method?

Exercise 7-21 Cost Allocation, General

Solution (15 min)

An organization’s service and administrative costs can be substantial, and some or all of these costs usually are allocated

to cost objects. Thus, the allocations of service and administrative costs can have a significant impact on product cost and

pricing, asset valuation, and segment profitability.

Required

When service and departmental costs are allocated, they are grouped into cost pools and then allocated to cost

objects according to some allocation base.

a. Compare and contrast the benefit received and cause-and-effect criteria for selecting an allocation base.

b. Explain what the ability-to-bear costs criterion means in selecting an allocation base.

Cost pools are collections of costs that are similar in nature and have

a presumed causal connection. Examples of cost pools include

Exercise 7-22 By-Products and Decision-Making Strategy

Solution (15 min)

Lowman Gourmet Products produces a wide variety of gourmet coffees (sold in pounds of roasted beans), jams,

jellies, and condiments such as spicy mustard sauce. The firm has a reputation as a high-quality source of these

products. Lowman sells the products through a mail-order catalog that is revised twice a year. Joe, the president, is

interested in developing a new line of products to complement the coffees. The manufacture of the jams and jellies

presently produces an excess of fruit liquid that is not used in these products. The firm is now selling excess liquid to

other firms as flavoring for canned fruit products. Joe is planning to refine the liquid and add other ingredients to it to

produce a coffee-flavoring product instead of selling the liquid. He figures that the cost of producing the jams and

jellies, and therefore the fruit liquid, is irrelevant; the only relevant concern is the lost sales to the canneries and the

cost of the additional ingredients, processing, and packaging.

Required

How would you evaluate the financial and strategic issues facing Joe regarding the potential coffee-flavoring

product?

Joe is considering using a fruit-liquid, which is a by-product of the processing for his jams and jellies,

to produce a new product–a coffee flavoring to complement his line of gourmet coffees. Joe is correct

in understanding that the production cost of jams and jellies is irrelevant, since the fruit-liquid is a

necessary by-product of the production of jams and jellies. He is also correct to understand that the

cost of the additional ingredients and processing is relevant.

The correct financial decision is to compare the additional costs of the added ingredients and

processing, plus any additional packaging and handling costs for the new product versus the net

revenue from the sales to canneries–price to canneries less any selling costs. The key to the decision is

to ignore the joint costs, but focus instead only on the separable costs and the increase in sales value.

This question is addressed further in chapter 11 under the heading, “Decisions to Sell Before or After

Additional Processing.”

The more critical consideration is the strategic issue: will the new product line enhance the sales of

Exercise 7-23 Federal Reserve Banks; Cost Allocation

In recent years, due to the effects of the Great Recession on the construction industry, a decline in demand for paper

products, and increased demand for reduced carbon emissions from climate change, significant changes have taken

place in the harvesting and processing of wood products. The demand for lumber for construction has decreased, and

the demand for alternative fuels has increased. The result is that the timber industry in the southeastern states and some

1. Should the wood pellets be accounted for as a by-product or a main product for the timber industry? Explain briefly.

2. Assess the sustainability issue for the production of wood pellets. What are the advantages and disadvantages of the

use of wood pellets in power generation as a replacement for coal?

3. Most of the current demand for wood pellets if from EU countries. Would your answers above differ if the wood

pellets were used domestically instead of shipped to the EU for use there?

1. The wood pellets should be accounted for as a by-product since the

2. Some environmentalists have argued against the use of wood pellets

as a green source of energy. They say that it would take 54 years

for a new tree to consume the carbon emissions of a single tree

burned as pellets. Others argue that the use of timber for wood

3. The issues of sustainability and climate change are global issues.

That is, emissions anywhere in the world have an effect on climate

Exercise 7-24 Cost Allocation and Taxation at Nonprofit Organizations

Nonprofit organizations are exempt from federal income tax except for income from any activities that are unrelated to

the nonprofit’s charitable purpose. An example is the use of a laboratory for both tax-exempt basic medical research and

for testing a taxable product for commercial pharmaceutical firms. A concern in these cases is that the tax-exempt

nonprofit organization will be able to compete unfairly with for-profit firms because of their tax-exempt status. The key

argument is that common costs for the nonprofit’s exempt and business activities will be used to “subsidize” the for -profit

business (in this case, the taxable product testing).

Required

How would cost allocation play a role in affecting the profits of a nonprofit organization which has both business and

charitable activities?

Exercise 7-25 Fuel Surcharges; Allocating the Increased Cost of Fuel

U.S. Railroads, including Burlington Northern Santa Fe Corp (BNSF) and CSX Corp. began using fuel surcharges in 2001

to recapture some of the additional costs due to the sharp rise in fuel costs in late 1999, continuing into 2000. Fuel costs

have continued to increase and the fuel surcharges have continued to increase as well, accounting for approximately 12% of

BNSF’s revenues in the third quarter of 2008. Companies that use the railroads for shipping agricultural, chemical, and

other commodities have been critical of the allocation methods the railroads use to apply the surcharges. The railroads have

used surcharges based upon a percentage of charges for the shipment. Shippers have argued that an allocation based on

1. How would you propose that the increased cost of fuel be charged to shippers by the railroads?

2. Do you think the STB ruling should solve the problem?

3. What are the key sustainability issues for a consumer of rail transport?

1.,2.

The rising cost of fuel has affected many industries, but particularly

those in the transportation industries. In air freight, trucking, and

railroads, the surcharges can be as high as 35% of average charges.

The surcharges can be a substantial portion of total revenues for

these firms. The practice of fuel surcharges has grown widely to

include many service firms, involving most types of deliveries of

products or services (florists, retailers, appliance repair, and many

others). Unfortunately, many of these surcharges do not seem to be

reduced or removed when fuel prices fall.

The issue of surcharges for railroads has been a contentious

one for the shippers and railroads. There have been several law

suits regarding the conflicts and currently several of the largest U.S.

railroads are subject to a suit charging price fixing regarding their use

of surcharges. The railroads’ attempt to have the suit dismissed

recently failed in U.S. courts (https://ecf.dcd.uscourts.gov/cgi-

3. The sustainability issue arises in the case of rail transport because

rail transport is more efficient than truck transport. A shipper that

has the option between the two methods of transport should

consider the cost of shipping as well as the speed of delivery and

quality of service, in addition to the consideration of the

environmental impact of the greater use of fuel for the trucking

option.

Based on: “U.S. Appellate Court Reverses Class-certification

Decision for Fuel Surcharge-fixing Lawsuit Against Four Class Is,”

August 12, 2013,

http://www.progressiverailroading.com/norfolk_southern/news/US-

appellate-court-reverses-classcertification-decision-for-fuel-

surchargefixing-lawsuit-against-four-Class-Is--37234;

Also, Christine Hauser, “Shippers May Raise Fuel Fees,” The New

York Times, April 26, 2011; Mina Kimes, “Railroads: Cartel or Free

3. The sustainability issue arises in the case of rail transport because

rail transport is more efficient than truck transport. A shipper that

has the option between the two methods of transport should

consider the cost of shipping as well as the speed of delivery and

quality of service, in addition to the consideration of the

environmental impact of the greater use of fuel for the trucking

option.

Based on: “U.S. Appellate Court Reverses Class-certification

Decision for Fuel Surcharge-fixing Lawsuit Against Four Class Is,”

August 12, 2013,

http://www.progressiverailroading.com/norfolk_southern/news/US-

appellate-court-reverses-classcertification-decision-for-fuel-

surchargefixing-lawsuit-against-four-Class-Is--37234;

Also, Christine Hauser, “Shippers May Raise Fuel Fees,” The New

York Times, April 26, 2011; Mina Kimes, “Railroads: Cartel or Free

Problem 7-26 Cost Allocation and Legal Disputes

Cost allocation is often the centerpiece of conflict that is resolved in court cases. The litigation usually involves the dispute over

how costs are allocated to a product or product line that is of interest to the plaintiff. This is particularly an issue when a company

produces some products or services for a price-competitive market while other products or services are produced for a

governmental unit on a cost-plus or reimbursement basis.

The following cost allocation disputes involve an organization (Nursing Care Inc, or NCI) that operates both a nursing

home and an apartment building for retirees (retirement home). A single kitchen is used to provide meals to both the nursing

home and retirement home. Also, certain labor costs and utilities costs of the kitchen are shared by the two homes. Many of

those living in the nursing home are indigent and are on Medicaid. The state Department of Health and Family Services (DHFS)

reimburses NCI at Medicaid approved cost reimbursement rates. The Medicaid reimbursement rates are based on cost

information supplied by the organization, in this case NCI, and are assumed to be accurate; cost allocations are assumed to be

reasonable. DHFS has examined the cost report of NCI and has raised the following issues which are now being litigated.

Required

(the above is based upon an actual case, with names disguised)

For each issue, consider whether you think the defendant (NCI) or the plaintiff (DHFS) has the valid position, based on your

understanding of cost allocation.

a. DHFS alleges that NCI charged specific milk, condiments, and paper products to the nursing home, without following the

8-0986&invol=1

a. The court determined that further documentation was not required,

but that the stated reason for charging these items to the nursing

home is persuasive, and that further, DHFS had not shown that it had

asked NCI for the documentation. The specific assignment of these

costs to the nursing home was therefore allowed.

b. The court determined that DHFS had “no substantial basis” for

disallowing the direct assignment of the nourishment costs to the

nursing home. The court judged that it was apparent that the nursing

home residents were the exclusive consumers of these costs and that

the costs should therefore be traced directly to the nursing home.

The actual case is based on a dispute between the Department of Health

8-0986&invol=1

a. The court determined that further documentation was not required,

but that the stated reason for charging these items to the nursing

home is persuasive, and that further, DHFS had not shown that it had

asked NCI for the documentation. The specific assignment of these

costs to the nursing home was therefore allowed.

b. The court determined that DHFS had “no substantial basis” for

disallowing the direct assignment of the nourishment costs to the

nursing home. The court judged that it was apparent that the nursing

home residents were the exclusive consumers of these costs and that

the costs should therefore be traced directly to the nursing home.

Problem 7-27 Cost Allocation; Cost Shifting

In the last several years, airlines have succeeded in boosting profits by adding fees for previously free services such as in-flight

snacks and meals, checked baggage, priority boarding, and other services. These fees have caused some shifts in customer

1. The cost-shifting in this case is from the airlines (that experience

lower costs of baggage handling) to TSA (that experience a larger

number of “carry-on” bags to examine) and to the airline passengers

(who experience the discomfort of increased time in going through

TSA security and the cost of the $2.50 security fee that is included in

2. Cost-shifting is frequently an area of ethical concern, as it involves

3. Given the emphasis airline customers place on price, air travel has

become somewhat of a commodity. It is hard to differentiate the

different carriers. The “fees for services” approach is consistent with

From: To:

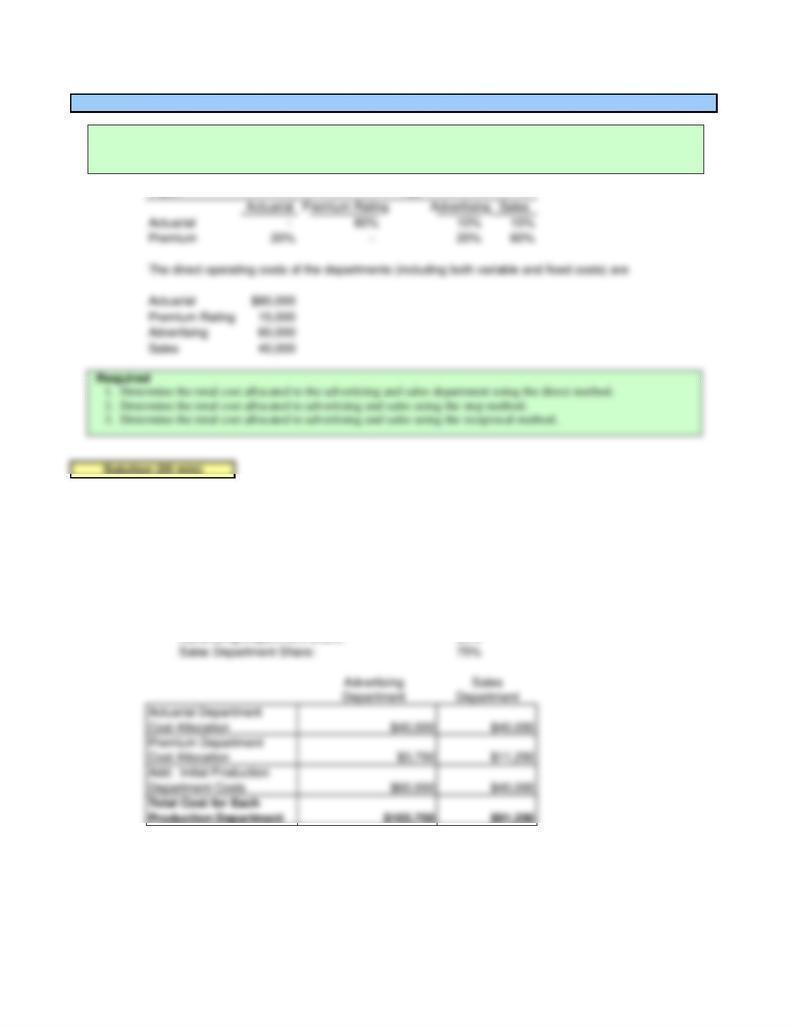

1) The Direct Method

Net service to both Production Departments

(Advertising and Sales) for the Actuarial Service Dept:

