4–1 What is the strategic role of a costing system?

4-4 Companies that are likely to use a job costing system have a wide variety

4–5 Which costing system is extensively used in the service

4–6 What document is prepared to accumulate costs for each

4-7 The determination of a predetermined overhead rate has four steps: (1)

estimate the factory overhead costs for an appropriate operating period,

usually a year, (2) select the most appropriate cost driver(s) for applying the

factory overhead costs, (3) estimate the total amount or activity level of the

4–8 What is the role of material requisition forms in a job costing

system? Time tickets? Bills of materials?

4–9 What does the statement that accounting for overhead

4-9 Since the overhead cost cannot be traced directly to a particular product, we need

a good costing system, which can assign overhead accurately to specific

products. Generally speaking, the more expensive or extensive a costing

4-10 Costs originate with the purchase of materials. These direct materials

4–11 What do underapplied overhead and overapplied overhead

mean? How are these amounts disposed of at the end of a period?

4-11 Underapplied overhead is the amount of actual factory overhead that

exceeds the factory overhead applied. Overapplied overhead is the amount

4-11 Underapplied overhead is the amount of actual factory overhead that

exceeds the factory overhead applied. Overapplied overhead is the amount

4–12 Why would manufacturing firms switch from direct labor-

hours to machine-hours as the cost driver for factory overhead

application?

4–14 Distinguish between an actual costing system and a normal

costing system. What are the components of the actual manufacturing

costs and the components of the normal manufacturing costs?

4–15 What is the best way to choose an appropriate cost driver when

applying factory overhead?

4–16 What is the difference between normal and abnormal spoilage?

Brief Exercises 4-17 through 4-28

4-17 How is job costing different in a service firm from a manufacturer?

4-20 If the overhead rate is $10 per machine hours, and there are 20 labor hours, 16

machine hours, and 2 personnel on the job, how much overhead should be applied

to the job?

4-19 Nieto Machine Shop has 4,000 labor hours and 8,000 machine hours used in May.

Total budgeted overhead for May is $40,000. What is the overhead rate using labor

hours and also using machine hours? Which would you pick and why?

4-18 A small consulting firm has an overhead rate of 200% of direct labor charged to

each job. The materials cost (including travel and other direct costs) for a

particular job is $10,000 and the direct labor is $20,000. What is total job cost

for this job?

4-21 Some firms pool overhead into a single plant wide overhead pool, while others

collect overhead costs into manufacturing departments, each of which has an

overhead cost pool and overhead cost application rate. Which approach is likely to

provide more accurate cost numbers for cost estimating, pricing, and performance

evaluation?

200,000$

222,000$

15,000$

43,000$

20,000$

50,000$

350,000$

360,000$

22,000$

650,000$

30,000$

700,000$

4-22 Basic Job Costing Assume the

following for White Top, Inc, for the

current year. White Top applies

overhead on the basis of units

produced.

Budgeted overhead

Actual overhead

Actual labor hours

Actual number of units sold

Underapplied overhead

Budgeted production

Required How many units were produced in

the current year?

4-22

4-23 Assume the following for Round Top, Inc.,

for the current year. Round Top applies

overhead on the basis of units produced.

Budgeted overhead

Actual overhead

Actual labor-hours

Actual number of units sold

Overapplied overhead

Budgeted production (units)

Required How many units were produced in in

the current year?

4-23

The information on units sold and the number of labor hours is

0.50$ per unit

4-26 If actual overhead is $613,000 in a given year and the overhead rate is $10

per unit, 60,000 units were sold, and 59,000 units were produced. For the

end of the year, is overhead underapplied or overapplied, and a by how

much?

4-24 Company A has a number of jobs that are processed through similar

manufacturing processes. However, most jobs have labor hours

requirements ranging from 100 to 130 hours, while these jobs differ

significantly in the number of machine hours required for each job –

some as low as 50, other as high as 5,000 hours. One reason for this

is a well trained labor pool that has the ability to work cross-

functionally, and perform a variety of duties. What do you think is the

best overhead rate basis for this firm, labor hours, machine hours, or

some other rate basis? Explain your answer.

4-24 Because of the greater variability of machine hours among jobs, job cost

will be more strongly influenced by the use of machine hours. The fact that

4-25 What are the three types of potential error in overhead application?

4-23

The information on units sold and the number of labor hours is

4-28 When overhead is overapplied, is the balance of cost of good sold, before

adjustment, too low or too high? Why?

1. New Century Software, Inc @ http://www.newcenturysoftware.com/

The goal of New Century Software, Inc. is to provide products and services to help meet the facilities-based

information needs of the pipeline industry through the use of Geographic Information Systems (GIS),

Automated Mapping and Facilities Management (AM/FM) software.

The company's Windows-based software products provide an integrated approach to GIS

implementation and augment the functionality of leading GIS packages.

Based in Colorado, the company has assisted in the development of GIS for pipeline companies in the

United States by providing facilities database consulting, data conversion services, and integrated software

applications.

2. FedExOffice @ http://www.fedex.com

FedExOffice is a provider of a variety of office and business services such as copying and printing.

The company uses job costing.

1. The following is a list of websites for a number of large companies. Briefly describe each company and

3. TXI Cement @ http://www.txi.com/

TXI Cement has a history in the cement industry of 90 years. They are one of only two companies in the USA that

produces white cement. TXI Cement is constantly trying to be energy efficient, by generating electricity, and using

alternate energy and raw materials sources. Distribution of products is done via two cement plants in Southern

California as well as terminals in San Diego and Stockton. TXI is one of the largest bagged cement producers in

the USA.

Cement is a finely ground, manufactured mineral product that when combined with water, sand, gravel and other

materials forms concrete, the most widely used construction material in the world.

The company uses process costing.

Reasons:

High volume, low cost product.

It is not economically feasible to keep track of the detailed cost elements applied to each unit of production (the

bag of cement).

TXI is largely a domestic company because its product is expensive to transport. The company’s operations are

primarily in Texas (production) and California (sales). TXI’s product is a highly environmentally sensitive

1. New Century Software, Inc @ http://www.newcenturysoftware.com/

The goal of New Century Software, Inc. is to provide products and services to help meet the facilities-based

information needs of the pipeline industry through the use of Geographic Information Systems (GIS),

Automated Mapping and Facilities Management (AM/FM) software.

The company's Windows-based software products provide an integrated approach to GIS

implementation and augment the functionality of leading GIS packages.

Based in Colorado, the company has assisted in the development of GIS for pipeline companies in the

United States by providing facilities database consulting, data conversion services, and integrated software

applications.

2. FedExOffice @ http://www.fedex.com

FedExOffice is a provider of a variety of office and business services such as copying and printing.

The company uses job costing.

