1

2

10

11

12

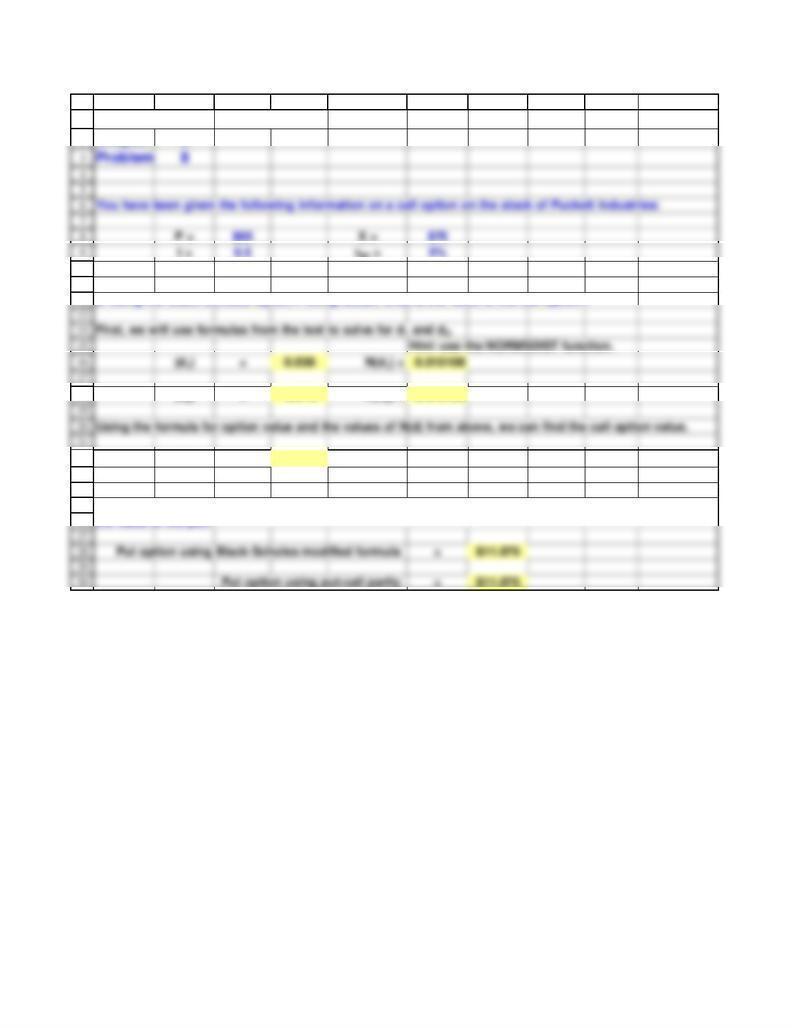

18

22

23

24

25

26

A B C D E F G H I J

Build a Model Solution 11/26/2018

Chapter:

8

s = 0.50

a. Using the Black-Scholes Option Pricing Model, what is the value of the call option?

(d2) = -0.316 N(d2) = 0.376125

VC= $7.803

b. Suppose there is a put option on Puckett's stock with exactly the same inputs as the call option. What is

the value of the put?