Chapter 10

Monetary Policy and Aggregate Demand

◼ Chapter Outline, Overview, and Teaching Tips

Chapter Outline

The Federal Reserve and Monetary Policy

The Monetary Policy Curve

The Taylor Principle: Why the Monetary Policy Curve Has an Upward Slope

Shifts in the MP Curve

Movements Along the MP Curve Versus Shifts in the Curve

Policy and Practice: Movements Along the MP Curve: The Rise in the Federal Funds Rate Target,

2004–2006

Policy and Practice: Shifts in the MP Curve: Autonomous Monetary Easing at the Onset of the 2007–

2009 Financial Crisis

The Aggregate Demand Curve

Deriving the Aggregate Demand Curve Graphically

Factors That Shift the Aggregate Demand Curve

The Money Market and Interest Rates

Liquidity Preference and the Demand for Money

Demand Curve for Money

Supply Curve for Money

Equilibrium in the Money Market

Changes in the Equilibrium Interest Rate

Chapter 10 Appendix: The Demand for Money

Keynesian Theories of Money Demand

Transactions Motive

Precautionary Motive

Speculative Motive

Putting the Three Motives Together

Portfolio Theories of Money Demand

Portfolio Theory

Portfolio Theory and Keynesian Liquidity Preference

98 Mishkin • Macroeconomics: Policy and Practice, Second Edition

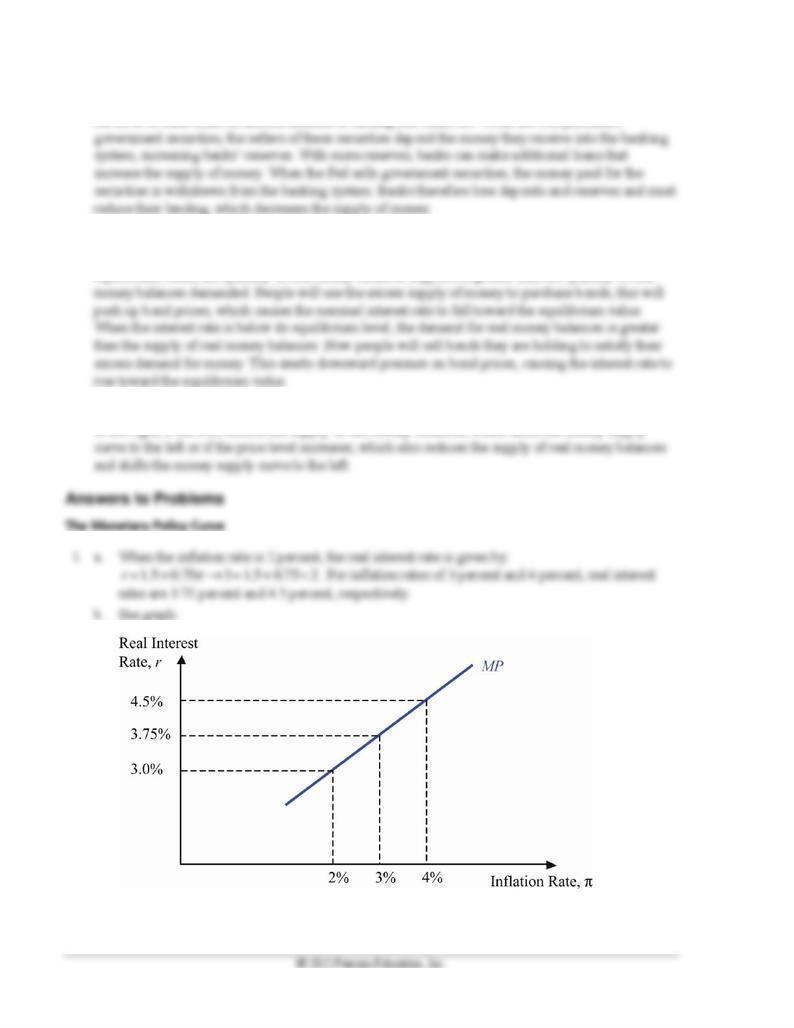

1. The real interest rate is the nominal interest rate minus the expected inflation rate. Because it adjusts

for inflation, the real interest rate indicates the reward for lending and the cost of borrowing money in

purchasing power rather than dollar terms. Because prices are sticky in the short run, changes in the

money supply have little if any short-run effect on prices and therefore on actual and expected