20%

Advertising Department Share: 50%

Sales Department Share: 50%

Net service to both Production Departments

for Premium Department: 80%

Advertising Department Share: 25%

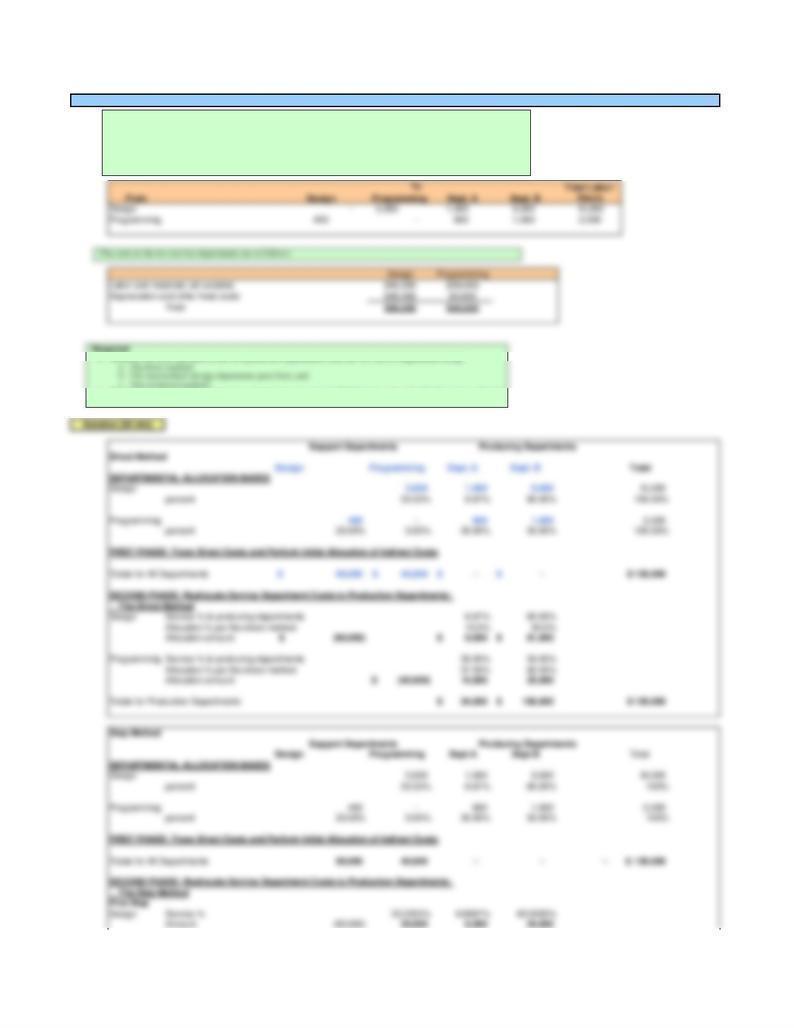

Exercise 7-28 Departmental Cost Allocation

HomeLife Life Insurance Company has two service departments (actuarial and premium rating) and two production

departments (advertising and sales). The distribution of each service department’s efforts (in percentages) to the other

departments is as follows:

2) The Step Method

The Actuarial Department goes first since it provides the greatest service to the other service

departments:

Actuarial Department

3) The Reciprocal Method

Solve the Simultaneous Equations: (S1=Actuarial; S2=Premium)

S1 = $80,000 + .2 x S2

S2 = $15,000 + .8 x S1

S1 = $80,000 + .2 x ($15,000 + .8 x S1)

S1 = $98,810

S2 = $15,000 + .8 x $98,810

S2 = $94,048

Advertising

Sales

Sales

Department

Department

Department

Premium

Advertising

S1 - 10% 20% ? %

S2 10% - ? % 30%

Exercise 7-29 Departmental Cost Allocation

3. Determine the total cost of P1 and P2 using the reciprocal method.

1) The Direct Method

Net service to both Production Departments

for Service Department 1: 90%

Production Department 1's Share: 22%

Production Department 2's Share: 78%

Net service to both Production Departments

for Service Department 2: 90%

Production Department 1's Share: 66.67%

Production Department 2's Share: 33.33%

2) The Step Method

Both service departments serve each other the same percentage of

total service; hence, either can go first. Here, Service Department 1 goes

first on the basis that it has the higher total cost:

Service Department 1

Production

Department 2

Department 2

Department 1

Service

Production

3) The Reciprocal Method

Solve the Simultaneous Equations:

S1 =

$180,000 + .1 x S2

S2 = $60,000 + .1 x S1

S1 = $180,000 + .1 x ($60,000 + .1 x S1)

S1 = $187,879

S2 = $60,000 + .1 x $187,879

S2 = $78,788

Solution (15 min)

Exercise 7-30 Joint Products; Blood Donation

3. Plasma, used after further processing, for the treatment of protein deficiency.

The joint cost of producing the three products consists of the blood collection costs, the safety testing costs, and further

processing in a laboratory to split off the three joint products. Commonly the joint costs are allocated to the three products on the

basis of physical

units produced. The National Blood Authority (NBA) in the U.K. observed the unfavorable effect of this approach is that the cost

of each blood product could change significantly from time to time, as the demand for the products varied; the demand for the

platelets was particularly volatile. In response, the NBA decided in to allocate all joint costs to red cells, on the basis, in part, that

plasma was routinely discarded to minimize the risk of Creutzfeld-Jacobs disease.

Required: What are the advantages and disadvantages of the allocation approach proposed by the NBA? What allocation

method would you suggest as an alternative, if any?

As the text notes, the physical units method often involves inappropriate allocation of costs as the physical

Units Produced

Product and Sold Total Additional Costs Total Sales Value

M 10,000 $10,000 $160,000

N 4,000 $10,000 $140,000

T 5,000 $5,000 $25,000

Exercise 7-31 Joint Products

After Split-Off

Solution (10 min)

Tango Company produces joint products, M, N, and T from a process. The following information concerns a batch

produced in April at a cost of $120,000:

Required

How much of the joint cost should be allocated to each joint product using the net realizable value method.

The allocation for the net realizable value method is shown below. Note

however, that Product B has a very small sales value relative to the two

other products. Should it more properly have been treated as a by-

product?

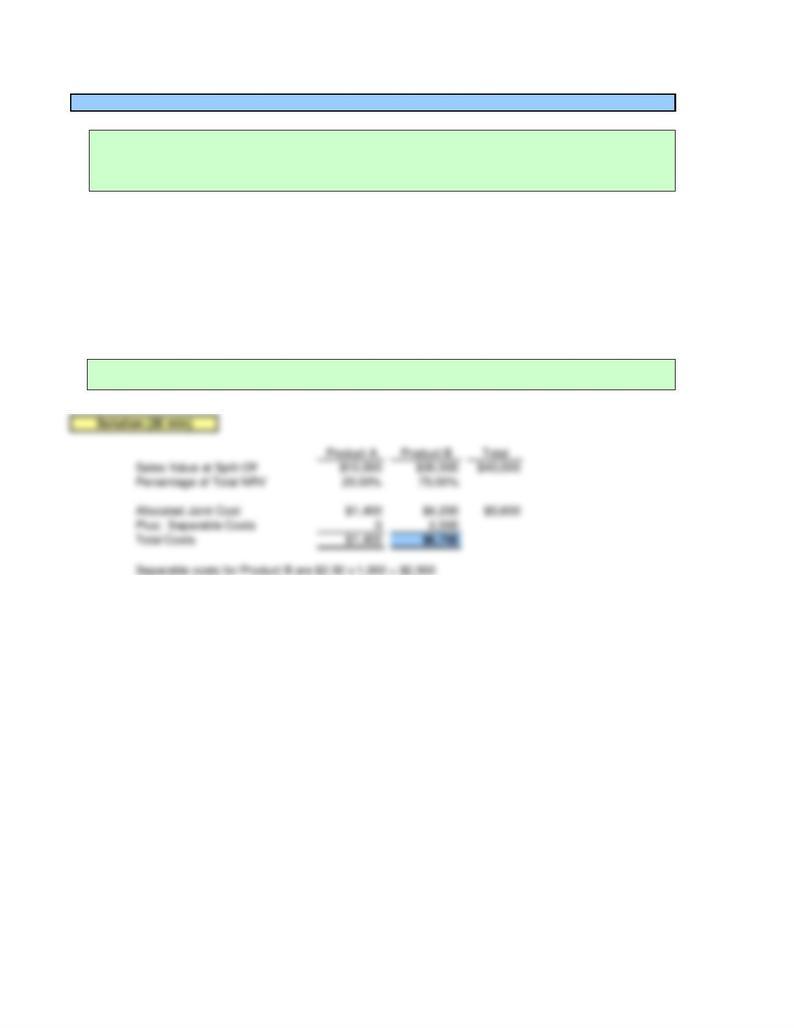

Outputs (gallons):

Product A = 5000

Product B = 1,000

Joint Costs = $5,600

Sales value at Split-off Point:

Product A = $2.00

Product B = $30.00

Separable costs per unit:

Product B = $2.50

Exercise 7-32 Joint Products

Arkansas Corporation manufactures liquid chemicals A and B from a joint process. It allocates joint costs on the

basis of sales value at split-off. Processing 5,000 gallons of product A and 1,000 gallons of product B to the split-off

point costs $5,600. The sales value at split-off is $2 per gallon for product A and $30 for product B. Product B

requires additional processing beyond the split-off point, at a cost of $2.50 per gallon, before it can be sold.

Required

What is the company’s cost to product 1,000 gallons of product B?

Output Volume:

A = 25,000

B = 20,000

C = 10,000

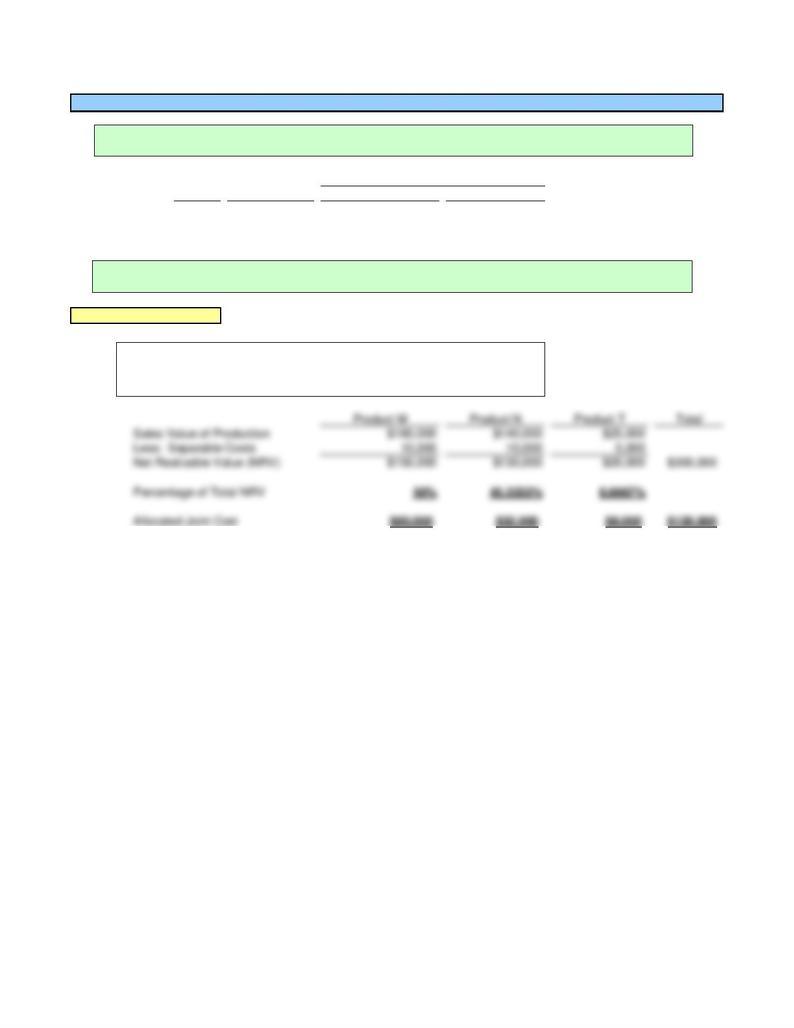

Exercise 7-33 Joint Products and By-Product Costing (Appendix)

Webster Company produces 25,000 units of A, 20,000 units of B, and 10,000 units of product C from the same

manufacturing process at a cost of $340,000. A and B are joint products, and C is regarded as a by-product. The unit

selling process of the products are $30 for A, $25 for B, and $1 for C. None of the products require additional

processing. Of the units produced, Webster Company sells 18,000 units of A, 19,000 units of B, and 10,000 units of

C. The company uses the net realizable value (NRV) method to allocate joint costs and by-product costs. Assume no

beginning inventory.

