Chapter 03 - The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential

CHAPTER 3

THE REPORTING ENTITY AND CONSOLIDATION OF LESS-THAN-WHOLLY-OWNED

SUBSIDIARIES WITH NO DIFFERENTIAL

ANSWERS TO QUESTIONS

Q3-2 Without consolidated statements it is often very difficult for an investor to gain an

Q3-3 Parent company shareholders are likely to find consolidated statements more useful.

Q3-5 Creditors of the parent company have primary claim to the assets held directly by the

parent. Short-term creditors of the parent are likely to look only at those assets. Because the

Q3-7 The primary criterion for consolidation is the ability to directly or indirectly exercise

control. Control normally has been based on ownership of a majority of the voting common

Chapter 03 - The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential

Q3-8 Consolidation is not appropriate when control is temporary or when the parent cannot

Q3-10 Special-purpose entities are corporations, trusts, or partnerships created for a single

Q3-11 Variable interest entities normally are not involved in general business activities such as

Q3-14 It is possible for a company to exercise control over another company without holding a

majority of the voting common stock. Contractual agreements, for example, may provide a

Q3-15 Subsidiary shares held by the parent are not owned by an outside party and therefore

cannot be reported as shares outstanding. Those held by the noncontrolling shareholders are

Chapter 03 - The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential

Q3-18 The procedures used in preparing consolidated and combined financial statements may

be virtually identical. In general, consolidated statements are prepared when a parent company

either directly or indirectly controls one or more subsidiaries. Combined financial statements are

Chapter 03 - The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential

C3-1 Computation of Total Asset Values

(2) Product lines or other segments of an enterprise, such as a division, department, profit

(4) Although the accounting entity often is defined in terms of a business enterprise that is

(5) The entire economy of the United States also can be viewed as an accounting entity.

Chapter 03 - The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential

C3-3 Joint Venture Investment

a. ASC 810 is the primary authoritative literature dealing with the types of ownership issues

arising in this situation. Under normal circumstances, the company holding majority ownership

in another entity is expected to consolidate that entity in preparing its financial statements. Thus,

unless other circumstances dictate, Dell should have planned to consolidate DFS as a result of

its 70 percent equity ownership. While ASC 810 is highly complex and greater detail of the

ownership agreement may be needed to decide this matter, the literature appears to permit

equity holders to avoid consolidating an entity if the equity holders (1) do not have the ability to

make decisions about the entity’s activities, (2) are not obligated to absorb the expected losses

of the entity if they occur, or (3) do not have the right to receive the expected residual returns of

the entity if they occur [ASC 810-10-15-14].

It does appear that Dell and CIT Group do, in fact, have the ability to make operating and other

Chapter 03 - The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential

C3-4 What Company is That?

Information for answering this case can be obtained from the SEC's EDGAR database

(www.sec.gov) and from the home pages for Viacom (www.viacom.com), ConAgra

(www.conagra.com), and Yum! Brands (www.yum.com).

a.. Viacom is well known for ownership of companies in the entertainment industry. On January

Chapter 03 - The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential

C3-5 Subsidiaries and Core Businesses

Most of the information needed to answer this case can be obtained from articles available in

libraries, on the Internet, or through various online databases. Some of the information is

available in filings with the SEC (www.sec.gov).

a. General Electric was never able to turn Kidder, Peabody into a profitable subsidiary. In fact,

Kidder became such a drain on the resources of General Electric, that GE decided to get rid of

Kidder. Unfortunately, GE was unable to sell the company as a whole and ultimately broke the

company into pieces and sold the pieces that it could. GE suffered large losses from its venture

into the brokerage business.

b. Sears, Roebuck and Co. has been a major retailer for many decades. For a while, Sears

attempted to provide virtually all consumer needs so that customers could purchase financial

and related services at Sears in addition to goods. It owned more than 200 other companies.

During that time, Sears sold insurance (Allstate Insurance Group, consisting of many

subsidiaries), real estate (Coldwell Banker Real Estate Group, consisting of many subsidiaries),

brokerage and investment advisor services (Dean Witter), credit cards (Sears and Discover

Card), and various other related services through many different subsidiaries. During the mid-

nineties, Sears sold or spun off most of its subsidiaries that were unrelated to its core business,

including Allstate, Coldwell Banker, Dean Witter, and Discover. On March 24, 2005, Sears

Holding Corporation was established and became the parent company for Sears, Roebuck and

Co. and K Mart Holding Corporation. From an accounting perspective, Kmart acquired Sears,

even though Kmart had just emerged from bankruptcy proceedings. Following the merger the

company now has approximately 2,350 full-line and off-mall stores and 1,100 specialty retail

stores in the United States, and approximately 370 full-line and specialty retail stores in Canada.

Chapter 03 - The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential

C3-6 International Consolidation Issues

The following answers are based on information from the Financial Accounting Standards Board

website at www.fasb.org, the International Accounting Standards Board website at

www.iasb.org, and from the PricewaterhouseCoopers publication entitled IFRS and US GAAP:

similarities and differences, available online at http://www.pwc.com/us/en/issues/ifrs-

reporting/publications/ifrs-and-us-gaap-similarities-and-differences.jhtml.

a. Consolidation under IFRS is required when an entity is able to govern the policies of another

entity in order to obtain benefits. To determine if consolidation is necessary, IFRS focuses on

the concept of control. Factors of control, such as voting rights and contractual rights, are given

by international standards. If control is not apparent, a general assessment of the relationship is

required, including an evaluation of the allocation of risks and benefits.

b. Under IFRS, Goodwill is reviewed annually (or more frequently) for impairment. Goodwill is

initially allocated at the organizational level where cash flows can be clearly identified. These

cash generating units (CGUs) may be combined for purposes of allocating goodwill and for the

Chapter 03 - The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential

(3) A company may create a new VIE and transfer assets to the new entity in exchange for

cash (generally borrowed by the VIE).

c. VIEs may serve a genuine business purpose, such as risk sharing among investors and

isolation of project risk from company risk.