Reasons:

Costs can be precisely calculated by the basis of the different jobs. Each package has a specific

TXI is largely a domestic company because its product is expensive to transport. The company’s operations are

primarily in Texas (production) and California (sales). TXI’s product is a highly environmentally sensitive

product, and the company’s Web site explains the efforts it makes on the production side of the business to

manage the environmental impact. From the TXI Web site:

“TXI offers one of the most eco

-friendly and cleanest options to address the issue of ready-mix concrete

construction waste. This is a major piece of the construction process that has been historically difficult to manage

–

where does one put all that waste concrete? TXI has developed a unique solution to this decades-long

4. Paramount Pictures @ http://www.paramount.com/

Paramount pictures, the motion picture production company, is a unit of Viacom, a large company in the

entertainment industry with such labels as MTV Films, Nickelodeon Movies, and DreamWorks Studios. It

offers an array of choices in the form of movies, TV shows, and musical entertainment.

The company uses job costing.

5. Coca-Cola: http://www.coca-cola.com/

Coca-Cola is the world’s most recognized brand, a significant global company with more than 400 different

beverage brands produced and sold in more than 200 countries.

1. Zurich Financial Services Group: www.zurich.com

The Zurich Financial Services Group is a global leader in the financial services industry, providing

its customers with solutions in the area of financial protection and asset accumulation. The Group

concentrates its activities in five business segments: non-life and life insurance, reinsurance,

2. Reichhold Chemical Company: http://www.reichhold.com/

Reichhold is a large manufacturer of chemical products including coatings (epoxy, acrylic and

other resins), latex (in a joint venture with Dow Chemical Company), and composites (gelcoats and

resins used in the manufacture of fiberglass products including boats, bathroom fixtures, and other

1. The following is a list of websites for a number of global companies. Briefly describe each company and

3. Nestle S.A.: www.nestle.com

Nestle is one of the leading food companies in the world. Its product portfolio includes brands such

as Perrier, Poland Springs, Nescafe, Lean Cuisine, Alpo, Butterfinger, and Kit Kat. The whole food

production process is a continuous high

-volume one and so will have a process costing system.

4. Evian @

http://www.evian.com/

Evian Natural Spring Water is bottled exclusively at its source in Evian

-les-Bains located in the

French Alps. Filled, sealed bottles are then shipped to over 120 countries throughout the world.

Evian spring water is perfect by

nature. Naturally pure and fresh, it is not artificially treated or processed in any way. Its unique

source in the heart of the French Alps guarantees Evian natural spring waters remarkable purity.

1. Zurich Financial Services Group: www.zurich.com

The Zurich Financial Services Group is a global leader in the financial services industry, providing

its customers with solutions in the area of financial protection and asset accumulation. The Group

concentrates its activities in five business segments: non-life and life insurance, reinsurance,

2. Reichhold Chemical Company: http://www.reichhold.com/

Reichhold is a large manufacturer of chemical products including coatings (epoxy, acrylic and

other resins), latex (in a joint venture with Dow Chemical Company), and composites (gelcoats and

resins used in the manufacture of fiberglass products including boats, bathroom fixtures, and other

The fact that Evian is a global company is clear from its Web site. The sustainability issues for Evian

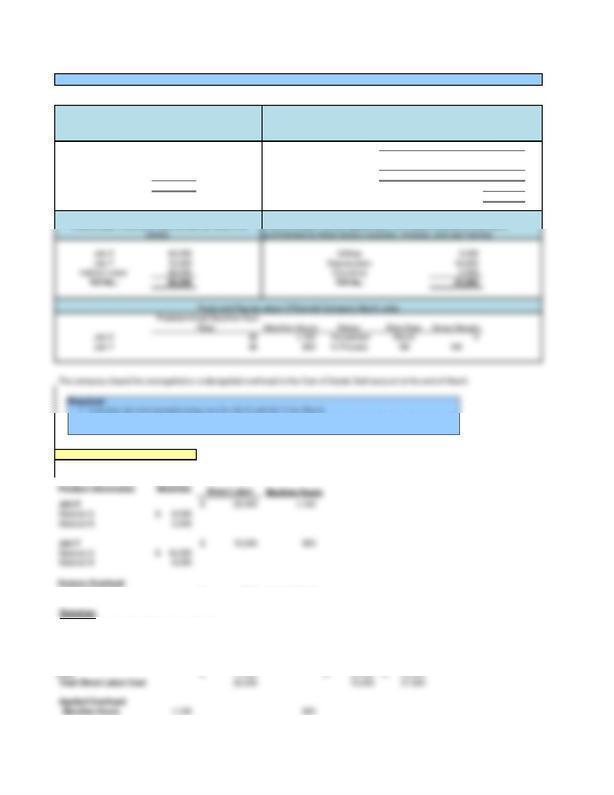

Exercise 4-31 Cost Flows, Applying Overhead

Erkens Company uses a job costing system with normal costing and applies factory overhead on the basis of

machine-hours. At the beginning of the year, management estimated that the company would incur $1,980,000 of

factory overhead costs and use 66,000 machine-hours.

Carlson Company recorded the following events during the month of April:

a. Purchased 180,000 pounds of materials on account; the cost was $5.00 per pound.

2. Journal Entries:

a. Materials Inventory 900,000

Accounts Payable 900,000

180,000 x $5 = $900,000

b. Work-in-Process Inventory 525,000

($600,000 - $75,000)

Factory Overhead 75,000

(15,000 x $5)

Materials Inventory (120,000 x$5) 600,000

c. Work-in-Process Inventory 240,000

2. Journal Entries:

a. Materials Inventory 900,000

Accounts Payable 900,000

180,000 x $5 = $900,000

b. Work-in-Process Inventory 525,000

($600,000 - $75,000)

Factory Overhead 75,000

(15,000 x $5)