1. What is the value of the ending inventory of product A?

2. What is the value of the ending inventory of product B?

Problem 7-34 Departmental Cost Allocation; Outsourcing

Marin Company produces two software products (Cloud-X and Cloud-Y) in two separate departments (A and B).

These products are highly regarded network-maintenance programs. Cloud-X is used for small networks and Cloud-Y

is used for large networks. Williams is known for the quality of its products and its ability to meet dates promised for

software upgrades.

Department A produces Cloud-X and Department B produces Cloud-Y. The production departments are supported by

two support departments, systems design and programming services. The source and use of the support department

time are summarized below:

2. The company is considering outsourcing programming services to DDB Services, Inc., for $25.00 per hour. Should

Tanner do this?

Second Step

Sourcing

Operations Assembly Finishing

Problem 7-35 Departmental Cost Allocation; Outsourcing

Total Labor Hours Used by Dpeartments

Logan Products has two production departments – assembly and finishing. These are supported by two service

departments – sourcing (purchasing and handling of raw materials and human resources) and operations (work

scheduling, supervision, and inspection). Logan has the following labor hours devoted by each of the service departments

to the other departments:

2. What are the total costs in the production departments after allocation?

percent 8.33% 0.00% 50.00% 41.67% 100%

1. Revised cost allocation:

Production Dept.

A 115,000$ 25% 112,500$

Allocation of Total

Maintenance Cost

Outside Price

Percentage based on

Outside Price

Problem 7-36 Departmental Cost Allocation; Outsourcing

McKeoun Enterprises is a large machine tool company now experiencing alarming increases in maintenance expense in

each of its four production departments. Maintenance costs are currently allocated to the production departments on the

basis of labor-hours incurred in the production department. To provide pressure for the production departments to use

less maintenance, and to provide an incentive for the maintenance department to become more efficient, McKeoun has

decided to investigate new methods of allocating maintenance costs. One suggestion now being evaluated is a form of

outsourcing: The producing departments could purchase maintenance service from an outside supplier. That is, they

2. If McKeoun follows the proposed plan, what is likely to happen to the overall use of maintenance? How will each

department managers be motivated to increase or decrease the use of maintenance? What will be the overall

effects of going to the new plan?

2. The overall effect of the new plan will be to motivate the production

departments to continue to use the internal supplier of maintenance

when the outside price is high (as in Departments A and C), and

motivate those departments which have an opportunity to obtain

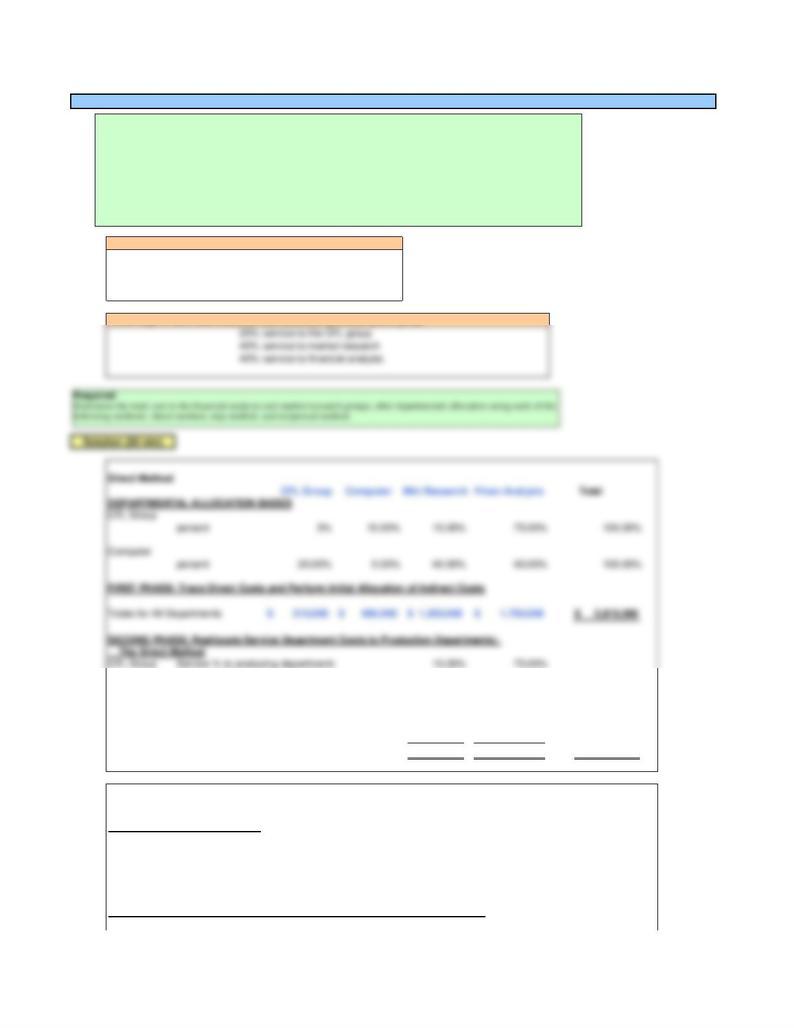

1,250,000 1,750,000

210,000 600,000

Percentage of estimated dollars of work and time by CFL:

10% service to the computer group

15% service to market research

75% service to financial analysis

Percentage of estimated dollars of work and time by the computer group:

CFL Group

15.00% 75.00%

Allocation % per the direct method 16.7% 83.3%

Allocation amount (210,000)$ 35,000$ 175,000$

Computer Service % to producing departments 40.00% 40.00%

Allocation % per the direct method 50.0000% 50.0000%

Allocation amount (600,000)$ 300,000 300,000

Totals for Production Departments 1,585,000$ 2,225,000$ 3,810,000$

Step Method

CFL Group Computer Mkt Resrch Finan Analysis Total

DEPARTMENTAL ALLOCATION BASES

CFL Group - - -

percent 10.00% 15.00% 75.00% 100%

Computer - - - - -

percent 20.00% 0.00% 40.00% 40.00% 100%

FIRST PHASE: Trace Direct Costs and Perform Initial Allocation of Indirect Costs

Support Departments

Producing Departments

Problem 7-37 Departmental Cost Allocation

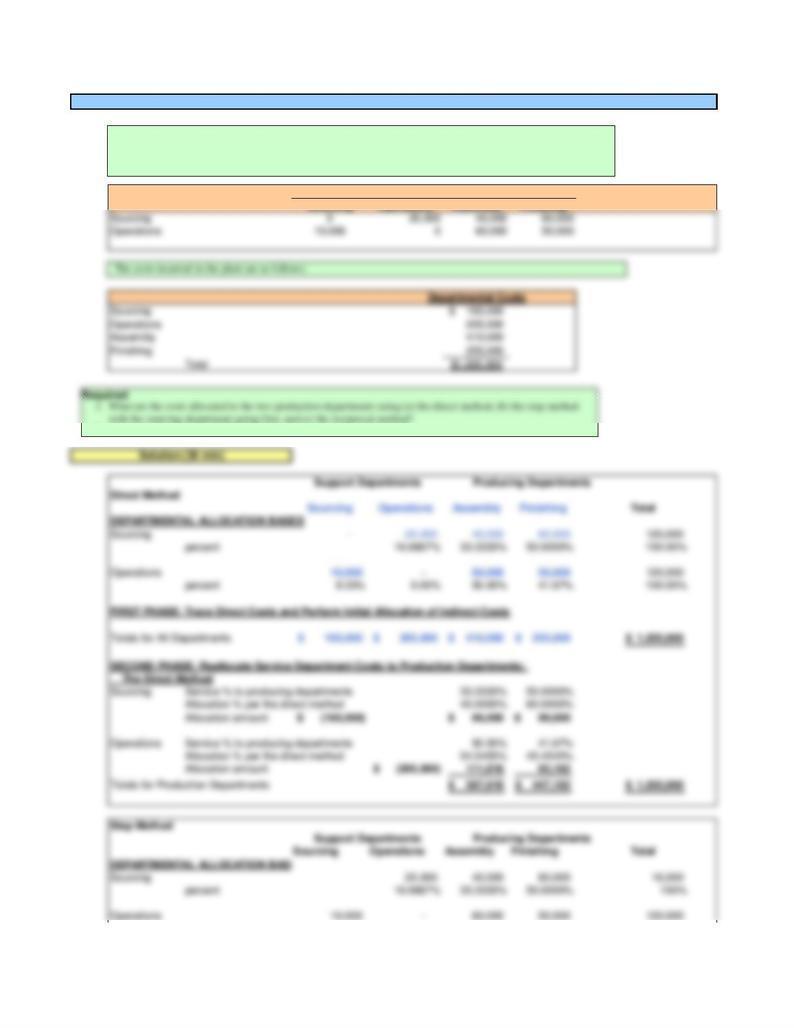

Barfield Corporation prepares business plans and marketing analysis for start-up companies in the Cleveland area.

Barfield has been very successful in recent years in providing effective service to a growing number of clients. The

company provides its service from a single office building in Cleveland, and is organized into two main client-service

groups: one for market research and the other for financial analysis. The two groups are treated as cost centers with

budgeted annual costs of $1,250,000 and $1,750,000, respectively. In addition, Barfield has a support staff that is

organized into two main functions; one for clerical, facilities, and logistical support (called the CFL group) and another

for computer-related support. The CFL group is also a cost center with budgeted annual costs of $210,000, while the

annual cost of the computer group is $600,000.

Tom Miggs, CFO of Barfield, plans to prepare a departmental cost allocation for his four groups, and he assembles the

following information:

Totals for All Departments $210,000 $600,000 $1,250,000 $1,750,000 $3,810,000

SECOND PHASE: Reallocate Service Department Costs to Production Departments:

The Step Method

First Step

Design Service % 10.00% 15.00% 75.00%

Amount (210,000) $21,000 $31,500 $157,500

Second Step

Programming Service % 40.00% 40.00%

Allocation percent per service share % 50.0000% 50.0000%

Amount ($621,000) 310,500 310,500

Totals for Production Departments $1,592,000 $2,218,000 $3,810,000

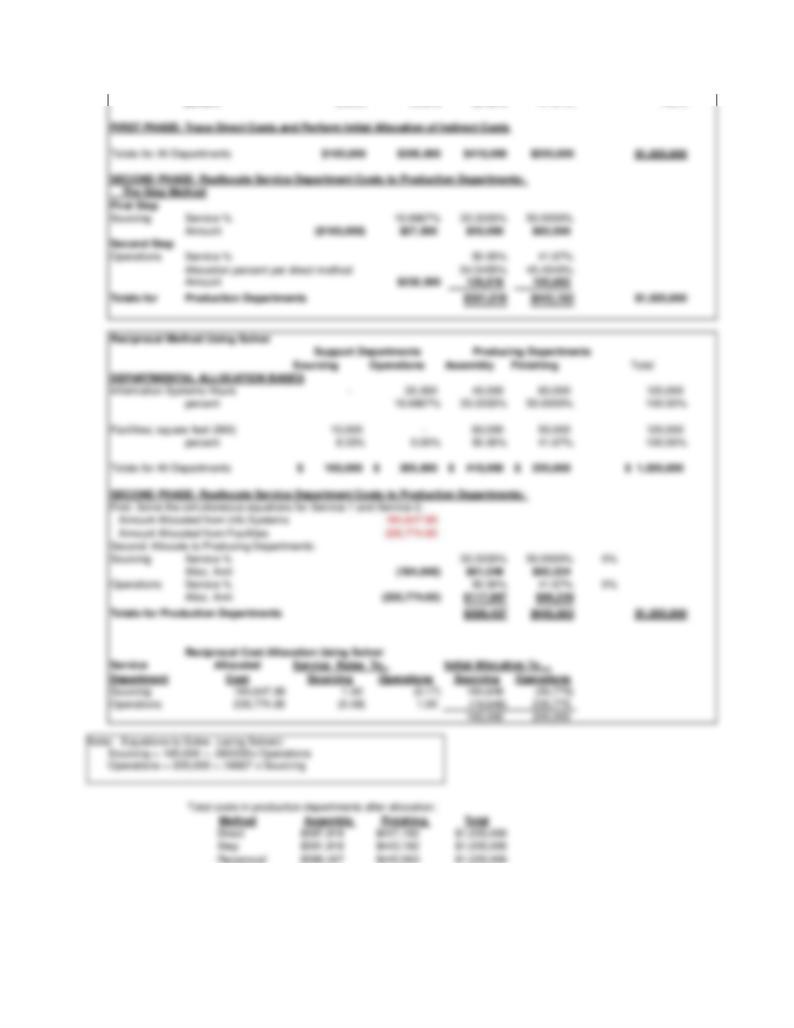

Maintenance Utilities

Overhead cost incurred $115,000

$65,000

Service provided to departments

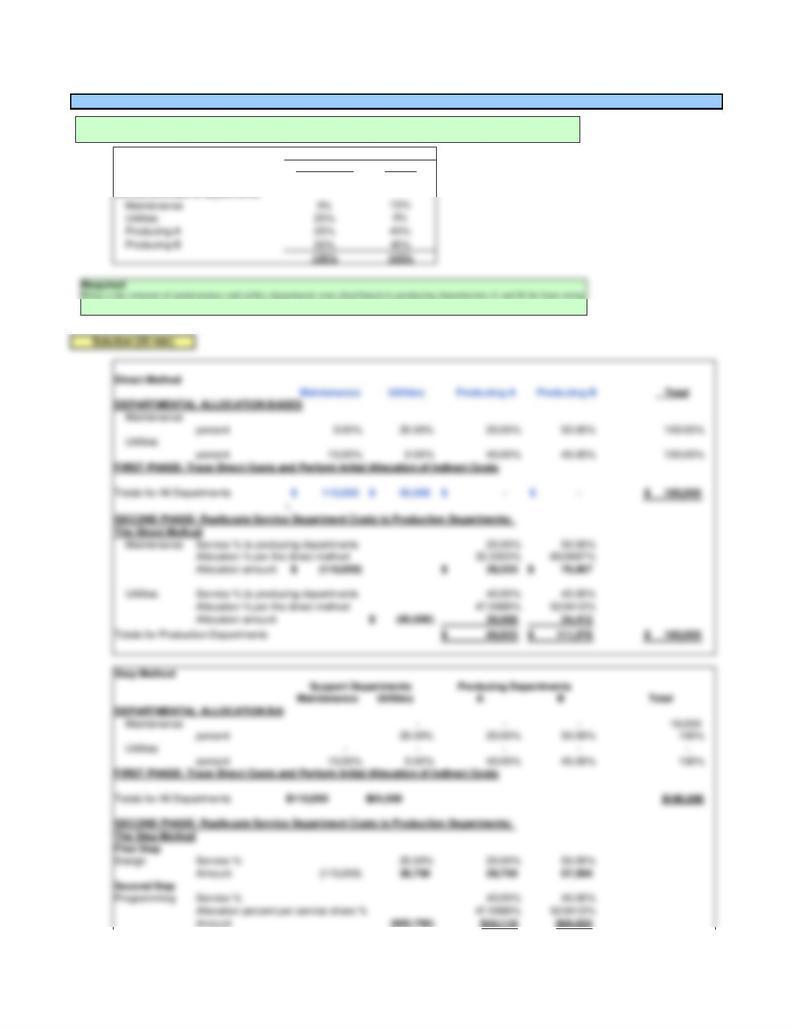

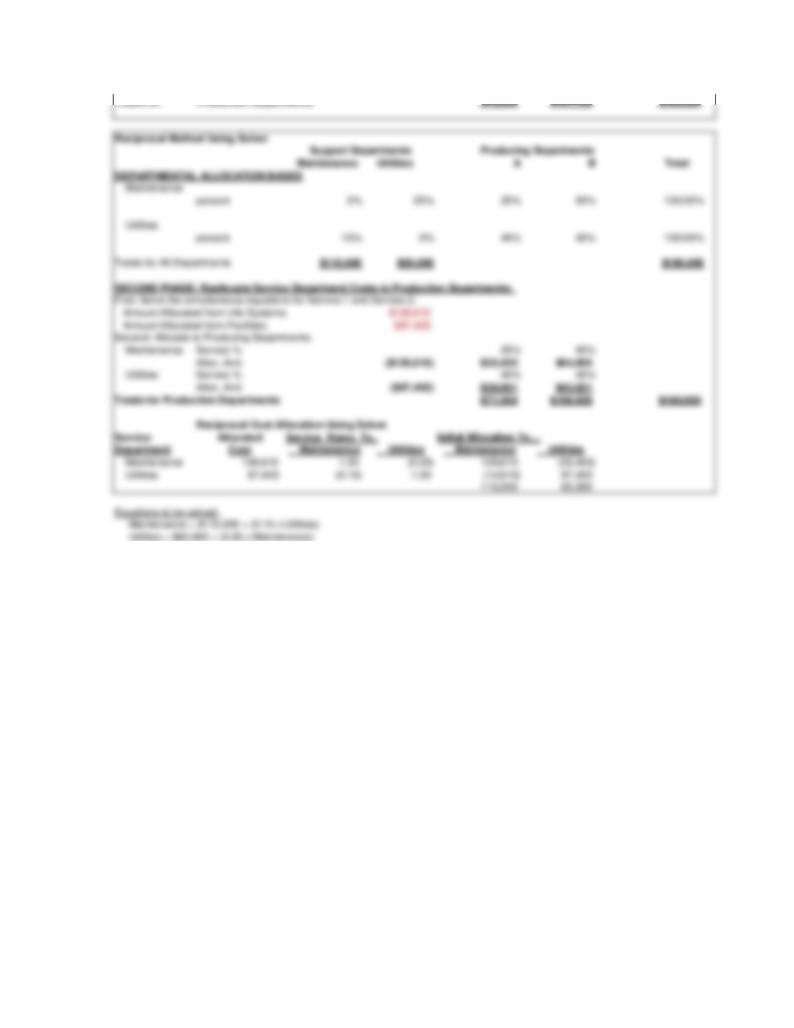

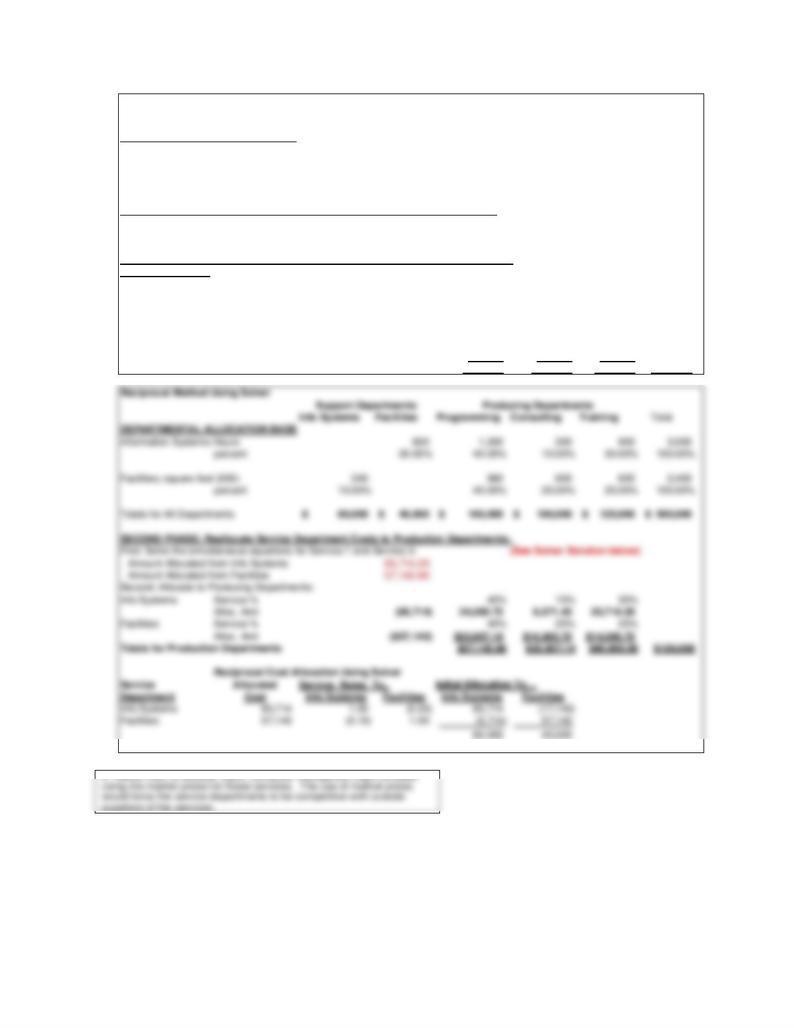

Problem 7-38 Departmental Cost Allocation

Service departments

Solexx Corporation distributes its service department overhead costs to product departments. This information is for the

month of June:

(1) the direct method, (2) the step method, and (3) the reciprocal allocation method?