C3-8 Consolidation Differences among Major Corporations

a. Union Pacific is rather unusual for a large company. It has only two subsidiaries:

Union Pacific Railroad Company

Southern Pacific Rail Corporation

b. ExxonMobil does not consolidate majority owned subsidiaries if the minority shareholders

Chapter 03 - The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential

1. d – Consolidated financial statements are intended to provide a meaningful representation of

the overall position and activities of a single economic entity comprising a number of

2. c – Under certain circumstances, a company can lose the ability to exercise control of a

subsidiary even when a controlling interest is held. For example, if the subsidiary were

under a legal reorganization or bankruptcy. As long as control cannot be exercised,

3. b – The consolidation method is typically used when ownership is greater than 50% of the

common stock of the subsidiary. Penn directly controls Sell and indirectly controls Vane,

thus, Sell and Vane should both be consolidated.

(a) Incorrect. Because Sell owns greater than 50% Vane’s common stock, Vane would be

4. b – The companies are each separate legal entities, but in substance they are one economic

entity

(a) Incorrect. The companies are not one in form, each company is a separate legal

Chapter 03 - The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential

1. c – SPE’s are typically financed primarily by debt, while equity financing is only a small

3. a – A primary beneficiary is defined as an enterprise that will absorb the majority of the VIE’s

expected losses, receive a majority of the VIE’s expected residual returns, or both.

4. b – The company that has the most at stake is typically required to consolidate the VIE. This

has been defined as the entity receiving a majority of the VIE’s profits, and/or absorbing

2. b – The consolidated balance in common stock is always equal to the parent’s common

stock and the common stock of the subsidiary is eliminated.

Chapter 03 - The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential

3. a – Neely directly controls Randle, and indirectly controls Walker as a result of owning 40%

plus an additional 30% as a result of Randle’s ownership of Walker, thus Neely should

1. d – Consolidation occurs when one company acquires a controlling interest in another

company. This controlling interest is typically defined has owning greater than 50% of the

company.

(a) Incorrect. The equity method alone does not require consolidation until greater than

2. a – The consolidated net earnings contains the net earnings of Aaron as well as the net

earnings of Belle. Thus, the consolidated net earnings are greater than just Aaron’s own

3. b – When the acquisition takes place, X Company only includes the earnings of Y Company

for the portion of the year in which a controlling ownership was held.

(a) Incorrect. Earnings of X Company for the entire year would be included in

consolidated net income.

4. d – Consolidation typically occurs when greater than 50% of the voting stock is obtained

because the parent company is said to have control over the subsidiary.

(a) Incorrect. Consolidation is required when over 50% is obtained. Additionally, the cost

E3-5 Balance Sheet Consolidation

a. $470,000 = $470,000 - $44,000 (cash outlay) + $44,000 (investment)

b. $616,000 = ($470,000 - $44,000 (investment) + $190,000

c. $405,000 = $270,000 + $135,000

d. $211,000

Chapter 03 - The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential

E3-6 Balance Sheet Consolidation with Intercompany Transfer

a. $631,500 = $510,000 + $121,500 (investment)

b. $860,000 = $510,000 + $350,000

c. $656,500 = ($320,000 + $121,500) + $215,000

d. $203,500

Chapter 03 - The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential

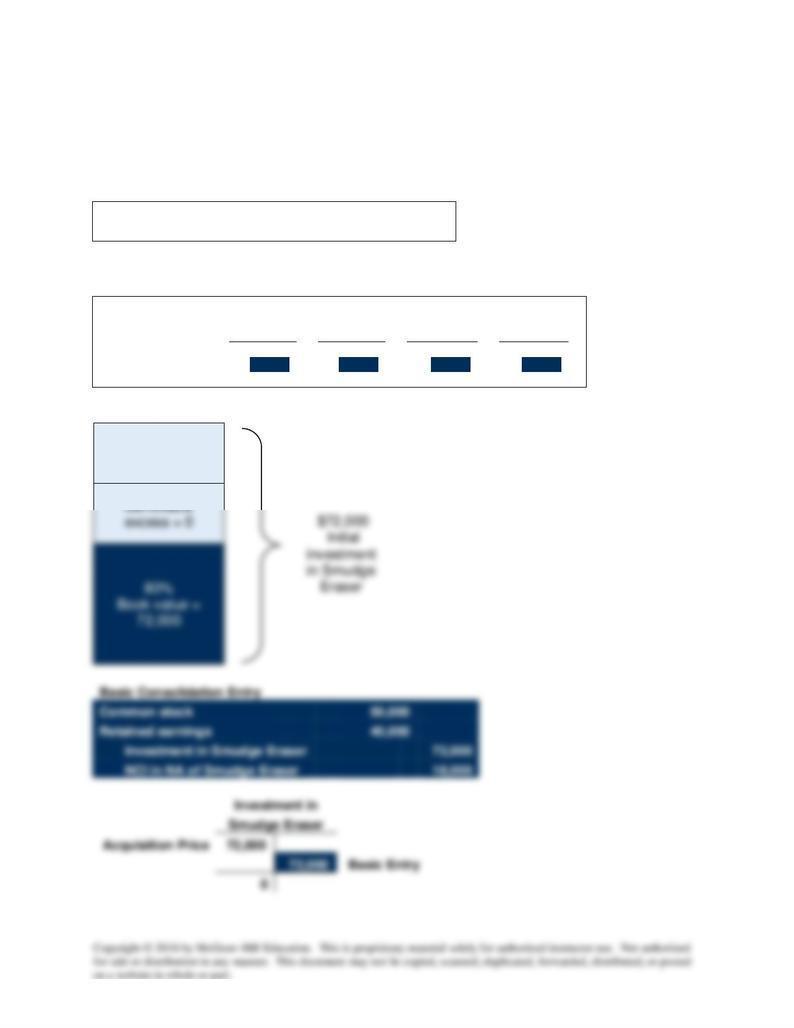

E3-7 Subsidiary Acquired for Cash

Note: Since the financial statements of these two companies are quite simple, it is possible to

prepare the consolidated balance sheet without completing all of the steps for a consolidation.