Materials Inventory (120,000 x$5) 600,000

c. Work-in-Process Inventory 240,000

Factory Overhead 40,000

Accrued Payroll 280,000

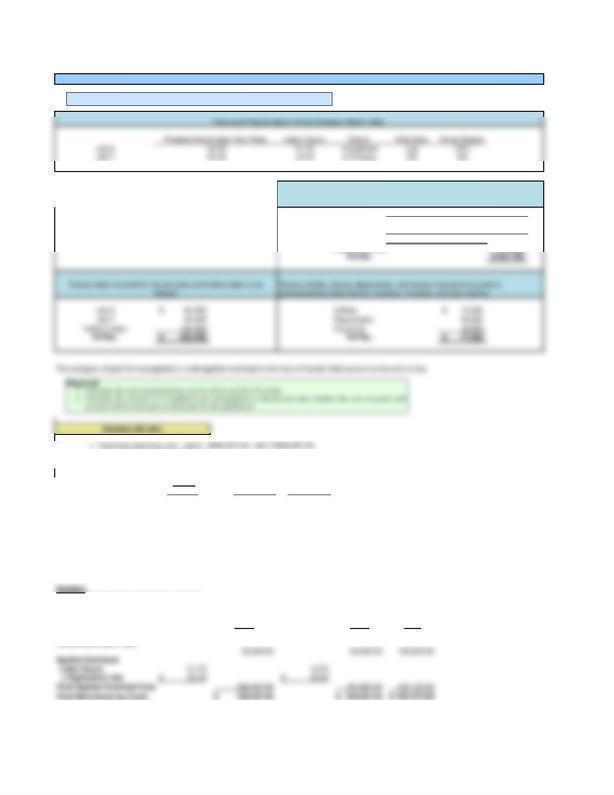

3. Actual factory overhead:

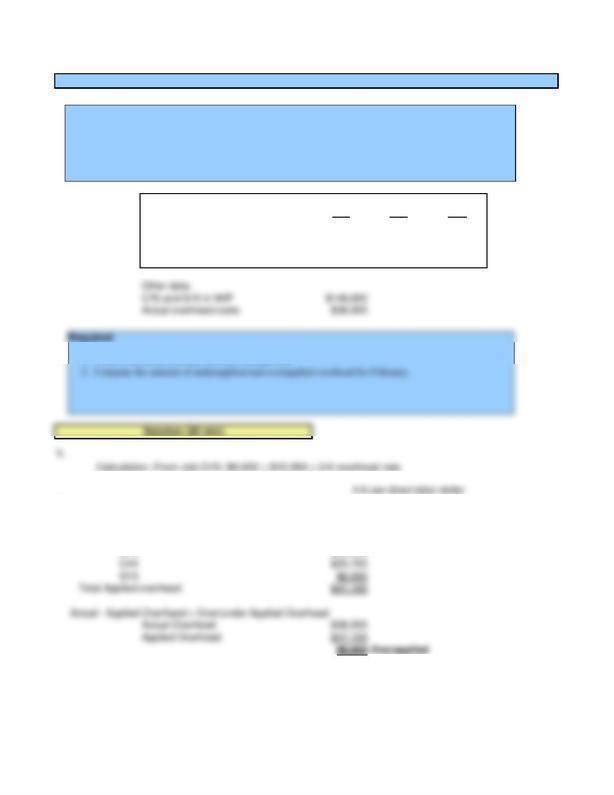

B10 C44 G15

Direct labor ($8/hour) $34,000 ? $10,000

Direct materials $42,000 $61,000 ?

Overhead applied ? $20,750 $6,000

2.

Applied overhead for B10 = .6x $34,000 = $20,400

Total applied overhead in February:

B10 $20,400

Exercise 4-32 Application of Overhead; Working with Unknowns

Job Number

Alles Company uses a job costing system that applies factory overhead on the basis of direct labor. No job

was in process on February 1. During the month of February, the company worked on these three jobs.

During the month, the company completed and transferred Job B10 to the finished goods inventory. Jobs

C44 and G15 were not completed and remain in work in process at the cost of $148,650 at the end of the

month. Actual factory overhead costs during the month totaled $38,500

1. What is the predetermined factory overhead rate?

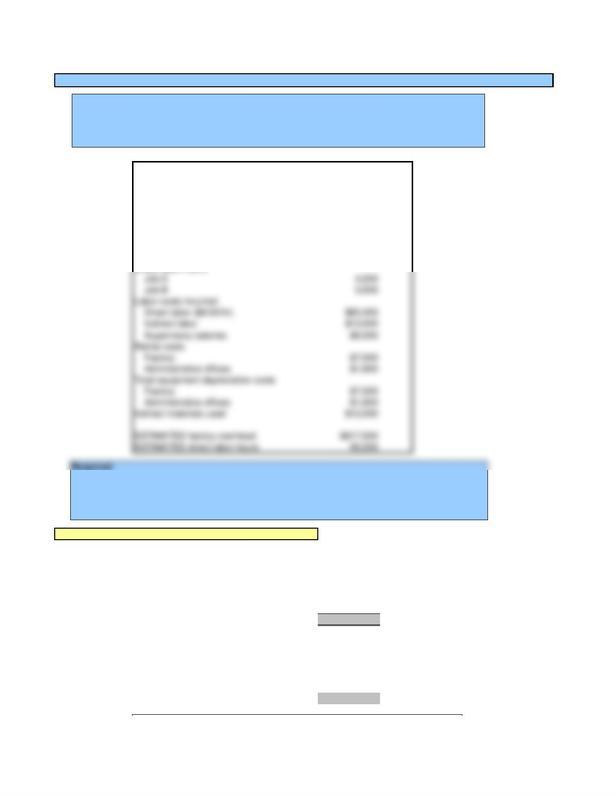

September 1, inventories

Materials inventory $7,500

Work-in-process inventory (All Job A) $31,200

Finished goods inventory $67,000

Material purchases $104,000

Direct material requisitioned

Job A $65,000

Job B $33,500

Direct labor-hours

What is the total Cost of Job A? Labor rate= $8.50

September Direct materials requisitioned 65,000$

September Direct labor cost 35,700

September Applied overhead 27,300

September 1 Work-in-process 31,200

TOTAL Cost Job A 159,200$

predetermined OH rate = $617,500/95,000 $6.50

What is the total factory overhead applied during September?

September Applied Overhead $50,050

Solution (30 min)

Exercise 4-33 Application of Overhead

Total overhead cost applied during September:

Applied Overhead = total direct labor-hours x overhead rate

= (4,200 + 3,500) x $6.50 = $50,050

Johnson Inc. is a job-order manufacturing company that uses a predetermined overhead rate based on direct

labor-hours to apply overhead to individual jobs. For the current year, estimated direct labor-hours are

95,000, and estimated factory overhead is $617,500. The following information is for September of the

current year. Job A was completed during September, and Job B was started but not finished.

1. What is the total Cost of Job A?

2. What is the total factory overhead applied during September?

3. What is the overapplied or underapplied overhead for September?

What is the overapplied or underapplied overhead for September?

Total overhead cost applied during September:

Applied Overhead = total direct labor-hours x overhead rate

= (4,200 + 3,500) x $6.50 = $50,050

Exercise 4-34 Application of Overhead

Whitley Construction Company is in the home remodeling business. Whitley has three teams of highly-skilled employees, each of

whom has multiple skills of carpentry, painting, and other home remodeling activities. Each team is led by an experienced e

mpl

oyee

who coordinates the work done on each job. As the needs of different jobs change, some team members may be shifted to other

teams for short periods of time. Whitley uses a job costing system to determine job costs and to serve as a basis for biddi

ng and

pricing the jobs. Direct materials and direct labor are easily traced to each job, using Whitley’s cost tracking software.

Overhead

2.Suppose that for the entire year, Whitley used 23,800 labor hours and total actual overhead was $525,000. What 3. is the

4.