Totals for Production Departments $72,868 $107,132 $180,000

Info Systems

Service % to producing departments

40.0000% 10.0000% 30.0000%

Allocation % per the direct method 50.0000% 12.5000% 37.5000%

Allocation amount ($80,000) $40,000 $10,000 $30,000

Facilities Service % to producing departments 40.00% 25.00% 25.00%

Allocation % per the direct method 44.4444% 27.7778% 27.7778%

Allocation amount ($40,000) $17,778 $11,111 $11,111

Totals for Production Departments $217,778 $211,111 $166,111 $595,000

Step Method: Information Systems Goes First

Info Systems Facilities Programming Consulting Training Total

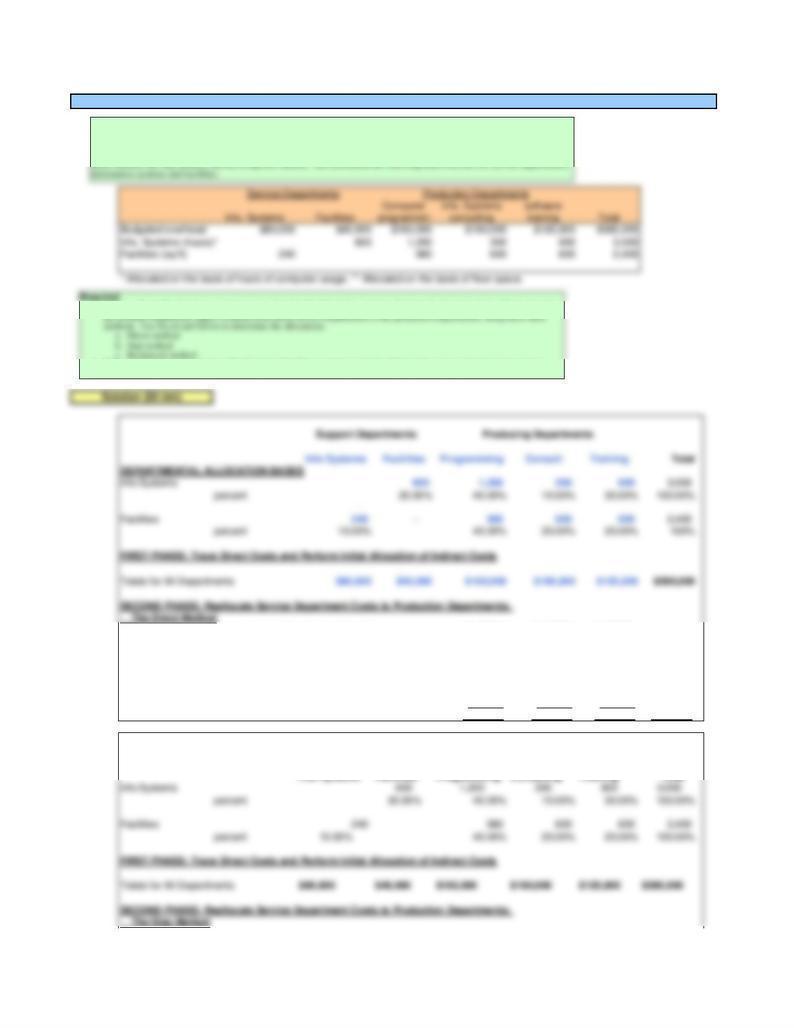

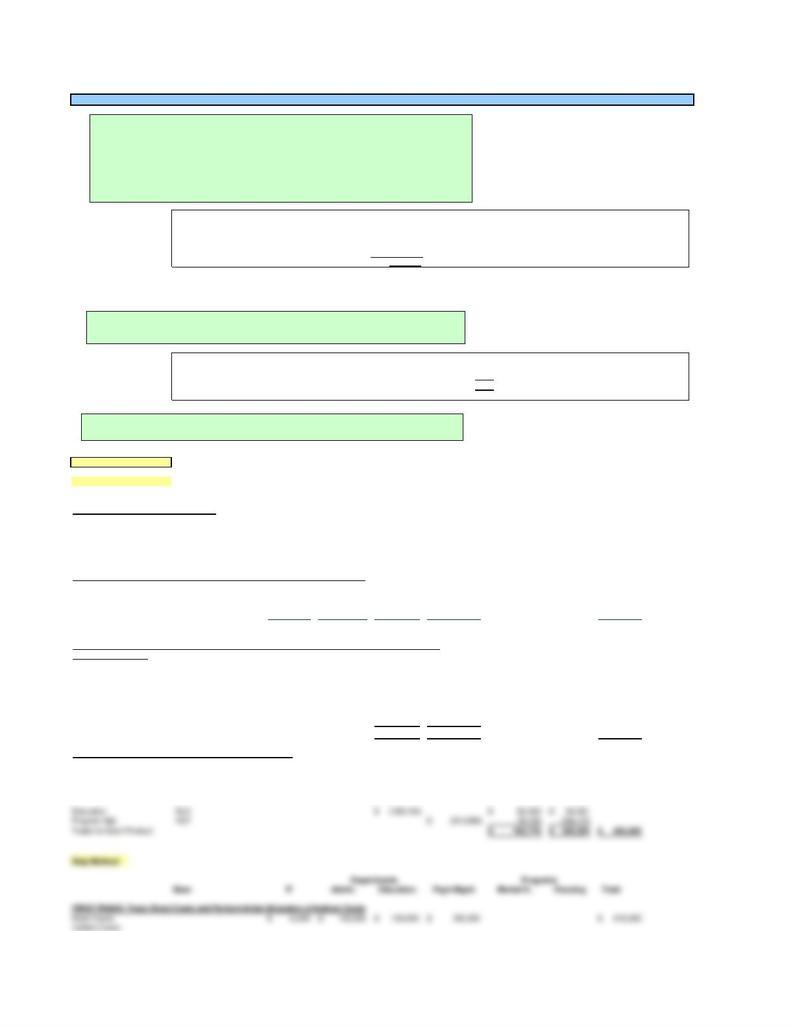

Problem 7-39 Departmental Cost Allocation

Support Departments

Producing Departments

Computer Intelligence, a computer software consulting company, has three major functional areas: computer programming,

information systems consulting, and software training. Carol Bingham, a pricing analyst in the accounting department, has been

asked to develop total costs for the functional areas. These costs will be used as a guide in pricing a new contract. In computing

these costs, Carol is considering three different methods of the departmental allocation approach to allocate overhead costs: the

1. Using as the application base computer usage time for the information systems department and square feet of floor space for

2. Rather than allocate costs, how might Computer Intelligence bet ter assign the information systems department’s costs?

First Step 20.0000% 40.0000% 10.0000% 30.0000%

Allocation percent per direct method

44.4444% 27.7778% 27.7778%

Amount ($56,000) $24,889 $15,556 $15,556

Totals for Production Departments $216,889 $213,556 $164,556 $595,000

Step Method: Facilities Goes First

Info Systems Facilities Programming Consulting Training Total

DEPARTMENTAL ALLOCATION BASES

Info Systems 600 1,200 300 900 3,000

percent 20.00% 40.00% 10.00% 30.00% 100.00%

Facilities 240 960 600 600 2,400

percent 10.00% 40.00% 25.00% 25.00% 100.00%

FIRST PHASE: Trace Direct Costs and Perform Initial Allocation of Indirect Costs

Totals for All Departments $80,000 $40,000 $160,000 $190,000 $125,000 $595,000

SECOND PHASE: Reallocate Service Department Costs to Production Departments:

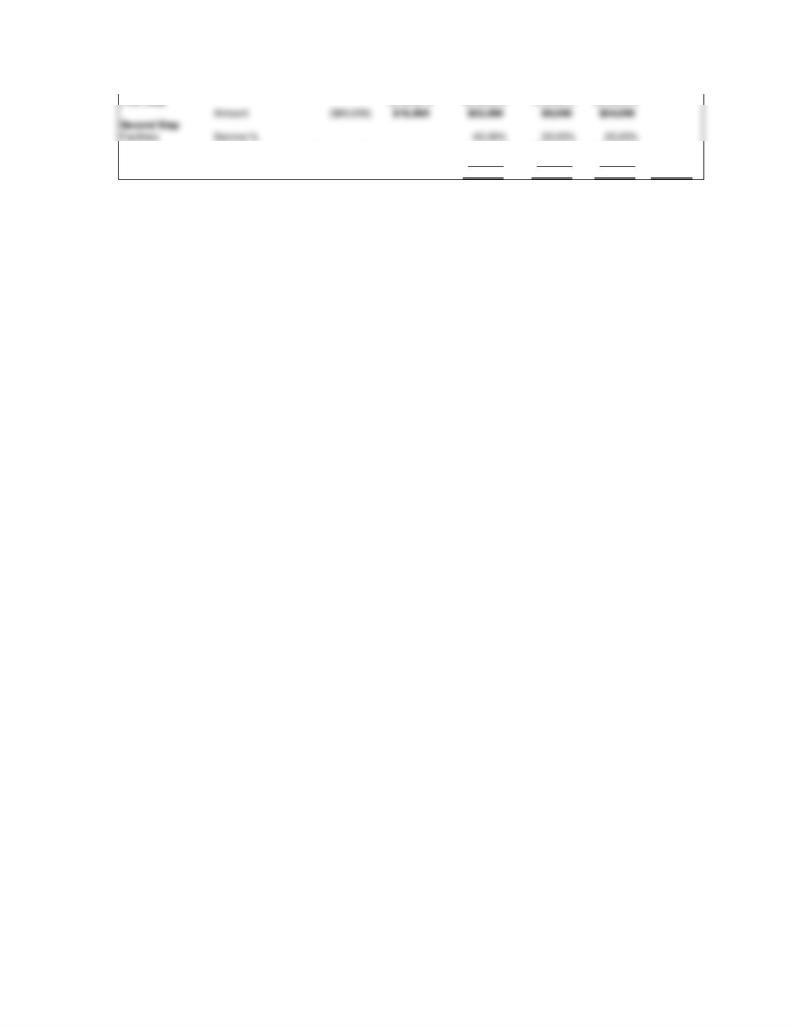

The Step Method

First Step

Facilities Service % 10% 40.00% 25.00% 25.00% 100%

Amount $4,000 ($40,000) $16,000 $10,000 $10,000

Second Step

Info Systems Service % 40.0000% 10.0000% 30.0000%

Allocation per service share % 50.0000% 12.5000% 37.5000% 100%

Amount ($84,000) $42,000 $10,500 $31,500

Totals for Production Departments $218,000 $210,500 $166,500 $595,000

Support Departments

Producing Departments

Direct Cost

Information technology $6,000

Administration $122,000

Education $100,000

Program management $190,000

$418,000

Indirect Costs:

Allocated on basis of DLHs = $50,000

Allocated on basis of headcount = $15,000

Mental health

Housing

Labor-hours in education

Headcount in program management

DIRECT METHOD

Base IT Admin Education Program Mgt Mental Health Housing

Total

DEPARTMENTAL ALLOCATION BASES

Direct Labor Hr DLH 2,000 6,000 4,000 4,000 16,000

percent 12.5% 37.5% 25.0% 25.0% 100%

Headcount HCT 2 3 3 4 12

percent 16.7% 25.0% 25.0% 33.3% 100.0%

FIRST PHASE: Trace Direct Costs and Perform Initial Allocation of Indirect Costs

Direct Costs 6,000$ 122,000$ 100,000$ 190,000$ 418,000$

Indirect Costs:

Labor DLH 6,250 18,750 12,500 12,500 50,000$

Supplies HCT 2,500 3,750 3,750 5,000 15,000$

Totals for All Departments 14,750$ 144,500$ 116,250$ 207,500$ 483,000$

SECOND PHASE: Reallocate Service Department Costs to Education and Program Mgt Departments:

The Direct Method

IT Service % to producing departments 20% 60%

Allocation % per the direct method 25.0% 75.0%

Allocation amount (14,750)$ 3,688$ 11,063$

Admin Service % to producing departments 30% 60%

Allocation % per the direct method 33.3333% 66.6667%

Allocation amount (144,500)$ 48,167 96,333

Totals for Production Departments 168,104$ 314,896$ 483,000$

THIRD PHASE: Allocate Main Department Costs to Programs

Base: Direct Labor Hours for each product 2,000 2,000 4,000

percent 50% 50%

Headcount 1 3 4

percent 25% 75%

Programs

Solution (35 min)

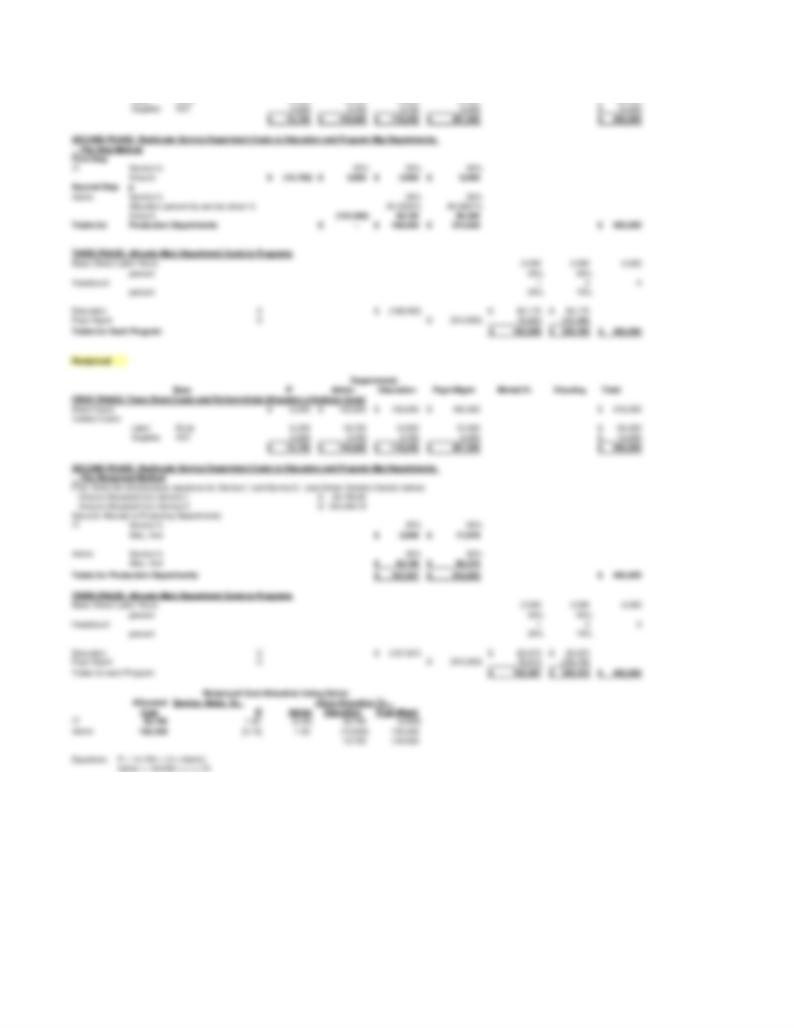

Problem 7-40 Departmental Cost Allocation; Not-for-Profit

Labor Hours

No. of Personnel

2,000

2

6,000

3

4,000

4

3

4,000

Departments

Service

Main

4

Headcount

2,000

1

2,000

Labor Hours

4,000

3

The Fleming Foundation is a charitable organization founded by Gaylord Fleming and Sandy Fleming. The Flemings

intended for the charity to provide programs in health care for the elderly, particularly those in poverty. The two main

program divisions of the foundation are mental health for the elderly and housing for the elderly. In addition to these

programs, the Foundation also provides health care educational programs and has a significant fund-raising effort to help the

Foundation to grow and to accomplish the goals of the founders. The foundation is organized into two main departments –

education and program management. These departments are supported by two service departments – information technology

(IT) and administration.