However, we present the formal calculations without skipping any steps.

Equity Method Entries on Fineline Pencil's Books:

Investment in Smudge Eraser

72,000

Cash

72,000

Record the initial investment in Smudge Eraser

Book Value Calculations:

NCI

20%

+

Fineline

Pencil

80%

=

Common

Stock

+

Retained

Earnings

Book value at

acquisition

18,000

72,000

50,000

40,000

1/1/X3

Goodwill = 0

Chapter 03 - The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential

E3-7 (continued)

Fineline

Pencil

Smudge

Eraser

Consolidation

Entries

DR

CR

Consolidated

Balance Sheet

Cash

128,000

50,000

178,000

Other Assets

400,000

120,000

520,000

Investment in Smudge Eraser

72,000

72,000

0

Total Assets

600,000

170,000

0

72,000

698,000

Current Liabilities

100,000

80,000

180,000

Common Stock

300,000

50,000

50,000

300,000

Retained Earnings

200,000

40,000

40,000

200,000

Chapter 03 - The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential

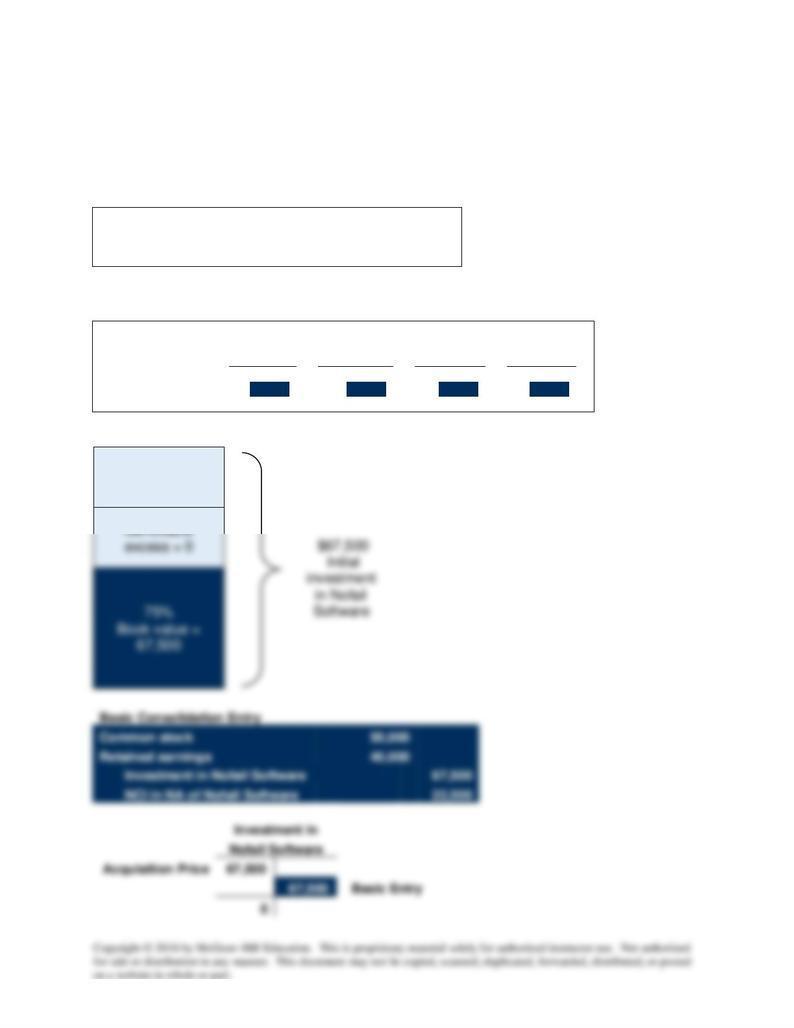

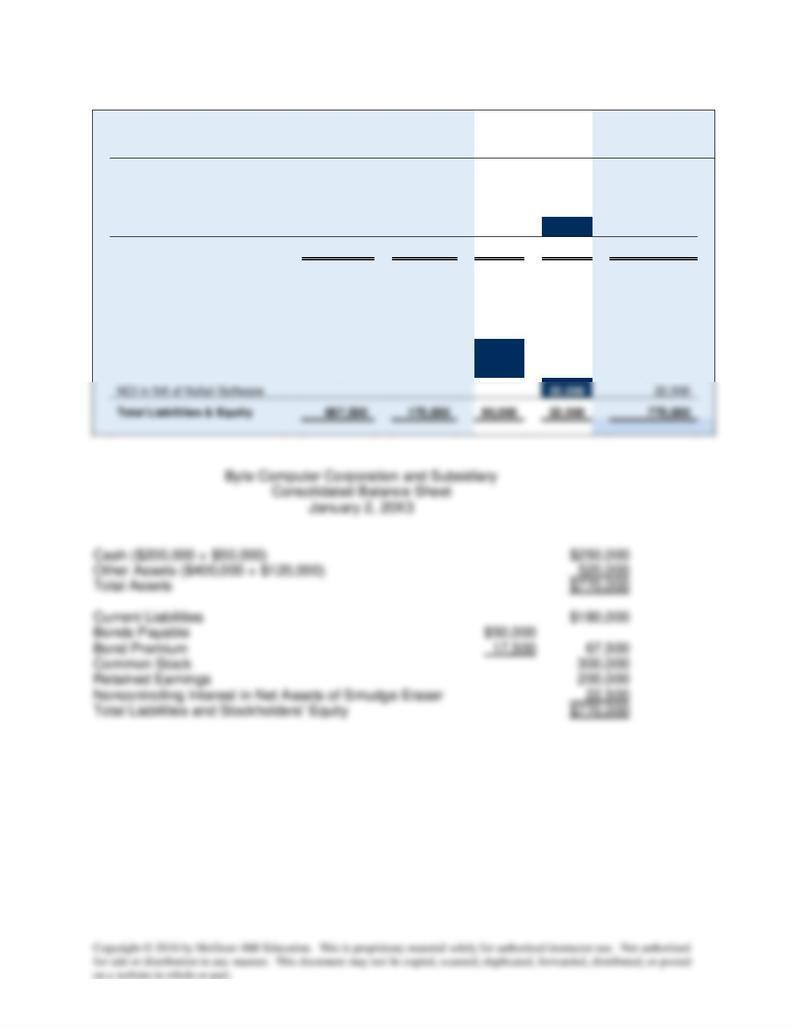

E3-8 Subsidiary Acquired with Bonds

Note: Since the financial statements of these two companies are quite simple, it is possible to

prepare the consolidated balance sheet without completing all of the steps for a consolidation.

However, we present the formal calculations without skipping any steps.