What are some of the potential sustainability issues for Whitley?

5. Whitley has chosen direct labor hours as the cost driver

-base for applying overhead. What are some alternative cost drivers,

and how would you choose among them?

4. As a construction company, Whitley has a lot of waste to dispose of, most of which

are less harmful.

5. The possible cost drivers in this case include direct labor hours (used by Whitley),

direct labor cost, and materials cost. There is not likely to be much difference between

Budgeted total factory overhead $568,000

Budgeted total direct labor-hours 71,000

Company's Ledger

2.

Exercise 4-35 Application of Overhead

Tomek Company uses a job costing system that applies factory overhead on the basis of direct labor-

hours. The company’s factory overhead budget for the current year included the following estimates:

1.

Exercise 4-36 Overhead Rate; Pricing

Norton Associates is an advertising agency in Columbus, Ohio. The company's controller estimated

that it would incur $325,000 in overhead costs for the current year. Because the overhead costs of each

project change in direct proportion to the amount of direct professional hours incurred, the controller

decided that overhead should be applied on the basis of professional hours. The controller estimated

25,000 professional hours for the year. During October, Norton incurred the following costs to make a

20-second TV commercial for Central Ohio Bank. Actual overhead costs to make the commercial

2. What is the total amount of the bill that Norton will send Central Texas Bank?

Direct Materials

Paint

Hours

Labor Cost

at $10.75

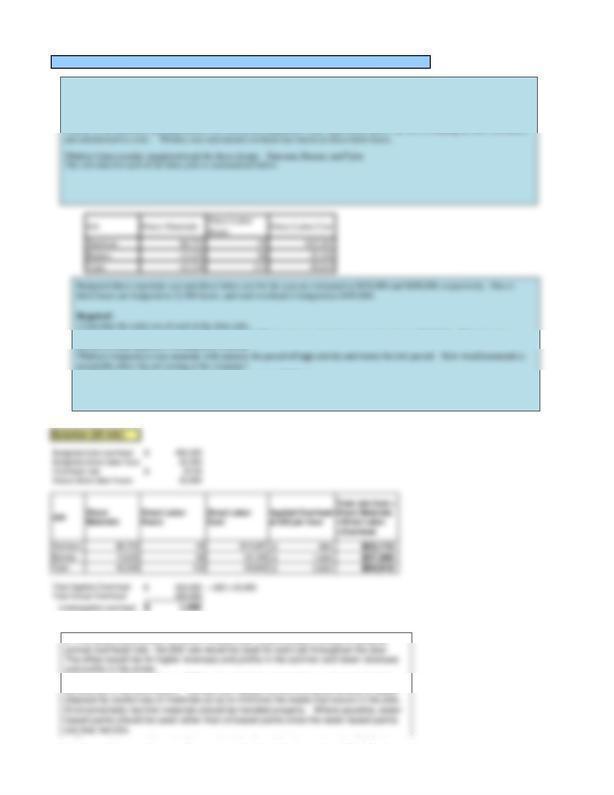

Exercise 4-37 Overhead Application

Progressive Painting Company (PPC) is a successful company in commercial and residential painting. PPC has a

variety of jobs: new construction, repair and repainting existing structures, and restoration of very old buildings and

homes. The company is known for the quality and reliability of its work, and customers expect to pay a little more

for those benefits. One of the company’s core values is sustainability, and it insists on using the most

environmentally friendly paints and materials in its work; it has refused jobs where the client required a more

environmentally harmful paint than PPC thought was appropriate for the application.

This value has lost PPC some

jobs, but has attracted a loyal and growing customer base.

The company uses job costing and applies overhead on the basis of direct labor hours. Overhead for the company

consists of painting equipment, trucks, supervisory labor, supplies and administrative operation costs. The total

budgeted costs for the year are shown below.

2.

The Prevette job required oil-based paint and the clean-up after the job required the use of chemicals that,

after use, had to be disposed of in an environmentally appropriate way. In contrast, the Harmon job required

water

-based paint and the job clean-up was very quick and simple and involved no harmful chemicals. Does

the job costing in part 1 above capture the difference between the two jobs in the types of paint used? Do you

think the costing system should capture this difference, if any, and if so how do you think the cost system should

be changed?

2. The oil-based paint, because it required more clean-up time and materials (harmful chemicals),

increased direct labor hours and increased materials costs (due to the purchase of the clean

-up

chemicals), both of which are included in job cost. The disposal of the clean

-up waste is likely to be

disposing of the waste clean

-up materials in an environmentally appropriate manner is commendable.

Exercise 4-38 Spoilage and Scrap

1. Journal entries to record spoilage costs:

a. To record the normal spoilage attributable to Job X12

2. Journal entries to record scrap sold:

a. To record the scrap sold attributable to a specific job

Note: See also the Comments on Cost Management in Action at the end of the chapter regarding a similar costing situation.

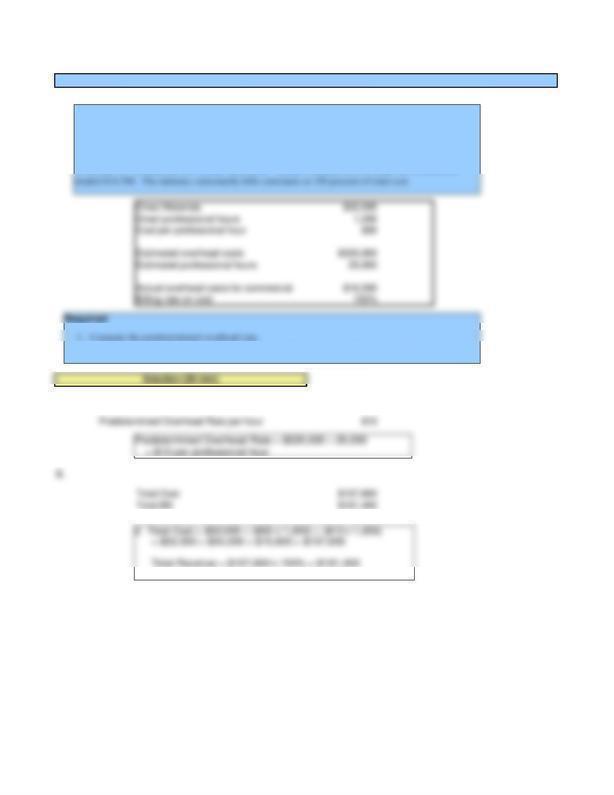

Problem 4-39 Overhead Rates Used for Each Machine in a Printing Plant

Solution (25 min)

Ennis Inc.’s Forms Solutions Group (http://www.ennis.com/) is a Texas-based machine-

intensive printing company that produces business forms. The resources demanded by a

specific job depend on the type and amount of paper used and the composition and the

construction of the business form. All jobs are constrained by the time necessary on a press

and on a collator capable of producing forms at the required size.

