Chapter 02 - Implementing Strategy: The Value Chain, the Balanced Scorecard, and the Strategy Map

Chapter 2

Implementing Strategy: The Value Chain, the Balanced Scorecard, and the

Strategy Map

Learning Objectives

New in this Edition

• All Real World Focus items are revised and updated, particularly the item on the

currency fluctuation; one new Real World Focus item on execution; real world

information throughout the chapter is revised for current information

• New Cost Management in Action item on strategy in consumer electronics – Apple

vs. Samsung

• The section on Execution is updated and enhanced

• Twelve new Brief Exercises, three new problems, and several revised exercises and

problems

Teaching Suggestions

This chapter is unique, and is not included in most cost and management accounting textbooks.

Because of the importance of the strategic theme of the book, this entire chapter is devoted to developing

the three key areas of strategy implementation. The chapter follows the introduction to strategy in chapter

1, which we view as a foundational topic, as is ethics, and is thus included in the first chapter. Chapter

two develops the strategic emphasis by explaining the methods in which it is implemented in

Chapter 02 - Implementing Strategy: The Value Chain, the Balanced Scorecard, and the Strategy Map

For the value chain. I pick a simple example and show it on the board or transparency. Then I ask

the class to help develop a value chain for a similar type of firm. Some students will at first find the

concept of the value chain too vague, and they are concerned how they will do homework problems

(2) how the scorecard differs among firms and industries.

An important point to convey in this chapter is that cost management must be based on a strategic

competitive assessment of the firm. That is, in order to develop effective cost management methods, it is

necessary to know how the firm competes, and how it is successful. The methods to be developed will

depend on this. If the firm is a cost leadership competitor, the choice of cost management methods will be

different than if the firm is a differentiator.

A related point is that the students must understand at this point that what they will see later in the

course, whether it be the master budget, the flexible budget, or productivity analysis, etc, must be viewed

within the context of how it helps the firm advance its strategy and become more successful. None of the

topics are covered simply because this topic or method is used in practice. Rather, each topic is

considered from the standpoint: how will this method help the firm succeed?

Lecture Notes

A. How a Firm Succeeds: The Competitive Strategy. It is useful to reinforce in chapter two the basic

concepts of strategy, using the Michael Porter framework introduced in chapter 1. A firm succeeds by

finding a sustainable strategy, which is a set of policies, procedures, and approaches to business to

Chapter 02 - Implementing Strategy: The Value Chain, the Balanced Scorecard, and the Strategy Map

market share and customer satisfaction) show the firm’s current and potential competitive position.

Strategic financial and nonfinancial measures of success are commonly called critical success factors

(CSFs).

B. Critical Success Factors and SWOT Analysis.

SWOT analysis is a systematic procedure for identifying a firm’s CSFs: its internal Strengths and

Weaknesses and its external Opportunities and Threats. Strengths are skills and resources that the firm

has more abundantly than other firms. Skills or competencies that the firm employs especially well are

called core competencies. Core competencies are important because they point to areas of significant

Chapter 02 - Implementing Strategy: The Value Chain, the Balanced Scorecard, and the Strategy Map

D. Cost, Quality, and Time. Many firms find that a consideration of critical success factors yields a

renewed focus on the three key factors: cost, quality, and speed of product development and product

delivery. Increasingly, firms find that they must compete effectively on each of these three factors.

Suppliers to these firms expect to meet very high standards of quality and to meet increasingly demanding

delivery terms.

E. Value-Chain Analysis. Value-chain analysis is a strategic analysis tool used to better understand the

firm’s competitive advantage, to identify where value to customers can be increased or costs reduced, and

to better understand the firm’s linkages with suppliers, customers, and other firms. The activities of the

value-chain include all steps necessary to provide a competitive product or service to the customer.

Although the value-chains are sometimes difficult to describe for a service or not-for-profit organization

because they might have no physical flow to visualize, the approach is applied to all types of firms. The

term value-chain is used because each activity is intended to add value to the product or service.