Equity Method Entries on Byte Computer's Books:

Investment in Nofail Software

67,500

Bonds Payable

50,000

Premium on Bonds Pay

17,500

Record the initial investment in Nofail Software

Book Value Calculations:

NCI

25%

+

Byte

Computer

75%

=

Common

Stock

+

Retained

Earnings

Book value at

acquisition

22,500

67,500

50,000

40,000

1/1/X3

Goodwill = 0

Chapter 03 - The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential

E3-8 (continued)

Byte

Computer

Nofail

Software

Consolidation

Entries

DR

CR

Consolidated

Balance Sheet

Cash

200,000

50,000

250,000

Other Assets

400,000

120,000

520,000

Investment in Nofail Software

67,500

67,500

0

Total Assets

667,500

170,000

0

67,500

770,000

Current Liabilities

100,000

80,000

180,000

Bonds Payable

50,000

50,000

Bond Premium

17,500

17,500

Common Stock

300,000

50,000

50,000

300,000

Retained Earnings

200,000

40,000

40,000

200,000

Chapter 03 - The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential

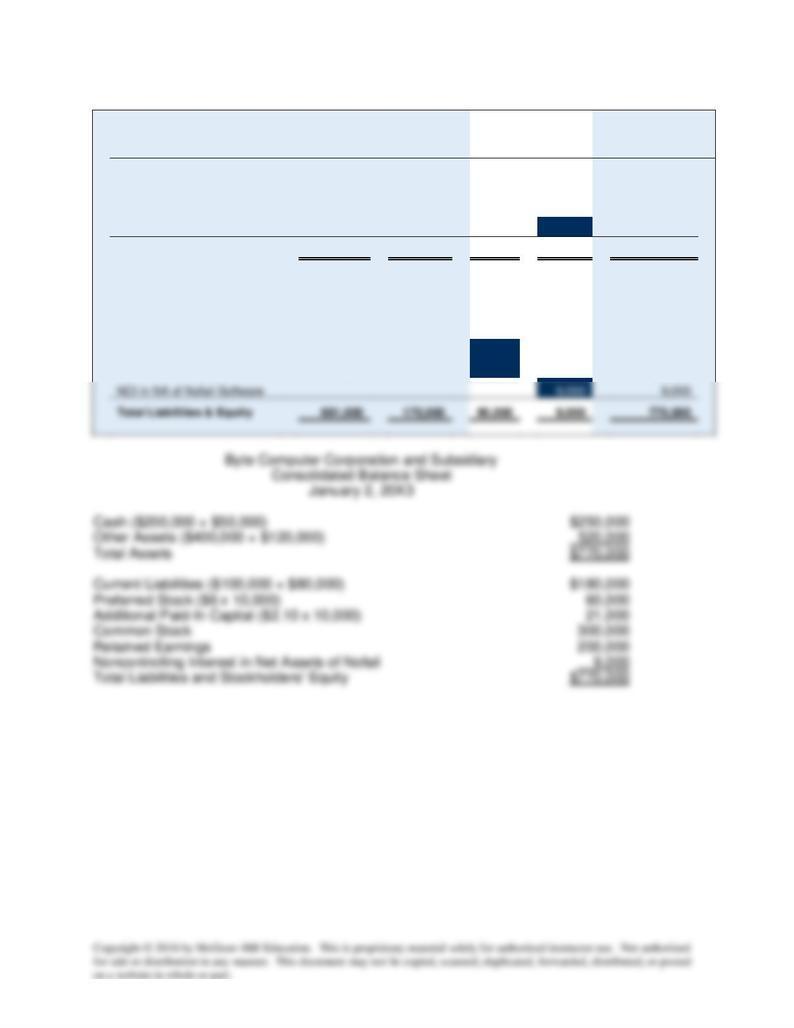

E3-9 Subsidiary Acquired by Issuing Preferred Stock

Note: Since the financial statements of these two companies are quite simple, it is possible to

prepare the consolidated balance sheet without completing all of the steps for a consolidation.

However, we present the formal calculations without skipping any steps.