There are $418,000 of costs directly traceable to each of the four departments. An additional $65,000 of indirect costs

are shared among the four departments - $50,000 of which is allocated to the departments based on direct labor-hours and

$15,000 to the departments based on the number of personnel (headcount) in the departments.

The cost, labor-hours, and headcount in these departments in the most recent year are as follows:

The costs of the two main departments (Education and Program Management) are allocated to the two programs (Mental

Health and Housting) as follows: the costs in education are allocated on the basis of labor-hours in the programs, while the

costs in program management are allocated using the headcount used in the two programs. The following table shows the

labor hours and headcount consumption by the two programs.

Required

Determine the costs allocated to the mental health and housing programs using the direct method, the step method (assuming

that IT goes first), and the reciprocal method.

Labor DLHs 6,250 18,750 12,500 12,500 50,000$

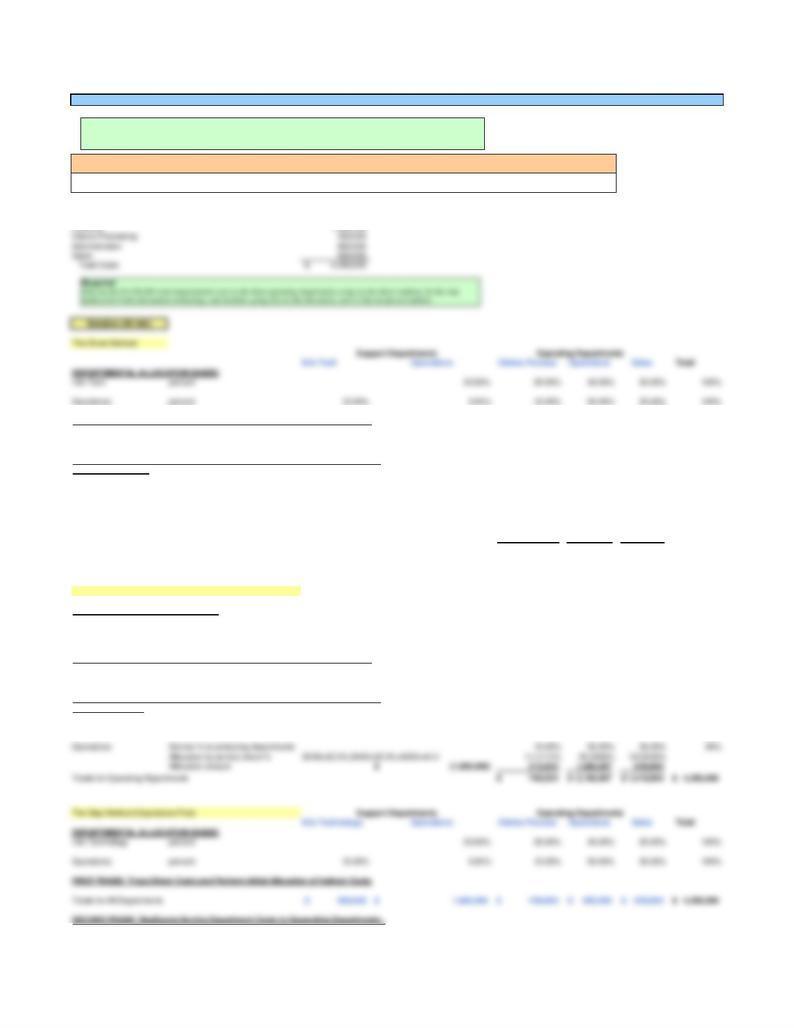

Info. Tech Operations Claims Proc. Administration Sales

Information Technology 20% 20% 40% 20%

Facilities 10% 10% 50% 30%

The total costs incurred in the five departments are:

Information Technologies 600,000$

Facilities 1,800,000

0.3

FIRST PHASE: Trace Direct Costs and Perform Initial Allocation of Indirect Costs

Totals for All Departments 600,000$ 1,800,000$ 450,000$ 850,000$ 650,000$ 4,350,000$

SECOND PHASE: Reallocate Service Department Costs to Operating Departments:

The Direct Method

Info Tech Service % to producing departments 20.00% 40.00% 20.00% 80%

Allocation % per the direct method 30/70=42.86%;20/70=28.57 25.0000% 50.0000% 25.0000%

Allocation amount (600,000)$ 150,000$ 300,000$ 150,000$

Operations Service % to producing departments 10.00% 50.00% 30.00% 90%

Allocation by service share % 20/90=22.22%;40/90=44.44%;30/90=33.33% 11.1111% 55.5556% 33.3333%

Allocation amount (1,800,000)$ 200,000 1,000,000 600,000

Totals for Operating Departments 800,000$ 2,150,000$ 1,400,000$ 4,350,000$

The Step Method (Info Tech First)

Info Technology Operations Claims Process Operations Sales

Total

DEPARTMENTAL ALLOCATION BASES

Info Technology percent 20.00% 20.00% 40.00% 20.00% 100%

Operations percent 10.00% 0.00% 10.00% 50.00% 30.00% 100%

FIRST PHASE: Trace Direct Costs and Perform Initial Allocation of Indirect Costs

Totals for All Departments 600,000$ 1,800,000$ 450,000$ 850,000$ 650,000$ 4,350,000$

SECOND PHASE: Reallocate Service Department Costs to Operating Departments:

The Step Method

Info Technology Service % to producing departments 20% 20% 40% 20% 100%

Allocation amount (600,000)$ 120,000$ 120,000$ 240,000$ 120,000$

Operating Departments

Support Departments

Problem 7-41 Departmental Cost Allocation; Insurance Company

Support Departments

Operating Departments

Comprehensive Insurance Company has two service lines, health insurance and auto insurance. The two product lines are served

by three operating departments which are necessary for providing the two types of services: claims processing, administration, and

sales. These three operating departments are supported by two departments: information technology and operations. The support

provided by information technology and operations to the other departments is shown below.

The Step Method

0.3

FIRST PHASE: Trace Direct Costs and Perform Initial Allocation of Indirect Costs

Totals for All Departments 600,000$ 1,800,000$ 450,000$ 850,000$ 650,000$ 4,350,000$

SECOND PHASE: Reallocate Service Department Costs to Operating Departments:

First: Solve the simultaneous equations for service 1 and service 2

Amount allocated from info systems

795,918.37

Amount allocated from facilities

1,959,183.67

Second: Allocate to Producing Departments

Smooth Skin =

$2.40 per gallon

Silken Skin = $3.90 per gallon

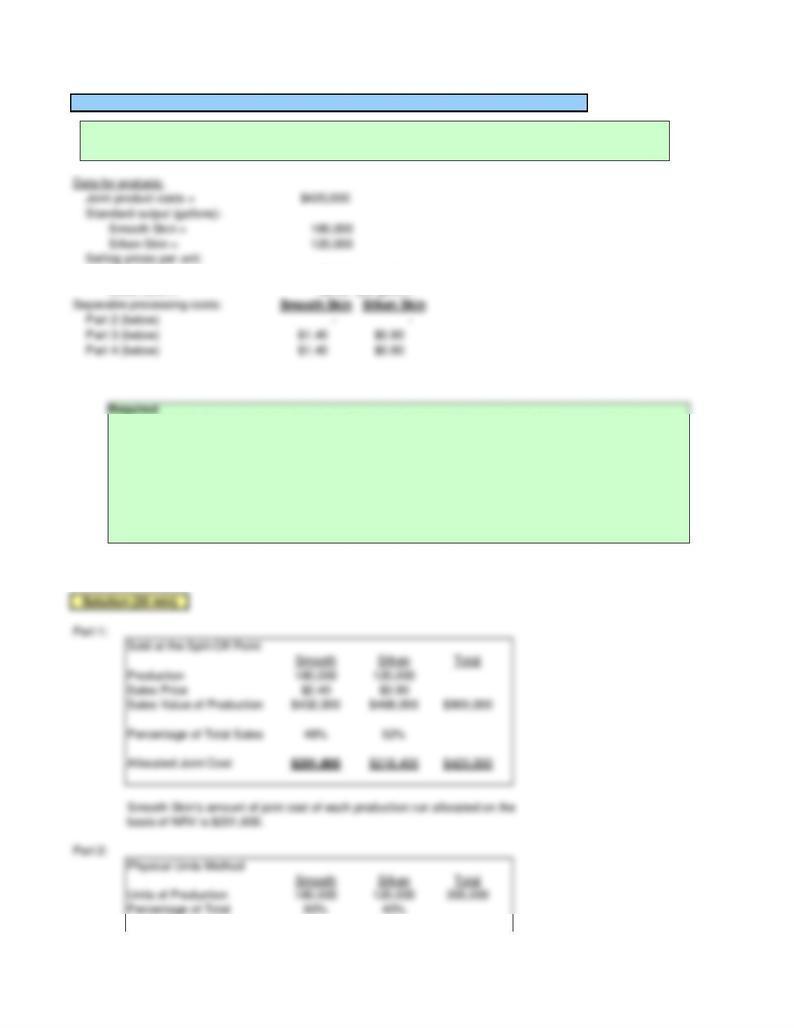

Problem 7-42 Joint Product Costing

Choi Company manufactures two skin care lotions, Smooth Skin and Silken Skin, from a joint process. The joint

costs incurred are $420,000 for a standard production run that generates 180,000 gallons of Smooth Skin and 120,000

gallons of Silken Skin. Smooth Skin sells for $2.40 per gallon, while Silken Skin sells for $3.90 per gallon.

1. Assuming that both products are sold at the split-off point, how much of the joint cost of each production run is

allocated to Smooth Skin on the sales value basis?

2. If not additional costs are incurred after the split-off point, how much of the joint cost of each production run is

allocated to Silken Skin on the physical measure method basis?

3. If additional processing costs beyond the split-off point are $1.40 per gallon for Smooth Skin and $0.90 per gallon for

Silken Skin, how much of the joint cost of each production run is allocated to Silken Skin on a net realizable value

basis?

4. If additional processing costs beyond the split-off point are $1.40 per gallon for Smooth Skin and $0.90 per gallon for

Silken Skin, how much of the join cost of each production run is allocated to Smooth Skin on a physical measure

method basis?

Allocated Joint Cost $252,000 $168,000 $420,000

Data for analysis:

Joint costs, standard production run = $450,000

Output (units), standard production run:

MSB = 80,000

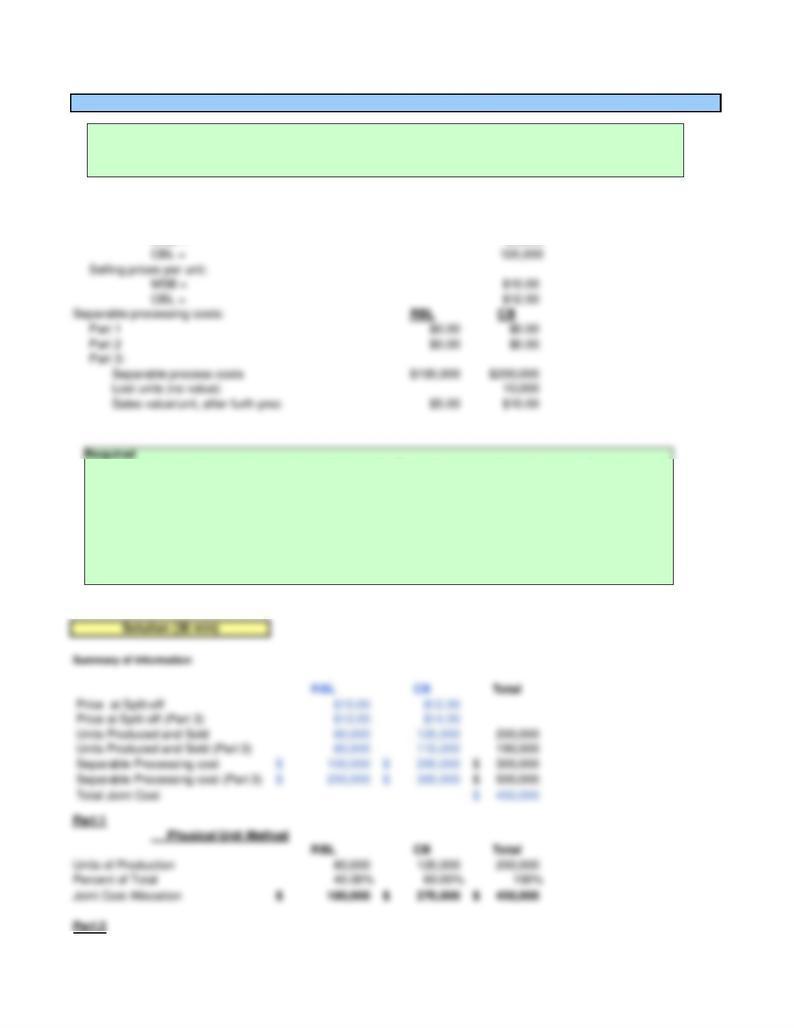

Problem 7-43 Joint Product Costing

Northwest Building Products (NBP) manufactures two lumber products from a joint milling process: residential

building lumber (RBL) and commercial building lumber (CB) A standard production run incurs joint costs of

$450,000 and results in 80,000 units of RBL and 120,000 units of CB. Each RBL sells for $10.00 per unit and each

CB sells for $12.00 per unit.