Management can better understand the firm’s competitive advantage by separating its operations

according to activity. The underlying concept of the analysis is that each firm occupies a selected part or

parts of the entire value chain. The determination of which part or parts of the chain to occupy is a

strategic analysis based on the consideration of comparative advantage for the firm. Value-chain analysis

Chapter 02 - Implementing Strategy: The Value Chain, the Balanced Scorecard, and the Strategy Map

2. Identify the Alternative Actions:

3. Obtain Information and Conduct Analyses of the Alternatives

4. Based on Strategy and Analysis, Choose and Implement the Desired Alternative

First decision: As a differentiator based on product quality and innovation, CIC

considers the importance of the quality of the part in question, and decides to manufacture the

5. Provide an On-going Evaluation of the Effectiveness of implementation in Step 4.

Management of CIC realize that the quality of the product and of customer service is

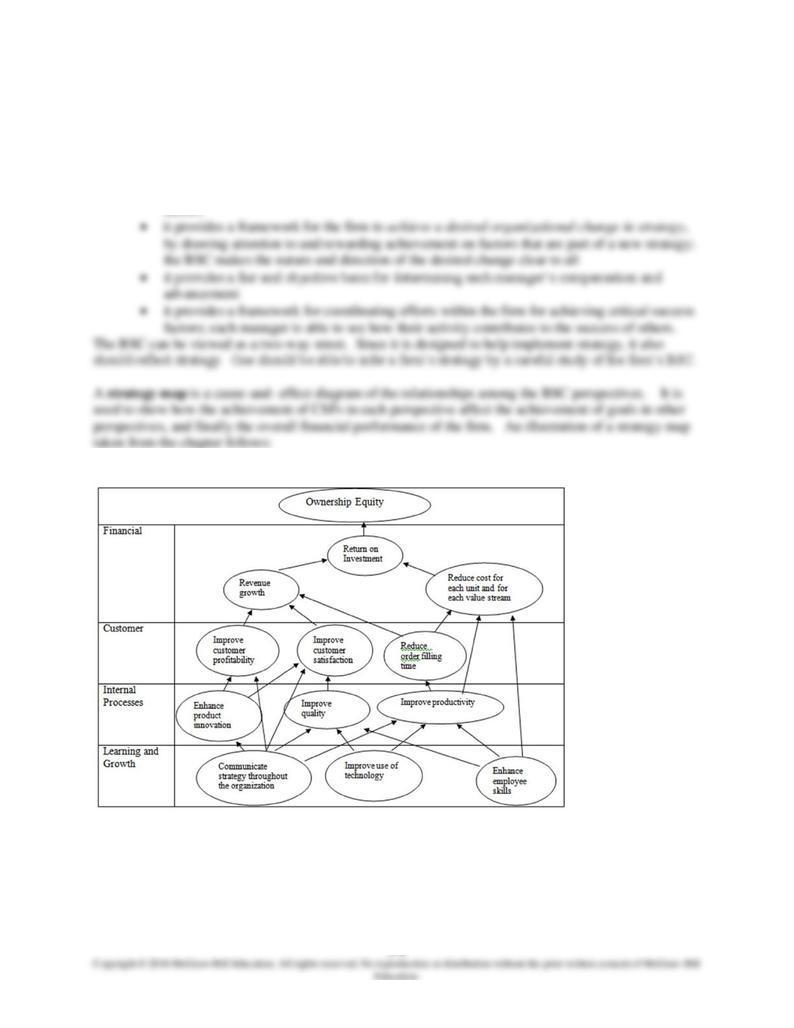

Chapter 02 - Implementing Strategy: The Value Chain, the Balanced Scorecard, and the Strategy Map

perspective, including measures of customer satisfaction, (3) internal process perspective, which includes

measures of productivity, speed, among others, and (4) learning and innovation, which includes such

measures as employee training hours, number of new patents or new products. The BSC provides four

key benefits:

• it provides a means for implementing strategy, by drawing managers attention to

strategically-relevant critical success factors, and rewarding them for achievement on these

factors

Chapter 02 - Implementing Strategy: The Value Chain, the Balanced Scorecard, and the Strategy Map

H. Expanding The Balanced Scorecard: Sustainability

More and more large companies, especially those in the extractive industries, are concerned about the

sustainability of their business, that is, the balancing of short and long term goals in all three dimensions

of the company’s performance – economic, social and environmental. Economic performance is