Ennis Inc.’s Forms Solutions (EFS) uses job costing for pricing and bidding decisions.

EFS uses a separate factory overhead rate for each machine. Costs of machine operator,

support personnel, and supplies are identified directly with presses and collators. Other factory

overhead costs – including insurance, supervision, and office salaries – are allocated to

machines based on their processing capacity (cost driven is the number of feet of business

form per minute), weighted by the maximum paper width and complexity (the cost driver is

the number of colors and other features) that they are capable of handling.

When EFS receives a request for a bid on a particular job, the company uses computer

software to determine direct material costs based on the type and quantity of paper. Then it

identifies the least expensive press and collator that are capable of handling the specifications

for the business form ordered. The third step is to estimate the total press and collator

processing costs by using specific cost-driver rates per machine time multiplied by the

estimated processing time. The bid price is calculated by adding a standard markup to the total

press, collator, and direct material costs. A higher markup is used for rush jobs and jobs

requiring special features.

Required

Discuss the strengths and weaknesses of the EFS costing system and its strategic implications.

This short case is intended as a basis for class discussion that could the following

topics and questions: application of job costing in the printing industry; what are the

factors driving the accuracy of product costing; how does the choice of job costing

method affect pricing; what is the effect of cost allocation methods on management

behavior, performance evaluation, and how does a chosen cost method advance or

hinder the firm’s progress to its strategic goals? Some observations that I would

bring out in this discussion include:

EFS uses a job costing system in which materials and direct labor are traced to the

job, and overhead is traced to each machine and then applied to the jobs based on

machine usage

A strength would be that EFS has put a lot of effort into tracing the printing costs

accurately and using an overhead allocation approach that attempts to trace the

costs of the machinery to the jobs that used that machinery

I would begin a discussion of the EFS approach to allocating other overhead costs –

insurance, supervision, and office salaries – to the jobs based on the capacity of the

machines. That is, machines with more printing capacity (where capacity is the

number of feet of forms produced per minute of machine time) will receive a larger

portion of this portion of overhead. This is very much like a volume based rate,

which is OK, but does not reflect the actual behavior of these costs. Suppose the

total of other overhead is significant. Then small jobs on high capacity (fast)

machines will be charged a relatively high rate. Conversely, large jobs on low-

capacity machines will be charged a relatively low rate. How this would affect

pricing and the allocation of jobs to machines is not easy to predict.

The strategic issue is (as in Problem 4-51above) the (unknown) impact of cost

calculations on competitive pricing, and therefore on the company’s

competitiveness. The success of the company depends on its ability to set a

competitive price, recognizing that the company has unused capacity (in a seasonal

business) in some periods of the year.

Source: Jacci L. Rodgers, S. Mark Comstock and Karl Pritz, “Customize Your

Costing System,” Management Accounting, May 1993, pp. 31-32. See also, Lisa

Cross, “Benefiting from Costing and Pricing Tools,” Graphic Arts Monthly, July

2004, pp 32-34.

This short case is intended as a basis for class discussion that could the following

topics and questions: application of job costing in the printing industry; what are the

factors driving the accuracy of product costing; how does the choice of job costing

method affect pricing; what is the effect of cost allocation methods on management

behavior, performance evaluation, and how does a chosen cost method advance or

Problem 4-40 Plantwide versus Departmental Overhead Rate

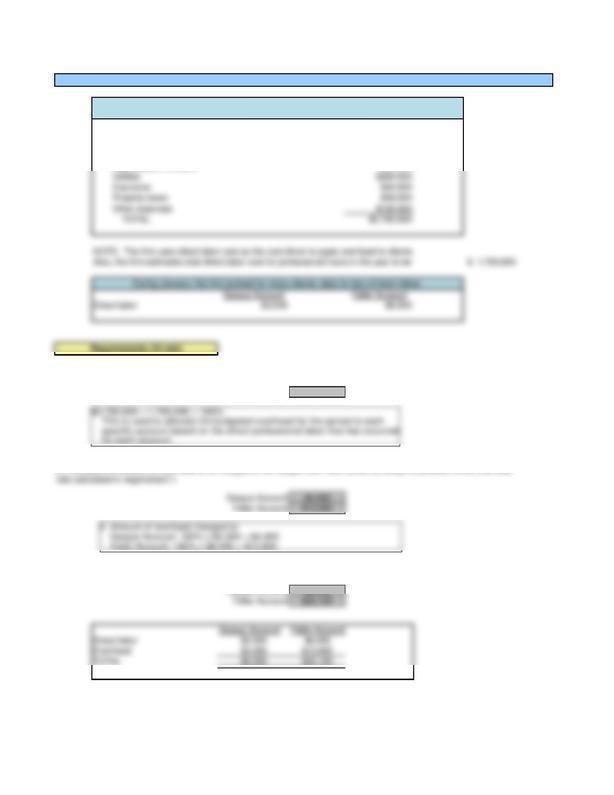

Rose Bach was recently hired as controller of Empco Inc., a sheet metal

manufacturer. Empco has been in the sheet metal business for many years and is

currently investigating ways to modernize its manufacturing process. At the first

staff meeting Rose attended, Bob Kelley, chief engineer, presented a proposal for

automating the drilling department. He recommended that Empco purchase two

3. How would you improve the allocation of overhead costs?

1. Empco Inc. is currently using a plantwide overhead rate that is

applied on the basis of direct labor dollars. In general, a plantwide

factory overhead rate is acceptable only if a similar relationship

between overhead and direct labor exists in all departments, or the

company manufactures products, which receive proportional

2. Because Empco uses a plantwide overhead rate applied on the

basis of direct labor dollars, thus elimination of direct labor in the

Drilling Department through the introduction of robots may appear to

3. In order to improve the allocation of overhead costs , Empco should:

1. Empco Inc. is currently using a plantwide overhead rate that is

applied on the basis of direct labor dollars. In general, a plantwide

factory overhead rate is acceptable only if a similar relationship

between overhead and direct labor exists in all departments, or the

company manufactures products, which receive proportional

2. Because Empco uses a plantwide overhead rate applied on the

basis of direct labor dollars, thus elimination of direct labor in the

Drilling Department through the introduction of robots may appear to

3. In order to improve the allocation of overhead costs , Empco should:

Direct Materials $200

Direct Labor $12 per hr. $300

Machine hours 20

DL Hours per Unit:

Problem 4-41 Plantwide versus Departmental Overhead Rate

2. If factory overhead were applied on the basis of machine-hours, what would

be the plantwide overhead rate?

3. If the company produced 1,000 units during the year, what was the total

amount of applied factory overhead in each department in requirements 1 and

2?