Chapter 10 Monetary Policy and Aggregate Demand 99

2. The monetary policy curve represents the relationship between the inflation rate and the real interest

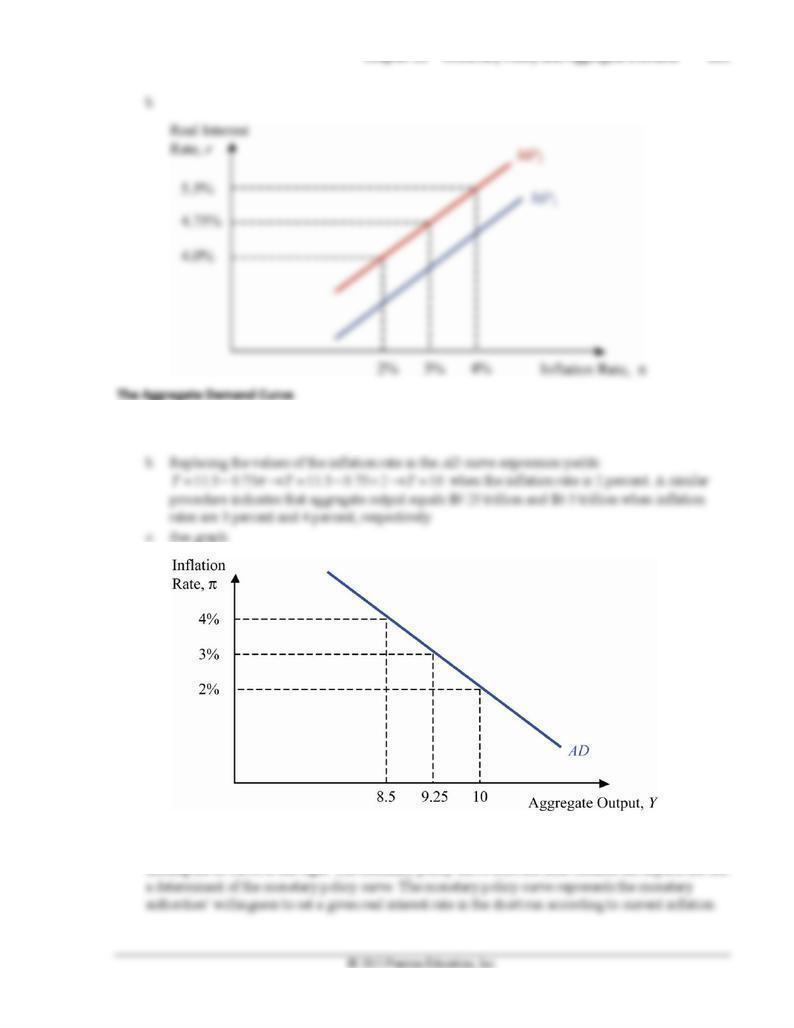

3. An autonomous monetary policy tightening occurs when the Fed decides to raise the real interest rate

4. The aggregate demand curve shows combinations of the inflation rate and the quantity of aggregate

output for which the goods market is in equilibrium with Y = C + I + G + NX. It slopes downward

because, as the MP curve indicates, an increase in inflation results in an increase in the real interest

5. The aggregate demand curve shifts to the right if autonomous consumption, autonomous investment,

6. When the Fed tightens monetary policy by raising the real interest rate at any given inflation rate, this

means that the quantity of aggregate output demanded at any given inflation rate will be lower and so