Equity Method Entries on Byte Computer's Books:

Investment in Nofail Software

81,000

Preferred Stock

60,000

Additional Paid-In Capital – Pref. Stock

21,000

Record the initial investment in Nofail Software

Book Value Calculations:

NCI

10%

+

Byte

Computer

90%

=

Common

Stock

+

Retained

Earnings

Book value at

acquisition

9,000

81,000

50,000

40,000

1/1/X3

Goodwill = 0

Chapter 03 - The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential

E3-9 (continued)

Byte

Computer

Nofail

Software

Consolidation

Entries

DR

CR

Consolidated

Balance Sheet

Cash

200,000

50,000

250,000

Other Assets

400,000

120,000

520,000

Investment in Nofail Software

81,000

81,000

0

Total Assets

681,000

170,000

0

81,000

770,000

Current Liabilities

100,000

80,000

180,000

Preferred Stock

60,000

60,000

Additional Paid-In Capital

21,000

21,000

Common Stock

300,000

50,000

50,000

300,000

Retained Earnings

200,000

40,000

40,000

200,000

Chapter 03 - The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential

E3-10 Reporting for a Variable Interest Entity

Gamble Company

Consolidated Balance Sheet

Cash

$ 18,600,000(a)

Buildings and Equipment

$370,600,000(b)

Less: Accumulated Depreciation

(10,100,000)

360,500,000

Total Assets

$379,100,000

E3-11 Consolidation of a Variable Interest Entity

Teal Corporation

Consolidated Balance Sheet

Total Assets

$682,500(a)

E3-12 Computation of Subsidiary Net Income

Chapter 03 - The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential

E3-13 Incomplete Consolidation

a. Belchfire apparently owns 100 percent of the stock of Premium Body Shop since the

balance in the investment account reported by Belchfire is equal to the net book value of

Premium Body Shop.

b.

Accounts Payable

$ 60,000

Accounts receivable were reduced by

E3-14 Noncontrolling Interest

a. The total noncontrolling interest reported in the consolidated balance sheet at January 1,

20X7, is $126,000 ($420,000 x .30).

b. The stockholders' equity section of the consolidated balance sheet includes the claim of the

noncontrolling interest and the stockholders' equity section of the subsidiary is eliminated

when the consolidated balance sheet is prepared:

Controlling Interest:

Chapter 03 - The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential

E3-15 Computation of Consolidated Net Income

a. Ambrose should report income from its subsidiary of $15,000 ($20,000 x .75) rather than

dividend income of $9,000.

b. A total of $5,000 ($20,000 x 0.25) should be assigned to the noncontrolling interest in the

20X4 consolidated income statement.

c. Consolidated net income of $70,0000 should be reported for 20X4, computed as follows:

E3-16 Computation of Subsidiary Balances

a. Light's net income for 20X2 was $32,000 ($8,000 / 0.25).

(1) Computation of common stock outstanding:

Chapter 03 - The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential

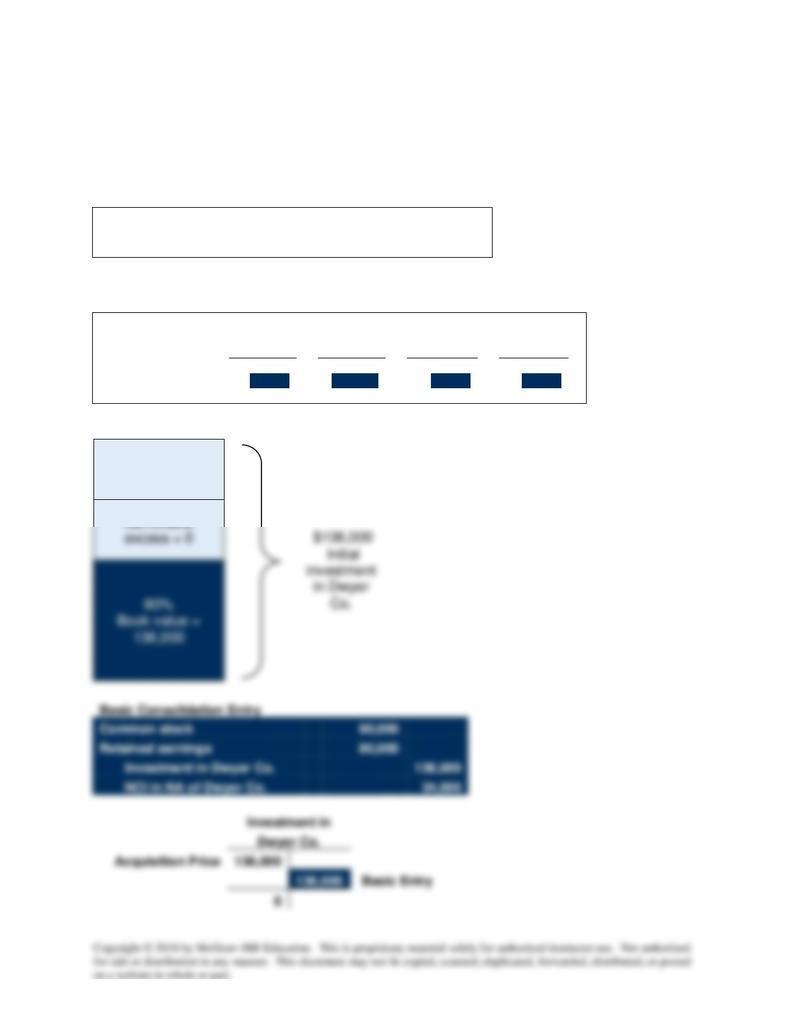

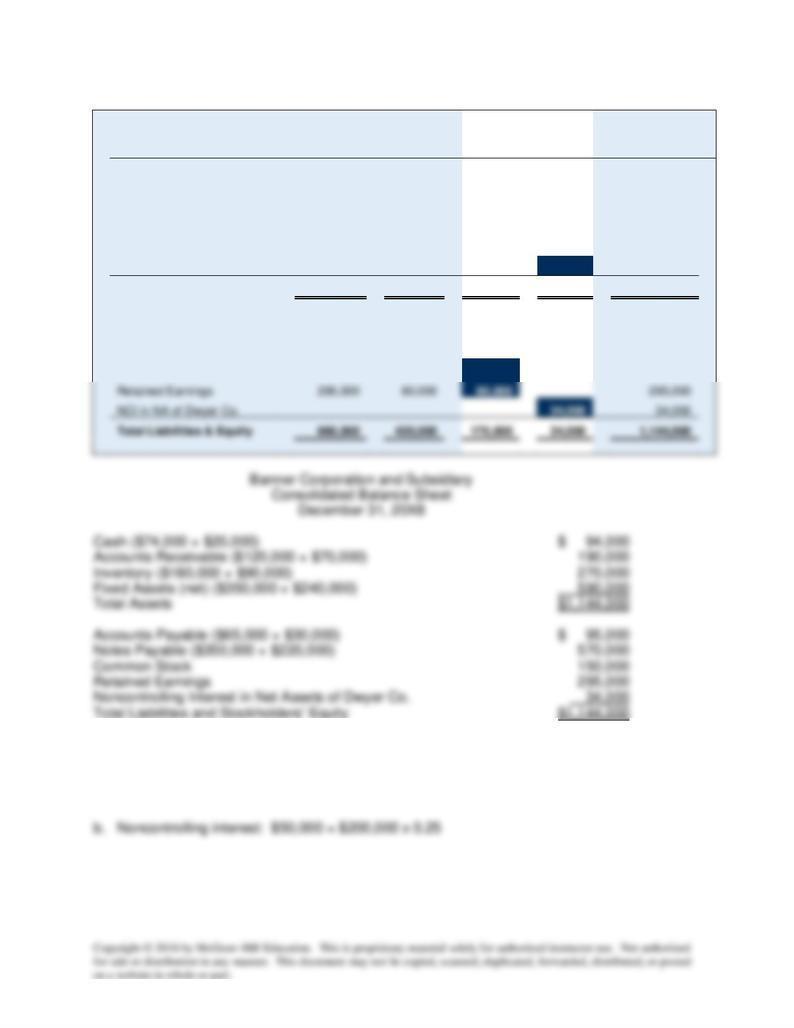

E3-17 Subsidiary Acquired at Net Book Value

Note: Since the financial statements of these two companies are quite simple, it is possible to

prepare the consolidated balance sheet without completing all of the steps for a consolidation.

However, we present the formal calculations without skipping any steps.

Equity Method Entries on Banner Corp.'s Books:

Investment in Dwyer Co.

136,000

Cash

136,000

Record the initial investment in Dwyer Co.

Book Value Calculations:

NCI

20%

+

Banner

Corp.

80%

=

Common

Stock

+

Retained

Earnings

Book value at

acquisition

34,000

136,000

90,000

80,000

1/1/X8

Goodwill = 0

Chapter 03 - The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential

E3-17 (continued)

Banner

Corp.

Dwyer

Co.

Consolidation

Entries

DR

CR

Consolidated

Balance Sheet

Cash

74,000

20,000

94,000

Accounts Receivable

120,000

70,000

190,000

Inventory

180,000

90,000

270,000

Fixed Assets (net)

350,000

240,000

590,000

Investment in Dwyer Co.

136,000

136,000

0

Total Assets

860,000

420,000

0

136,000

1,144,000

Accounts Payable

65,000

30,000

95,000

Notes Payable

350,000

220,000

570,000

Common Stock

150,000

90,000

90,000

150,000

E3-18 Acquisition of Majority Ownership

a. Net identifiable assets: $720,000 = $520,000 + $200,000

Chapter 03 - The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential

1. d – While previously reported in the ‘mezzanine’ area between liabilities and equity, FASB

2. c – Similar to consolidated statements, combined financial statements require the removal of

all intercompany loans and profits. Thus, neither amount is recorded in the combined