4. If you were asked to evaluate the performance of each department manager,

which allocation basis (cost driver) would you use? Why?

Ryan Corporation manufactures a popular fax machine. Cost estimates for one unit of the product

for the year follow:

Labor and machine-hour breakdowns by department:

4. If direct labor-hours are used to apply factory overhead, Department A is

assigned more than its total estimated overhead and Department B is assigned

5. Using DLHs for Departent A and Machine Hours for Department B:

4. If direct labor-hours are used to apply factory overhead, Department A is

assigned more than its total estimated overhead and Department B is assigned

JOB # MATERIALS LABOR OVERHEAD TOTAL

T114 $31,500 $16,250 $28,750 $76,500

Budgeted Overhead

Variable

Indirect Materials $68,000

Indirect Labor $56,000

Employee Benefits $28,000

Fixed

Supervision $13,000

Depreciation $15,000

- 50,000 - 50,000

Problem 4-42 Application of Overhead

Work in Process Inventory for Carston, Inc. at the beginning of period:

The company's budgeted costs for the year

are as follows:

Indirect Labor

1. What was the actual overhead for the year?

2. What was overapplied or underapplied overhead for the year?

3. Job T114 was the only job completed and sold in the year. What amount was included in the cost of the goods sold

for this job?

4. What was the amount of Work-in-Process Inventory at the end of the year?

2. LABOR Applied OH

10,000$

18,000

4. Work-in-Process Inventory: $237,000 =$33,000 + $68,000 + $136,000

MATERIALS LABOR Applied OH

-$

x

JOB #

T114

T119

JOB #

T114

1Predetermined Overhead Rate

= $455,600 ÷ 33,500 = $13.60 per direct labor hour

2a. Factory Overhead 1,800

Prepaid Insurance 1,800

1,025

Accumulated Depreciation 1,025

c. Materials Inventory 336

Accounts Payable 336

$16 x21 = $336

d. Factory Overhead 6,510

Cash 6,510

e. Work-in-Process Inventory 140,000

Factory Overhead

20,000

Cash 160,000

f. Factory Overhead 6,270

Cash 6,270

Problem 4-43 Cost Flows, Application of Overhead

Solution (40 min)

b. Selling & Administrative Expense

Dream Makers is a small manufacturer of gold and platinum. It uses a job costing system that applies overhead on

the basis of direct labor-hours. Budgeted factory overhead for the year was $455,600, and management budgeted

33,500 direct labor-hours. The company had no materials, work-in-process or finished goods inventory at the

beginning of April. These transactions were recorded during April:

a. April insurance cost for the manufacturing property and equipment was $1,800. The premium had been paid in

January.

b. Recorded $1,025 depreciation on an administrative asset.

c. Purchased 21 pounds of high-grade polishing materials at $15 per pound (indirect material).

5. Prepare the income statement for April

n. Accounts Receivable 56,410

3. Actual Overhead = $1,800 + $6,510 + $20,000 + $6,270 + $1,600

+ $3,505 = $39,685

Overapplied Overhead = $40,800 - $39,685 = $1,115

Decrease Cost of Goods Sold

4,5

Dream Makers

April 30

Data

Cost of Goods Manufactured 64,000$

Cost of Goods Sold 47,860

Estimated depreciation 455,600

Estimated direct labor hours 33,500

Direct labor hours in April 3,000

Depreciation Expense--Plant 3,505$

Direct Materials Used 18,500

Indirect Materials Used 1,600

Direct Labor 140,000

Indirect Labor 20,000

Finished Goods Inventory, Beginning -

Finished Goods Inventory, Ending 16,140 =64,000-47,860

Factory utilities 6,510

Factory insurance 1,800

Selling and Administrative 6,685 =1,025+5,660

Work-in-Process Inventory, Beginning -

Work-in-Process Inventory, Ending 135,500 =140,000+18,500+42,000-65,000

Advertising Expense 2,650

Sales Revenue 56,410

Other factory overhead 6,270

Dream Makers

Statement of Cost of Goods Manufactured

Direct Materials Used 18,500$

For the Month Ended April 30

The following information applies to the O'Donnell Company for March production. There are only two jobs (X and Y) in production in March.

Job X Job Y TOTAL

Material A 16,000 Material A 8,000 16,000 24,000

Material B 12,000 Material B 3,000 8,000 11,000

Indirect Materials 3,000 Subtotal: 11,000 24,000 35,000

TOTAL: 31,000 Indirect Materials 39,000

TOTAL: 74,000

Problem Data Summary:

Direct

Application Rate

46.00$ per machine hr

1. Total Manufacturing Costs for each job

Job X Job Y Total

Total Direct Materials

Cost

11,000$ 24,000$ 35,000$

Solution (20 min)

Purchased direct materials and indirect materials with the

following summary of receiving reports:

Issued direct materials and indirect materials with this summary of requisitions:

Problem 4-44 Application of Overhead

Factory labor incurred is summarized by these time

Factory utilities, factory depreciation, and factory insurance incurred is

2. Calculate the amount of overapplied or underapplied overhead and state whether the cost of goods sold

account will be increased or decreased by the adjustment.

x Application rate 46$ 46$

2. Calculate Factory Overhead Under or Overapplied

Actual Factory OH:

Indirect Materials 39,000$

Indirect Labor 28,000

Utilities 3,000

Job S Job T TOTAL

Material A 28,500$ 71,250$ 99,750$

Material B 12,000 35,000 47,000

Subtotal: 40,500$ 106,250$ 146,750

Indirect Materials 211,000

2. Overapplied overhead: $22,875

See calculations below:

Problem Information

Direct

Materials

Direct Labor Labor Hours

Job S 55,500$ 6,175

Material A 28,500$

Material B 12,000

Job T 45,000$ 4,275

Material A 71,250$

Material B 35,000

Factory Overhead Application Rate $42.50 per labor hr

1. Total Manufacturing Costs for each job

Job S Job T Total

Total Direct Materials Cost 40,500.00$ 106,250.00$ 146,750.00$

Total Direct Labor Cost

2. Calculate Factory Overhead Under or Overapplied

42.50

Problem 4-45 Application of Overhead

Direct materials and indirect materials used are as follows:

The following information is for Punta Company for July 2013:

Actual Factory OH:

Indirect Materials 211,000$

Indirect Labor 133,000

Problem 4-46 Cost Flows, Application of Overhead

2.