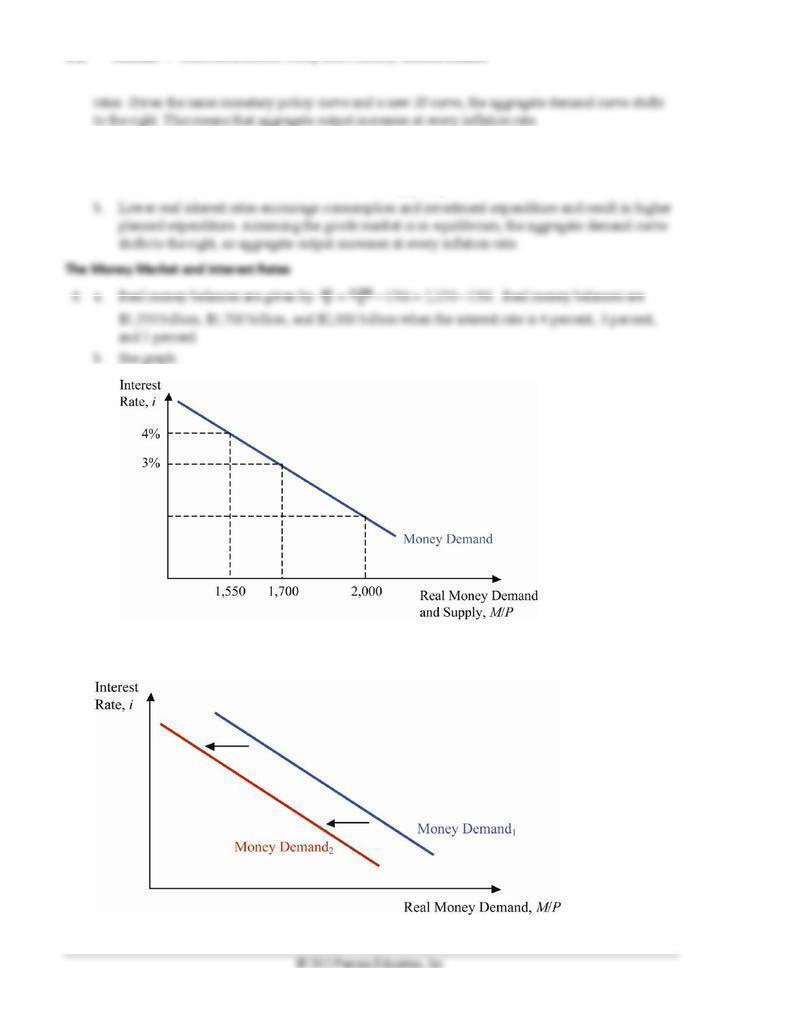

7. The demand for real money balances (M d/P) depends on the nominal interest rate i and real income

Y. Real money balances earn little or no interest; the opportunity cost of holding them is the nominal

interest rate that could be earned on bonds. The higher this interest rate, the greater the interest

earnings that people sacrifice when they hold money rather than investing in bonds. As the nominal

interest rate rises, so does the opportunity cost of holding money, and the quantity demanded of real

100 Mishkin • Macroeconomics: Policy and Practice, Second Edition

8. Open market operations are purchases or sales of government securities the Fed undertakes to change

the level of bank reserves and the amount of lending that banks do. When the Fed purchases