1. Assuming that no further processing occurs after the split-off point, how much of the joint costs are allocated to

commercial lumber (CB) on a physical measure method basis?

2. If not further processing occurs after the split-off point, how much of the joint cost is allocated to the mine support

braces (RBL) on a sales value basis?

3. Assume that the CB is not marketable at split-off but must be planed and sized at a cost of $300,000 per production

run. During the process, 10,000 units are unavoidably lost and have no value. The remaining units of CBL are

salable at $14 per unit. The RBL, although salable immediately at the split-off point, are coated with a tarlike

preservative that costs $200,000 per production run. The braces are then sold for $12 each. Using the net realizable

value basis, how much of the completed cost should be assigned to each unit of CBL?

4. Should NBP choose to process the RBL beyond split-off? What would be the contribution if it did so?

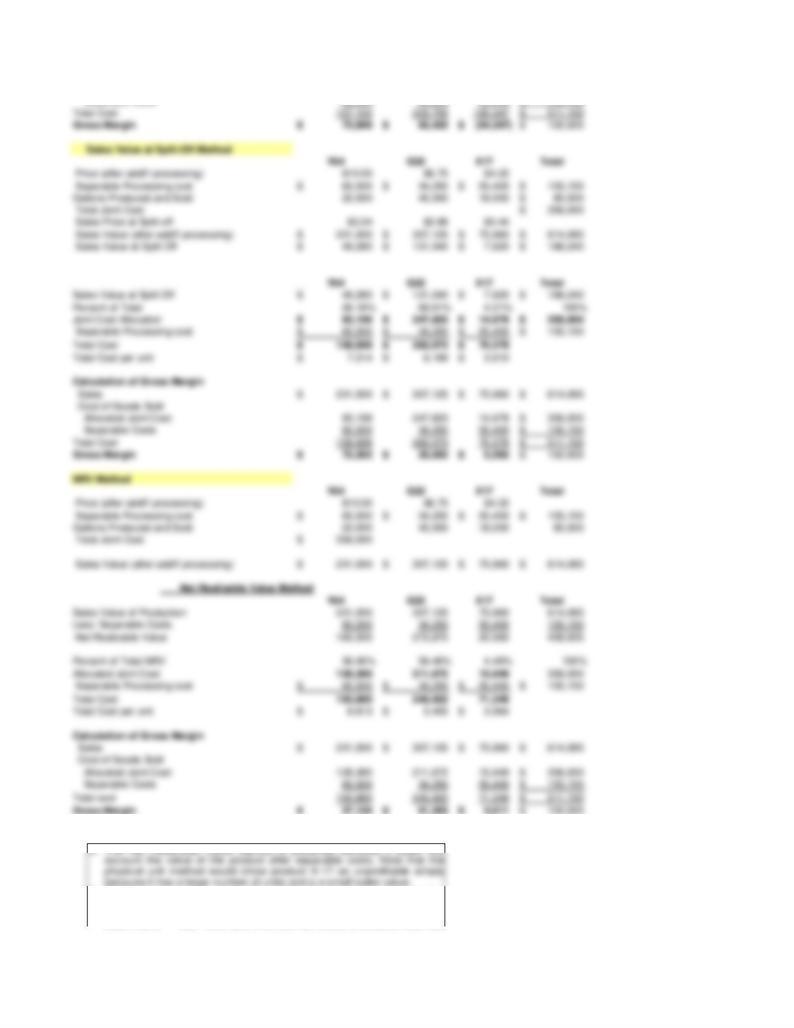

Sales Value Method RBL CB Total

Problem 7-44 Joint Products

The Salinas Company produces three products, X, Y, and Z, from a joint process. Each product can be sold at the split-

off point or processed further. Additional processing requires no special facilities, and the production costs of further

processing are entirely variable and traceable to the products involved. Last year all three products were processed

3. Should the firm sell any of its products after further processing?

4. Salinas has been selling all of its products at the split-off point. Selling any of the products after further processing

will entail direct competition with some major customers. What strategic factors does the firm need to consider in

deciding whether to process any of the products futher?

Unit Gross Profit $1.6000 $0.8167 -$1.4000

A101 A204 B216 Total

Units Sold 175,000 135,000 115,000 425,000

Price (after addt'l processing) 14.00$ 10.00$ 12.00$

Separable Processing cost 550,000 125,000 625,000 1,300,000$

Units Produced 175,000 135,000 115,000 425,000

Total Joint Cost 3,500,000

Sales Price at Split-off 10.00 5.00 10.00

Sales Value (after addt'l processing) 2,450,000 1,350,000 1,380,000 5,180,000

Sales Value at Split Off 1,750,000 675,000 1,150,000 3,575,000

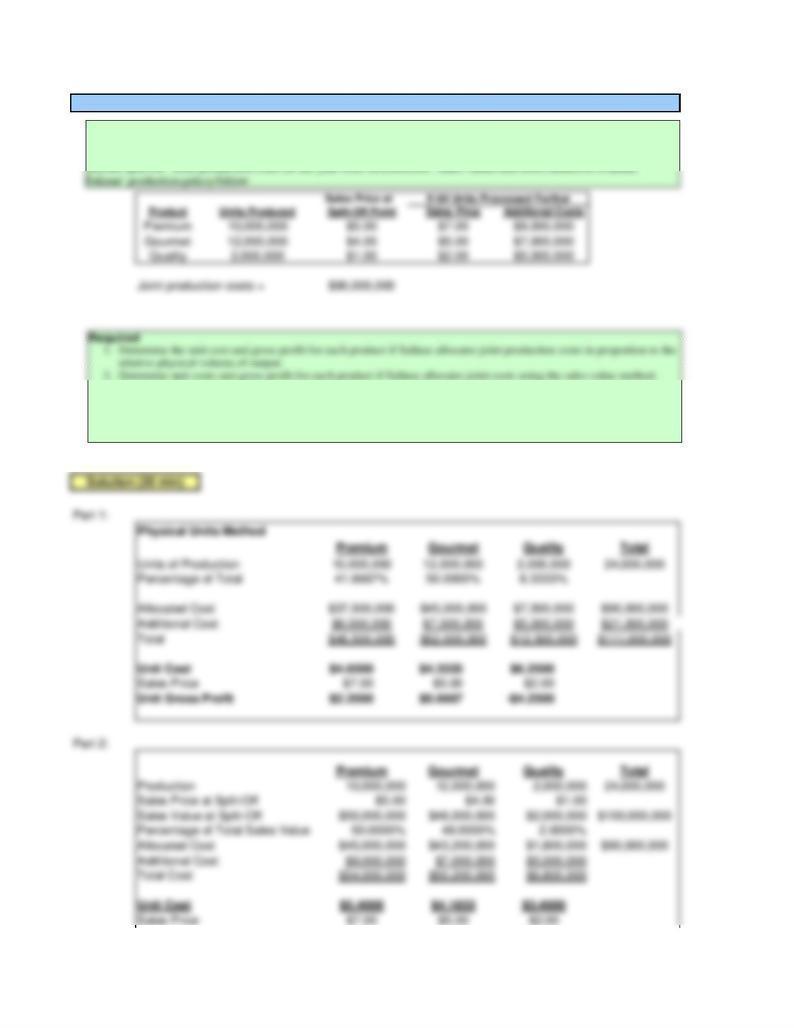

(a) Physical Unit Method

A101 A204 B216 Total

Units of Production 175,000 135,000 115,000 425,000

Percent of Total 41.18% 31.76% 27.06% 100%

Joint Cost Allocation 1,441,176$ 1,111,765$ 947,059$ 3,500,000$

Separable Processing cost 550,000 125,000 625,000 1,300,000

Total Cost 1,991,176$ 1,236,765$ 1,572,059$ 4,800,000$

Total Cost per unit 11.3782$ 9.1612$ 13.6701$

Calculation of Gross Margin

Sales 2,450,000$ 1,350,000$ 1,380,000$ 5,180,000$

Cost of Goods Sold

Allocated Joint Cost 1,441,176 1,111,765 947,059 3,500,000$

Separable Costs 550,000 125,000 625,000 1,300,000$

Total Cost 1,991,176$ 1,236,765$ 1,572,059$ 4,800,000$

Gross Margin 458,824$ 113,235$ (192,059)$ 380,000$

Sales Value at Split Off Method - Data A101 A204 B216 Total

Units Sold 175,000 135,000 115,000 425,000

Price (after addt'l processing) 14.00$ 10.00$ 12.00$

Separable Processing cost 550,000$ 125,000$ 625,000$ 1,300,000$

Units Produced 175,000 135,000 115,000 425,000

Total Joint Cost 3,500,000$

Sales Price at Split-off 10 510

Sales Value (after addt'l processing) 2,450,000$ 1,350,000$ 1,380,000$ 5,180,000$

Problem 7-45 Joint Products

Solution (20 min)

Johnston Adhesives Company makes three widely used industrial adhesives: A101, A204, and B216. See sales and production

information for a gallon of each of the three adhesives in the following table. Most of Johnston’s customers ask for a special

blend of the three products which improves heat resistance. The additional processing requires additional time and materials,

and the price is increased accordingly, as shown in the table. Assume that Johnston produces only for specific customer orders,

2. Which of the four methods do you think would be preferred in this case? Why?

Sales Value at Split Off 1,750,000$ 675,000$ 1,150,000$ 3,575,000$

(b) Sales Value at Split-Off Method

A101 A204 B216 Total

Sales Value at Split Off 1,750,000$ 675,000$ 1,150,000$ 3,575,000$

Percent of Total 48.9510% 18.8811% 32.1678% 100%

Joint Cost Allocation 1,713,287$ 660,839$ 1,125,874$ 3,500,000$

Separable Processing cost 550,000$ 125,000$ 625,000$ 1,300,000$

Total Cost 2,263,287$ 785,839$ 1,750,874$ 4,800,000$

Total Cost per unit 12.933$ 5.821$ 15.225$

Calculation of Gross Margin

Sales 2,450,000$ 1,350,000$ 1,380,000$ 5,180,000$

Cost of Goods Sold

Allocated Joint Cost 1,713,287 660,839 1,125,874 3,500,000$

Separable Costs 550,000 125,000 625,000 1,300,000$

Total Cost 2,263,287 785,839 1,750,874 4,800,000$

Gross Margin 186,713$ 564,161$ (370,874)$ 380,000$

A101 A204 B216 Total

2. In this case the net realizable value method should be preferred because

all Johnston’s production is processed further, and the NRV method

Problem 7-46 Joint Products; By-Products (Appendix)

Multiproduct Corporation is a chemical manufacturer that produces two main products (Pepco-1 and Repke-3) and a by-

product (SE-5) from a joint process. If Multiproduct had the proper facilities, it could process SE-5 further into a main

product. The ratio of output quantities to input quantity of direct material used in the joint process remains consistent with

the processing conditions and activity level. Multiproduct currently uses the physical measure method of allocating joint

costs to the main products. It uses the first-in, first-out (FIF) inventory method to value the main products. The by-product is

inventoried at its net realizable value, which is used to reduce the joint production costs before they are allocated to the main

products. Jim Simpson, Multiproduct’s controller, wants to implement the sales value method of joint cost allocation. He

believes that inventory costs should be based on each product’s ability to contribute to the recovery of joint production costs.

The net realizable value of the by-product would be treated in the same manner that the physical method would. Data

1. The relative sales value method of joint cost allocation assigns cost in

proportion to each product's sales value to the sales value of all products.

If there is no sales value at split-off, then the value at the first sales point

less separable costs is used. If joint products have a sales value at the

split-off point, the margin for all joint products at the split-off point will be

2. a. Because both main products have a market value at the split-off

point, this value is used to allocate the joint cost rather than the final sales

value.