a. Direct Materials Inventory 130,000

Accounts Payable 130,000

$26 x 5,000 = $130,000

b. Materials Inventory 1,800

Accounts Payable 1,800

$36 x 50 = $1,800

c. Work-in-Process Inventory 91,000

Factory Overhead 1,116

Materials Inventory 91,000

Materials Inventory 1,116

$26 x 3,500 = $91,000

$36 x 31.0 = $1,116

d. Work-in-Process Inventory 141,900

Factory Overhead 46,000

Cash 187,900

$187,900 - $46,000 = $141,900

Direct labor-hours used = $141,900 ÷$22 = 6,450 hours

e. Factory Overhead 15,230

Cash 15,230

f. Factory Overhead 3,500

Prepaid Insurance 3,500

g. Factory Overhead 8,500

Accumulated Depreciation 8,500

h. Selling & Administrative Expense 2,400

Accumulated Depreciation 2,400

i. Advertising Expense 5,500

Cash 5,500

j. Factory Overhead 13,500

Cash 13,500

k. Selling & Administrative Expense 13,250

Cash 13,250

l. Applied Overhead = $14.50 x 6,450 DL hour = $93,525

Mooresville Corporation manufactures eighteenth-century, classical-style furniture. It uses a job costing system that

applies factory overhead on the basis of direct labor-hours. Budgeted factory overhead for the year was $1,261,500, and

management budgeted 87,000 direct labor-hours. These transactions were recorded during August:

a. Purchased 5,000 square feet of oak on account at $26 per square foot.

b. Purchased 50 gallons of glue on account at $36 per gallon (indirect material).

c. Requisitioned 3,500 square feet of oak and 31 gallons of glue for production.

d. Incurred and paid payroll costs of $187,900. Of this amount, $46,000 were indirect labor costs; direct labor

l. Applied Overhead = $14.50 x 6,450 DL hour = $93,525

Work-in-Process Inventory 93,525

Factory overhead 93,525

m. Finished Goods Inventory 146,000

Work-in-Process Inventory 146,000

n. Accounts Receivable 132,000

Sales Revenue 132,000

Cost of Goods Sold 112,000

Finished Goods Inventory 112,000

Overhead

Indirect materials $300,000

Indirect labor $1,600,000

Depreciation-Building $293,000

Depreciation-Furniture $25,000

1.) Compute the firm's overhead rate

Budgeted overhead rate 160%

3.) Compute a separate job cost for the Gargus and the Feller accounts.

Gargus Account $6,500

2.) Compute the amount of overhead to be charged to the Gargus and Feller accounts using the predetermined overhead

Problem 4-47 Application of Overhead; Service Industry

Meyers CPA Firm

Annual Budget

Dept. Number Job Number Requisition Number Quantity Cost per Unit

12906 B9766 4,550 1.34$

22907 B9767 110 22.18$

1 $3.00 per direct labor-hour

2150% of direct labor cost

1.

Job Number Direct Materials Direct Labor Factory Overhead Total Costs

Increase in Department 1 direct labor rate 10%

Increase in Department 2 direct labor rate 25%

Job Number Direct Materials Direct Labor Factory Overhead Total Costs

2906 $12,077.50 $13,670.80 $5,736.00 $31,484.30

2907 $2,439.80 $1,509.60 $2,264.40 $6,213.80

Problem 4-48 Job Cost; Pivot Tables in Excel (Excel tutorial on text web site)

Summary of Direct Materials Requisitions

2.

Summary of Job Completion

Decker Screw Manufacturing Company produces special screws made to customer specification. During

June, the following data pertained to the below listed costs. Decker had no beginning work-in-process

inventory for June. Of the jobs begun in June, Job 2906 was completed and sold on account for $30,000,

Job 2907 was completed but not sold, and Job 2908 was still in process.

SEE ALSO Solution Below for greater detail

22908 23 48.00$ 1,104.00$ 32

Labor Overhead

Department 1 6.50$ 3.00$ per labor hour

Department 2 8.88$ 150% per labor dollar

22907 110 22.18$ 2,439.80$

22908 23 48.00$ 1,104.00$

2908 Total 10,104.00$

Grand Total 24,621.30$

Labor

Department Number Job No. Labor Hours Labor Cost

22908 32 284.16

2908 Total 183 1,265.66

Grand Total 2,231 14,901.34$

Applied Overhead

Labor hours Dept 1 1,912 0 151

OH Rate in Dept 1 $3.00 $3.00 $3.00

Subtotal Dept 1 $5,736.00 $0.00 $453.00

Labor Hours Dept 2 0 136.00 32.00

Labor Rate Dept 2 8.88$ 8.88$ 8.88$

OH Rate in Dept 2 150% 150% 150%

22908 23 48.00$ 1,104.00$ 32

Labor Overhead

Department 1 7.15$ 3.00$ per labor hour

Department 2 11.10$ 150% per labor dollar

Job 2906

Job 2907

Job 2908

22907 110 22.18$ 2,439.80

22908 23 48.00$ 1,104.00

2908 Total 10,104.00

Grand Total 24,621.30$

Labor

Department Number Job No. Labor Hours Labor Cost

12906

22908 32

355.20

2908 Total 183 1,434.85

Grand Total 2,231 16,615.25$

Applied Overhead

Labor hours Dept 1 1,912 0 151

OH Rate in Dept 1 $3.00 $3.00 $3.00

Subtotal Dept 1 $5,736.00 $0.00 $453.00

Job 2906

Job 2907

Job 2908

Part 3

Solution Using Pivot Tables in Excel

DATA:

Requistions for matreial or time tickets

22908 23 48.00$ 1,104.00$ 32

Rates: Labor Overhead

Department 1 6.50$ 3.00$ per labor hour

Department 2 8.88$ 150% per labor dollar

Solution:

First, do a Pivot Table on Jobs and Departments for labor hours and materials cost:

Job No.

Department Number Data 2906 2907 2908 Grand Total

1 Sum of Materials Cost 12,077.50$ 9,000.00$ 21,077.50$

Sum of Labor Hours 1912 151 2063

2 Sum of Materials Cost 2,439.80$ 1,104.00$ 3,543.80$

Sum of Labor Hours 136 32 168

Total Sum of Materials Cost 12,077.50$ 2,439.80$ 10,104.00$ 24,621.30$

Total Sum of Labor Hours 1912 136 183 2231

Then, complete the cost report below to obtain cost for each job:

Problem 4-48 Job Cost; Pivot Tables in Excel (Excel tutorial on text web site)

Applied Overhead

Part 4

Solution Using Pivot Tables in Excel

DATA:

Requistions for material or time tickets

22908 23 48.00$ 1,104.00$ 32

Rates: Labor Overhead

Department 1 7.15$ 3.00$ per labor hour

Department 2 11.10$ 150% per labor dollar

Solution:

First, do a Pivot Table on Jobs and Departments for labor hours and materials cost:

Job No.