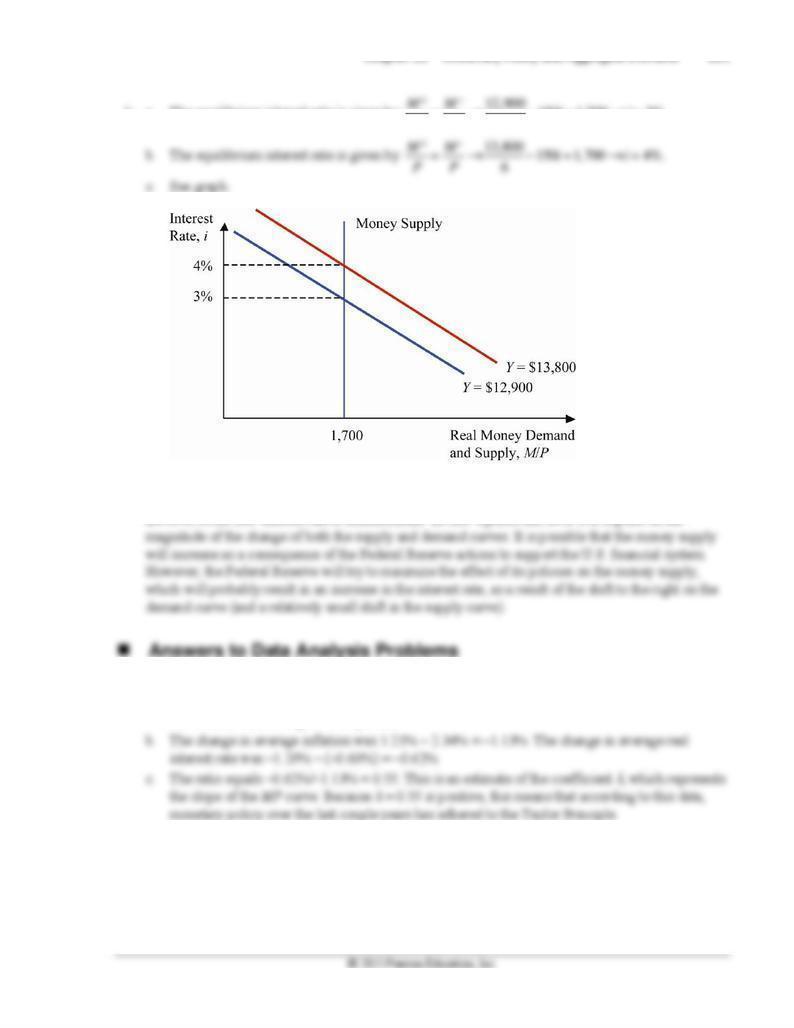

9. Equilibrium in the money market occurs through adjustments in the nominal interest rate to bring the

demand and supply for real money balances into equality. If the nominal interest rate is above its

equilibrium value, the quantity of real money balances supplied is greater than the quantity of real

10. The equilibrium interest rate increases if real income increases, which shifts the money demand curve

to the right; if the Fed reduces the supply of real money balances, which shifts the money supply

2. a. According to the new monetary policy curve, the real interest rate is higher at every inflation rate.

This means that there is an autonomous tightening of monetary policy.

Chapter 10 Monetary Policy and Aggregate Demand 101

3. a. Substituting the expression for the monetary policy curve in the IS curve equation yields:

13 (1.5 0.75 ) 11.5 0.75Y

= − + = −

4. An increase in U.S. net exports directly affects the IS curve because planned expenditure increases at

every real interest rate. Assuming the goods market is in equilibrium, aggregate output increases,

shifting the IS curve to the right. The monetary policy curve does not shift because net exports are not

102 Mishkin • Macroeconomics: Policy and Practice, Second Edition

5. a. A Fed chairman mostly worried about decreasing unemployment will probably result in a

loosening of monetary policy. Graphically, this translates as lower real interest rates at each

inflation rate, or a shift downward of the monetary policy curve.

7. If aggregate output decreases, the demand for real money balances decreases at every given interest

rate. This results in a shift to the left in the demand curve.