Joint production costs to be allocated $2,640,000

Less net realizable value of by product $120,000

Joint costs to be allocated $2,520,000

SE-5 $120,000

November joint production costs $2,640,000

Pepco-1 Repke-3 SE-5

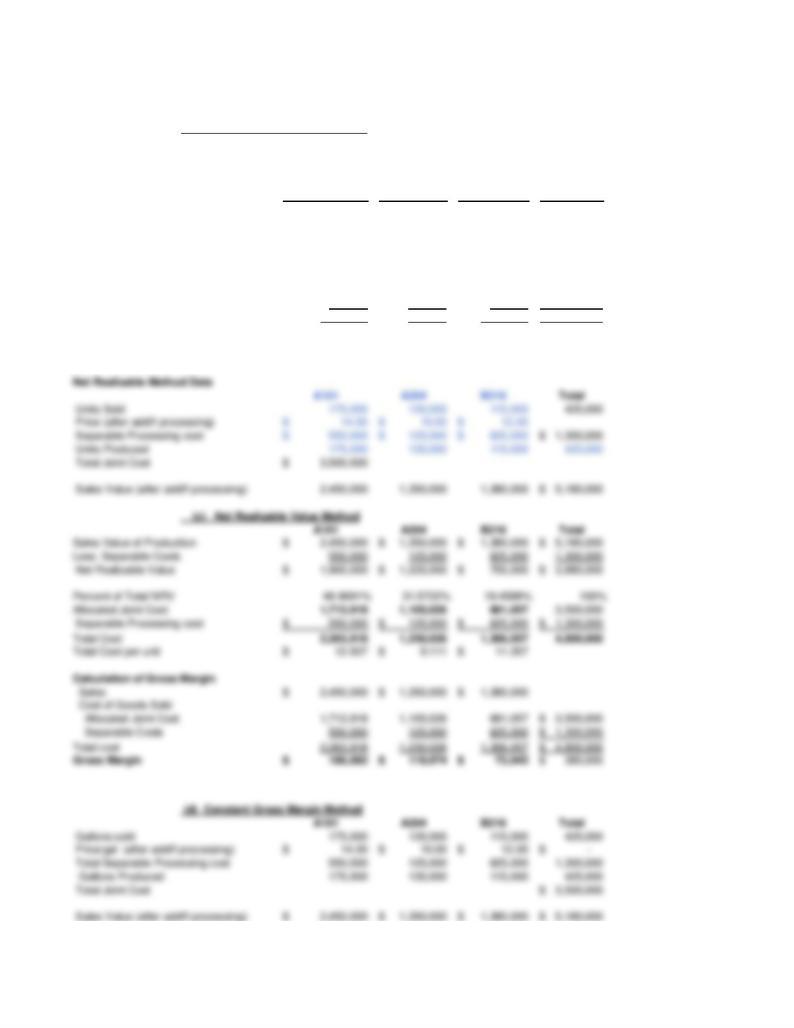

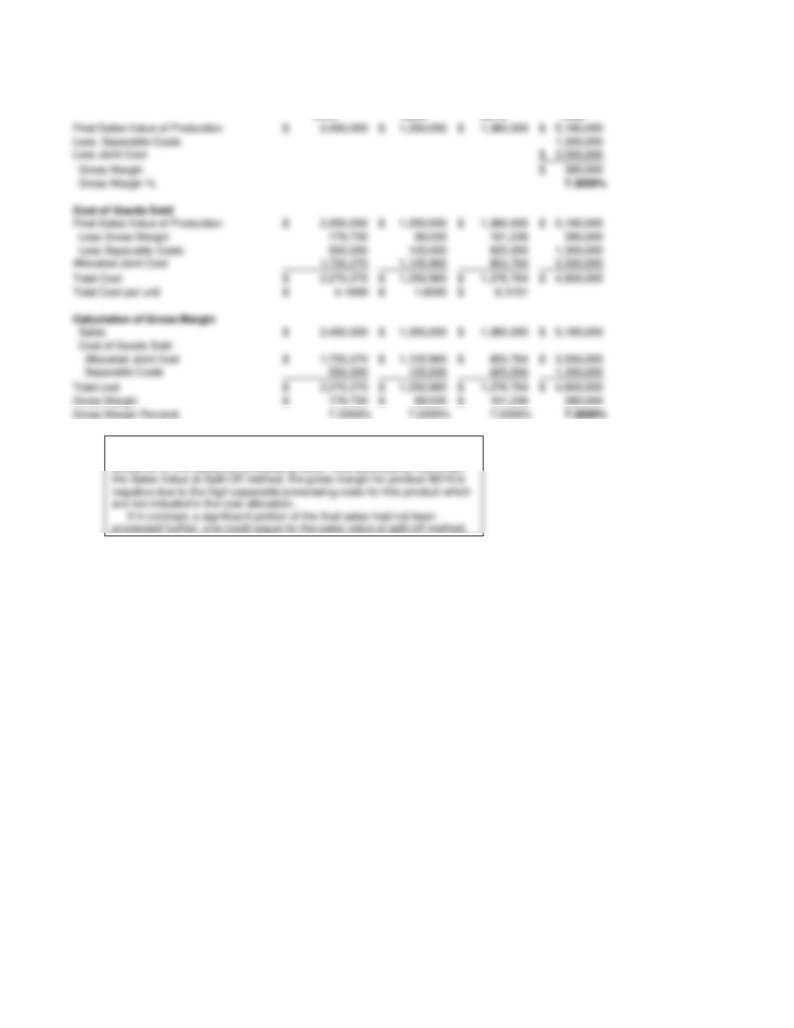

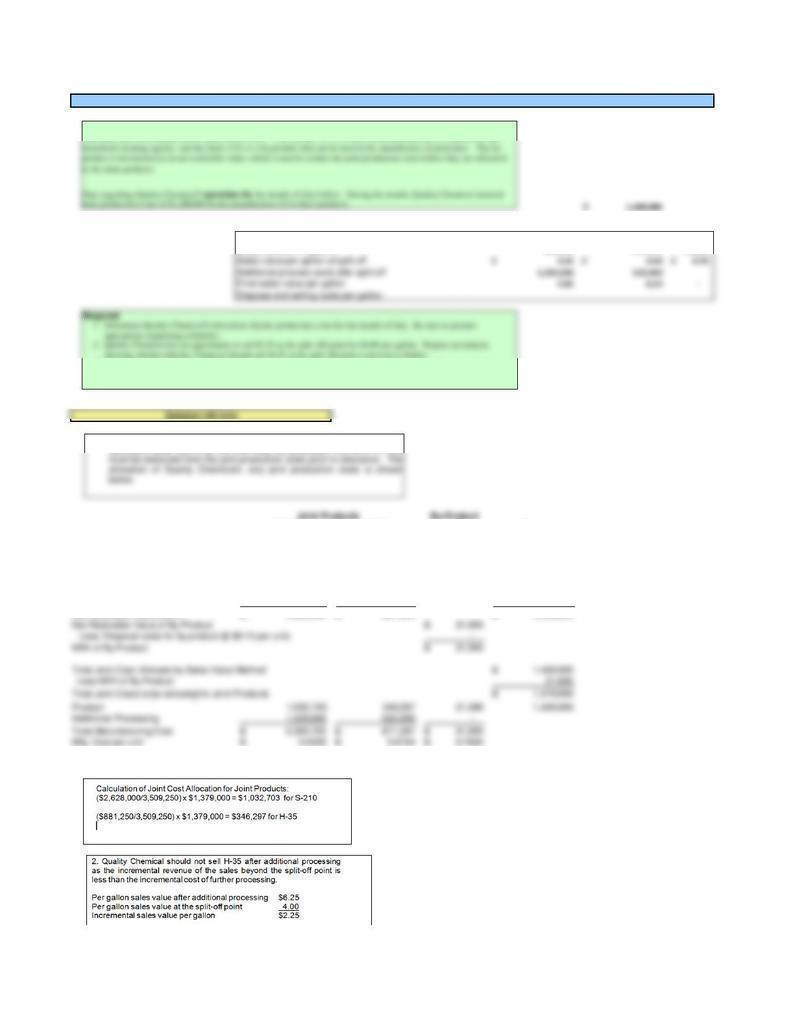

S-210 H-35 J-23

July sales in gallons 600,000 225,000 20,000

July production in gallons 660,000 225,000 30,000

S-210 H-35 J-23 Total

Units Sold 600,000 225,000 20,000 845,000

Units Produced 660,000 225,000 30,000 915,000

Final Sales Price 5.85$ 6.25$ 0.70$

Sales Value of By-Product 21,000$

Final Sales Value of Joint Products 3,861,000$ 1,406,250$ 5,267,250$

Additional Processing Costs 1,233,000 525,000 - 1,758,000

Net Realizable Value (NRV) 2,628,000$ 881,250$ 3,509,250$

Problem 7-47 Joint Products

Quality Chemicals manufactures three chemicals for industrial and retail customers. The largest volume product, S-210, is a

sweetener used in the preparation of processed foods. The second, H-35, is used in the manufacture of commercial and

3. As a production supervisor for Quality Chemical, you have learned that small quantities of the critical chemical

compound in H-35 might be present in S-210. What should you do?

1. Because by-products are assigned an inventory cost equal to their net

Summary of Recent Month's Activity Ying Yang Bit

Units Sold 50,000 40,000 10,000

Units Produced 50,000 40,000 10,000

Additional Processing Costs - Variable 140,000$ 42,000$ -$

Additional Processing Costs - Fixed 10,000$ 8,000$ -$

Sales Price 6.00$ 12.50$ 1.60$

Total Joint Cost 265,000$ ($115,000 variable)

By-Product

Ying Yang Bit Total

Units Sold 50,000 40,000 10,000 100,000

Units Produced 50,000 40,000 10,000 100,000

Separable Processing Costs - Variable 140,000$ 42,000$ -$ 182,000$

Separable Processing Costs - Fixed 10,000 8,000 - 18,000

Problem 7-48 Joint Products; By-Products (Appendix)

Solution (40 min)

Joint Products

2. Calculate the gross margin for each product

Problem 7-49 Joint Products

Yonica Petroleum is a global manufacturer of specialty chemicals which are made from the waste products of the petroleum

industry. Yonica in effect recycles a good portion of the waste from the refineries used by the large oil companies. The specialty

chemicals are used as cleaning solvents and lubricants in industrial applications. Yonica has three products -- Y64, G22 and X17

1. Calculate the product cost of each of the three product lines using the following methods:

2. Which of the three methods do you think would be preferred in this case? Why?

3. While Yonica chose to process all three products beyond the split-off point, do you think this is the correct

decision? Which products, if any, do you think should have been processed beyond the split-off point, and

4. Since Yonica is involved in the recycling of waste chemicals, it is able to purchase its raw materials at

greatly reduced cost. However, its manufacturing costs are slightly higher than some of its competitors

5. What are some of the global issues that Yonica should consider in effectively executing its strategy?

6. What should Yonica do, if anything, to improve the overall effect of its operations on the environment?

Separable Costs 65,500 34,250 55,400 155,150$

3. The increase in sales value after additional processing cost is greater

than the additional processing costs for all three products, so that

Yonica has the correct policy in processing all products to the final

3. The increase in sales value after additional processing cost is greater

than the additional processing costs for all three products, so that

Yonica has the correct policy in processing all products to the final

4. Yonica’s strategy is based on environmentally friendly policies, and

the odds are that the company’s customers will increasingly seek out

companies, like Yonica, that produce environmentally friendly

5. The key global issues for Yonica include the strategic decisions

6. Yonica has a good position in sustainability because the company’s

Problem 7-50 Joint Cost Allocation: Managerial Incentives

Cameron Manufacturing produces auto parts for auto manufacturers and parts wholesalers. The business is very competitive, and

productivity measures are used throughout its eight manufacturing plants. Jill Owens, the manufacturing vice president, explains to

her plant managers the importance of reducing cycle time, improving throughput, and reducing waste. One type of waste she keeps

close track of is that due to accidents and injuries on the job. Jill believes that a safe work place also contributes to productivity. A

reduction in accidents and injuries can also lead to a reduction in the insurance the firm pays to cover its liability in these incidents.

The premium for this insurance coverage is a single policy and is a joint cost shared by all eight plants. One of the plant managers,

Mike Griffin, notes that the current procedure for allocating the cost of insurance, which is based on the total plant output, does not

provide plant managers with the desired incentive to reduce accidents. It just means that the larger plants get charged more. Mike

suggests that the insurance cost should be charged to the plants based on the number of manufacturing personnel in each plant.

Required

What do you think of Mike’s suggestion? What alternative would you suggest, if any, for allocating the cost of insurance to the

plants?