Department Number Data 2906 2907 2908 Grand Total

1 Sum of Materials Cost 12,077.50$ 9,000.00$ 21,077.50$

Sum of Labor Hours 1912 151 2063

2 Sum of Materials Cost 2,439.80$ 1,104.00$ 3,543.80$

Sum of Labor Hours 136 32 168

Total Sum of Materials Cost 12,077.50$ 2,439.80$ 10,104.00$ 24,621.30$

Total Sum of Labor Hours 1912 136 183 2231

Then, complete the cost report below to obtain cost for each job:

Problem 4-48 Job Cost; Pivot Tables in Excel (Excel tutorial on text web site)

Applied Overhead

Inventories July 1 July 31

Direct Materials $36,500 ?

Work in Process $41,000 ?

Finished Goods $0 $0

Cost of Goods Sold, July ?

1Total Direct Labor cost incurred for for July 237,000$ =(3,500+2,800+1,600) x $30

OH applied in July (given) 900,600$

OH Application Rate 380%

=$900,600 ÷ 237,000

2Beginning Materials Inventory 36,500$

+Purchases in July 55,000

-Materials used in July 54,600

=Ending Balanced in Materials Inventory 36,900$

3Actual factory overhead cost incurred during the month of July:

Indirect labor 6,900hrs x $30/hr 207,000$

Rent 131,500

Utility 180,600

Repairs and maintenance 188,500

Depreciation 131,100

Other 56,000

Actual factory OH cost in July 894,700$

4

Solution (40 min)

Problem 4-59 Application of Overhead; Schedule of Cost of Goods Manufactured

Haughton Company uses a job costing system for its production costs and a predetermined factory

overhead rate based on direct labor costs to apply factory overhead to all jobs. During the month of

July, the firm processed three jobs: X13, X14, and X15, of which X13 was started in June. The firm

was able to recover only a fragment of its records, as shown below, after a recent attack on its

computer.

7. What is the cost per unit of Job X13 if it has a total of 100 units?

8. Prepare the statement of cost of goods sold for July.

Ending balance of work in process inventory account

Job X14 Job X15 Total

DM 24,220$ 14,000$ 38,220$

DL 84,000 48,000 132,000

Applied overhead 319,200 182,400 501,600

427,420$ 244,400$ 671,820$

5

Haughton Company

6Over- or under-applied overhead:

Problem 4-50 Application of Overhead; Ethics

Aero Systems is a manufacturer of airplane parts and engines for a variety of military and commercial aircraft.

It has two production departments. Department A is machine intensive; Department B is labor intensive. Aero

Systems has adopted a traditional plantwide rate using the direct labor-hour-based overhead allocation system.

The company recently conducted a pilot study using a departmental overhead rate costing system. This system

used two overhead allocation bases: machine-hours for Department A and direct labor-hours for Department

B. The study showed that the system, which will be more accurate and timely, will assign lower costs to the

government jobs and higher costs to the company’s nongovernmental jobs. Apparently, the current (less

accurate) direct labor-based costing system has overcosted government jobs and undercosted private business

jobs. On hearing of this, top management has decided to scrap the plans for adopting the new departmental

overhead rate costing system because government jobs constitute 40 percent of Aero Systems’ business and

the new system will reduce the price and thus the profit for this part of its business.

Required

As the management accountant participating in this pilot study project, what is your responsibility when you

hear of top management’s decision to cancel the plans to implement the new departmental overhead rate

costing system? Can you ignore your professional ethics code in this case? What would you do?

1.

Raw sweet corn $6.50

2.

Cost per Pound

Problem 4-51 Operation Costing

Cost Information for the Month of January

Brian Canning Co., which sells canned corn, uses an operation costing system. Cans of corn are

classified as either sweet or regular, depending on the type of corn used. Both types of corn go through

the separating and cleaning operations, but only regular corn goes through the creaming operation.

During January, tow batches of corn were canned from start to finish. Batch X consisted of 800 pounds

of sweet corn and batch Y consisted of 700 pounds of regular corn. The company had no beginning or

ending work-in-process inventory. The following cost information is for the month of January:

a. To record the requisition of the raw corn for both types less

the cream cost:

WIP Inventory: Separation Department.......7,350

Direct Materials Inventory....………….......7,350

$5,200 + $2,450 - $300 = $7,350

b. To apply conversion costs to the Separation Department:

WIP Inventory: Separation Department .......1,500

Conversion Costs Applied ……...…………1,500

c. To transfer both types of corn to the Cleaning Department:

WIP Inventory: Cleaning Department.....…...8,850

WIP Inventory: Separation Department.....8,850

$7,350 + $1,500 = $8,850

d. To apply conversion cost to the Cleaning Department:

WIP Inventory: Cleaning Department......…….900

Conversion Costs Applied..………….…..…. 900

e. To transfer the Regular Corn to the Creaming Department

and the Sweet Corn to Finished Goods Inventory:

WIP Inventory: Creaming Department........3,270

Finished Goods Inventory……………..…....6,480

WIP Inventory: Cleaning Department......9,750

$2,450 - $300 + ($1 x 700) + ($0.60 x 700) = $3,270

$5,200 + ($1 x 800) + ($0.60 x 800) = $6,480

$8,850 + $900 = $9,750

f. To transfer cream costs and conversion cost to the

Creaming Department:

WIP Inventory: Creaming Department….......510

Direct Materials Inventory.……….………..300

Conversion Costs Applied ………………..210

Problem 4-52 Spoilage, Rework, and Scrap

1. Normal spoilage is the occurrence of unacceptable units arising under efficient operating

2. a. Spoiled units are unacceptable units of production that are either

discarded or sold for disposal value.

b. Rework units are unacceptable units or production that are

3. a. An analysis of the 5,000 units rejected by Richport Company for Job

No. N1192-122 yields the following breakdown between normal and

abnormal spoilage.

Units

Richport Company manufactures products that often require specification changes or modifications to

meet customer needs. Consequently, Richport employs a job costing system for its operations.

Although the specification changes and modifications are commonplace, Richport has been able to

establish a normal spoilage rate of 2.5% of good units produced (before spoilage). The company

recognizes normal spoilage during the budgeting process and classifies it as a component of factory

overhead. Thus, the predetermined overhead rate used to apply factory overhead costs to jobs includes an

allowance for net spoilage cost for normal spoilage. If spoilage on a job exceeds the normal rate, it is

considered abnormal and then must be analyzed and the cause of the spoilage must be submitted to

management.

1. Normal spoilage is the occurrence of unacceptable units arising under efficient operating

2. a. Spoiled units are unacceptable units of production that are either

discarded or sold for disposal value.

b. Rework units are unacceptable units or production that are

3. a. An analysis of the 5,000 units rejected by Richport Company for Job

No. N1192-122 yields the following breakdown between normal and

abnormal spoilage.

Units

Normal spoilage* 3,000

Abnormal spoilage:

Design defect 900

Other [5,000 – (3,000 + 900)] 1,100

Total units rejected 5,000

*Normal spoilage = .025 of normal input

Normal input = 117,000 ÷ (1-.025)

= 120,000 units