Chapter 10 Monetary Policy and Aggregate Demand 103

8. a. The equilibrium interest rate is given by

6

PP

= → − = → =

9. The increase in aggregate output shifts the demand curve to the right, increasing the interest rate,

holding everything else constant. If the Federal Reserve decides to increase the money supply, then

the level of the new interest rate is indeterminate. Its new equilibrium level will depend on the

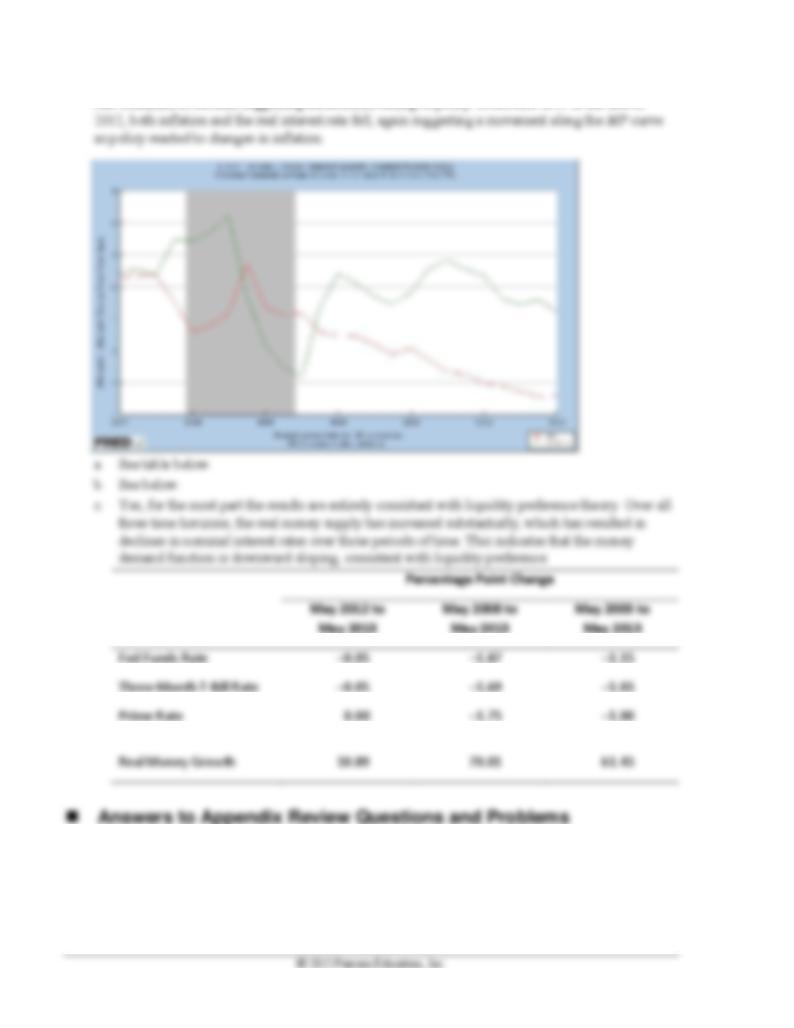

1. a. For the period of 2011:Q2 to 2012:Q1, average inflation was 2.34 percent, and the average real

interest rate was –0.68 percent. For 2012:Q2 to 2013:Q1, inflation averaged 1.21 percent, and the

real interest rate averaged –1.29 percent.

2. See graph on the next page. Periods of autonomous monetary policy change are characterized by a

decoupling of real rates and inflation rates. From the middle of 2007 to late 2008, inflation increased,

while the real interest rate fell, indicating an autonomous easing of policy. The period from late 2008

through mid-2009 was consistent with a move along the MP curve, where policy was reacting to

variation in inflation. From mid-2009 through mid-2011, inflation rose steadily, while the real interest

104 Mishkin • Macroeconomics: Policy and Practice, Second Edition

rate continued to decline, suggesting autonomous easing of policy. From mid-2011 to the end of

1. The three motives Keynes discussed were the transactions motive, the precautionary motive, and the

speculative motive. The transactions motive refers to people wishing to hold money because it is the

medium of exchange they need for their daily transactions. The precautionary motive refers to people

holding money so they will be able to take advantage of unexpected opportunities or handle unexpected

expenses as they arise. People’s speculative motive for holding money recognizes that money is a store