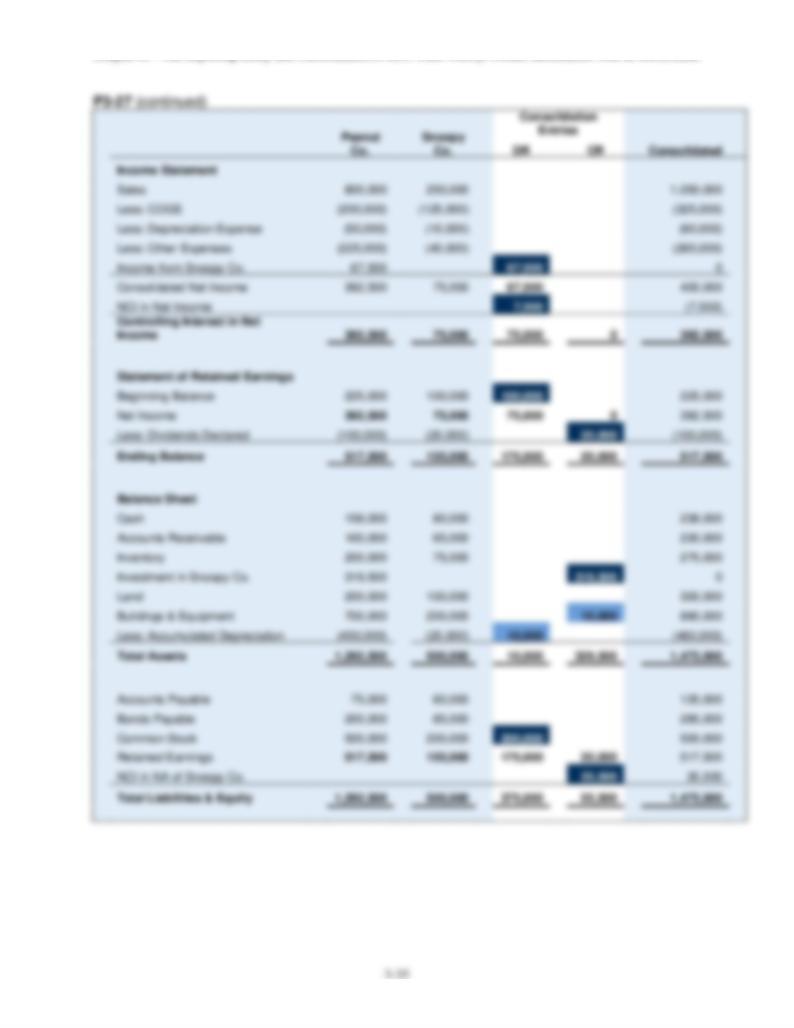

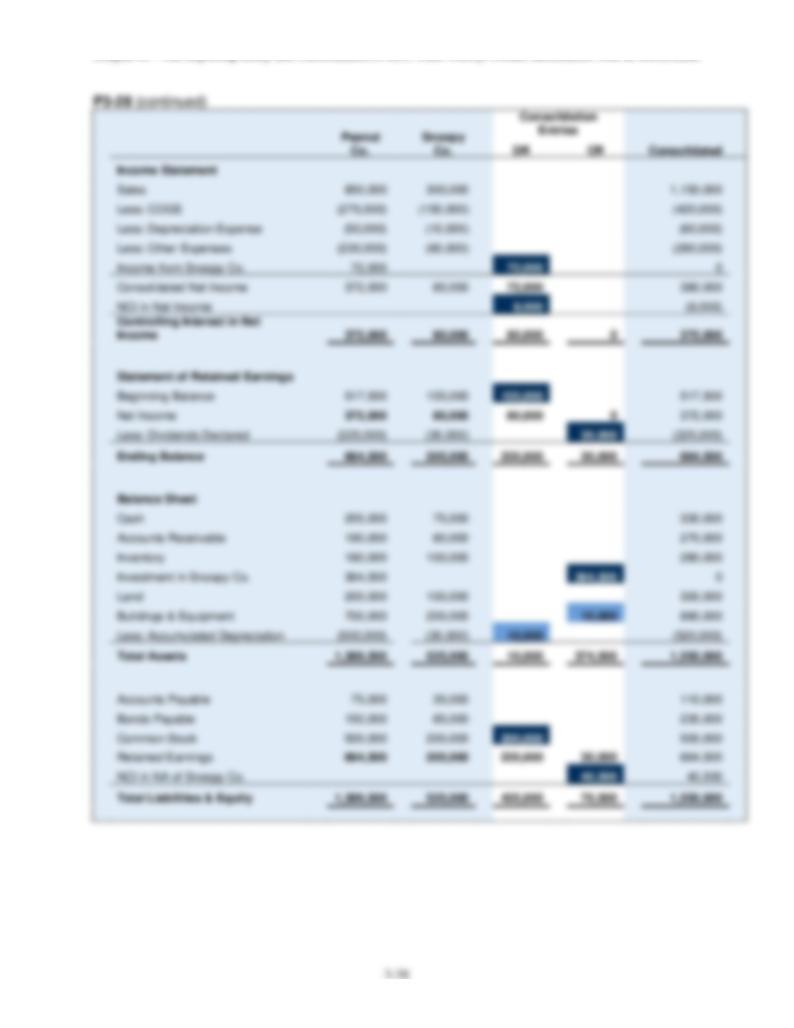

P3-20 Determining Net Income of Parent Company

P3-21 Consolidation of a Variable Interest Entity

Stern Corporation

Consolidated Balance Sheet

January 1, 20X4

Cash

$ 8,150,000

(a)

Accounts Receivable

$12,200,000

(b)

Less: Allowance for Uncollectibles

(610,000)

(c)

11,590,000

Other Assets

5,400,000

Total Assets

$25,140,000

Accounts Payable

$ 950,000

Chapter 03 - The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential

P3-22 Reporting for Variable Interest Entities

Purified Oil Company

Consolidated Balance Sheet

Cash

$ 640,000

Drilling Supplies

420,000

Accounts Receivable

640,000

Equipment (net)