Chapter 10 Monetary Policy and Aggregate Demand 105

2. The four determinants of money demand identified in portfolio theory are wealth, expected return

3. Macroeconomic researchers use data on money supply (which in equilibrium equals money demand),

output, and interest rates to estimate the money demand function. Comparing the results of numerous

studies covering various time periods shows how consistent the relationships between money

demand, output, and interest rates are over time. Based on this approach, the money demand function

appeared to be stable until the early 1970s. After that time, the stable relationship between money

4. This technology would result in a decrease in the transactions component of the demand for money

and, therefore, in a decrease in the demand for money. This would allow individuals to hold smaller

5. The lack of the necessary infrastructure needed by some payment technologies (e.g., credit card

reading machines, reliable phone lines, reliable electricity supply) or its high cost determines that

6. If most people hold cash to insure themselves against unfortunate events, then the precautionary

7.

106 Mishkin • Macroeconomics: Policy and Practice, Second Edition

8.10

9. a. During a business cycle contraction, income decreases. As income and wealth are closely related,

wealth usually decreases as well. The decrease in wealth directly affects the demand for money,

10. High and volatile inflation rates decrease the relative real return of money, decreasing the demand for

money. As individuals observe a persistent increase in the price level, they tend to get rid of money

11. The portfolio theory approach to money demand predicts that the real return of holding money

sharply decreases during hyperinflations. During hyperinflations, the demand for money contracts so

much that sometimes other mediums of exchange are used to conduct trades. In some situations,

people have even resorted to barter to exchange goods and services. This of course results in a

decrease in economic efficiency, as many people spend a significant portion of their time designing

Chapter 10 Monetary Policy and Aggregate Demand 107

12. In the aftermath of a stock market crash, uncertainty about the performance of many firms increases,

and stock price volatility increases as well. The increase in stock price volatility increases the relative

safety of holding money. Thus, money demand should increase. However, shares of stock are a

significant portion of some individuals’ wealth. A stock market crash means that stock prices

decrease, negatively affecting the wealth of these individuals. As a consequence, the demand for