8,500,000

P3-23 Parent Company and Consolidated Amounts

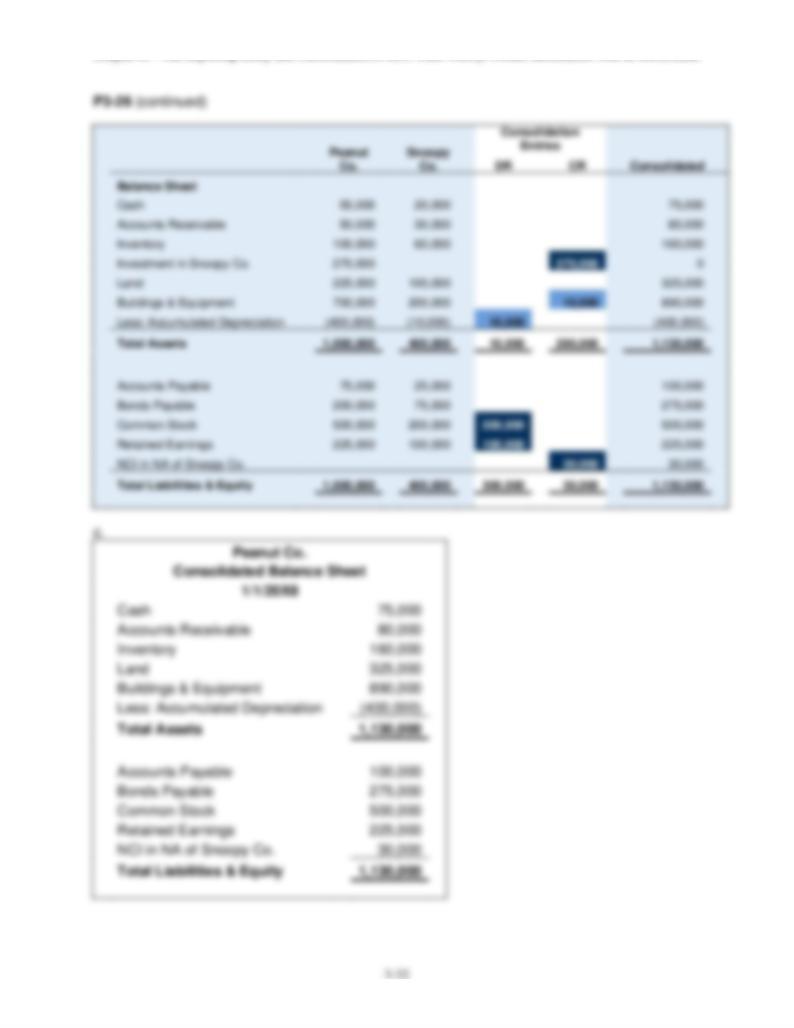

a.

Common stock of Tempro Company

on December 31, 20X5

$ 90,000

Proportion of stock acquired by Quoton

x 0.80

Purchase price

$192,000

Chapter 03 - The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential

noncontrolling interest

x 0.20

Balance assigned to noncontrolling interest

$ 48,000

P3-24 Parent Company and Consolidated Balances

Proportion of stock held by True Corporation

x 0.75

Total Amount Debited to Investment Account

(48,000)

Purchase Amount

$211,800

b. $282,400 ($211,800 / 0.75) is the fair value of net assets on January 1, 20X5

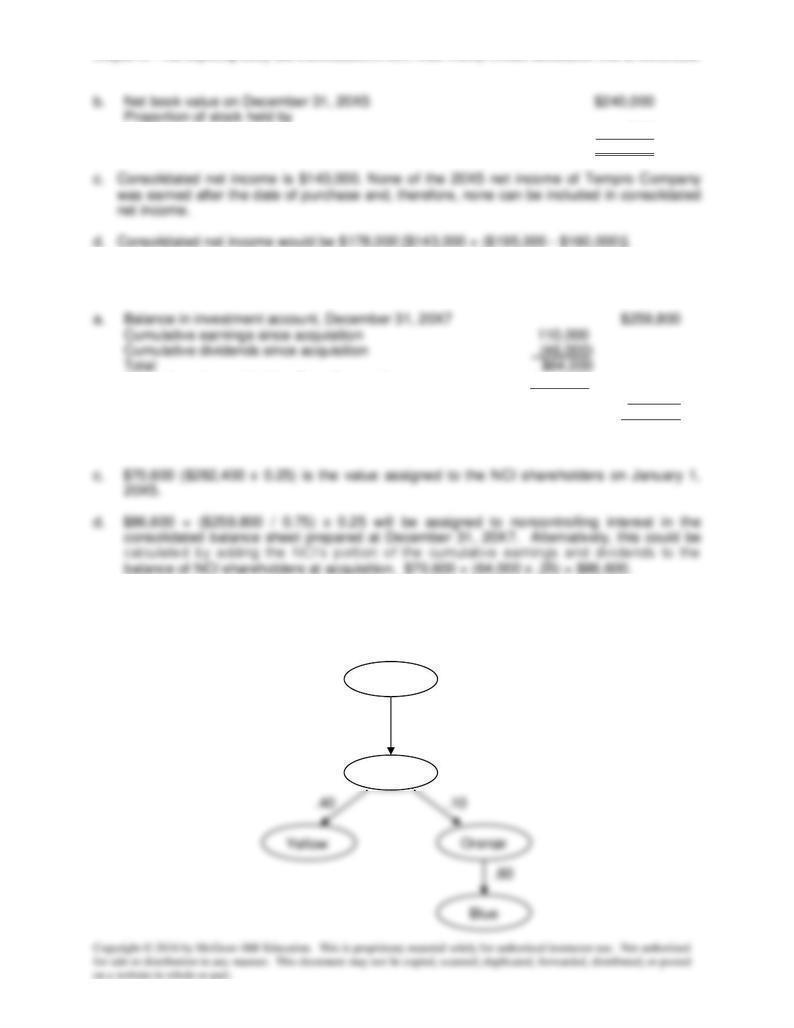

P3-25 Indirect Ownership

The following ownership chain exists:

Purple

.70

Green

Chapter 03 - The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential

P3-25 (continued)

The earnings of Blue Company and Orange Corporation are included under cost method

reporting due to the 10 percent ownership level of Orange Corporation. The earnings of Yellow

Corporation are included under equity method accounting due to the 40 percent ownership

level.

Net income of Green Company:

Reported operating income

$ 20,000

Dividend income from Orange ($30,000 x 0.10)

3,000

Chapter 03 - The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential

Chapter 03 - The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential

Chapter 03 - The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential

Chapter 03 - The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential

Chapter 03 - The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential

Chapter 03 - The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential

Chapter 03 - The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential

Chapter 03 - The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential

Chapter 03 - The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential

Chapter 03 - The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential

Chapter 03 - The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential

Chapter 03 - The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential

Chapter 03 - The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential

Chapter 03 - The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential

Chapter 03 - The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential

Chapter 03 - The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries with no Differential