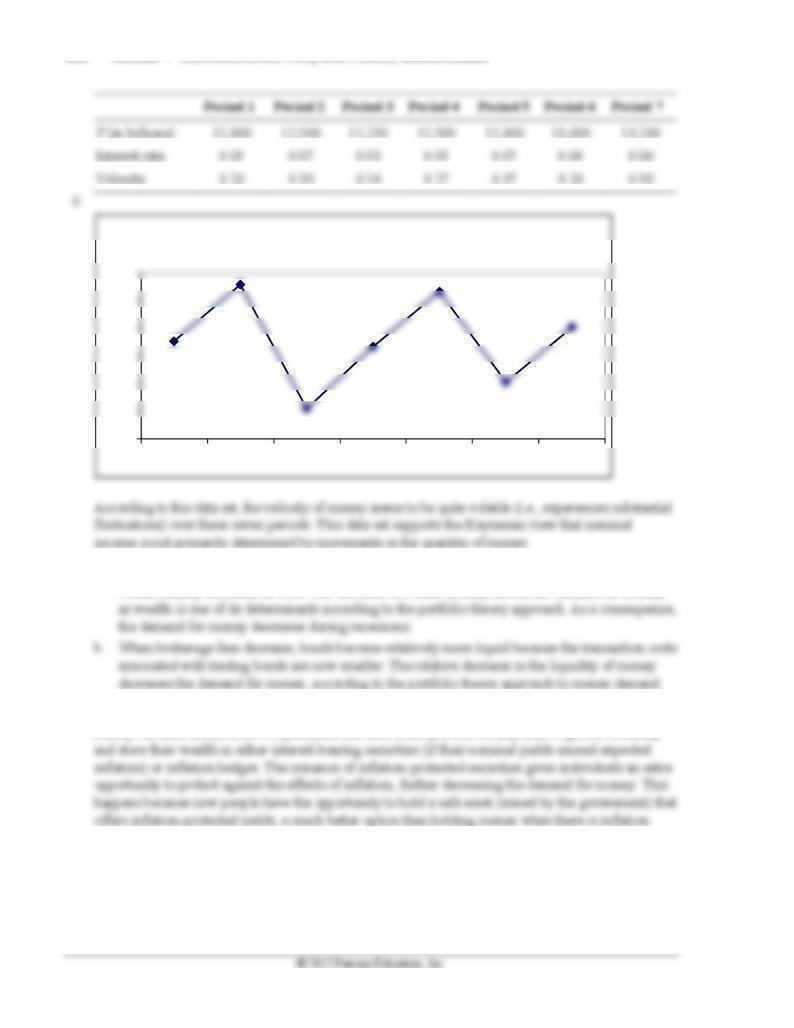

13. For this country, the evidence shows that velocity can be considered a constant, meaning that the

relationship between the money supply (as measured by M2) is closely related to aggregate spending

(nominal GDP). In this case it would be a good idea to focus the attention of monetary policy on a

monetary aggregate, as its growth rate would be a good indicator of the stance of monetary policy. A

risk associated with this strategy is that if the relationship between the monetary aggregate and

aggregate spending breaks down, monetary policy authorities would be focusing on the wrong

instrument to reach their monetary policy objectives.

◼ Data Sources, Related Articles, and Discussion Questions

A. For Information About Policy and Practice: Movements Along the MP

Curve: The Rise in the Federal Funds Rate Target, 2004–2006

Data Source

Federal Reserve Bank of St. Louis data base (FRED):

http://research.stlouisfed.org/fred2/series/FF?cid=118. Click on “Edit” and change the years to 2003–2007

to observe changes in the effective federal funds rate engineered by the Fed during this period.

Related Article

Federal Reserve System, “Press Release”:

http://www.federalreserve.gov/boarddocs/press/monetary/2004/20040630/default.htm. This is the FOMC

statement (June 2004) that declares the first rise in the federal funds rate target in the 2004–2006 period.

Discussion Question

In the second paragraph of the June 30, 2004, FOMC statement, the committee affirmed that it increased

the federal funds rate target partly due to the fact that “The evidence accumulated over the intermeeting

period indicates that output is continuing to expand at a solid pace and labor market conditions have

108 Mishkin • Macroeconomics: Policy and Practice, Second Edition

improved.” Explain why this should be interpreted as a movement along the MP curve and not as a shift in

the MP curve.

Answer; In this case, the FOMC quotes changes in economic conditions that are linked to future changes

in the inflation rate. Fears that the expansion of economic activity could lead to accelerating inflation lead

the FOMC to start a path of continual increases in the federal funds rate target. In order to interpret this

policy as a shift of the MP curve, the FOMC should have quoted a reason not related to inflationary

pressures in order to increase the federal funds rate target.

B. For Information About Policy and Practice: Shifts in the MP Curve:

Autonomous Monetary Easing at the Onset of the 2007–2009 Financial Crisis

Data Source

Federal Reserve Bank of St. Louis data base (FRED):

http://research.stlouisfed.org/fred2/series/FF?cid=118. Click on “Edit Graph” and change the years to

2007–2010 to see the decrease in the effective federal funds rate engineered by the Fed during this period.

Related Article

Federal Reserve System, “Press Release”:

http://www.federalreserve.gov/newsevents/press/monetary/20070918a.htm. Here you can find the Fed’s

statement about the first change to the federal funds rate target and discount rate engineered during the

2007–2009 period.

Discussion Question

In the second paragraph of the January 22, 2008, FOMC statement, the committee affirmed that it lowered

the federal funds rate target “… to help forestall some of the adverse effects on the broader economy that

might otherwise arise from the disruptions in financial markets and to promote moderate growth over

time.” Explain how this argument should be interpreted as a shift in the MP curve and not as a movement

along the MP curve.